AAVVF - Advantage Energy: Trading At A 10% Free Cash Flow Yield At Spot Prices

2023-05-04 11:30:00 ET

Summary

- Advantage Energy is a natural gas producer in Canada.

- Thanks to its diversified points of sale, it is selling the majority of its output based on non-AECO terms.

- The Entropy carbon capture asset is a hidden asset on the balance sheet, but I consider it to be just icing on the cake.

- I have a long position and may add on weakness.

Introduction

Advantage Energy ( AAV:CA ) ( AAVVF ) is one of my largest positions in the Canadian Natural Gas space and will likely become the largest position after the completion of the strategic deal as announced by Spartan Delta ( SDE:CA ) ( DALXF ) so I am definitely keeping my finger on the pulse. The natural gas price has been weak lately, and no one is immune. Advantage Energy confirmed the average realized natural gas price decreased by approximately 30% across the board compared to the first quarter of last year, and I was wondering how this was impacting the company's cash flows.

Unfortunately, the company's website contains download-only links, but you can find all relevant information and documentation here and here.

The Q1 results were relatively weak, as expected

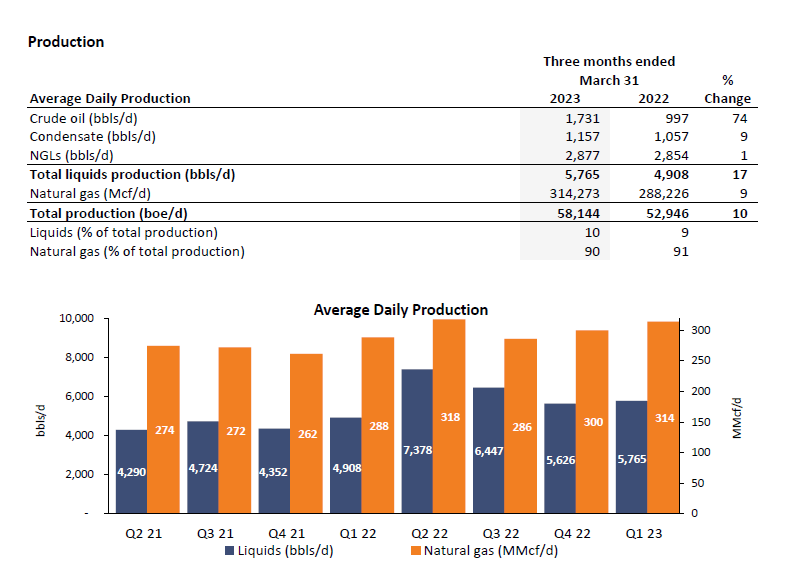

During the first quarter of the year, Advantage Energy produced an average of just over 58,100 barrels of oil-equivalent per day , of which 90% consisted of natural gas. The pure oil production was pretty low (3%) while the condensate production came in at around 2%.

{kind=link}

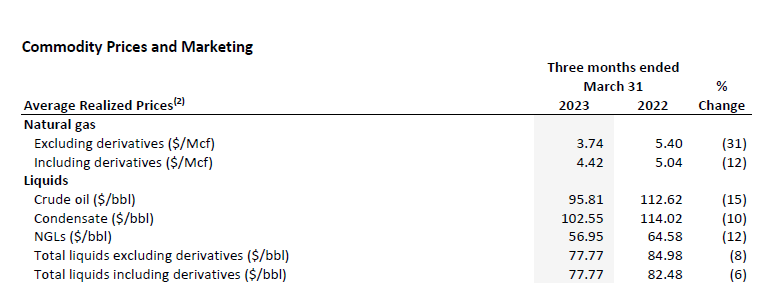

Advantage had some active hedges and that explains why the average realized price was C$4.42 per Mcf compared to the market price of C$3.74. And as you can see below, every commodity sold by Advantage Energy reported double-digit price decreases (even after taking the hedging income into consideration).

{kind=link}

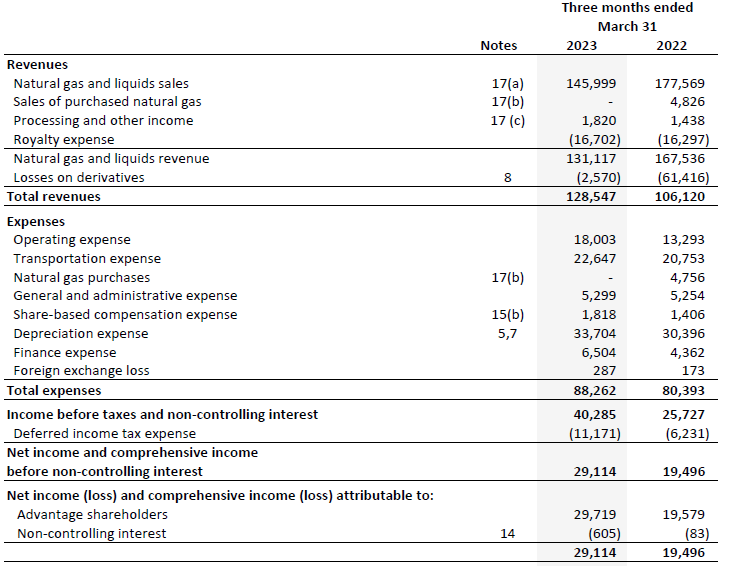

The total revenue in the first quarter of the year came in at C$146M and despite this lower revenue, the total amount of royalty payments remained pretty much unchanged. The company also reported a net loss on derivatives of C$2.6M (it reported a realized gain on derivatives in Q1 but a larger unrealized loss for hedging contracts expiring after the first quarter) resulting in a total net revenue of approximately C$128.5M.

{kind=link}

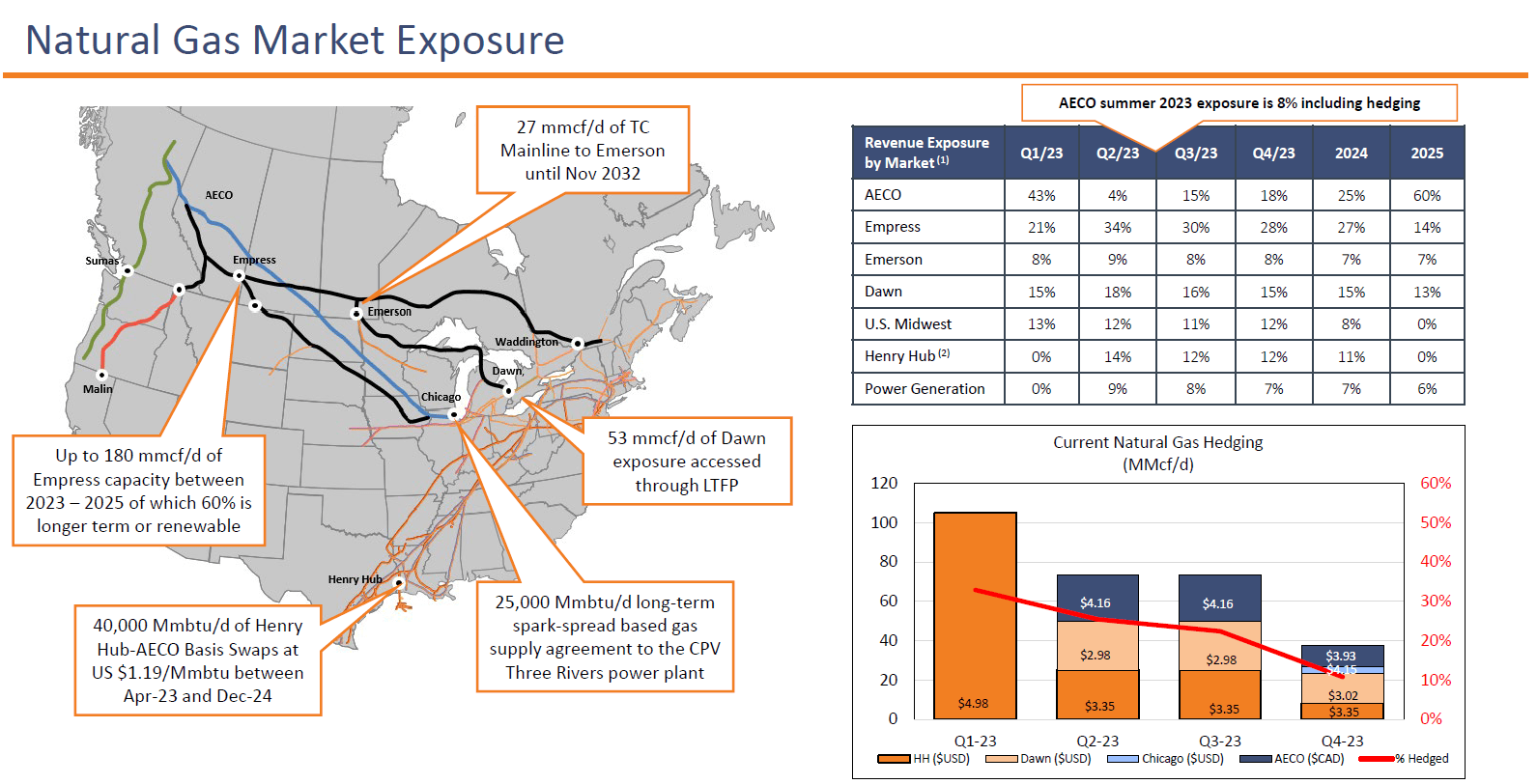

Advantage Energy still has one of the lowest pure operating costs in the sector and its transportation expenses are even higher than the operating costs (this is mainly because Advantage doesn't just sell its natural gas in Canada using (lower) AECO prices but also ships about 57% of its production to the USA and the Midwest where prices are higher and as long as transportation expenses aren't spectacularly high, it makes sense for Advantage to do this and diversify its end market risk. Over the next few quarters, the exposure to the AECO natural gas prices decreases pretty substantially to less than 5% in Q2 and less than 20% in the second half of the year.

{kind=link}

Despite the net hedging loss, the company's pre-tax income was C$40.3M, resulting in a net income of C$29.1M or C$0.18 per share. That's not bad at all given the relatively weak natural gas prices.

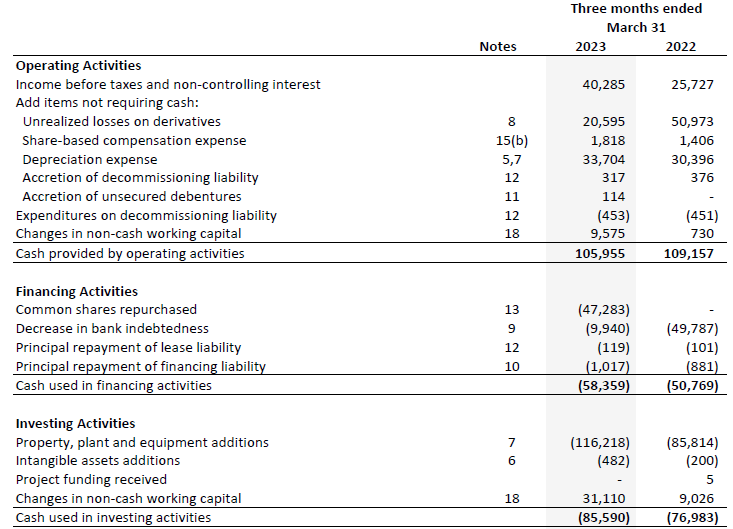

The total operating cash flow during the first quarter was C$106M, but this includes a C$9.6M working capital contribution but also includes about C$18M in hedging gains. So on an adjusted basis, including after deducting the lease payments, the operating cash flow was approximately C$78M.

{kind=link}

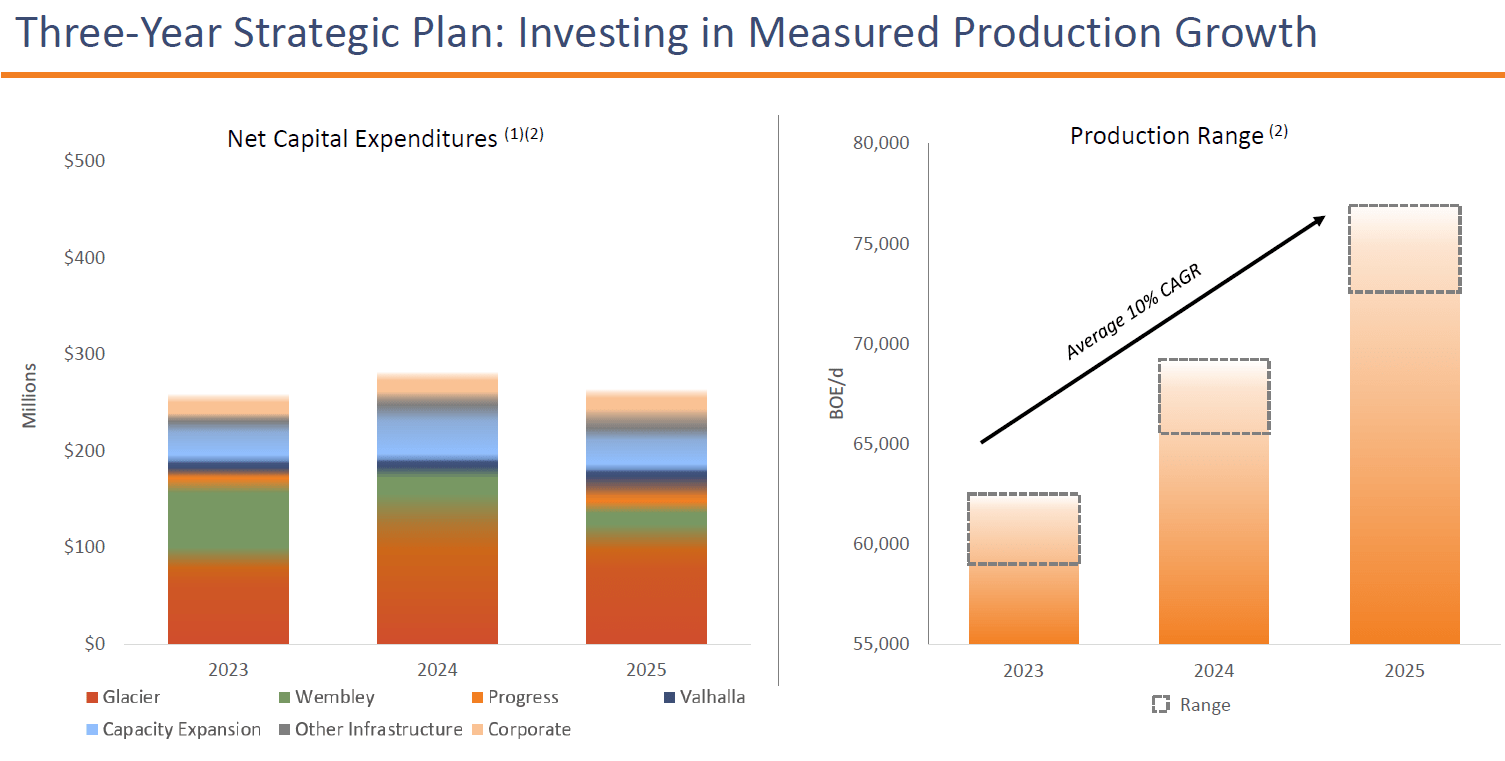

The total capex was C$116M which means Advantage was free cash flow negative, but rest assured this is entirely caused by a seasonal effect as Advantage's financial years are very cash-heavy in the first quarter of the year. The company's guidance for this year is to spend C$250-280M, which means the Q1 capex of C$116M already represents almost half of the full-year capex. In the next few quarters, the total capex will for sure be lower.

{kind=link}

Also keep in mind, the C$250-280M capex program includes growth capex. Despite producing just over 58,000 boe/day in Q1, the company expects to have an average production rate of 59,000-62,500 barrels of oil-equivalent per day this year, and it plans to maintain a 10% CAGR for its production as it anticipates to end 2025 with a production rate of around 75,000 boe/day, that's about 30% higher than the Q1 production rate and the 10% annual growth rate should result in a 20% CAGR on the adjusted funds flow per share.

We also know the company's capital intensity is approximately C$14,250 per flowing barrel, and we know the decline rate is about 24%. This means the underlying sustaining capex to keep the production stable at the current production rate of 58,000 boe/day, the company would have to spend approximately C$200M per year in sustaining capex. Which is comfortably covered by the anticipated Adjusted Funds Flow even if the natural gas price would decrease to US$2/mmbtu on a Henry Hub level.

This also means that using the average realized gas price of C$3.74 (excluding the hedging gains) in the first quarter, the underlying free cash flow result was approximately C$28M and thus pretty close to the reported net income.

Investment thesis

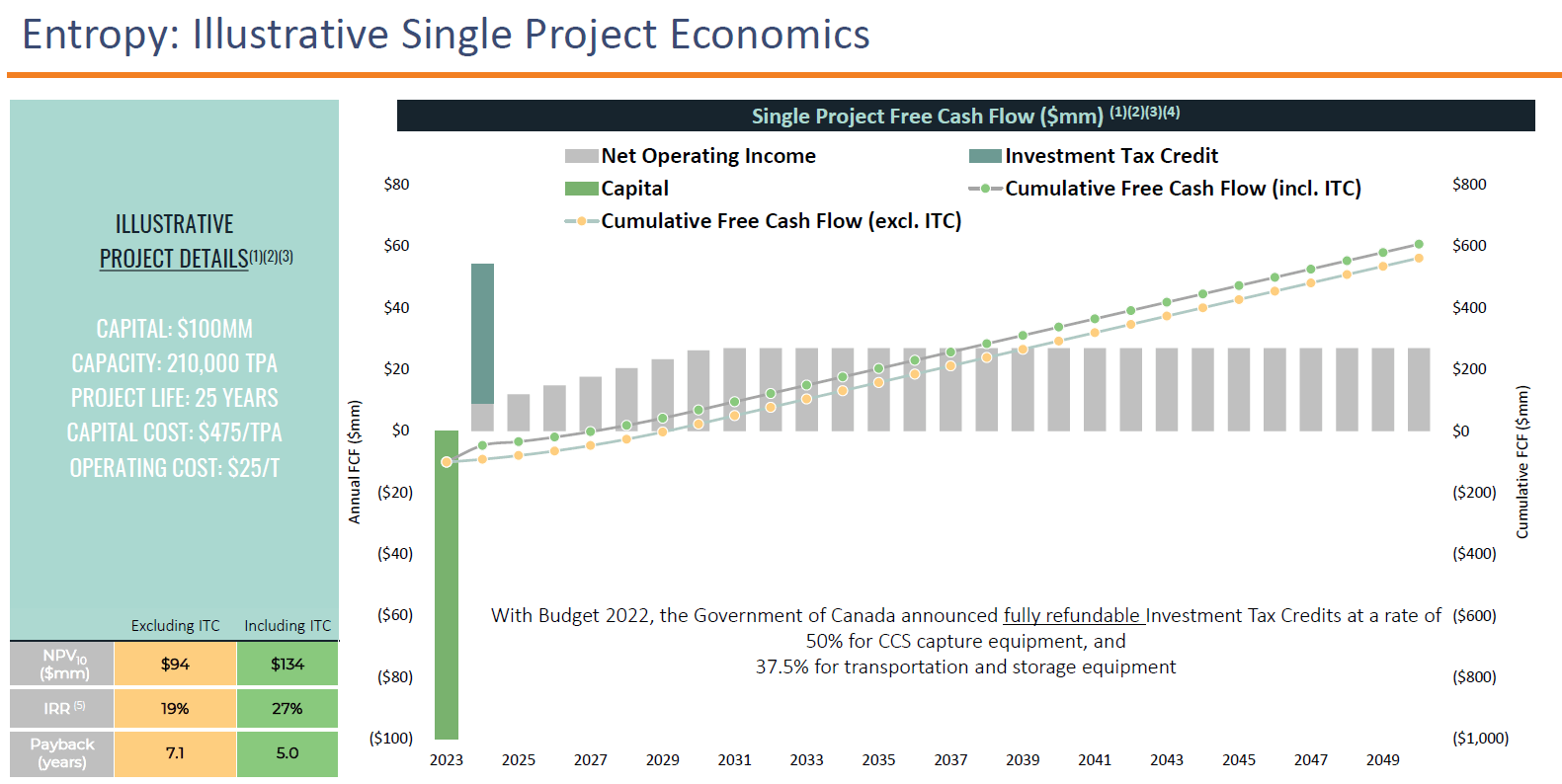

Advantage Energy still owns a majority stake in Entropy , a Carbon Capture subsidiary where Brookfield is earning a 50% stake. As I'm mainly interested in Advantage for its natural gas exposure, I consider the Entropy subsidiary just the icing on the cake. If the carbon capture division takes off and generates a profit (and the theoretical economics shown below look pretty impressive thanks to the Canadian government tax credit), that's great. But right now, I mainly care about the natural gas performance.

{kind=link}

I have a long position in Advantage Energy and could add to this position on weakness.

For further details see:

Advantage Energy: Trading At A 10% Free Cash Flow Yield At Spot Prices