ADYEY - Adyen: A Fintech Diamond In The Rough

2023-08-31 17:49:46 ET

Summary

- Adyen is the payment platform of choice for leading businesses all over the world.

- Even in the midst of competitive pressures, management stood their ground and did not surrender to price cutting.

- Ultimately, Adyen is not in the commodity business — the company strives to deliver a premium product.

- Before H1 earnings results, Adyen was priced to perfection. Today, Adyen is priced for disaster.

- Adyen is a fintech diamond in the rough. Take advantage of the selloff.

Introduction

Adyen ( ADYEY ) has been on my watchlist for a couple of years now, but I've never really looked into the company for one reason and one reason only: overvaluation.

The stock has always traded at a large premium which is why I avoided it entirely. However, due to recent events, Adyen's market cap took a 40% haircut within a couple of days, which got me very interested in the company.

That said, here's a deep dive on Adyen. I hope you enjoy it.

Also, here are the main takeaways of the article:

- Adyen is dealing with short-term headwinds from price competition and accelerated hiring, which nearly cut the stock by half.

- But these problems seem temporary - growth and profitability should return to where they were as the company invests in its team and platform, which should drive future growth.

- Following the selloff, valuation looks reasonably attractive - take advantage of this opportunity.

Company

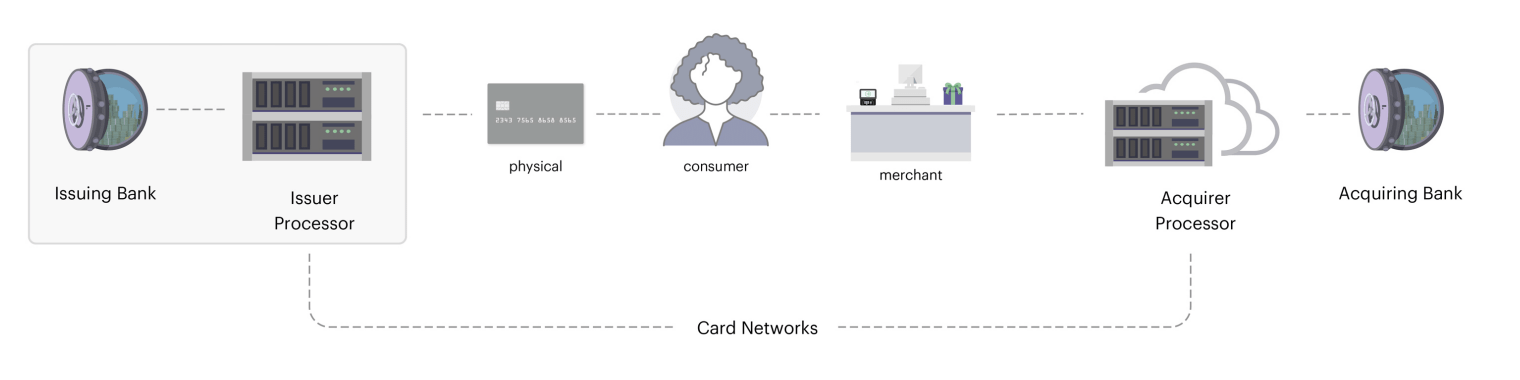

As with most of my fintech deep dives, I'd like to begin by briefly going through the key players within the payment ecosystem - Marqeta's ( MQ ) Annual Report does a good job of illustrating the legacy payments industry in a single chart:

{kind=link}

In a cashless transaction, seven parties are typically involved:

- Cardholder : The consumer visits a merchant's website or offline store and uses a physical, digital, or virtual payment card to perform a transaction - that's me and you.

- Merchant : The business receives payment for providing goods or services to the paying cardholder - think NIKE ( NKE ), Costco ( COST ), or your local gyms.

- Issuing Bank : To make purchases, the consumer needs to open a bank account with an issuing bank, which consequently issues a credit, debit, or prepaid card to the consumer. Issuing banks include JPMorgan Chase ( JPM ) and Citibank ( C ).

- Acquiring Bank : To hold funds and receive payments from consumers, merchants need to open an account with an acquiring bank. Do note that the same bank that issues cards to consumers can also act as the acquiring bank for merchants.

- Issuer Processor : To authorize and settle transactions, the issuing bank needs to partner with an issuer processor, which also connects the issuing bank with the card networks. Marqeta is a good example.

- Acquirer Processor : Similar to issuer processors, acquirer processors also authorize and settle transactions for merchants. They also connect merchants with the card networks. Payment gateways such as PayPal ( PYPL ), Apple Pay ( AAPL ), or Stripe may also be involved to facilitate these transactions.

- Card Network : This is the payment rail that provides the infrastructure for the flow of settlement and card payment information, which is apparent in all card transactions. Card networks such as Visa ( V ) and Mastercard ( MA ) act as the bridge between issuer processors and acquirer processors.

With that out of the way, let's talk about what Adyen does as a business.

Adyen was founded in 2006 in Amsterdam, Netherlands, by Pieter van der Does and Arnout Schuijff. Previously, the two co-founders launched a payments company called Bibit which was ultimately sold to the Royal Bank of Scotland.

The name Adyen means 'start again'... which was what they did after selling Bibit.

In a nutshell, Adyen is a global payment processor that provides an end-to-end platform for merchants to accept a variety of payment methods across e-commerce, mobile, and point-of-sale ((POS)) applications.

As you already know, the payment ecosystem involves many different players, and traditionally, merchants need to establish relationships with a list of different companies in order to fulfill their processing needs. This complexity gave rise to many issues, including:

- Uncertain processing fees

- Inconsistent reporting

- Poor consumer experience

- Lack of scalability

- Rejected payments

Adyen solves these issues by offering a single, modern, simple platform for merchants to accept payments.

Adyen FY2020 Capital Markets Day Presentation

{kind=link}

As shown above, by partnering with Adyen, merchants enjoy a full suite of payment solutions that cover the entire spectrum of the payments ecosystem, including both the issuing and acquiring side of the payment ecosystem. In addition, Adyen integrates the full payments stack with a single back-end infrastructure.

As of this writing, Adyen offers three commercial pillars: 1) Digital, 2) Unified Commerce, and 3) Platforms.

Digital

The Digital pillar is Adyen's bread and butter - the company was initially formed to modernize the payment processing experience in the e-commerce sector.

With Adyen, merchants can accept payments online, including every payment method you can think of:

- Debit and credit cards

- Bank transfers

- Digital wallets such as Apple Pay, PayPal, and Cash App ( SQ )

- Buy now, pay later such as Affirm ( AFRM ) and Klarna

- Vouchers, prepaid cards, and gift cards

Adyen Website

Pricing is very transparent - Adyen charges a flat processing fee of about €0.11 per transaction, plus a percentage of the transaction volume or fixed fee based on the payment method used. You can see the full price list here .

{kind=link}

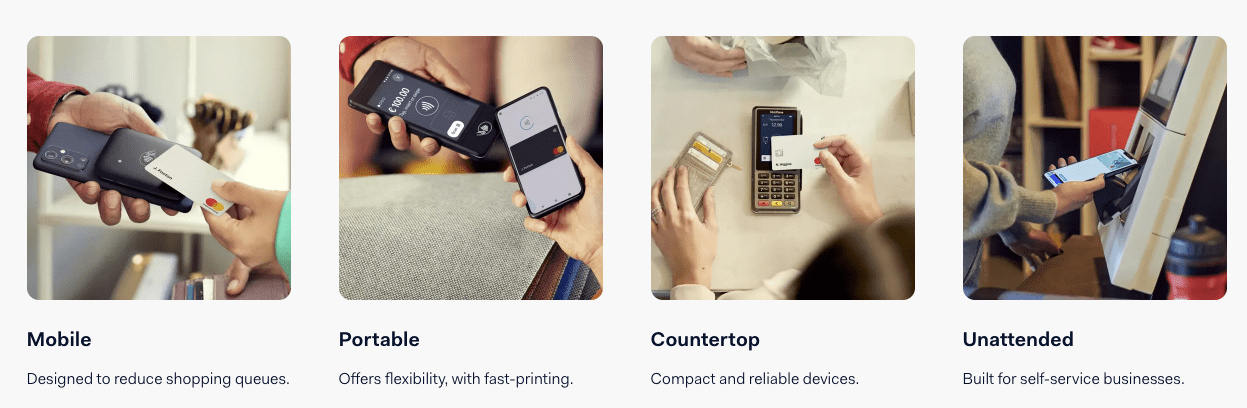

Unified Commerce

Adyen also offers a wide range of in-person POS solutions which vary in terms of size, connectivity, and payment experience.

{kind=link}

Adyen's Digital and POS solutions, together, form its Unified Commerce offering, which consequently collects online and offline payment data into a single platform.

Some examples of Unified Commerce in action include:

- Order in-app, collect in person

- Self-scan and pay

- Buy online, return in store

- Buy in-store, ship to home

- Pay with a QR code

- Pay via a self-service kiosk

While alternative solutions can provide similar offerings, their systems are usually siloed, which means that merchants do not get valuable cross-channel insights.

In other words, Adyen is able to support these omnichannel experiences within the same system, made possible through its vertically integrated technology stack.

Platforms

Launched in 2016, Adyen for Platforms allows merchants to embed financial products into their platforms or marketplaces.

Adyen primarily focuses on large enterprises as their merchants and some of them operate as a platform/marketplace, which subsequently has a large network of smaller merchants under their platforms. Fundamentally, Platforms serves as a gateway to distribute enterprise-quality financial products to small and medium businesses (SMBs).

In essence, Adyen for Platforms is a banking-as-a-service offering for platforms and marketplaces, which includes the following features:

- Payments : Allows SMBs to make payments a part of their product offering.

- Accounts : Enables SMBs and users to open a business account and digital wallet, respectively, which enables them to manage their finances in the same platform where they do business.

- Issuing : Enables platforms to issue virtual or physical cards to their users. This creates an additional revenue stream for platforms as they receive a revenue share of the interchange fee whenever a platform user transacts using the cards issued.

- Capital : Enables platforms to provide users quick access to business financing to grow their businesses.

- Payouts : Enables platforms to send payouts to their sellers, creators, suppliers, vendors, and staff in real-time, 24/7.

Adyen FY2022 Capital Markets Day Presentation

{kind=link}

In short, these three commercial pillars combined make Adyen the one-stop shop for modern-day payment processing. The company offers other value-added services such as risk management, fraud prevention, and marketing tools, but these three pillars form Adyen's core value proposition.

Put simply, Adyen's end-to-end payment capabilities within the payment ecosystem make it the financial technology platform of choice for leading businesses all over the world.

Moats

Based on my research and analysis, I identified four competitive moats for Adyen: technology, network effects, switching cost, and cost advantages.

Technology

Adyen's platform is built in-house and is one of the most vertically integrated payment platforms out there. Its simple, all-in-one technology stack is a major reason why leading global brands choose Adyen to be their sole payment processor. Just look at some of their customers:

{kind=link}

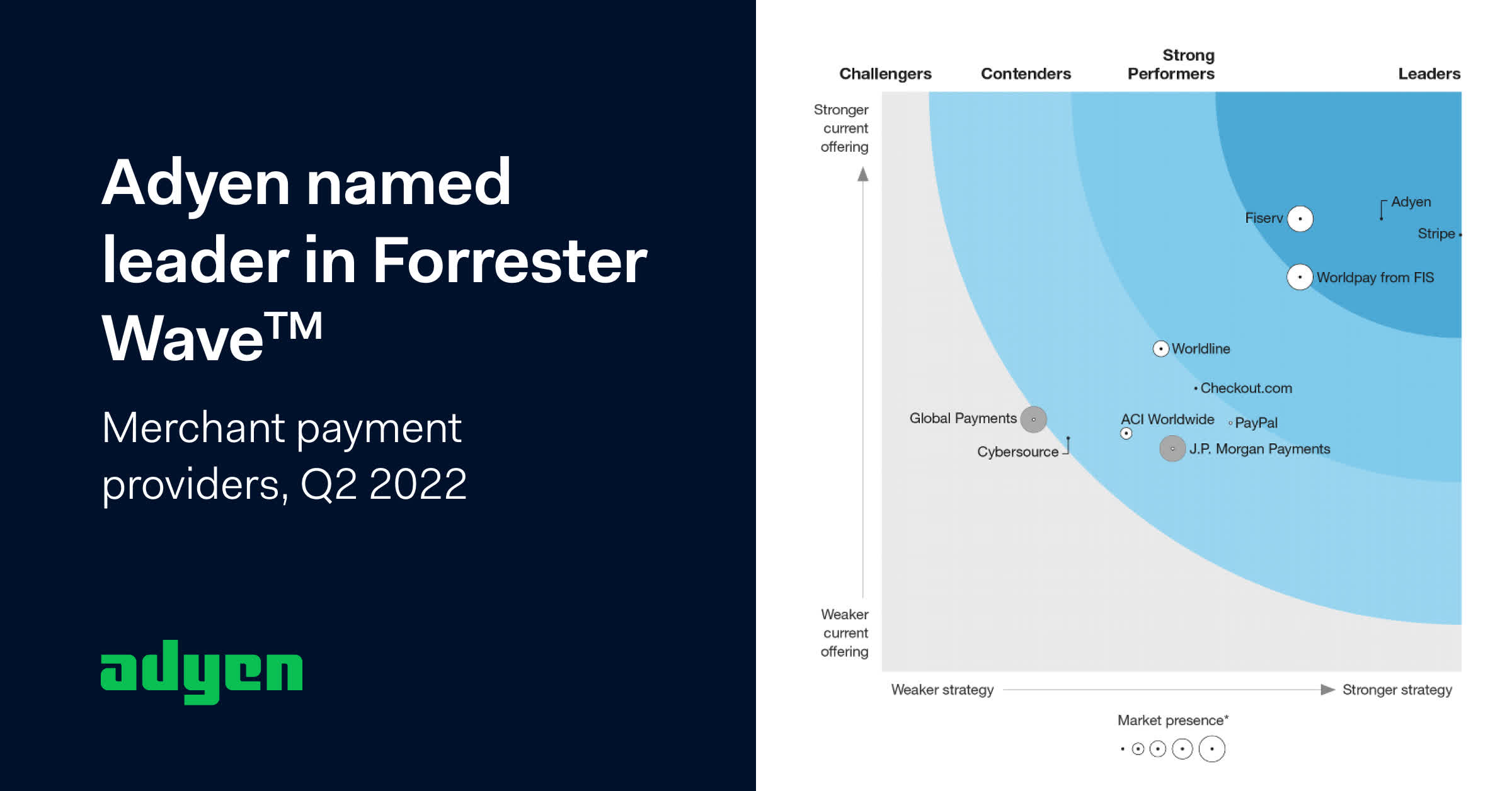

Adyen is also recognized as the undisputed leader in the 2022 Forrester Wave: Merchant Payment Provider report, ahead of competitors such as Stripe, Worldpay, and Fiserv.

{kind=link}

In addition, The Strawhecker Group recognizes Adyen as the Leading Payment Gateway with API .

TSG

In short, Adyen's high-quality clientele base as well as recognition from industry analysts, are testaments to the company's best-in-class technology platform.

Network Effects

Because of Adyen's partnership with large enterprises, Adyen enjoys powerful network effects - as these enterprises grow, Adyen grows as well.

Network effects are especially prevalent with Adyen for Platforms, where enterprises embed Adyen's financial technology into their existing software.

Partnering with platforms simultaneously opens the door to an interesting customer demographic: the SMBs they host. Through our platform customers, we are naturally moving from the enterprise level down to the long tail of the market, which is rapidly digitizing.

For context, here are some metrics among Adyen's platform customers:

- Facebook ( META ): 3.03B Monthly Active Users

- Spotify ( SPOT ): 551M Monthly Active Users

- Uber ( UBER ): 137M Monthly Active Platform Consumers

- Shopify ( SHOP ): 1.75M Merchants

- Etsy ( ETSY ): 8.3M Active Sellers and 96.3M Active Buyers

As you can see, these are not small figures, and as these platforms add additional users or SMBs to their business, payment activity naturally rises as well, which bodes well for Adyen.

It's also important to note that Adyen accepts 91 different payment methods (yes, I counted) and its platform is integrated with 119 partners such as Salesforce ( CRM ), SAP ( SAP ), and Microsoft ( MSFT ), which means Adyen's back-end technology is pretty much ubiquitous.

Switching Costs

Adyen provides the essential payment infrastructure for enterprises to do business. The company employs a land-and-expand strategy, focusing first on providing digital payment processing for enterprises. As these customers gain more confidence and trust during the testing phase, they begin to roll out Adyen's offerings across their entire businesses, which can be deployed seamlessly since Adyen has the technology, scalability, and connectivity.

Once customers fully commit to Adyen's platform, it would be very difficult for them to switch to an alternative provider, which may involve: 1) operational suspension, 2) a steep learning curve, and 3) feature downgrades.

This reflects high switching costs for customers, and this is evident from Adyen's low volume churn of less than 1%.

Cost Advantages

Since its inception, Adyen has built a full payment stack from the ground up, with zero acquisitions. The result is a high-quality, vertically integrated platform, and because of its relentless commitment to building the best payments platform possible, management doesn't shy away from charging higher prices than its competitors.

Even in the midst of competitive pressures in the North American market, management refuses to sell themselves short and join the price war:

So if you look at our strategy in the U.S., it is to roll out all products: platform, unified commerce and also digital. Our strategy is to invest in the product. We think that cost of ownership is very important, and we think that is the lowest with our product. We could -- I mean, we run a single platform. We run at the lowest cost. So we could join a price fight. We don't think that's the right strategy.

(Co-CEO Pieter van der Does - Adyen FY2023 H1 Earnings Call )

Management is confident that they have the best financial product out there and if customers want quality, they would have to pay more for it. There's no compromise and I think that's the right (and bold) strategy moving forward.

Even so, as a tech-enabled payment processor, Adyen has the highest EBITDA Margin among peers, at about 55% in FY2022 (Margins are under pressure lately but that's because Adyen is on a hiring spree. More on that later.)

Below are the EBITDA Margins of some of Adyen's competitors and as you can see, Adyen reigns supreme in terms of profitability. More importantly, Adyen can afford to cut prices - but they chose not to. Instead, Adyen will use its profits to reinvest in the business to improve its platform.

Ultimately, Adyen is not in the commodity business - the company strives to deliver a premium product.

Growth

Let's now dig into the financials. Keep in mind that Adyen reports bi-annually, rather than quarterly.

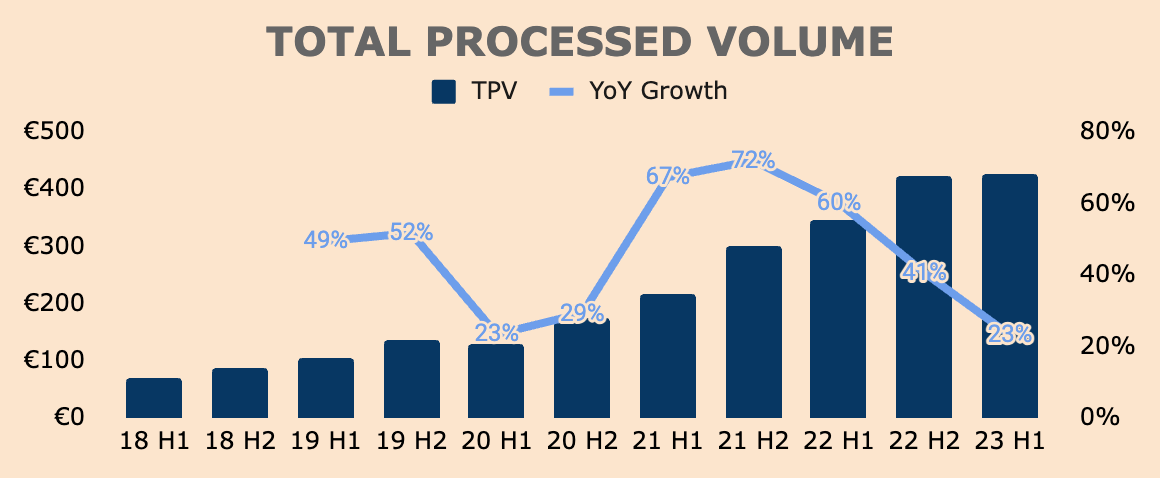

That said, Total Processed Volume, or TPV, was €426B in H1, which is up 23% YoY.

Growth in TPV was primarily due to the company's land-and-expand strategy, whereby existing customers drove more than 80% of the company's growth. Such a high contribution from existing customers was, again, due to the company's high switching cost moat, as exemplified by its ultra-low volume churn of less than 1% - this trend has been consistent since the company went public in 2018.

Nevertheless, growth has been slowing down - we can assume that years of growth have been pulled forward due to the pandemic and now, Adyen is facing tough YoY comps as the company grows over a larger base. Still, the steep deceleration in H1 is a major concern for investors as it questions the overall growth story of the business.

{kind=link}

Having said that, we can see how TPV is broken down by its three commercial pillars.

{kind=link}

As it stands, Digital volumes remain the bulk of the company's TPV, at 63% of TPV. Digital Processed Volume was €267B in H1, which is up by 23% YoY. The slowdown in the segment was due to price competition in the North American market:

First, as a natural consequence of the shifting economic climate - driven by higher inflation and interest rates - profit outweighed growth for many North American digital businesses in H1. Enterprise businesses prioritized cost optimization , while competition for digital volumes in the region provided savings over functionality. These dynamics are not new, and online volumes are easiest to transition back and forth. Amid these developments, we consciously continued to price for the value we bring.

(Adyen FY2023 H1 Shareholder Letter)

Unified Commerce is faring better, with a Processed Volume of €109B in H1, which is up 36% YoY. This segment represents 26% of TPV, and most of its growth was due to robust growth in POS Processed Volume, which grew 49% YoY, to €62B in H1. Retail is clearly not dead, which is why Adyen is capitalizing on the growth of multi-channel experiences.

Finally, Platforms Processed Volume was €50B in H1, which only grew 3% YoY, making up only 12% of TPV. The chronic slowdown in this segment was due to eBay ( EBAY ) which accounts for the majority of volumes in the Platforms pillar - for context, eBay's Gross Merchandise Volume dropped 2% YoY in Q2. Excluding eBay, Platforms would have grown 82% YoY, which is remarkable.

Moving on, Adyen generates the majority of its Revenue from settling and processing payments, which correlates with TPV.

- Settlement Fees are paid by merchants, which include interchange fees, payment network fees, and other costs incurred from financial institutions. Settlement Fees are usually a percentage of the transaction volume.

- Processing Fees are paid by merchants as well, basically for using Adyen's platform to process payments. Processing Fees are fixed per transaction, regardless of the transaction value.

The company also sells POS terminals as well as other value-added services (such as foreign exchange fees and card issuing services), but they make a tiny portion of Revenue.

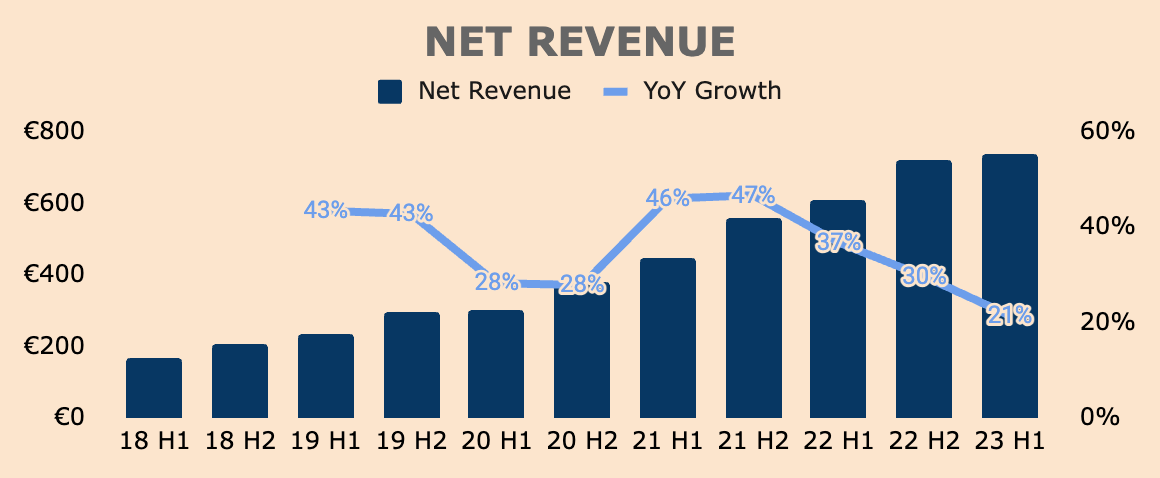

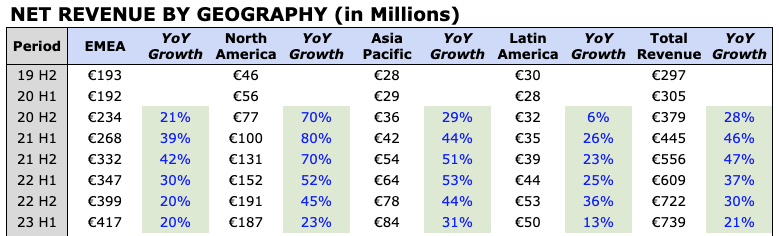

As you can see, Net Revenue has been slowing down as well, which was €739M in H1, up 21% YoY.

{kind=link}

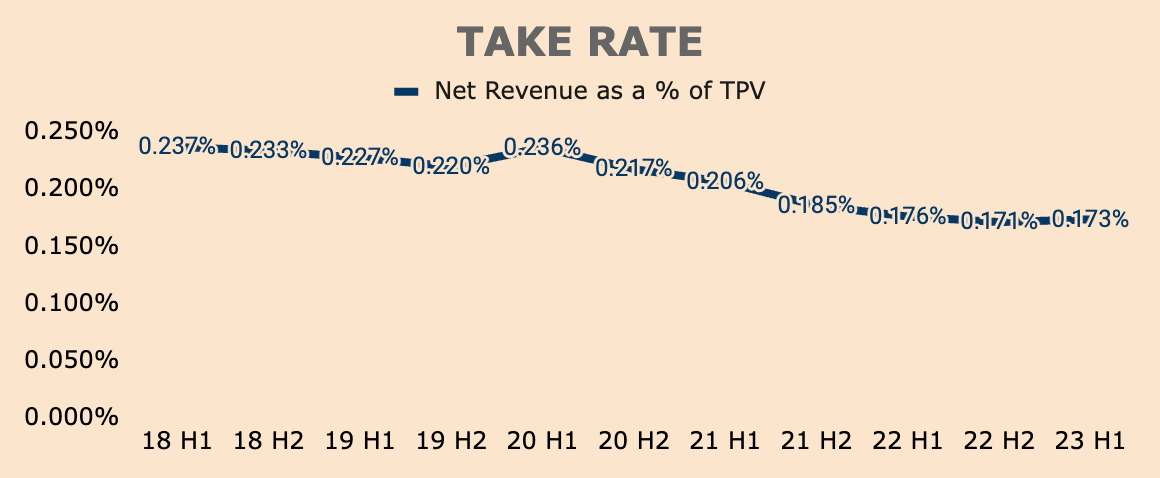

As you may have noticed, Net Revenue growth (21%) is slower than TPV growth (23%), and this is due to lower Take Rates as a result of existing customers growing within Adyen's platform. In other words, as these customers generate more volume, they get a lower price per transaction as Adyen's contract with these customers typically contain volume tier incentives.

{kind=link}

That said, there were two other factors that pressured Take Rates:

One of the big reasons that Take Rate was declining in the past was that the average transaction value is going up and the full stack percentage was going down .

(CFO Ethan Tandowsky - Adyen FY2023 H1 Earnings Call)

For the first reason, remember that Adyen charges a fixed Processing Fee of about €0.11 per transaction. All else equal, if average transaction values increase, Adyen collects lower gross Processing Fees.

For the second reason, Take Rates declined due to travel volumes rebounding - Adyen only provides processing services for customers in the travel industry, not the full payment stack. Fortunately, the travel industry has stabilized, which is why Take Rates have stabilized as well.

As you can see in the chart above, Take Rates were 0.173% in H1, which is a slight improvement from H2 last year. However, Take Rates today are still lower than H1 last year, which was 0.176%.

While declining Take Rates may look unfavorable from the surface, it's actually a good thing as it means that Adyen is growing with its customers, which, at the end of the day, is what Adyen wants.

Nonetheless, you can see how Net Revenue is broken down by geography.

As mentioned earlier, the deceleration was primarily due to price competition in North America, which was previously its fastest-growing market. In H1, North America Net Revenue was €187M, up 23% YoY but down QoQ and a steep deceleration from last year's H1 and H2 growth of 52% and 45%, respectively.

Fortunately, this seems to be an "isolated phenomenon" as mentioned by management during the earnings call.

{kind=link}

Another reason for the slowdown in growth in North America - and the rest of the world for that matter - was due to the fact that the company was slow to grow its team, which limited operational expansion:

We now see the impact of a sales team size that did not match our ambitions , particularly in North America. Since then, we have ramped up our investments. That being said, investments in the team and revenue never move simultaneously. Rather, the former drives the latter over time .

(Adyen FY2023 H1 Shareholder Letter)

That said, Adyen has been on a hiring spree lately, which should start to materialize and contribute to topline growth over the next few years.

Regardless, I still see massive growth potential for Adyen as the company positions itself as one of, if not, the best payments stack in the emerging fintech industry. At the same time, Adyen has a high-quality client base and volume churn is basically non-existent, which speaks volumes about its platform.

In addition, I admire management's decision to stand their ground and not surrender to price cutting, which could lead to an endless cycle of price undercutting. I think this strategy reflects strength within the business, confidence among management, and differentiation in the platform.

Profitability

Adyen has a highly profitable business model.

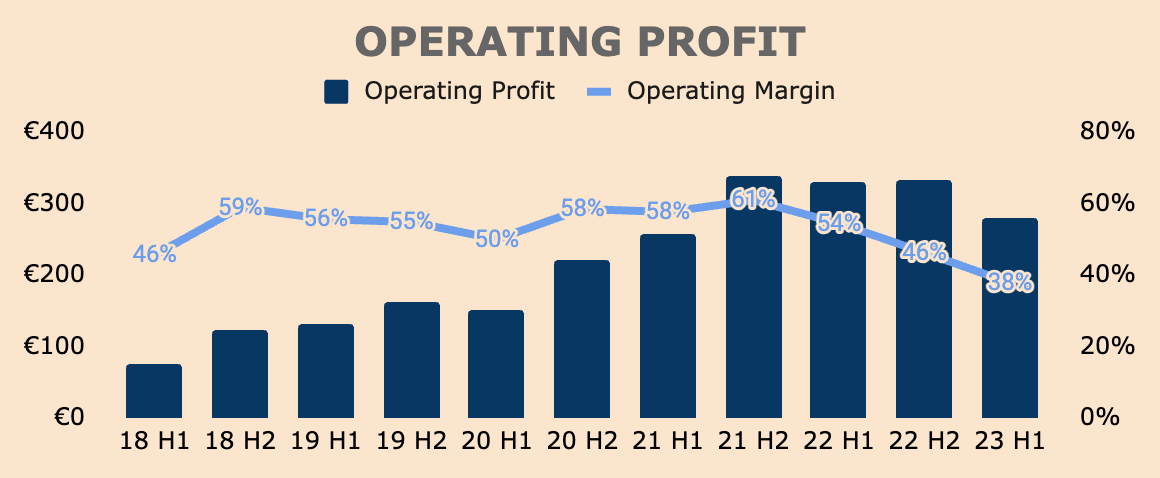

Operating Profit (excluding Net Finance Income) was €279M in H1, representing an Operating Margin of 38%. However, you can see that Operating Margin is in a downtrend, and this is due to aggressive hiring in the past two years as the company prepares for the next stage of growth.

{kind=link}

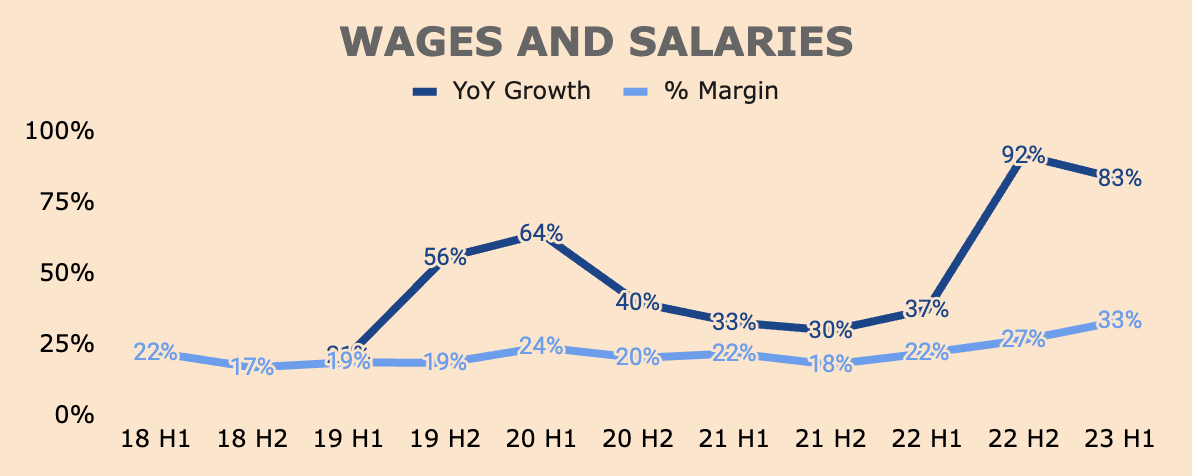

While other tech companies undergo rounds of layoffs, Adyen goes into expansion mode, and this is reflected in the company's recent surge in Wages and Salaries, which significantly outpaced overall business growth. As you can see, Wages and Salaries grew by 83% in H1, which accounted for 33% of Net Revenue.

{kind=link}

The company added 551 FTE in H1, bringing the total to 3,883 FTE, which is a 17% increase from H2. That is a lot of hiring, but this should moderate heading into 2024. Consequently, we should see Operating Margins improve as the company regains operating leverage.

We foresee our team reaching its next level of maturity at the start of 2024 with a mix of both commercial and tech roles. After this point, we will phase out of our accelerated investment mode and hire as needed.

(Adyen FY2023 H1 Shareholder Letter)

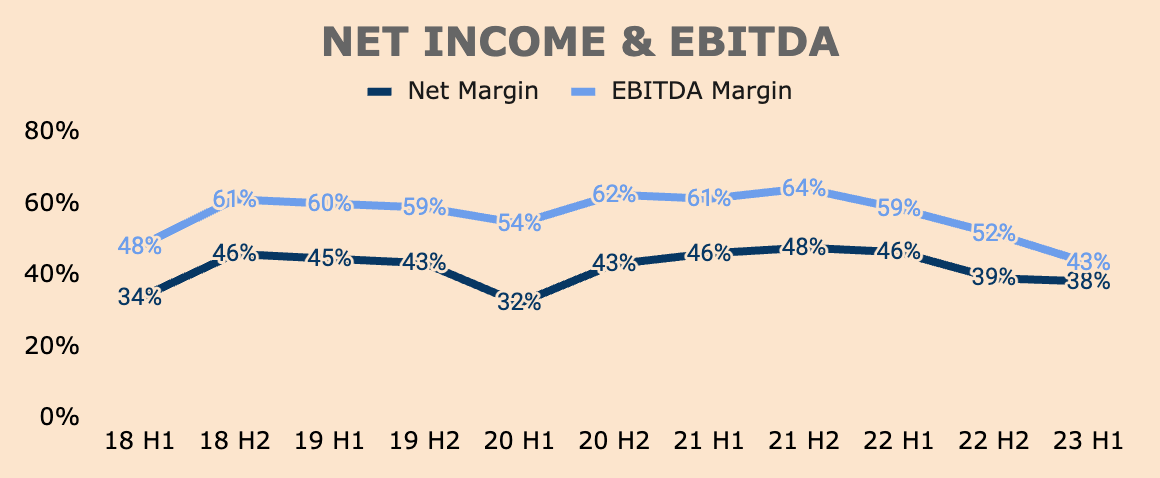

Despite all the hiring, Adyen still maintains strong bottom-line numbers in H1:

- Net Income of €282M (38% Net Margin)

- EBITDA of €320M (43% EBITDA Margin)

{kind=link}

Sure, margins are not as high as they were, but the company is reinvesting for growth by expanding its team and improving the platform, which should pay off in the long run.

Instead of turning cautious like peers and instead of optimizing profitability for the sake of satisfying shareholders in the short term, Adyen chose to continue to build, build, and build. Put simply, Adyen is just a different breed.

It is also important to note that the short-term impact of accelerated hiring is temporary and that margins should improve in 2024 and beyond.

That said, Adyen is a highly profitable business with high earnings potential, and when the company regains operating leverage, it should supercharge shareholder value once again.

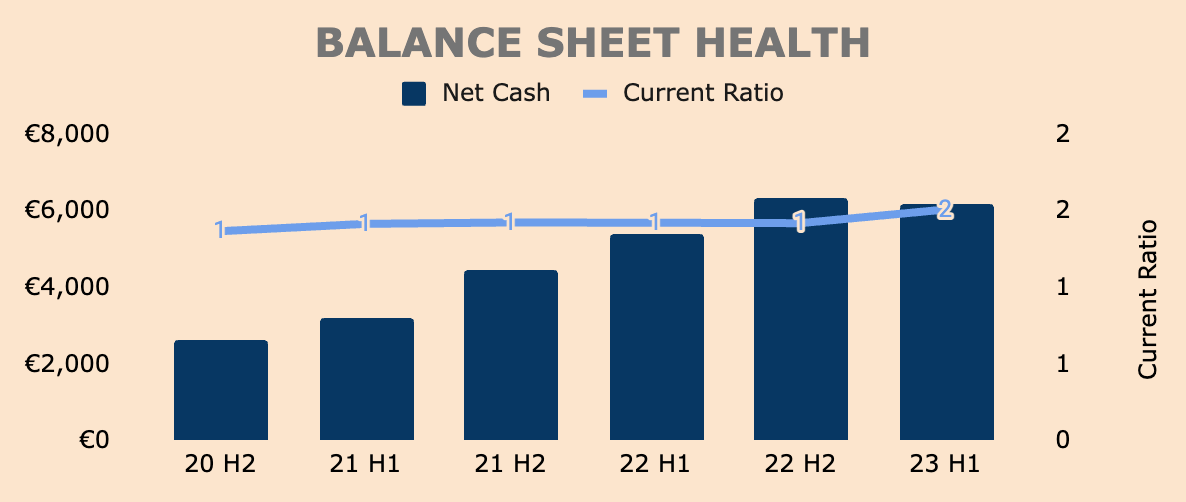

Financial Health

Adyen has a fortress balance sheet. The company has €6.4B in Cash and Short-term Investments, with €0.2B of Total Debt (mostly in the form of Operating Lease Liabilities), which puts its Net Cash position to be about €6.2B. This means that Net Cash represents more than 25% of its market cap of €24B.

{kind=link}

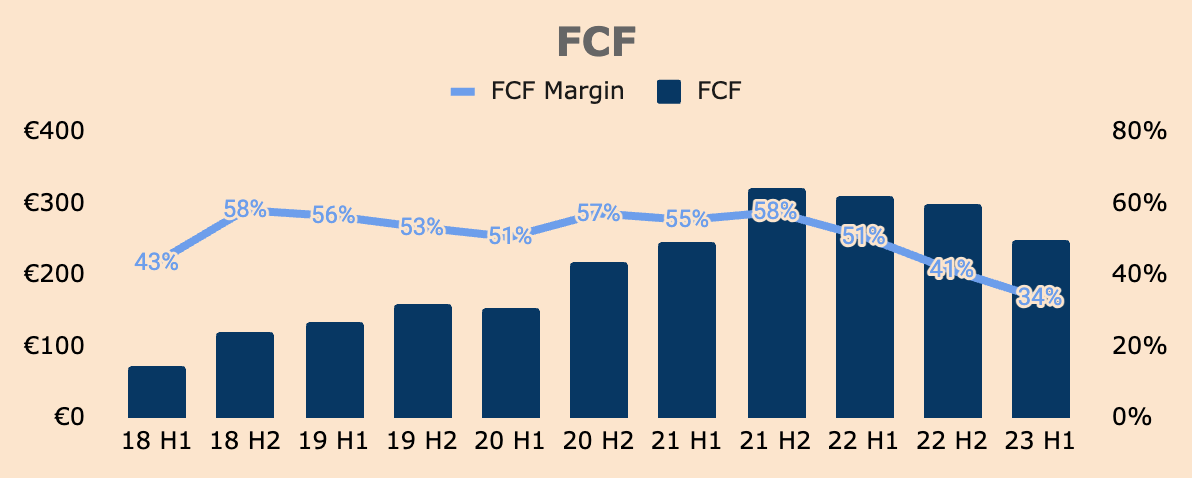

Adyen is not just highly profitable - it is also a cash-generating machine.

In H1, Adyen generated a Free Cash Flow of €248M at a FCF Margin of 34%. Adyen has historically produced high Free Cash Flow Margins of over 50%, but we can see that FCF Margins are falling, due to:

- Accelerated hiring

- Front-loaded CapEx for infrastructure investments, which was 7.6% of Net Revenue in H1

Again, the company is investing heavily for future growth.

{kind=link}

Adyen is super capital efficient as well, with an ROIC of more than 20% over the last few years. Although not as high as DLocal ( DLO ), Adyen's ROIC is still higher than most fintech peers such as PayPal and Block.

High ROIC is a trait of long-term compounders and given its consistent track record of high ROIC, I don't mind Adyen splurging some capital in the short term to fuel long-term growth.

Outlook

In terms of outlook, management sees no change in their long-term financial objectives:

- Net Revenue growth between the mid-twenties and low-thirties in the medium term. Given the recent investments the company made recently, I won't be surprised if growth reaccelerates in 2024.

- Long-term EBITDA Margin of more than 65%. Once hiring slows down, the company should regain operating leverage, with EBITDA Margins returning above 60%.

- Sustained CapEx level of up to 5% of Net Revenue. Adyen has a capital-light business model so I don't see CapEx exceeding 5% for long periods of time.

Whatever it is, Adyen still has a long growth runway ahead as the leader in modern payment processing.

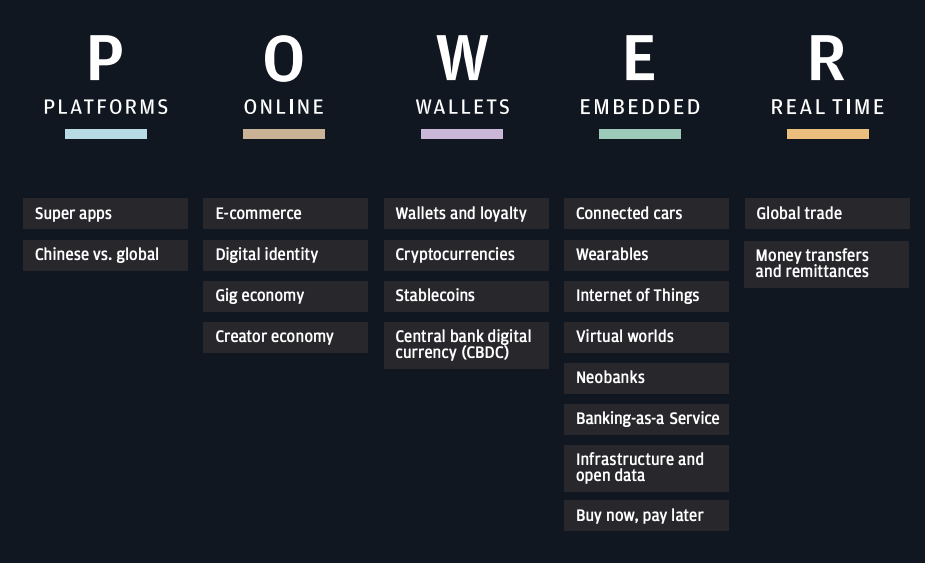

According to JP Morgan, approximately $54T of payment volumes flow through five mega-themes: Platforms, Online, Wallets, Embedded, and Real Time. With a TPV of $848B in the last twelve months, Adyen has roughly ~1.6% market share. In other words, Adyen has massive growth opportunities ahead.

{kind=link}

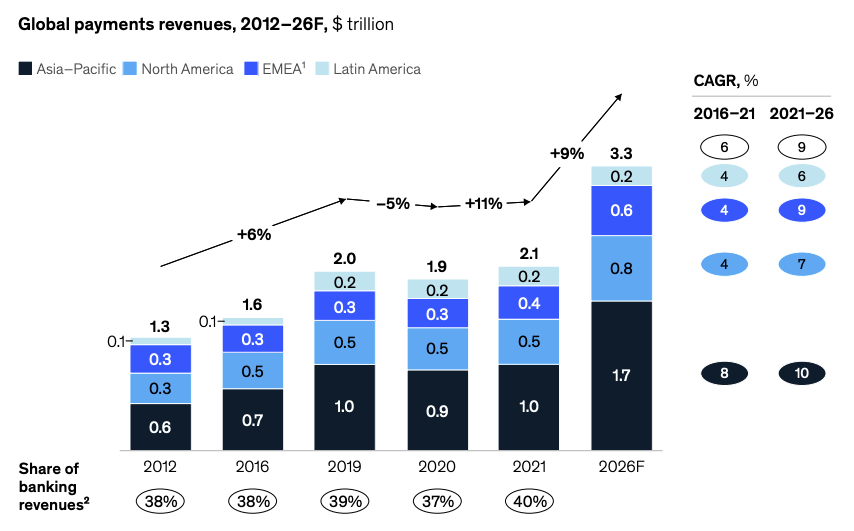

All that volume could translate to $3.3T of Global Payments Revenues by 2026.

{kind=link}

I am particularly excited about Adyen for Platforms as enterprises are only beginning to see the benefits of embedding financial products on their platforms. According to EY, embedded finance adoption will grow exponentially over the next few years.

Embedded finance covers many domains, but payments is the largest game in town in terms of revenue. According to our research, the volume of payments through embedded channels reached US$2.5T in 2021 and is expected to reach US$6.5T by 2025 .

(EY - How banks are staking a claim in the embedded finance ecosystem )

As you can tell, Adyen is still in its early stages. Management knows this - and that's why they're investing heavily to capture the massive payments industry.

Valuation

The problem with investing in Adyen stock was that the stock was incredibly expensive. As you can see, Adyen has been trading at an EV to EBITDA multiple of more than 50x ever since the company went public, with a peak multiple of almost 200x. Put another way, Adyen was trading at nosebleed valuations.

The keyword here is 'was'.

As you may know, the stock plunged by ~40% following H1 results, due to pricing competition, slowing growth, and falling margins. This selloff suddenly made the stock much more reasonably valued, now trading at just 22x its EBITDA.

It's not dirt cheap, but it's an attractive valuation multiple given the high-growth, high-quality, high-profitability business model that Adyen flexes.

So, on a historical basis, Adyen has never traded this cheap before.

Now let's compare its valuation to its closest competitor: Stripe.

Back in March this year, Stripe raised over $6.5B at a valuation of $50B .

According to its annual report , Stripe's TPV in 2022 was $817B, which was up 26% YoY.

On the other hand, Adyen's TPV in 2022 was €768 (~$832B), which was up 49% YoY.

With today's market cap of $26B, Adyen trades at half of Stripe's valuation, despite similar TPV as well as growing TPV nearly twice the pace of Stripe - let that sink in.

So, compared to Stripe, Adyen is attractively valued.

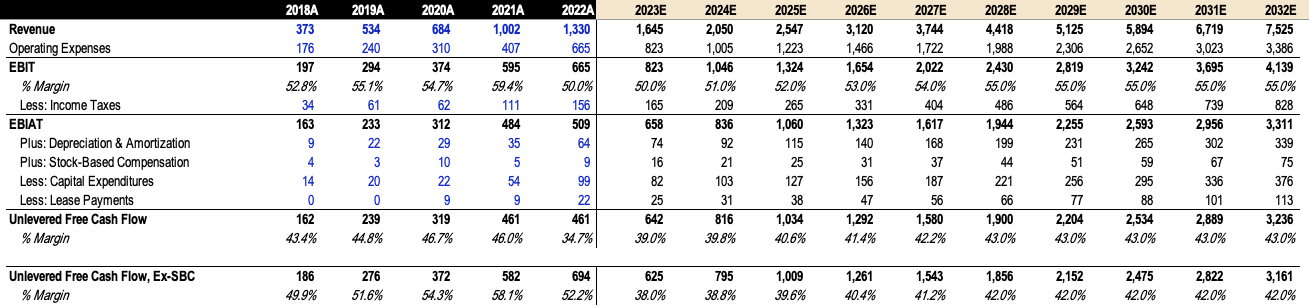

Now let's take a look at my DCF model. Keep in mind that Adyen calculates FCF by taking EBITDA minus CapEx and Lease Payments (instead of the traditional formula, Cash Flow from Operations minus CapEx). As for me, I will use Adyen's FCF calculation method, subtracting Income Tax as well.

That said, here are my key assumptions:

- Revenue Growth : I will follow analyst estimates for the first three years and then drop growth rates gradually, to just 12% by 2032.

- CapEx : Set at 5% of Revenue as guided by management.

- FCF Margin : Management guided a long-term EBITDA Margin of 65%. Take that figure and minus CapEx, we get an FCF Margin of roughly 60%. Minus a 20% Income Tax, I'm projecting a long-term FCF Margin of about 43%.

{kind=link}

Based on these assumptions, I project a €7.5B Revenue by 2032 at an FCF Margin of 43%.

{kind=link}

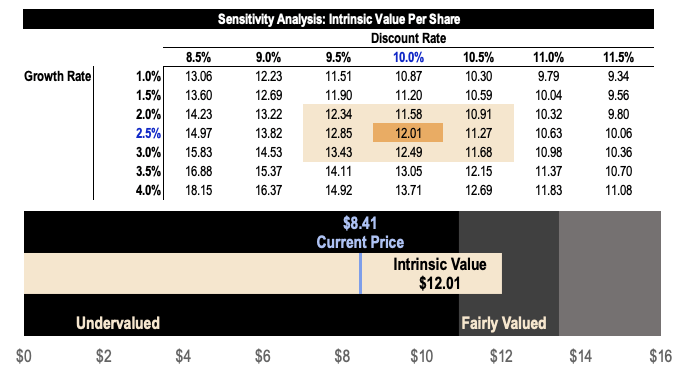

Using a perpetual growth rate of 2.5% and a discount rate of 10.0%, I arrive at a fair value estimate of $12 per share for Adyen, assuming a $1.08 EUR/USD currency conversion rate.

{kind=link}

Based on the current price of $8.41, this represents an upside potential of about 43%. As such, I believe Adyen is undervalued at the moment.

It's important to look at Adyen's stock price with some context as well: In the last three years, Adyen grew EBITDA and Net Income by ~100% while its stock price collapsed by 64%.

Before H1 earnings results, Adyen was priced to perfection. Today, Adyen is priced for disaster.

The best time to buy a stock is when there's an overreaction to the downside - we just saw a ridiculous selloff, and I believe this presents an excellent buying opportunity.

Risks

Competition

As highlighted by management, Adyen experienced price competition in North America - PayPal and Stripe are prime suspects.

- PayPal : The fintech pioneer, although popular for its PayPal-branded checkout buttons, also has Braintree, which is its unbranded payment processing business. In Q1 and Q2, PayPal grew unbranded checkout by 30% in both quarters, which outpaced Adyen's H1 TPV growth of 23%. You can read my recent analysis on PayPal here .

- Stripe : Although Stripe grew slower than Adyen in 2022, we can't completely ignore the company's innovative platform. As you can see, Stripe offers more products and services than Adyen, which some companies might prefer.

{kind=link}

Not only that, but Adyen also faces competition from legacy processors like Fiserv, modern issuer processors like Marqeta, and even POS solutions like Square.

If growth continues to slow down, it may be a sign of intense competition, which may force Adyen to cut prices - the markets will not like that.

Overhiring

As discussed earlier, Adyen is expanding its team at a breakneck pace, which could lead to overhiring that puts unnecessary pressure on margins and profitability. At the same time, new hires may not fit well with the company's culture, which may give rise to internal conflict.

That said, I won't rule out the possibility of company layoffs.

Long-term Financial Objectives

This risk is directly tied to the first two risks: if the issues of competition and overhiring intensify, we may not see the company deliver its financial objectives, which can lead to a loss of confidence among investors.

Or worse, management could drop their long-term targets, and that may cause yet another selloff.

Thesis

To wrap up, Adyen is the leading payments platform with technology, network effects, switching costs, and cost advantage moats. As such, the company is well-positioned to be the front-runner in the fintech revolution for years to come.

The company has robust growth potential, high profitability, and a strong balance sheet, which should protect the company from temporary headwinds such as price competition and a worsening macro environment.

In addition, the 40% price plunge following H1 earnings results presents a wide margin of safety and an attractive entry point for investors.

Adyen has always traded at insanely expensive valuations ever since it went public in 2018. That is no longer the case today, thanks to the market's drunken behavior.

Take advantage of this panic - this gift.

Adyen is a fintech diamond in the rough.

For further details see:

Adyen: A Fintech Diamond In The Rough