AAVVF - Advantage Energy: Carbon Capture Bonus

2023-11-01 11:08:49 ET

Summary

- Advantage Energy Ltd. is a highly efficient Canadian operator with a focus on growth and shareholder repurchases.

- The company is transitioning to more liquids, which is improving margins, and has a carbon capture synergy that could benefit shareholders if it goes public.

- Advantage Energy has been successful in keeping operating costs low and may benefit from the increasing ability to export natural gas in the future.

- Margins will grow as more profitable liquids are added to the production mix in the future.

- The addition of rich gas production allows superior profitability under a wider variety of industry conditions.

Advantage Energy Ltd. ( AAVVF ) is one of the more efficient Canadian operators. This is a growth story that traditionally handles free cash flows through shareholder repurchases. Therefore, investors looking for income can look elsewhere. However, in addition to the growth of a very efficient natural gas operation, there is both a transition to more liquids which is enhancing margins and a carbon capture synergy which could provide a bonus return to shareholders should it go public.

Advantage Energy reports in Canadian dollars. This company was long a dry gas producer until it discovered an interval that is essentially rich gas. When that happens, the usual strategy is to try to hang on to the natural gas operating costs when possible while adding the extra value of oil and condensate (among other things) to the natural gas stream.

Third Quarter Summary

To a large extent, this company has been very successful in doing just that.

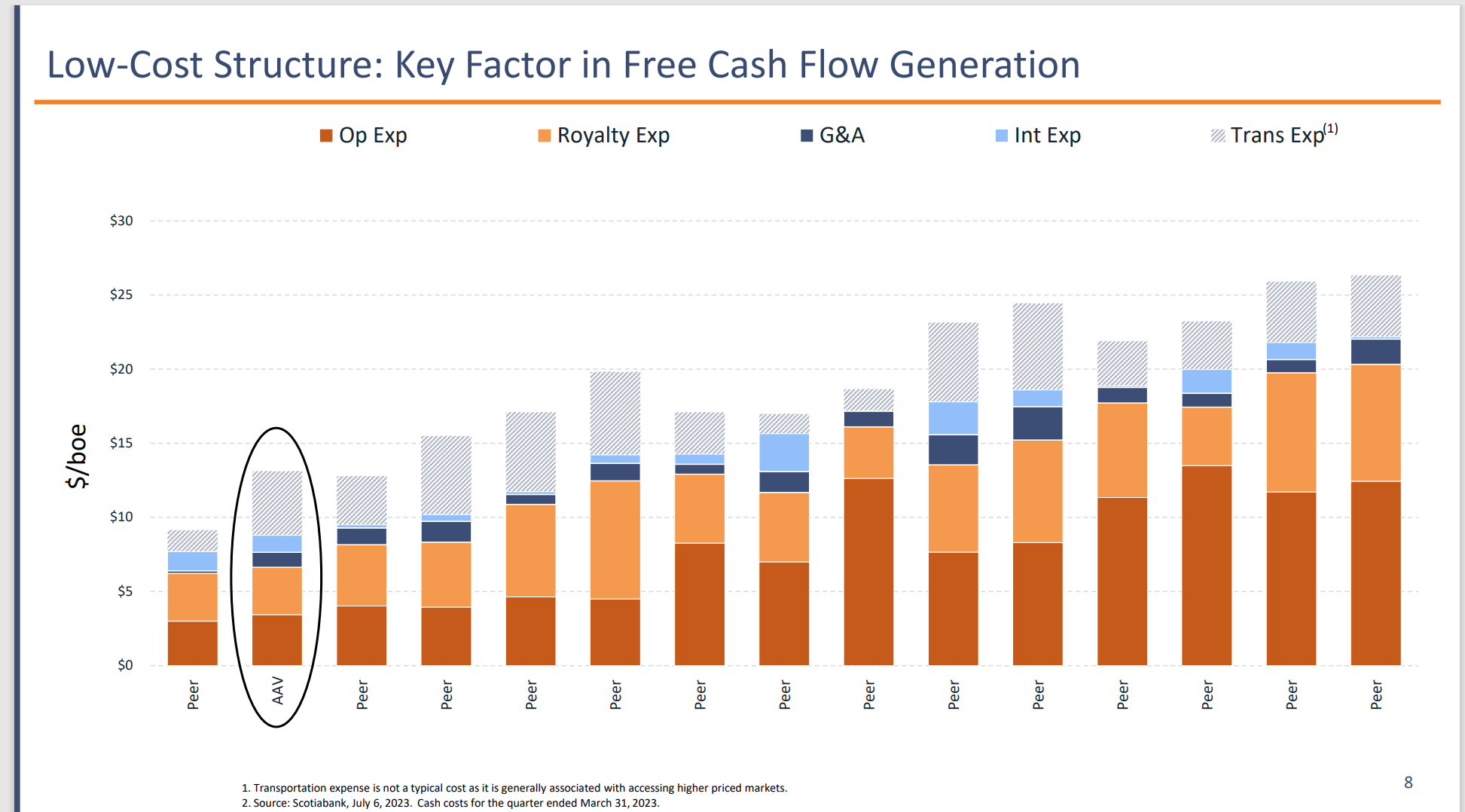

Advantage Energy Operating Cost Comparison (Advantage Energy Investor Presentation October 2023)

{kind=link}

Anytime a company offers a comparison, an investor can be sure that the company cherry-picked the competition. However, the latest quarterly report for Q3 would appear to confirm that the company has been remarkably able to hang on to low costs just like the comparison above shows.

Transportation expenses are on the high side. But if that higher expense gets the company's product to premium markets, then that expense could well be justified.

Natural gas pricing should, in the future, benefit from the increasing ability of North America to export natural gas. That may lessen the need for the ability to move natural gas from one premium market to another as market conditions vary.

Operations

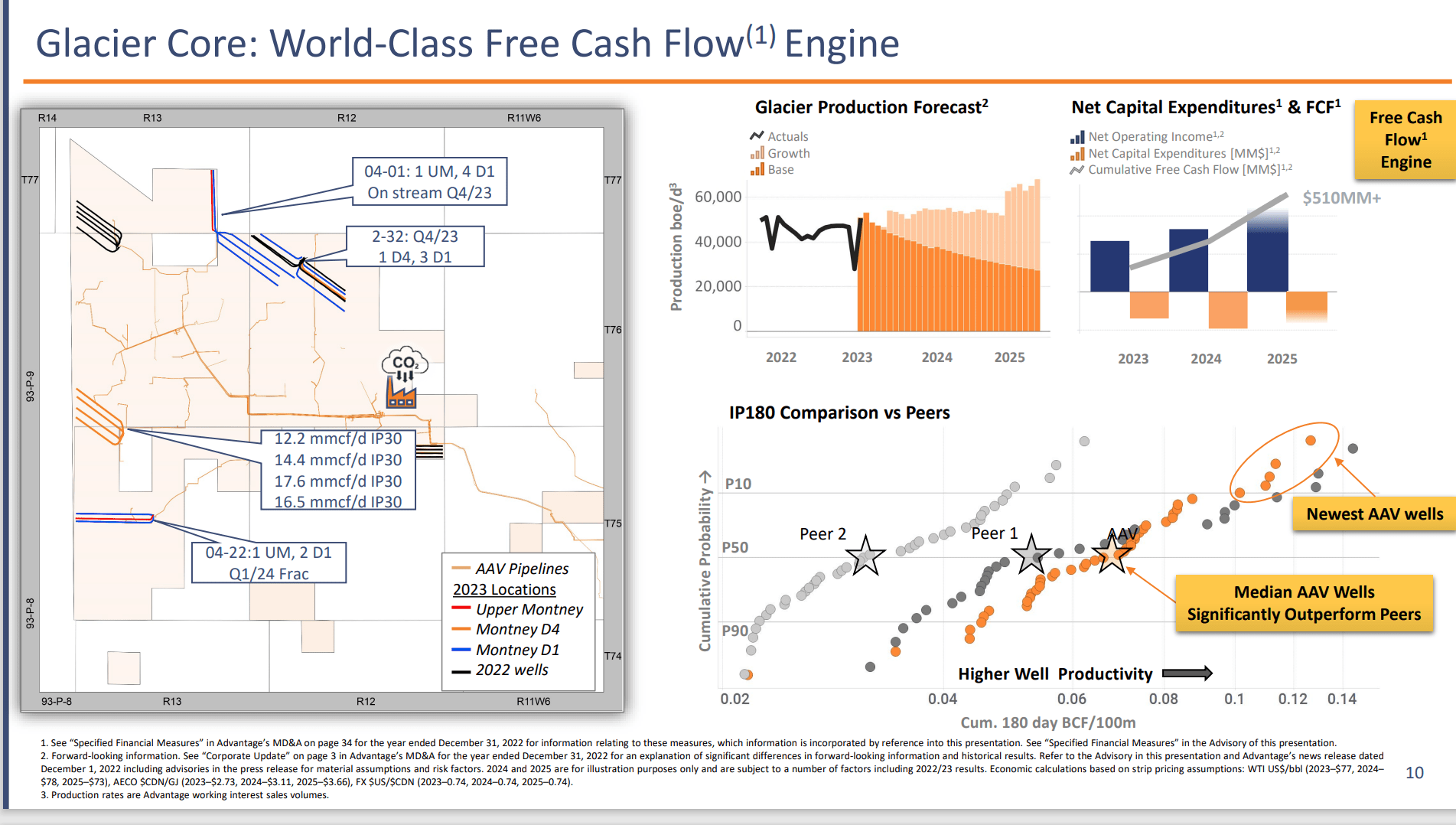

The dry gas area where the Glacier plant is located is very competitive for capital with the recently discovered rich gas areas.

Advantage Energy Glacier Characteristics (Advantage Energy Corporate Presentation October 2023)

{kind=link}

Some unexpected progress in well designs has aided the already tremendous profitability characteristics of the area. The result is shown above with flow rates that more than compensate for the relatively cheap costs in the area. Paybacks in this area are often below one year under a wide variety of industry scenarios.

The only threat to profitability comes from the AECO benchmark variations. Management has long routed natural gas out of the area to avoid those price gyrations.

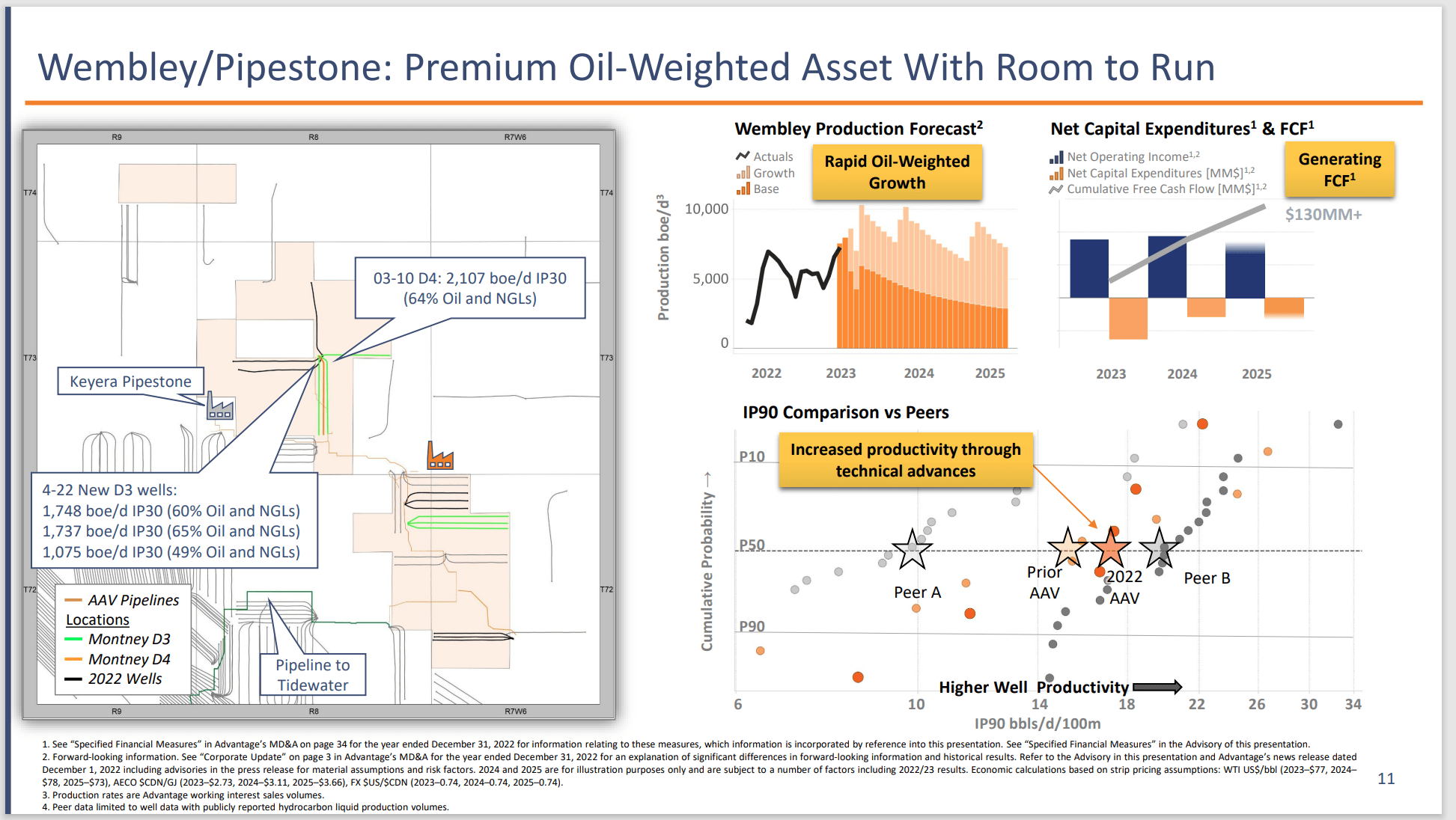

Oil Weighted

Fighting for the most profitable part of the company is the oil weighted acreage. The only reason this is a fair fight is because of the unusually good profitability of the dry gas production. That profitability has at times slowed the exploration of rich gas but right now the oil-weighted liquids acreage appears to have the upper hand. This management is smart enough to realize having the flexibility of both rich gas plays and dry gas plays to cater to changing market conditions is likely to prove to be a competitive advantage.

Advantage Energy Summary Of Some Of The Oil Weighted Acreage Characteristics (Advantage Energy Investor Presentation October 2023)

{kind=link}

As shown above these profitable wells likewise have outstanding characteristics as well. More importantly they give management some flexibility should the natural gas market crash as it has in the past.

This is one of the oil weighted plays. Some characteristics will vary with acreage. But the main ideas presented above pretty much have the same point as this area.

Overall Profit Characteristics

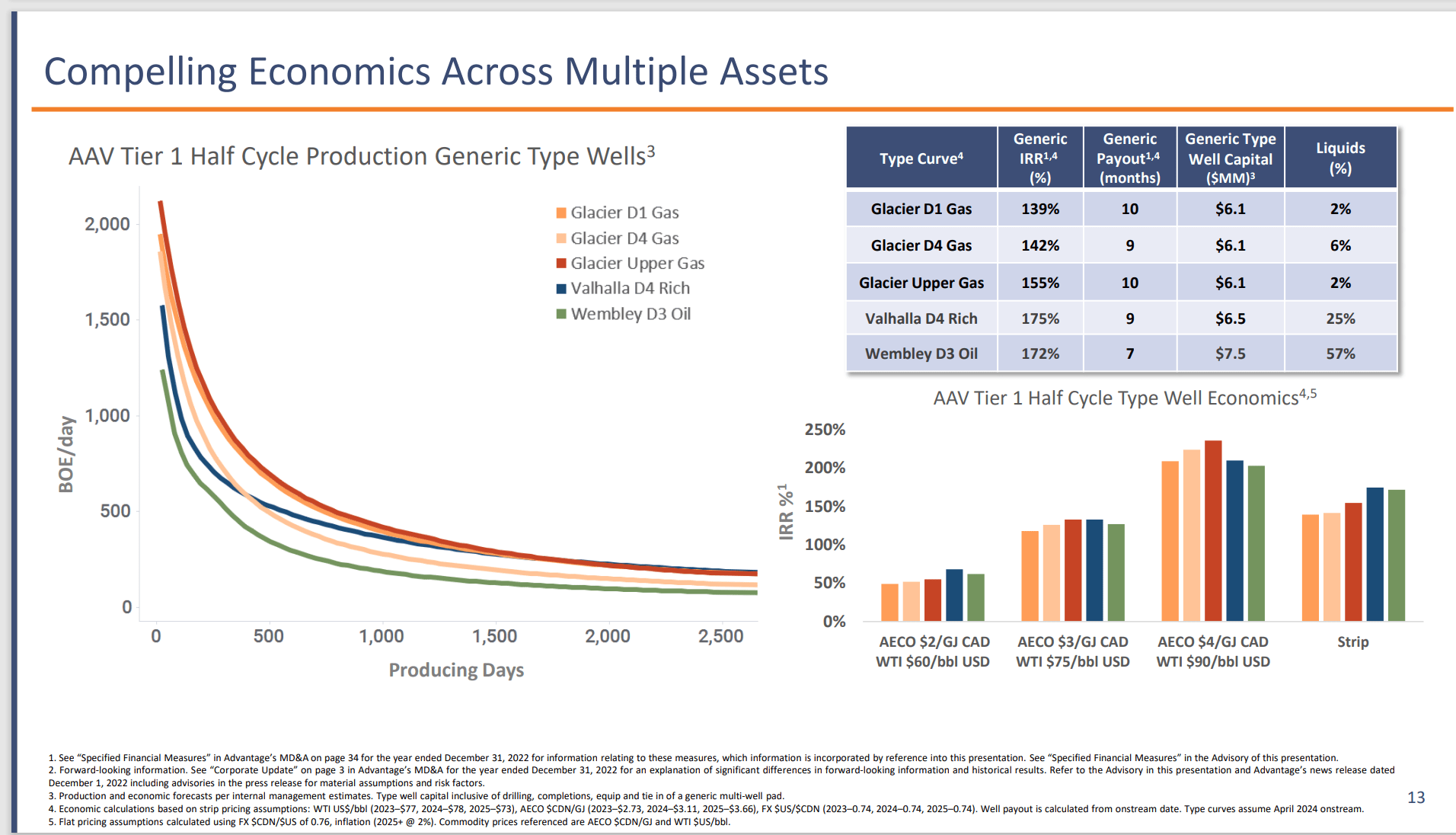

In the current environment, this is one very profitable company.

Advantage Energy Schedule Of Payout Periods And IRR's (Advantage Energy Investor Presentation October 2023)

{kind=link}

The only way this company is not very profitable is if both natural gas and oil prices crash and stay low for a significant period of time. That is unlikely. Since management has also found some condensate production, and condensate is a premium product as well, this company appears to have a long-term profitability advantage over much of the industry.

The best news is that technology continues to evolve which makes the acreage even more profitable in the future. There are going to be a lot of companies suffering in a downturn before this company is at all financially stressed.

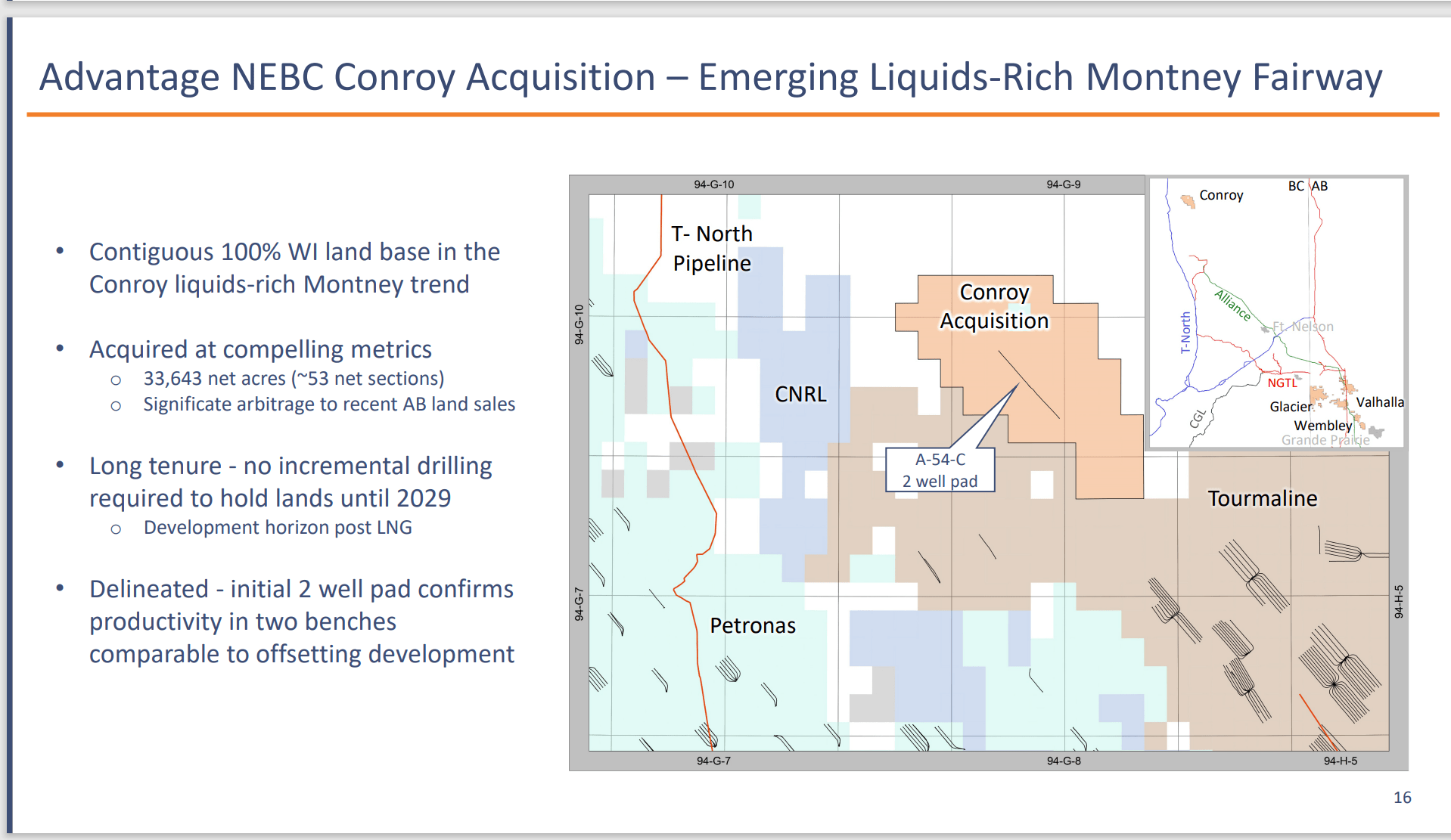

Acquired Acreage

It looks as though the rich gas production is such that there is a "land grab" underway to claim the perceived best acreage.

Advantage Energy Acreage Acquisition (Advantage Energy Investor Presentation October 2023)

{kind=link}

This acreage is a little bit "down the road" from the company's area of operation. But it is probably close enough that management is familiar with the acreage. this is bolstering the company's rich gas or liquids weighted holdings (depending upon you preference terminology).

What is interesting is the names of companies already there. Much of the interest in liquids came after the Middle Montney was discovered to be commercial. Canada, like the United States has a lot of oil and gas that new technology is enabling to be produced with a very reasonable profit. Some years back that was not the case.

This technology improvement keeps adding more acreage to Tier 1 as well as more commercial well locations over time. If one reviews the reserve report from a decent sized group of oil and gas companies, the Tier 1 acreage over time as well as drillable locations tends to hold steady or increase because technology keeps moving forward to make more intervals and more acreage both desirable and commercial. This company goes through that process in its presentation (and its one of the few that does). But it is happening throughout the industry with no end in sight.

Finances

This company generally keeps finances conservative. This company has been known in the past to sell an interest in some of the midstream assets to keep both, the balance sheet conservative while preserving growth options in a cyclical downtrend. That probably will not change in the foreseeable future.

Keeping the finances conservative is a stock repurchase program that takes the place of a dividend. As was noted before, this company has a policy that returns to shareholders will be done with stock repurchases. This allows management considerable flexibility to decide whether to repay debt without worrying about a market reaction to cutting the dividend.

The Future

Advantage Energy also has a subsidiary that Brookfield funded called Entropy that is entering the carbon capture race. should that subsidiary go public it could result in a windfall to shareholders (and the company as well). This is a speculative idea that is really just getting started. But there is potential upside with the Entropy subsidiary that does not exist with many competitors.

In the meantime, management has an immediate future goal to grow production roughly 10% per year. There is probably another couple of percent that will likely happen from technology improvements that cause well outperformance compared to guidance. Stock repurchases when possible will also aid per share growth.

Most likely, profits will grow faster as the margin widens with the addition of very profitable liquids production that has a different cycle from natural gas. The company is definitely not leaving the dry gas production. It is instead insuring decent profitability under a wider variety of industry conditions in the future.

Longtime readers know that the CEO is relatively new. So, there is a little more management risk here than is typically the case. But the conservative balance sheet management as well as the diversification into liquids production is reassuring.

This company grew production the whole-time natural gas prices were declining from the rapid growth of the unconventional business and this company was profitable much of the time. That unusual profitability is likely to continue as management specializes in one area of Canada.

Advantage Energy Ltd. is a speculative strong buy consideration due to the conservative balance sheet, the profitability and the growth prospects. It may be best to make a basket of small companies rather than load up on any one company.

For further details see:

Advantage Energy: Carbon Capture Bonus