AEIS - Advanced Energy Industries: Near-Term Headwinds And Fair Valuation

2024-01-16 18:29:58 ET

Summary

- Challenging macro will likely continue to act as a headwind to the company's revenue.

- Margin will likely contract in the near term due to volume deleverage.

- Premium valuation and negative near-term prospects keep me on the sidelines.

Editor's note: Seeking Alpha is proud to welcome ResearchWise as a new contributor. It's easy to become a Seeking Alpha contributor and earn money for your best investment ideas. Active contributors also get free access to SA Premium. Click here to find out more »

Investment Thesis

Advanced Energy Industries, Inc. ( AEIS ) should continue to face headwinds in the near term as the challenges related to the macroeconomic environment continue. I believe the company stock should be under pressure as the margins are also expected to be hit due to volume deleverage in the near term. The market is also anticipating a decline of 26.25% in the company's EPS for the full year 2023 to $4.79.

However, the long term looks good for the company due to its broad product portfolio and diversified market base, which should benefit the company once the economy starts to recover. However, despite positive long-term, near near-term headwinds and a slight premium valuation of AEIS stock as compared to its historical levels keeps me on the sideline for now. Hence, I am neutral on this stock.

Brief Overview of AEIS

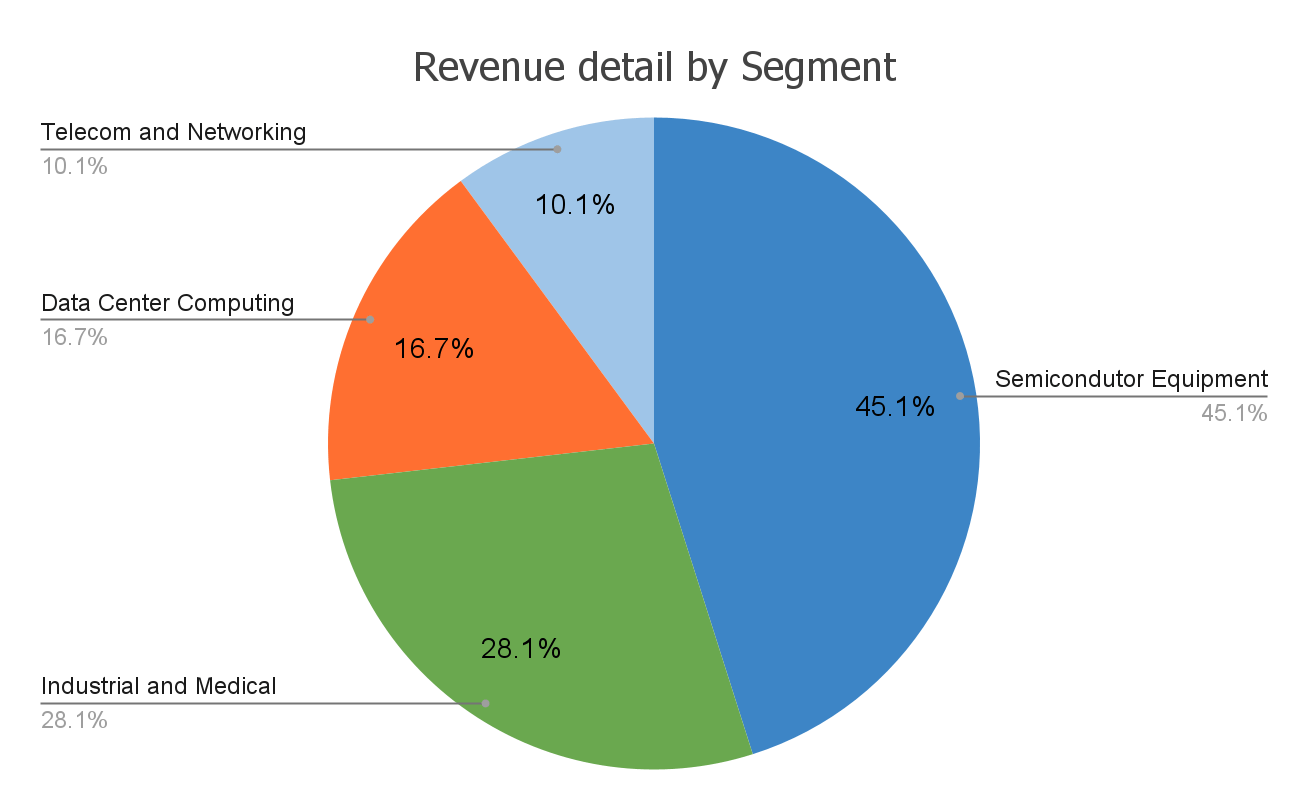

AEIS is a global company that provides highly engineered, mission-critical, precision power conversion, measurement, and control solutions to its customers worldwide. The company operates through four segments: Semiconductor Market, Industrial and Medical, Data Center Computing, and Telecom and Networking.

AEIS's largest segment, the Semiconductor Market, comprises 45% of Q3 2023 revenue, driven by the increasing demand for semiconductor production capacity and new process technologies. In the Industrial and Medical segment, AEIS serves with mission-critical power components, prioritizing reliability and precision. The Data Center Computing segment delivers top-notch power conversion products to data center OEMs, ODMs, and cloud service providers. Despite its smaller 10% contribution, the Telecom and Networking segment strategically targets key vendors to capitalize on substantial growth opportunities emerging from the ongoing 5G evolution.

Revenue share by segments (Research wise)

{kind=link}

Last Quarter Performance

After strong double-digit growth in 2022, the company's revenue growth continued to deteriorate in 2023 as the company experienced softening demand across all the segments due to challenging macroeconomic factors, with, two segments, the Semiconductor Equipment segment and the Data Center Computing segment being the worst impacted with Y/Y decline of 30.6% and 22% respectively. Both these segments collectively account for about 60-65% of the total revenue, which resulted in an overall revenue decline of 20.6% to $410 million in the third quarter of 2023.

AEIS Historical revenue (Research wise) Segment wise revenue (Company presentation)

The company's operating margin on the other hand contracted 570bps as compared to the prior year quarter to 12.4% in the third quarter of 2023. This contraction was primarily due to volume deleverage followed by a challenging demand environment, which more than offset the benefit from the improved mix and lower material cost.

Furthermore, the company's adjusted EPS was $1.28 in the third quarter, which is at the higher end of the guidance of $1.3 by the company. However, the margins have also impacted the bottom line which more than offset the benefit related to tax strategies that the company implemented this quarter to lower its tax rate, resulting in a 39.6% decline from $2.12 in the prior year quarter.

AEIS consolidated operating margin (Research wise)

Headwinds to continue in the near term

AEIS has been experiencing a significant amount of headwinds due to demand softness, which I believe should continue further in the coming quarter due to continued challenging macroeconomic conditions. Looking ahead, in 2024, the company is expecting its semiconductor revenue to be flat, however, I believe the ongoing inventory digestion should negatively impact the company's overall business as the last time the company had to deal with inventory digestion, it took them more than 3 quarters to get through it. The Data Center Computing segment revenue should also be under pressure due to the cyclical downturn in the enterprise server further impacting the revenue growth.

The Telecom and Networking segment is also expected to face challenges, primarily due to the ongoing normalization in segment revenue toward $30 million. This, coupled with demand softness, is expected to negatively impact the segment in the near term. On the flip side, the Industrial and Medical segment appears comparatively stronger. The company foresees some incremental revenue in the upcoming quarters from previous design wins in this segment, which is anticipated to partially offset the adverse effects of the sluggish macroeconomic conditions across the entire business in the near term.

The company Backlog is also expected to come down to settle around $400-$500 million by the year-end, mainly due to improved lead time. And, as a result of the improved lead times, customers might find it more convenient to place orders closer to the time they need the products, rather than ordering in advance for out-quarter deliveries. The improved lead times should result in faster backlog conversion in the near term further helping the company in offsetting the negative impact from lower volumes in the coming quarters.

AEIS revenue and Backlog graph (Company presentation)

Similar to the top-line performance, I anticipate that the company's margin will face challenges in the near term. This is primarily attributed to volume deleverage across all business segments, compounded by a challenging macroeconomic environment. Despite the company's proactive measures, including a mix shift, restructuring, and efforts to enhance operational efficiencies through consolidating production into a highly efficient factory for economies of scale, the anticipated volume impact is expected to outweigh these benefits in the short term. Consequently, an overall decline in margins is foreseen in the coming quarters.

Long-term opportunity

While the short-term outlook for the company appears negative, there is a positive long-term perspective as the company remains committed to developing new products and technologies. This commitment has the potential to drive significant revenue growth in the years ahead.

Progress on the new product front has been substantial, with the launch of 19 products across various markets. Furthermore, the company is expanding its quick-turn customization activity, allowing AEIS to promptly tailor its new products to meet the specific needs of its customers. This adaptability is expected to contribute to the company's revenue growth in the coming years.

Additionally, the company is actively collaborating with key customers to design next-generation platforms such as eVerest and eVos . These platforms are anticipated to assist AEIS customers in addressing the technical challenges of sub-2 nanometer processes more effectively. The company has already secured numerous orders for these platforms, and their implementation in the upcoming quarter is poised to positively impact the company's revenue.

Moreover, the company is currently observing robust momentum in design wins across a range of high-value applications within its targeted markets. Anticipating a record number of design wins in the upcoming quarters, this trend is establishing a strong foundation for future growth. The successful design wins span various sectors, including Robotics, Factory Automation, Diagnostics and Therapeutic applications, Thin-film manufacturing applications, and others throughout the business.

In addition to its focus on design wins, the company is actively exploring merger and acquisition (M&A) opportunities. In my opinion, the company's solid financial position is expected to persist, providing ongoing support for strategic M&A initiatives in the years to come.

Overall, I am optimistic about AEIS's prospects in the coming years as the economy begins to recover. This optimism stems from its diverse portfolio of highly differentiated products catering to a broad market. The company's strength in its design win pipeline and potential benefits from future mergers and acquisitions are poised to be key drivers for its long-term revenue growth.

Valuation

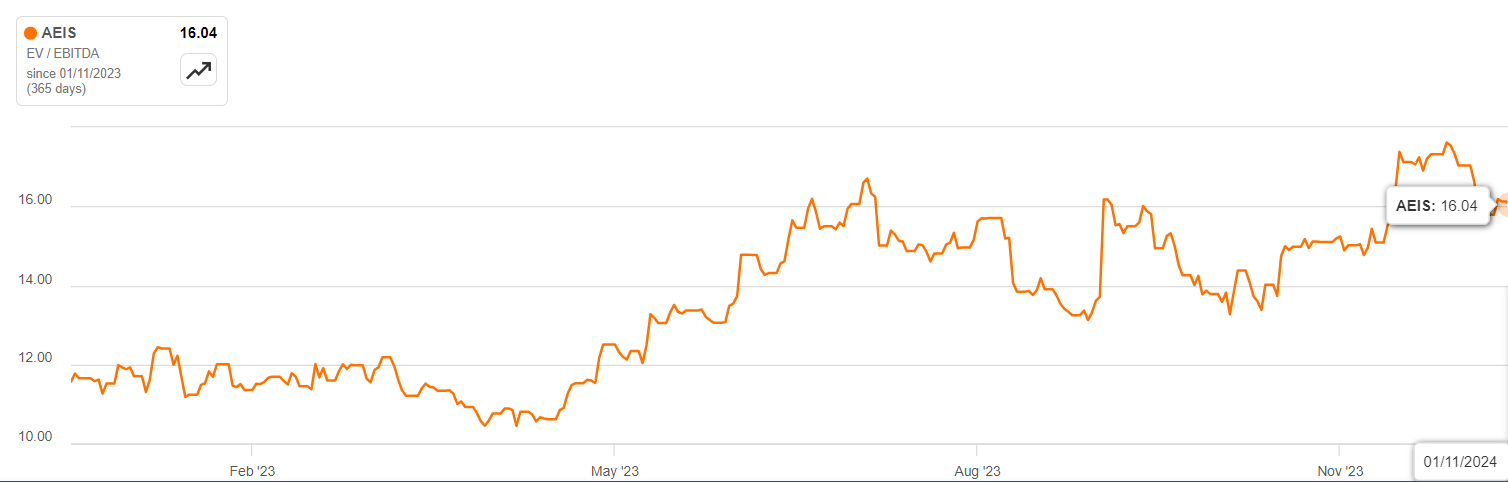

I am using the EV/EBITDA approach to evaluate the valuation of this stock, as it provides a more comprehensive perspective by encompassing both the equity and debt components of the capital structure. At present, AEIS's stock is traded at an EV/EBITDA ratio of 16.04 , indicating a premium compared to the 5-year average of 15.50 and the sector medium of 15.9. As mentioned in the near-term outlook, the expected decline in AEIS's margin in the coming quarters is likely to push this EV/EBITDA metric higher, suggesting potential overvaluation of the stock in the short term.

AEIS EV/EBITDA (TTM) (Seeking Alpha)

{kind=link}

Conclusion

As discussed above, AEIS is currently trading at a slight premium compared to its historical levels. The company is expected to face near-term challenges due to ongoing macroeconomic issues negatively impacting both revenue and margin in the short term across the market. Nevertheless, there is a positive outlook for the longer term, with the expectation of volume recovery in the coming quarters.

AEIS is strategically positioned for margin growth in the future, supported by initiatives such as the consolidation of small-scale production into large, highly efficient factories, and a shift towards higher-margin products. Despite these positive factors, considering the current valuation and the near-term challenges, I am taking a neutral stance on this stock, choosing to remain on the sidelines for now.

For further details see:

Advanced Energy Industries: Near-Term Headwinds And Fair Valuation