ASIX - AdvanSix: Consumer Recycled Offerings Could Imply Undervaluation

2023-11-07 12:44:20 ET

Summary

- AdvanSix Inc. does not have a positive outlook for nylon in 2023, but the North American acetone industry and agriculture industry show promise.

- The company offers specialty materials for various industries and has a broad client base.

- The balance sheet shows a strong current ratio and significant assets, indicating a stable financial position.

AdvanSix Inc. (ASIX) did not report a beneficial outlook for nylon in 2023, however, the outlook for the North American acetone industry and the agriculture industry does look promising. Promises about higher productivity, beneficial effects from exports, and FCF growth from new post-industrial and post-consumer recycled offerings are also quite appealing. Even considering potential strikes, cyclical behavior of some industries served, and failed introduction of products, I think that ASIX looks quite undervalued.

AdvanSix

With clients participating in a wide variety of end markets such as construction, general industrial, agrochemical, paint, packaging, fertilizers, and metals, AdvanSix is a company that plays a key role in the operation of global production chains, offering specialty materials for industrial application internationally through its five production plants in the United States.

The main products manufactured and distributed by this company are nylon, chemicals, ammonium sulfate, and caprolactam. Each of these products fulfills specific functions within the industries it serves, such as nylon for a variety of clothing manufacturers or automotive companies, or ammonium sulfate for the manufacture of plant nutrients essential in the agroindustrial market.

Operations are conducted via a single business segment that functions equally in each of its five production facilities throughout the country. The benefit that this company has is that due to the large number of final applications that its products have, the outlet to different markets is equally broad, and allows permanent demand for production within a large number of diverse clients.

Balance Sheet

Taking into account that the book value per share appears a bit higher than the current stock price, I decided to take a careful look at the assets and liabilities reported by the company.

Source: Ycharts

With cash and cash equivalents worth $22 million, the company noted accounts and other receivables of $144 million, inventories worth $229 million, and total current assets of about $413 million. The current ratio appears larger than 1x, so the company may not suffer a liquidity crisis any time soon. Additionally, with property, plant, and equipment worth $830 million, goodwill close to $56 million, and intangible assets of $46 million, total assets were equal to $1476 million. The asset/liability ratio is close to 2x.

Source: 10-Q

Among the most relevant liabilities, I found accounts payable close to $230 million, accrued liabilities of $41 million, a line of credit of $170 million, and postretirement benefit obligations close to $3 million. Total liabilities are equal to $721 million.

Source: 10-Q

Beneficial Outlook, And Market Expectations Outside The Nylon Industry

I took very seriously the outlook given by management about the unfavorable supply and demand conditions for nylon. With that, I believe that the company will most likely profit from other materials sold including caprolactam, chemical intermediaries, and ammonium. At the end of the day, in the three months ended September 30, 2023, Nylon only represented about 27% of the total amount of sales.

{kind=link}

I decided to have a look at the positive parts of the outlook noted by management, including favorable numbers in the agriculture industry and beneficial market conditions for the North American acetone industry. With that, I also believe that the capex expected in 2023 of about $115 million will most likely be appreciated by investors. In my view, it means an increase in infrastructure and capacity.

Source: Quarterly Presentation

With the previous outlook, I also had a look at the expectations of other market participants, which I believe are a bit better than those reported by the company. They are expecting a decline in net sales in 2023, however, both net sales and FCF growth are expected to come back in 2024. In my view, if the numbers trend up higher in the coming months, we may see a turnaround in the stock price.

Source: SA

In particular, 2024 net sales are expected to be close to $1.583 billion, with net sales growth close to 1.8% in 2024, and 2024 EBITDA of about $216 million. Besides, the investment community is expecting earnings before tax of $132 million, 2024 net income of $100 million, and 2024 free cash flow of about $63.2 million.

Source: S&P

Debt Analysis

Since 2016, the company has made significant efforts to lower its leverage. From around 0.8x, its financial leverage declined to close to 0.1x in 2023. I believe that further declines in net leverage would most likely bring the attention of more market participants, and may bring stock demand. With that, small increases in leverage for acquisitions would not be worrying.

Source: Ycharts

With that about the total amount of leverage, I studied a bit the terms obtained for different credit agreements reported in the last annual report. The company is paying close to Eurodollar rate plus a margin ranging from 1.25% to 2.25%. The Eurodollar rate is currently at close to 5%-6%, so I believe that the cost of capital of around 8%-10% would be quite conservative.

"Borrowings under the Credit Agreement bear interest at a rate equal to either the sum of a base rate plus a margin ranging from 0.25% to 1.25% or the sum of a Eurodollar rate plus a margin ranging from 1.25% to 2.25%, with either such margin varying according to the Company's Consolidated Leverage Ratio (as defined in the Credit Agreement). The Company is also required to pay a commitment fee in respect of unused commitments under the Revolving Credit Facility, if any, at a rate ranging from 0.15% to 0.35% per annum depending on the Company's Consolidated Leverage Ratio." Source: 10-k

Base Case Scenario: Profit Margin Increases, Higher Quality Products, Exports, And Post Consumer Recycled Offerings Will Most Likely Bring FCF Margin Growth

At present, the company seeks to increase its profit margin by using a smarter low-cost production structure with global reach for distribution as well as promoting portfolio simplification. Additionally, the company appears to be exiting production of certain low-margin products, which will most likely enhance FCF margins in the coming years. A clear example of this strategy was the decision to exit production of some low-margin oximes products in 2023.

{kind=link}

Under this scenario, I assumed that AdvanSix would successfully lower its investment in the Nylon industry, and take successful actions already announced. With higher productivity, leveraging new sales channels, and offering new post-industrial and post-consumer recycled offerings, I would expect FCF growth.

{kind=link}

It is worth noting that AdvanSix is expanding its relationship with international clients, which will most likely offer more access to a larger target market. In the nine months that ended September 30, 2023, international sales represented 17% of the total amount of sales, a bit more than that in 2022.

{kind=link}

Finally, under this scenario, I assumed that stock repurchase agreements will most likely continue, which may bring more demand for the stock, and may enhance the stock price in the coming years. In the last presentation, management offered several explanations about the recent million shares repurchased from the open market.

Source: Quarterly Presentation

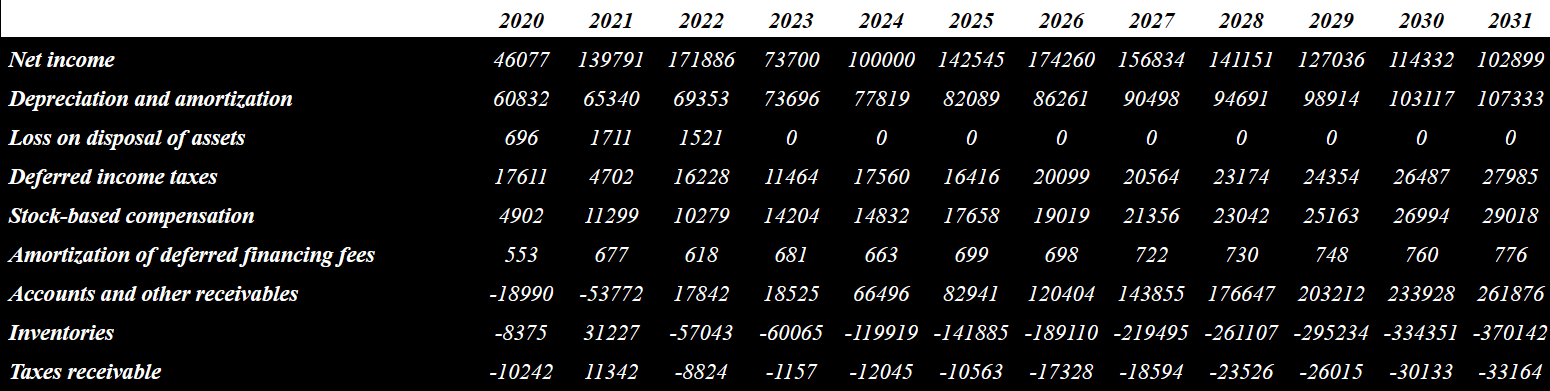

Under this case scenario, my numbers include 2031 net income of about $102 million, depreciation and amortization worth $107 million, and stock-based compensation of $29 million.

{kind=link}

Additionally, with accounts and other receivables of $261 million, inventories worth -$371 million, accounts payable of about $144 million, and other assets and liabilities of -$121 million, I obtained 2031 CFO close to $277 million. Finally, taking into account expenditures for property, plant, and equipment of -$163 million, 2031 FCF would be about $115 million, which is in line with previous results.

Source: Ycharts

{kind=link}

Now, taking into account a cost of capital of about 8.1%, which I believe is quite conservative, the NPV of future FCF from 2023 to 2031 would be close to $859 million. Besides, if we include an EV/FCF of 7x, the total enterprise value would not be far from $1.259 billion. Adding cash in hand, and subtracting benefit obligations and the line of credit, the implied equity valuation would be close to $40 per share, and the IRR would be 7%.

Source: DCF Model

Note that the enterprise value/FCF multiple used is pretty much close to what the company reported in the past. Median EV/FCF multiples stand between 13x and 6x.

Source: Ycharts

Worst Case Scenario And Major Risks

Added to the competitive position that forces the company to be successful in launching its new products and reading market demand trends, in my view, the cyclical behavior of the industries it serves can generate volatility in the results, and lead to an imprecise forecast in the short term. Under this case scenario, I assumed that cyclical behavior would affect future cash flow statements a bit more than in the base case scenario.

Furthermore, I assumed that the breakdown of relations with one of its main clients may lead to serious complications in terms of the operating margin and the current channels through which it makes its sales. As a result, under the worst-case scenario, we may see a certain decline in net sales.

Likewise, the company's activities require a large amount of liquidity available to be carried out. This factor can mean a risk in terms of access to financing sources or the ability to generate liquidity to finance the course of its operations. Under the financial model in this case scenario, I assumed a small increase in the cost of debt.

Additionally, I assumed that AdvanSix could suffer certain labor strikes like that announced in April 2023. As a result, management may have to increase salaries, which could lower future FCF margins, and lower the stock capitalization.

"On April 7, 2023, the Company issued a press release announcing that a labor strike had been initiated by the Hopewell South bargaining unit, consisting of the International Chemical Workers Union Council/the United Food and Commercial Workers, Local 591-C, the International Brotherhood of Electrical Workers, Local 666" Source: 10-Q

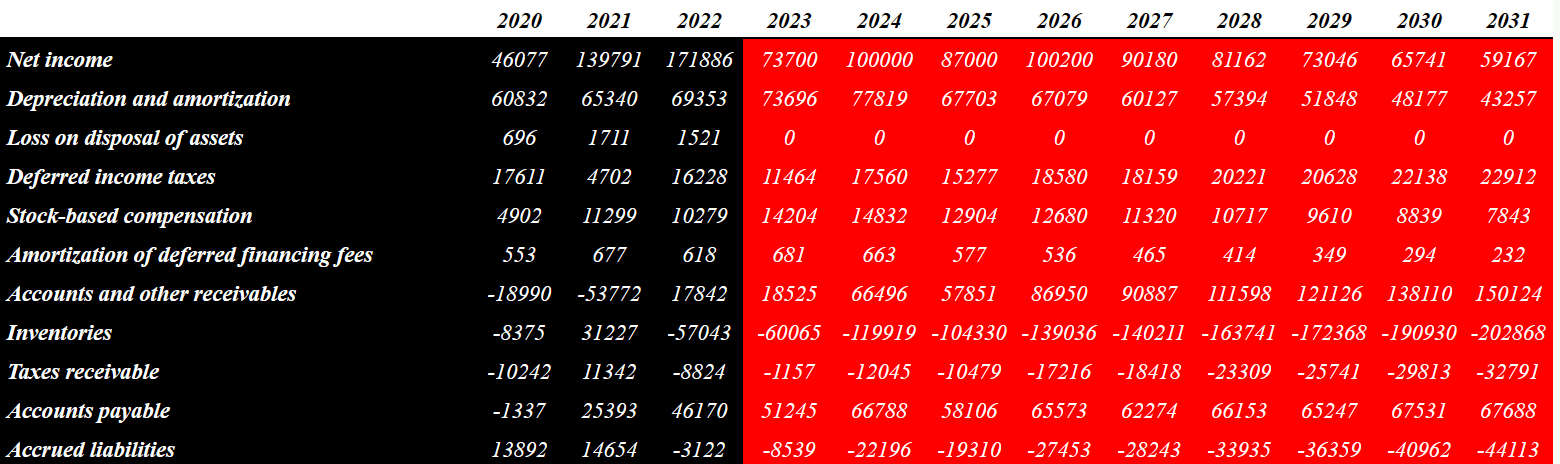

My cash flow forecasts under my worst-case scenario included lower net income, lower D&A, and lower changes in accounts receivables. Finally, I also assumed that FCF would not really cross $117 million.

More in particular, I assumed 2031 net income of close to $59 million, 2031 depreciation and amortization worth $43 million, stock-based compensation of $7 million, and accounts and other receivables of $150 million.

{kind=link}

Finally, with changes in inventories of -$203 million, taxes receivable worth -$33 million, and changes in accounts payable of $67 million, I obtained 2031 CFO of $145 million. Taking into consideration expenditures for property, plant, and equipment worth -$62 million, 2031 FCF would be $84.55 million.

{kind=link}

Under this scenario, which included FCF between $84 million and $117 million, I included a WACC of 10% and an EV/FCF multiple of 6x. The results were a forecast price of $23 per share and an IRR of less than 1%.

Source: DCF Model

Competitors

Highsun Group Holdings Ltd., BASF Corporation (BASFY) (BFFAF), Sinopec (SPTJF), DOMO Chemicals GmbH, LANXESS AG (LNXSF), and UBE Corporation (UBEOF) are the main competitors in terms of integrated manufacturers, to which are added Pasadena Commodities International and Nutrients Ltd. in the production of ammonium sulfate and INEOS Phenol and Altivia in the production of acetone. In my view, due to the complexity of the industrial processes associated with these products, it is not easy to enter the industry. It has high entry barriers.

Conclusion

Even considering the difficult period that the nylon industry goes through, AdvanSix did deliver beneficial words with respect to numbers in the agriculture industry and beneficial market conditions for the North American acetone industry. With these words, like other market participants, I believe that we may see an increase in both net sales and profitability from 2024. Taking into account announcements of higher productivity, new sales channels, and new post-industrial and post-consumer recycled offerings, there is room for optimism. Even considering risks from labor strikes, cyclical behavior of the industries served, or failed introduction of products, AdvanSix does look undervalued.

For further details see:

AdvanSix: Consumer Recycled Offerings Could Imply Undervaluation