ADV - Advantage Solutions Stock: Undervalued But Still Risky

2023-10-11 15:52:42 ET

Summary

- Advantage Solutions Inc. is a $980-million market cap company that provides outsourced solutions to consumer goods companies and retailers in North America and internationally.

- In Q2 FY2023, ADV reported revenue growth of 5.7% YoY increase, and adjusted EBITDA at $104 million. But net income turned into a net loss due to increased costs.

- If the management succeeds in what it promised, I think ADV's equity value should be ~$1,179 million at 7x EV/EBITDA - that's 21% more than its current market cap.

- However, I am particularly interested in how long shareholders will have to wait for the necessary reversal.

- In the foreseeable future, the world could experience a recession, and then ADV simply won't have time to complete the turnaround running into a new obstacle. The stock is a Hold today.

The Company

Advantage Solutions Inc. ( ADV ) is a $980-million market cap company that provides outsourced solutions to consumer goods companies and retailers in North America and internationally to help them optimize their operations and improve their performance. It operates in 2 main segments:

- Sales [59.2% of total sales in 1H FY2023 ] - focuses on brand-centric services like relationship management, analytics, administration, and merchandising. It also offers retailer-centric services, including in-store media and digital commerce.

- Marketing [40.8% of total sales] - provides shopper and consumer marketing services, brand experiential services, retail experiential services, private label, and digital marketing and advertising.

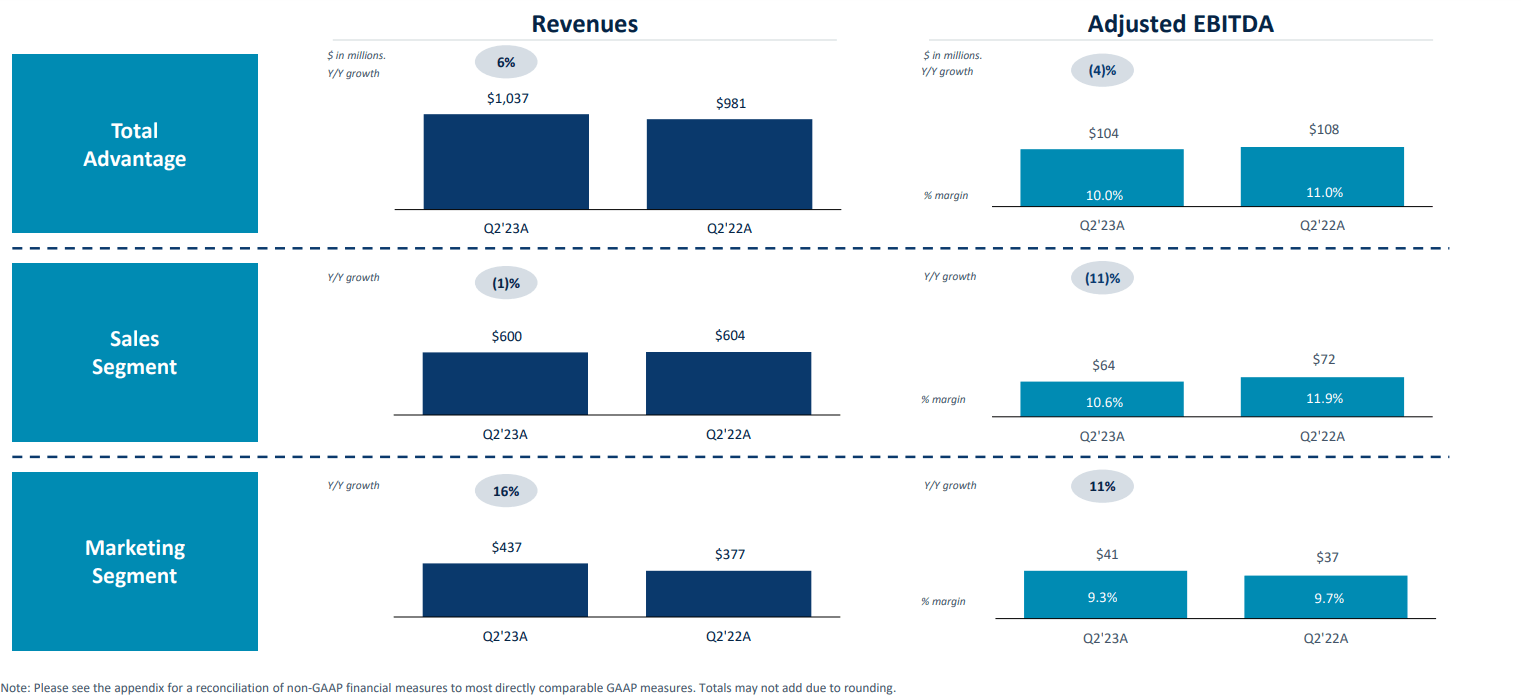

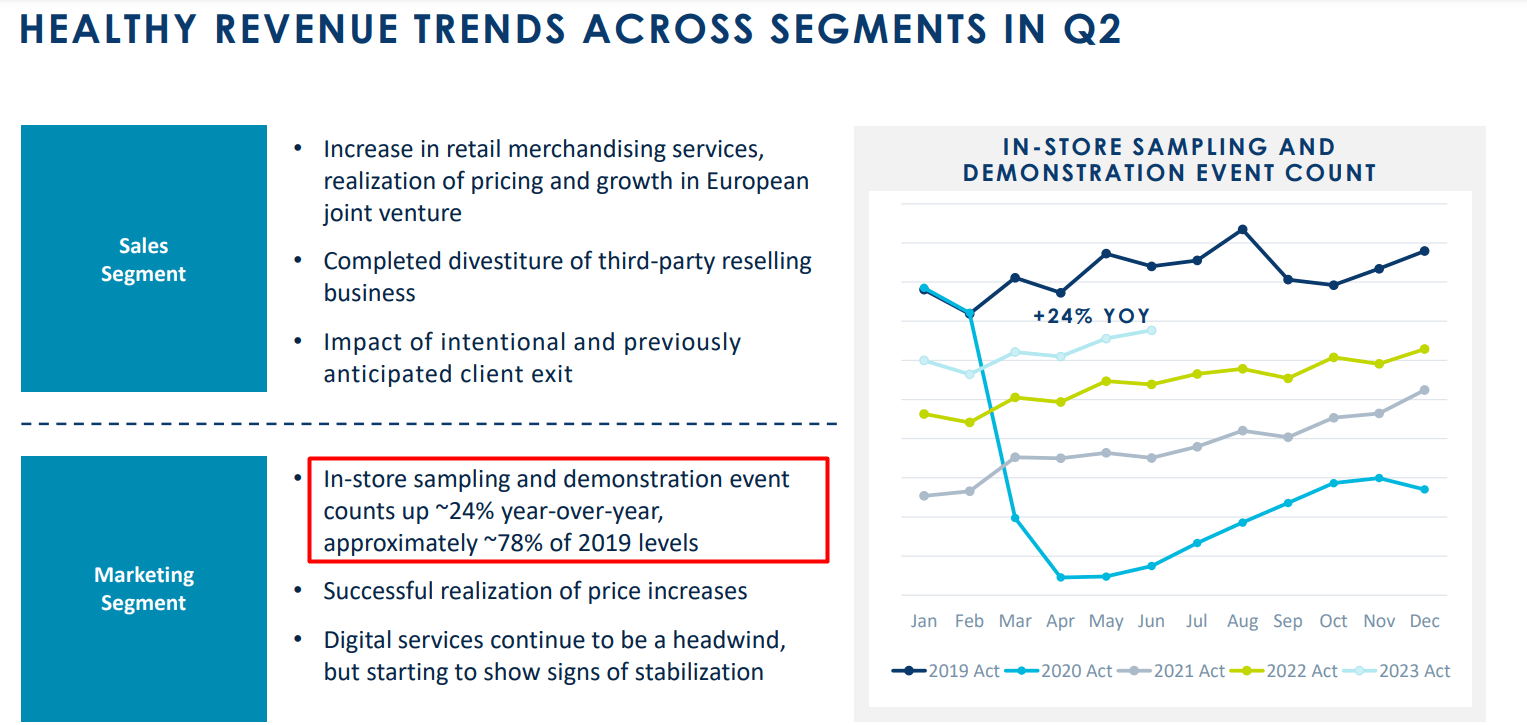

In Q2 FY2023 ADV reported revenue reaching $1 billion, a 5.7% YoY increase, and adjusted EBITDA at $104 million [+3.8% YoY]. The sales segment saw some decline, mainly due to completed divestitures and intentional client exits, but the marketing segment experienced growth, driven by in-store sampling and demonstration services and pricing realization.

{kind=link}

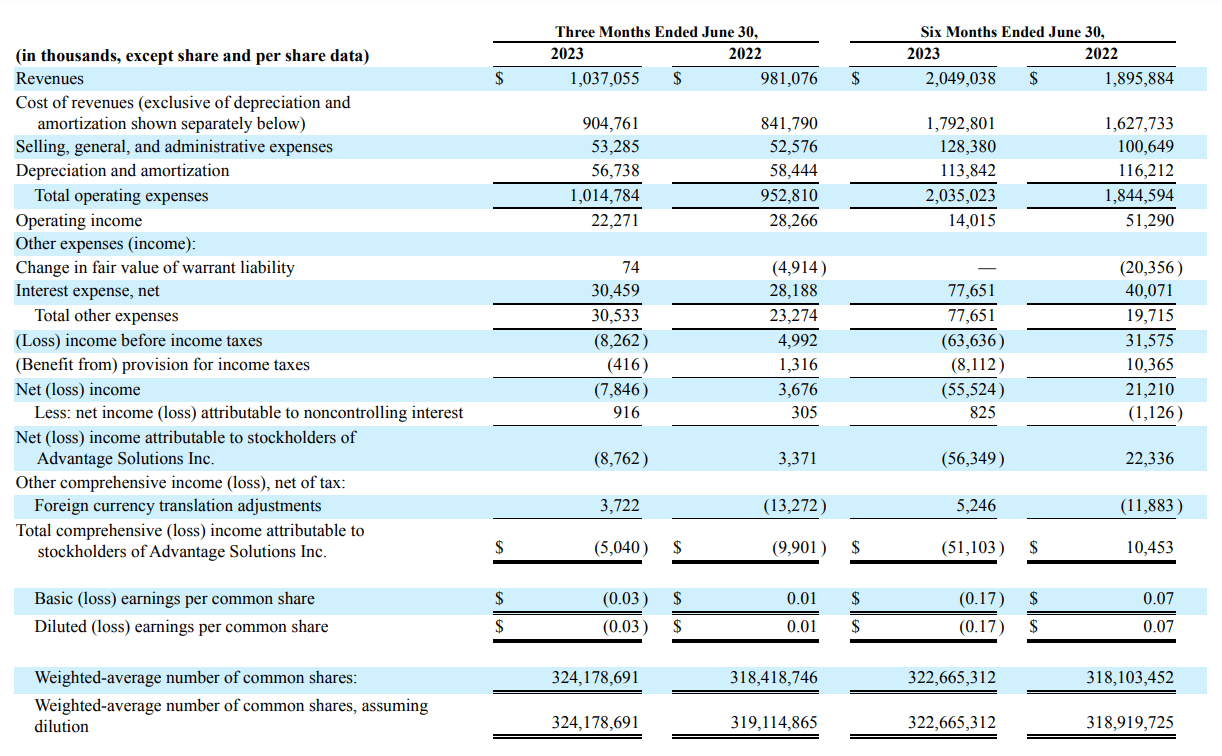

During the quarter, the company faced labor cost inflation: Total operating expenses [OPEX] increased 6.5% year-on-year, 79 basis points higher than sales growth. Due to high operating leverage, ADV's operating income decreased by 21.2% compared to the previous year. Interest expenses increased by 8.1% year-on-year, although total debt decreased by 2.7%. As a result of all this, ADV reported a loss on diluted shares of -$0.03:

{kind=link}

On the positive side, ADV has seen a significant increase in adjusted unlevered free cash flow [$119 million], representing 114% of adjusted EBITDA. The company also experienced growth in new hires and event counts, supporting its sampling and demonstration business.

Also, the company saw a substantial increase in in-store sampling and demonstration event counts [the Marketing segment], up approximately 24% year-over-year and reaching nearly 78% of 2019 levels, indicating strong engagement in these activities.

{kind=link}

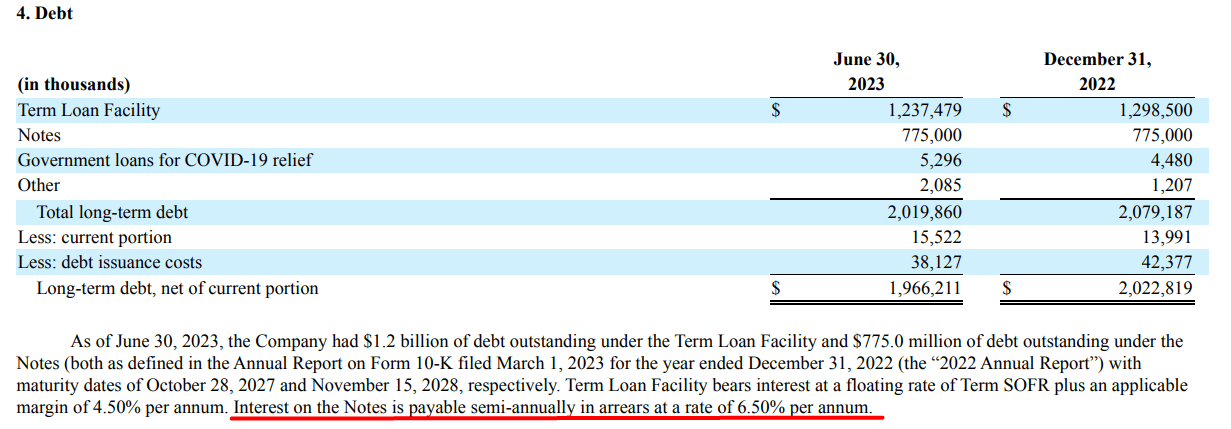

ADV's balance sheet looks healthy, and the company is actively exploring opportunities to reduce leverage, according to the latest earnings call . They've repurchased debt at an attractive discount and have most of their debt [~85%] hedged or at a fixed interest rate.

{kind=link}

For the full year 2023, Advantage reaffirmed adjusted EBITDA guidance in the range of $400-420 million, focusing on pricing realization, in-store sampling, demonstration events, and investments in technology and talent.

During the Q&A session of the earnings call, the executives noted the tight labor market, which is still impacting the business but highlighted strong net new hires and a 10% reduction in turnover. They expect continued growth in their in-store sampling and demonstration business, and while they've made progress, they believe there's still a gap to close to reach pre-COVID levels. They also addressed pricing strategies and indicated that pricing is a significant contributor to their organic growth, with discussions on pricing going well, driven by cost escalation and the value proposition of their services. They see opportunities in the market, such as innovation and private-label growth, which can support their pricing power.

In my opinion, if management manages to maintain reduced turnover and gradually raise prices (which is long overdue due to inflation), I believe ADV's business should continue to recover to pre-COVID levels.

And what about valuation?

The Valuation

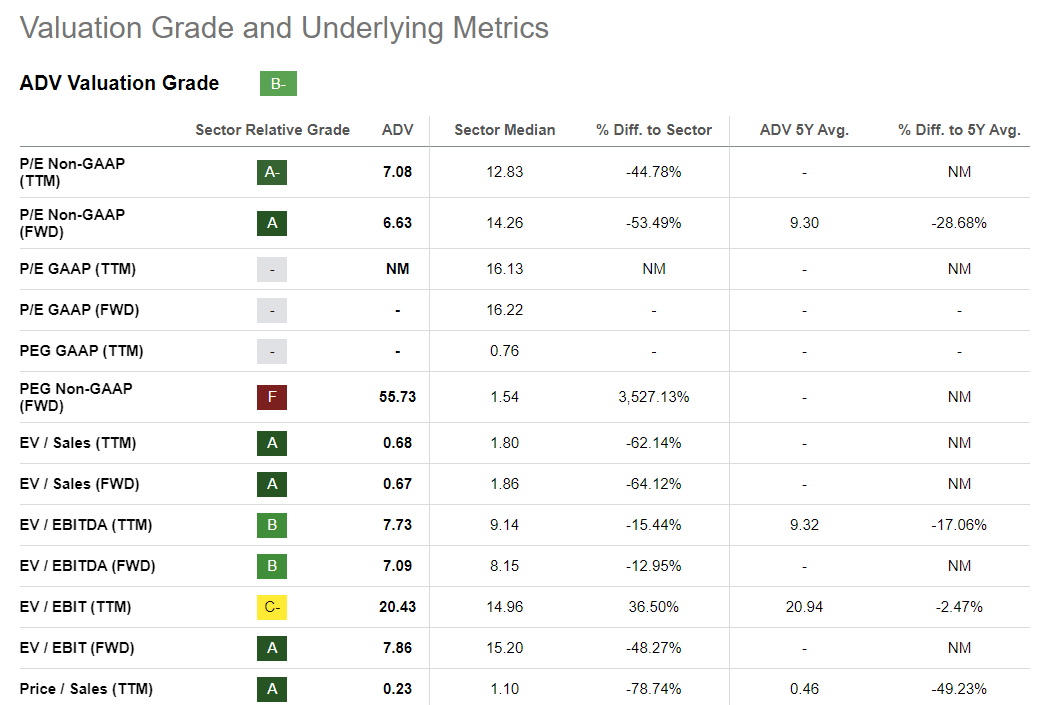

Seeking Alpha rates the stock's valuation as "A", which is a pretty good indicator for the communications services sector: ADV's key multiples are significantly lower compared to others.

{kind=link}

From a historical perspective, it is easy to see how the market has valued the stock using the EBITDA margin and the EV/EBITDA multiple - as the first indicator fell, the second fell, dragging the stock price with it:

Recently, the company's EBITDA has remained flat - at least on an adjusted basis. Judging by management's projections, that should change soon - the company is gradually reaching pre-Covid operating levels, and business metrics like event counts also bode well for a positive outlook.

At an adjusted EBITDA of $410 (the midpoint of the projected range) and taking into account net debt of ~$1.7 billion, ADV's equity value should be around $1,179 million at an EV/EBITDA of 7x - that's 21% more than its current market cap.

The Bottom Line

It seems that the presence of undervaluation should lead me to conclude that ADV stock is attractive. But in reality, undervaluation is far from the only factor investors should pay attention to. As history shows, the future performance of ADV stock will likely depend heavily on how the company's margins and organic growth behave, and I personally have questions about this. I am particularly interested in how long shareholders will have to wait for the necessary reversal. In the foreseeable future, the world could experience a recession, and then ADV simply won't have time to complete the turnaround running into a new obstacle. Moreover, the 21% growth potential I calculated is not high enough to provide investors with a sufficient margin of safety. Therefore, I rate ADV's stock a "Hold" today, with a possible upgrade when the EBITDA guidance becomes reality.

Thanks for reading!

For further details see:

Advantage Solutions Stock: Undervalued, But Still Risky