ATEYY - Advantest: A Tough Quarter But Expect A Strong Recovery

2023-07-30 02:07:29 ET

Summary

- Advantest, the world's largest Automated Test Equipment (ATE) maker, will benefit strongly from high performance AI semiconductor demand.

- AI chips require more complex levels of testing.

- Advantest has several competitive advantages of strong relationships and partnerships with GPU makers.

- Advantest is a larger part of an ATE duopoly with Teradyne.

- Advantest should recover after a weak June quarter in the second half of 2023.

A Tough Quarter

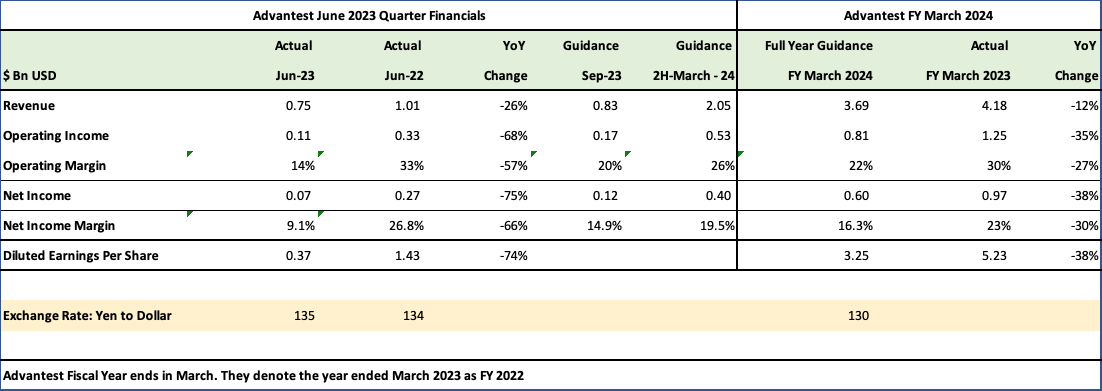

Advantest ( OTCPK:ATEYY ) had a horrible June 2023 quarter, with sales dropping 26% and net income plummeting 75%. This was expected and the company had guided as much, warning of industry wide slowdowns and inventory reductions after the massive growth of three years, which had pulled demand forward. The biggest damage came from PCs and cellphones, which continued to drop due to sluggish demand.

Automated Test Equipment (ATE’s) are not perishable variable cost components for semiconductor manufacturers; you can continue to use older equipment and delay Capex as customers did last year and continue to do so till they clear inventory.

Auto and Industrial demand were bright spots. Maintenance services dropped 10%, much lower than SoC's and management expects it to improve in the next 3 quarters, eventually ending flat compared to last year. Services are about 15% of revenues and non-cyclical revenues from this segment does mitigate big SoC testing revenue drops.

There was a small silver lining - even with such a difficult quarter they still maintained their guidance for FY March 2024, at a more modest 12% decline in revenues to $3.69Bn and a smaller drop of 38% in net income to $0.6Bn. The second half should be a lot better, as chipmakers resume demand for test equipment.

Advantest June Quarter Financials (Advantest, Seeking Alpha, Fountainhead)

{kind=link}

To put this in context, Advantest is coming of its best year in history in FY 2022 with $4.18Bn in revenues and $970Mn in net income. Between 2019 and 2022, Advantest had grown revenues and net income at a CAGR of 26% and 42%, respectively!. This down year was overdue and a lot better than closest competitor Teradyne ( TER ), which is now in its 7th quarter of YoY revenue declines.

The Artificial Intelligence Opportunity

I continue to believe that Advantest will benefit strongly from Generational AI demand.

Here are Yoshiaki Yoshida's, Advantest's CEO's comments on the AI opportunity from their earnings call. Emphasis mine.

The trend towards larger scale and high-performance semiconductors, including high-end SoCs with high computing power and high-end memory such as HBM, will continue. Also, the technical hurdle of improving yields is higher and more thorough testing is required.

We believe that the increase in production of such semiconductors will increase demand for testers over the mid and long-term, leading to growth in our core business. In addition, demand for more diverse functionality not only for servers, but also on the end application side is manifesting itself in the growing number of new players entering semiconductor design.

The increase in the number of devices being developed will also drive tester demand. Heterogeneous integration through the use of advanced packaging technology is also progressing to achieve even higher performance. We have been strengthening our system level test technology.

Therefore, we are able to contribute to the improving the quality of semiconductors in a variety of test processes, including SoC and memory tests, as well as system level tests. Furthermore, we believe that in the future, generative AI technology is likely to change the very process of semiconductor development and manufacturing.

This outlook, echoing Jensen Huang, Nvidia's CEO's call for generational changes and paradigm shifts adds several interesting dimensions of growth for Advantest.

That, this is just the beginning of a secular growth trend for testing equipment.

- Designs will be different.

- Use cases and applications will increase.

- The semiconductor industry will move to new, much more complex testing standards.

- There will be a lot of new players and devices.

The need for higher standards for high grade memory testing chips also augurs well for Advantest. While the memory chips industry suffers from cyclicality and over capacity, secular growth from high grade memory testing should mitigate some of that cyclicality.

Advantest's management summarized their AI opportunities as under, highlighting and emphasizing major shifts in the industry.

And also stressed their competitive advantages of strong relationships and partnerships.

Management had alluded to their readiness for HPC, last quarter as well, mentioning that they were testing prototypes and were ready to handle a deluge of orders. They have solid inroads into the business with a strong customer base comprising fabless, foundries and OSATs, which in turn is helping them pick up new AI business as the experienced competitor.

Here's an interesting exchange from their earnings call between Tetsuya Wadaki, from Mitsubishi with Makoto Nakahara, EVP, Sales, emphasis mine.

Tetsuya Wadaki

Thank you. Then let me ask a follow-up question. Regarding generative AI, you mentioned about memory, but what about processors, GPU, ASIC? What is your outlook? I think market share is one important question. You are strong, but competitors will definitely try to catch up. So in the business related to generative AI, what is your outlook for the next fiscal year also including the competitive landscape?

Makoto Nakahara

Then I would like to respond. This is Nakahara speaking. Processors related to generative AI, as Wadaki-san you may know. We recognize that we have a meaningful market share today. But it is difficult to build such position in a short period of time. We need to spend a long time to build relationships with the important customers.

For example, in GPU, we have a relationship with a world leading company. That engagement started from ten years ago. And in the market, engineering support has been continued. And based on that experience, we also expand our relationships to global customers in the AI area. We have built such a foundation over a long period of time, which includes a relationship of trust which is not likely to collapse in a short time.

Such fabless customers or partners partnered with foundries and OSATs. And we have a collaborative relationship that we have built over many years. So we are willing to maintain that and we are willing to offer new solutions so that we can maintain strong market position.

Any guesses who the leading GPU company is?

Corroborating Advantest's forecast and confidence in AI demand was Taiwan Semiconductor Manufacturing Corp's ( TSM ) CEO, C.C. Wei, who had this to say a few days earlier at its earnings call. Emphasis mine

Today, server AI processor demand, which we define as CPUs, GPUs and AI accelerators that are performing training and inference functions accounts for approximately 6% of TSMC's total revenue. We forecast this to grow at close to 50% CAGR in the next 5 years and increase to low teens percent of our revenue.

Reiterating Buy on Declines:

It helps to be in a duopoly : Advantest is the larger of the ATE (Automated Test Equipment) sector duopoly with Teradyne. There are a lot more details of the virtues of investing in a duopoly in my first article recommending Advantest and I will summarize them here.

- High barriers to entry.

- A specialized business with a long learning curve.

- High switching costs for customers.

- Good pricing power.

- Decades of relationships with existing customers.

Semiconductor sales should recover in the next two quarters : While PC and Cell Phone semi demand has been faltering for the past 4 quarters, Intel ( INTC ) surprised yesterday with a relative beat and positive guidance , which augurs well for a decent recovery towards the later part of the year.

On the flip side, Microsoft's ( MSFT ) June quarter wasn't an AI victory lap. While management emphasized new revenue opportunities and initiatives like the Azure Open AI, the Microsoft 365 Copilot and the BingChat, they didn't put specific revenues or growth numbers for any. It will come over time and from Advantest's perspective it should not matter if there are no clear winners. Instead, more competitors entering this space should expand the market further for test equipment.

The stronger competitor : Compared to Teradyne, Advantest has a more robust and diverse client base, which reduced their down cycle of revenue declines to just on year, - 2023, as compared to Teradyne's two years, 2022 and 2023. I expect Advantest to get back to their 2022 revenue of $4.2Bn by FY 2024 (March 2025). Revenues should grow 16-18% next year from a lower base of $3.69Bn to about $4.3 to $4.4Bn, and 17-20% growth should continue for at least another 3 years.

Advantest is not cheap. The second time I recommended this stock in May 2023, it was at $89 and now at $143, it is at 7X sales; some of the future spoils of AI demand are already priced in and further gains are not going to be as lucrative as the 60% realized in the last 3 months. However, the positives of secular growth for the next 3-5 years and being the market leader in a duopoly are huge. I continue to buy on dips, like I did the day after earnings knocked 10% off its price.

For further details see:

Advantest: A Tough Quarter But Expect A Strong Recovery