ATEYY - Advantest: This Semiconductor Test Equipment Market Leader Is A Good Bargain

2023-05-11 06:48:55 ET

Summary

- Advantest had a phenomenal and historic FY 2022, growing revenues 34% and EPS 55%.

- Mirroring the decline in the semiconductor industry, it forecasted 14% lower revenue growth for FY2023.

- Poor guidance led to the stock dropping more than 10% after earnings.

- I had recommended the stock pre earnings around $88 and think it is an even better bargain now. The long-term story remains powerful.

- As the market leader in the ATE duopoly with Teradyne, Advantest should have sustainable revenue and earnings growth for the next decade.

FY2022 Earnings and FY2023 Forecast

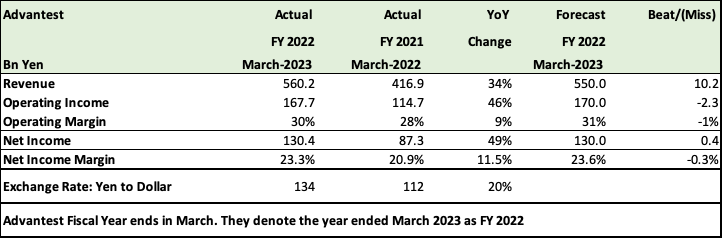

Advantest ( ATEYY ) narrowly beat revenue and net income estimates for Fiscal Year 2022. While the beats were narrow, the performance was nothing short of spectacular, with Sales jumping 34% and Net Income vaulting 49% YoY.

Advantest FY2022 Financials (Advantest, Seeking Alpha, Fountainhead)

{kind=link}

I've maintained the numbers in Japanese Yen to show the comparison in constant currency. There was a currency tailwind aiding Advantest with the Yen dropping 20% from 112/US$ to 134/US$ in the last 12 months. The stronger US Dollar or a weaker Yen helped the Japanese company. With a steady US Dollar this year, I don't believe that it would get the same tailwind in FY2023.

Earnings per share went up from Yen 450 in FY2021 to Yen 697 in FY2022, a gain of 55%!

Unlike its Automated Test Equipment industry duopoly partner, Teradyne ( TER ), which had a terrible 2022, Advantest actually had its best year in its history.

However, reflecting the weaker conditions in the semiconductor industry as we've seen in Qualcomm's ( QCOM ), Advanced Micro Devices's ( AMD ) and Teradyne results so far, Advantest too, expects a difficult year ahead.

Advantest expects the Semiconductor Tester market to contract for the second straight year, with the SoC market size shrinking from $4Bn to $3.4-$3.8Bn and the Memory Tester market from $1.2Bn to $0.9B - $1.1Bn. Worse, these have been knocked down further from just January 2023 estimates of $3.5Bn to $4.2Bn for SOC's and $0.9Bn to $1.2Bn for Memory. At midpoint, the YoY drop is 10% for SoC's and 17% for Memory. Compared to earlier estimates, the guidance is 6 and 5% lower, respectively for SoC's and Memory.

Not surprisingly, Advantest expects a 14% drop in Sales from Yen 560Bn to Yen 480Bn and whopping 37% and 40% drops in Operating and Net Income to Yen 105Bn and Yen 78Bn, respectively. Brutal all right; cyclical semiconductor market weakness didn't catch up with Advantest in FY2022, but it sure is catching up in FY2023. Advantest too, like Teradyne had customers with long wait times, often because of supply chain lags and it was lucky enough to stretch demand fulfillment through FY2022.

I had recommended Advantest, pre earnings around $88, only to see it fall to $77 a few days later after the lower 2023 guidance . The stock has bounced back to $84-85; it was a bargain then and is an even bigger bargain now.

Advantest FY2023 Forecast

Like Teradyne, Advantest is usually very detailed and gives a lot of information in its earnings presentation - another reason to like the stock. The management is also usually conservative.

Advantest doesn't have a single customer over 10%, and because of its wider customer base, it did not suffer the same fate as Teradyne, which lost out in 2022 and at least the first half of 2023, because of the delay in the 3nm roll out and expected ramp up from chip manufacturer, Taiwan Semiconductor Manufacturing ( TSM ).

Here are my insights from the conference call.

- The semiconductor industry started weakening around the second half of 2022, and Advantest doesn't expect a meaningful turnaround till 2024.

- HPC was a standout performer in 2022 and Auto and Industrial demand were good as well.

- The two bright spots in 2023 are expected to be:

- a) The SEM metrology product segment; that's not going to decline because of better demand for mature process photomasks and increased use of EUV lithography by customers.

- b) Services, which should grow 4% YoY on a higher installed base. The Services segment is about 10-11% of total sales.

- They are seeing significant discussions on ChatGPT/AI applications from customers. In this segment, they do have a significant advantage over Teradyne with relationships with almost all of the major players; a fact also mentioned by Teradyne in its earnings call .

- However, the major contribution to revenue from AI will start from 2H 2023 and ramp up only in 2024.

- They also expect some demand recovery for smart phones from the second half and believe that overall the second half would be more than 10% bigger than the first half.

- Advantest has been spending significantly and plans to continue doing so in FY2023 as well, (about Yen 60Bn - also a historic high) on Capex and R&D for HPC, Generative and Conversational AI. While this will hurt margins in FY2023, they believe that these investments on equipment and people will pay off from 2024 when demand grows significantly. They are very confident of strong demand from 2024.

In management's words from the conference call on AI and spending. Emphasis mine.

And we are also working on Advantest cloud and a better business, and we'd like to secure some manpower. So currently our phase is where we have to spend on expenses when revenue is declining, but we are considering this is as the investment phase for our future. So operating income and operating margin decline is something we have to accept at the moment in order to make progress.

Against this backdrop generative AI, could be a promising application.

Well, from customers, specifically, device tester projects are underway. So, it's not that we may receive orders. Devices are actually being designed and the prototypes are being created - that's the current situation. So, there are some specific projects that are underway.

Well, ChatGPT is a hot topic today, and because of the growth of our ChatGPT, GPU and accelerators processing capacity, business should grow, and we have customers in this space, so we should benefit from testing.

Investment Thesis

The virtues of a duopoly with Teradyne, such as barriers to entry and pricing power, gives it sustainable revenues and income for the next decade, as I have highlighted in my earlier article.

Besides, they both remain vital cogs in the semiconductor industry which still has a long runway of growth.

Advantest remains the market leader with 57% share, and it has exposure to a wider section of customers, reducing both demand and cyclical risk.

Having relationships with the major players in the industry, including GPU players, I expect it to benefit strongly from AI semi growth.

Earnings tend to stay rangebound for a couple of years and then breakout with periods of high demand as we can see from the 10 year chart. Its P/E ratio 16.86 is also reasonable.

I expect sales to grow at a CAGR of 12 to 14% for the next 4 years and earnings to grow at 16 to 18%. This includes a difficult FY2023, as I expect Advantest to bounce back solidly in FY2024.

This is a great long term buy and hold; The post earnings decline is a great buying opportunity.

For further details see:

Advantest: This Semiconductor Test Equipment Market Leader Is A Good Bargain