ADYEY - Adyen: Another Fintech Company That Is Undervalued

2023-10-04 07:13:46 ET

Summary

- Adyen is another fintech stock that declined 80% from its previous all-time high and seems like a bargain.

- The company is without a doubt a great business reporting high growth and high profitability metrics and we are still dealing with a founder-led business.

- In order for the stock to be undervalued at this point, Adyen has to grow its bottom line by at least 15% in the next ten years.

- Considering managements' assumptions and the expected growth rates for the overall market, such growth rates could be seen as realistic.

In the last few years, I covered PayPal Holdings, Inc. ( PYPL ) on a regular basis and saw the company as one of the major bargains currently existing in the market. PayPal was clearly overvalued a few years ago, but the stock declined about 80% since its previous all-time high.

And PayPal is not the only company that declined rather steeply in the last few quarters. Another fintech company that saw its stock price decline about 80% is the European payment company Adyen N.V. ( ADYEY ) ( ADYYF ). And in the following article we will take a closer look at Adyen and try to answer the question if we are dealing with a great business and a great investment.

Company Overview

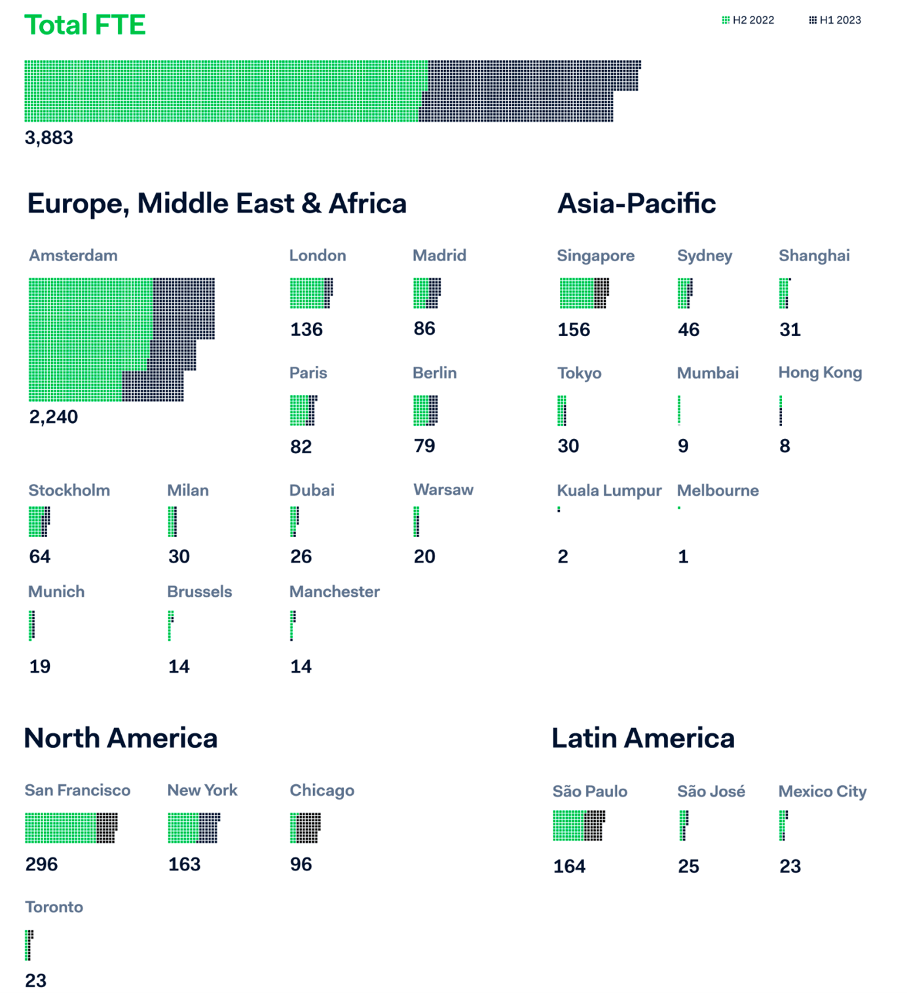

Adyen is a Dutch payment company that was founded in 2006 by Peter van der Does and Arnout Schuijff. Adyen has the status of an acquiring bank which allows businesses to accept e-commerce, mobile and point-of-sales payments. The company operates a payment platform in Europe, North America, Africa, the Middle East, Latin America and the Asian-Pacific region and the platform integrates payments stack that includes everything from gateway, to processing, issuing, acquiring, and settlement services as well as risk management. The company which is headquartered in Amsterdam is employing about 3,900 people with offices all around the world and is generating a net revenue of €1,330 million in fiscal 2022 and is already highly profitable - despite being a rather young company. And in the last few years, Adyen has reported extremely high top-line growth and in fiscal 2022 revenue increased about 33% year-over-year. Among the biggest customers are companies like Uber Technologies, Inc. ( UBER ), eBay Inc. ( EBAY ), Booking Holdings Inc. ( BKNG ), McDonald's Corporation ( MCD ), Microsoft Corporation ( MSFT ), and LinkedIn.

Disappointing Results

We mentioned above that Adyen declined 80% from its previous all-time high but when considering a highly profitable business still growing its top line over 30% one might wonder why we saw the steep sell-off in the last few quarters.

{kind=link}

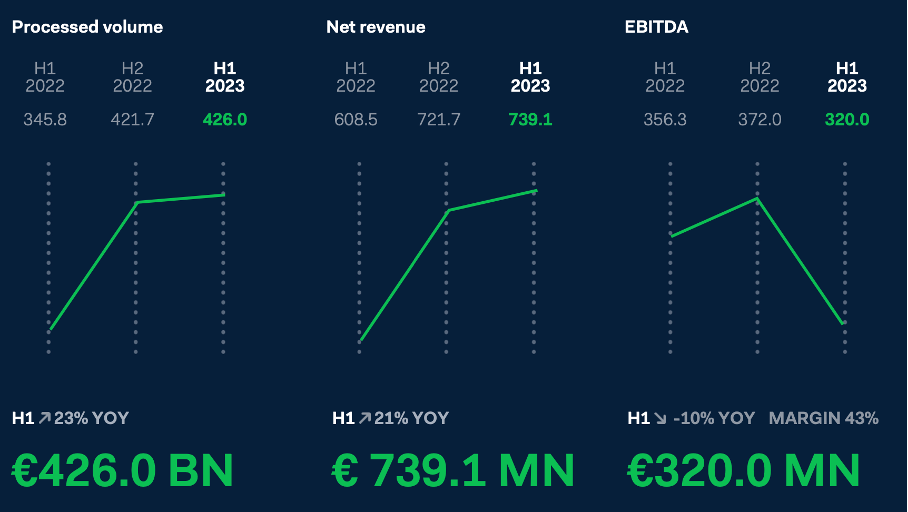

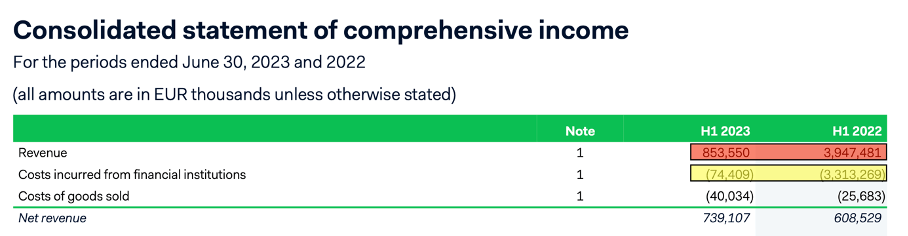

One reason was the results for the first half of fiscal 2023. At least investors were extremely disappointed, and the stock dropped almost 39% in a single day. When looking at the results for the first six months they were not so horrible. Net revenue increased 21.3% year-over-year from €609 million in H1/22 to €739 million in H1/23. Operating income declined from €331 million to €279 million - resulting in 15.7% YoY decline - and finally diluted earnings per share declined slightly from €9.09 to €9.07. The reason for earnings per share declining only slightly was the much higher "finance income." And finally, free cash flow declined from €309 million in H1/22 to €248 million in H1/23 - resulting in 19.7% YoY decline.

{kind=link}

The company is generating its revenue in four different categories:

- Settlement Fees : The biggest part of revenue is generated from settlement fees. In the first half of 2023, Adyen generated €486 million in revenue, but a year over year comparison doesn't make much sense for reasons I will explain in the next section.

- Processing Fees : €210 million in revenue is generated from processing fees and compared to the first half of 2022 the company could report 16.5% year-over-year growth.

- Sales of goods : In this segment, Adyen generated €41.2 million in revenue resulting in 46.2% year-over-year growth.

- Other services : In this segment Adyen generated €117.2 million in revenue resulting in 19.6% year-over-year growth.

Great Business

Adyen seems to be a great business. Although investors were disappointed by the growth rates Adyen could report in the first half of 2023, Adyen could grow revenue with a CAGR of 54.58% in the last five years, operating income with a CAGR of 48.07% and earnings per share with a CAGR of 50.85% in the same timeframe.

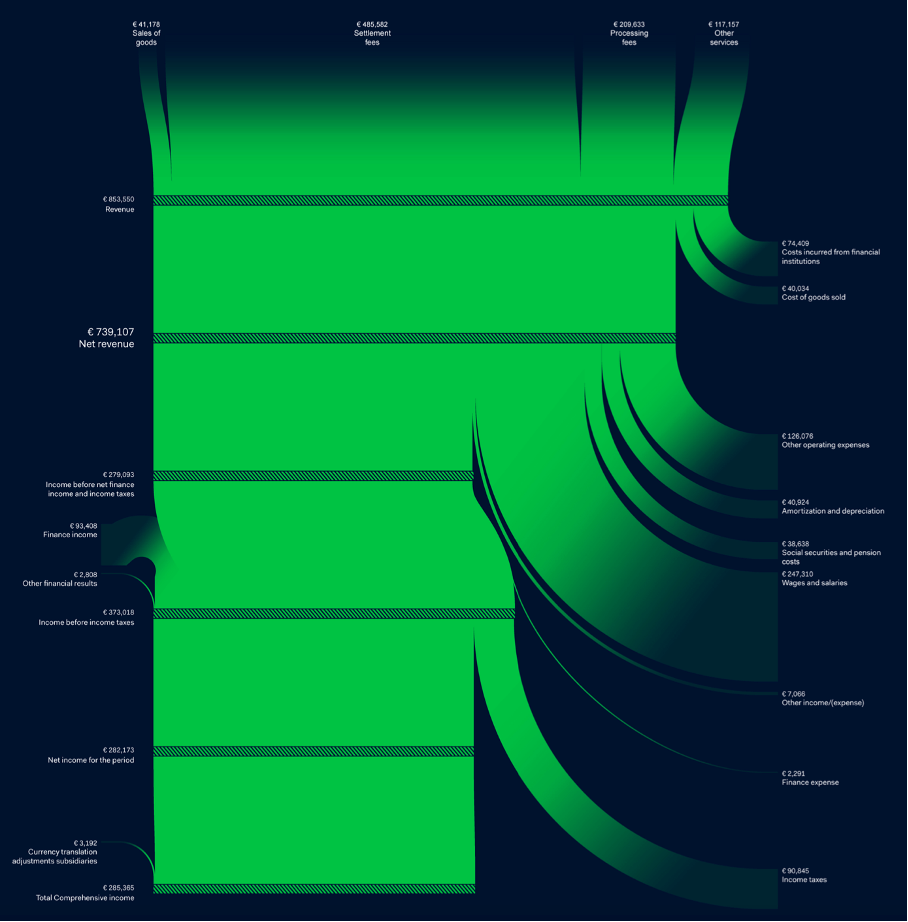

And while high growth rates are certainly great, we can find a lot of other businesses - mostly young companies - that are also growing with a high pace. What makes Adyen so special is the fact that we have a young business growing with a high pace but is already highly profitable. And when looking at the company's margins we can find different numbers. Adyen itself is reporting an adjusted EBITDA margin of 43% in H1/23 and 55% in fiscal 2022. Most financial sites - including Seeking Alpha - report very different and much lower margins. The reason is that these sites use revenue generated as basis and not "net revenue", which makes more sense.

{kind=link}

When looking at the last income statement we can see a huge decline in revenue (marked in red) but at the same time we can see a similar huge decline in "costs incurred from financial institutions". In its H1/23 report , Adyen explained:

In the current period, Adyen amended its terms and conditions applicable to merchant agreements in order to specify the responsibilities of the services provided by financial institutions and network scheme providers involved in the payment processing and acquiring services. The change in terms and conditions specifies the distinct services provided in the payment flow, clarifying that Adyen does not provide a significant service of integrating the services from third parties into one combined output for the merchant, nor does it control the inputs from third parties before services are provided to the merchant. As such, Adyen acts as agent for the pass-through settlement fees prospectively from January 1, 2023.

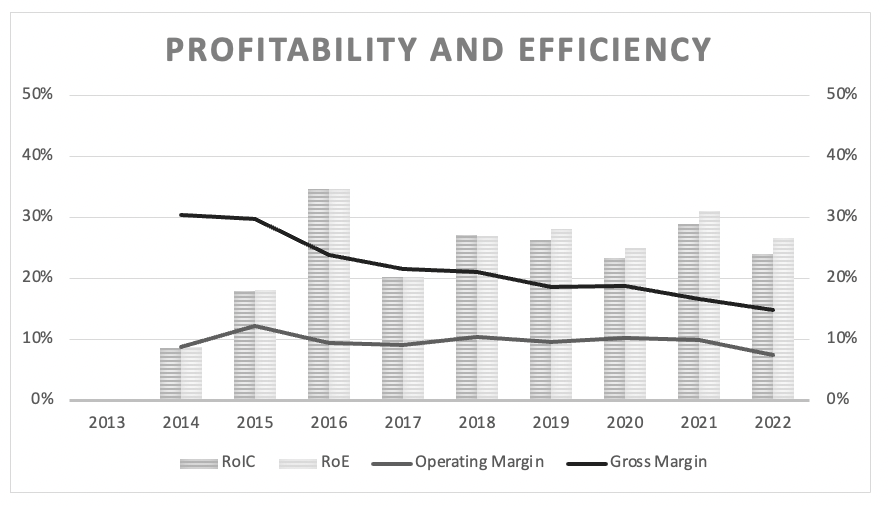

A strong hint for a great business with a wide economic moat around the business is the high return on invested capital Adyen could report in the past. In the last nine years, Adyen could report a return on invested capital of 23.5% - which is a strong hint for an economic moat around the business. And especially for a young business this is really impressive (by the way, in the following chart we used the margins as reported by most sites).

Adyen: Margins and return on invested capital (Author's work)

{kind=link}

Adyen is also owner-operated, which can often be seen as a good sign. I would like it even better when the founders still held the majority of (voting) shares and therefore had voting power as these are the typical characteristics of family-run businesses, which usually outperform over the long run. But we can also assume that the founder will rather have a long-term view and make strategic decisions about what is right for the business long term.

And Adyen is not only owner-operated but also extremely focused on who they hire and almost every new employee seems to be handpicked. This is part of the " Adyen Formula " and as the company is only hiring a few hundred people annually, it is possible to really focus on the hiring process. This might also be the reason why Adyen is presenting its employee statistics with such prominence in the annual and half-annual reports.

{kind=link}

Finally, Adyen also has a great balance sheet and on June 30, 2023, Adyen had not only no debt on its balance sheet (which is great for a rather young business), but the company also has €6,412 million in cash and cash equivalents. Without going further into detail, we can state that Adyen has also a great balance sheet.

Continue High Growth Path

The question that seems to be on everybody's mind right now is if Adyen can continue its path of high growth. During the last earnings call , management underlined several times that it sees its business model still intact and growing at a similar high pace as in the previous years. And in response to the question of analysts, management pointed out its focus on long-term thinking:

Then if you look at -- if your question is so what's happening next -- the next half year, that's not really the window that we look at. We are building for a longer -- for a way longer window. And then there's nothing where I would say this is not a sound strategy to keep on adding to the product. That's what brought us here. And you see we diversify indeed, as you ask, is the product diversification, yes, it's important to play in the platform economy, and it's important that we play in unified commerce. So I think that's a healthy way of looking at it and how we progress from here.

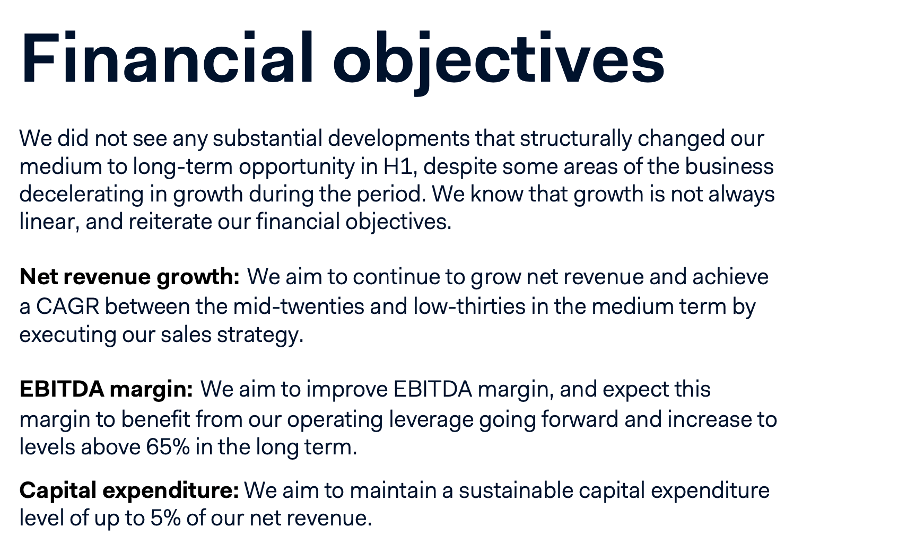

Management also reaffirmed its long-term growth targets. The company has its long-term financial objectives, which include the company's goal to achieve a CAGR between mid-twenties and low thirties in the medium term. And over the long run, the company is also aiming to improve its EBITDA margin and to increase it to levels of 65% in the long term.

{kind=link}

And although investors sold off the stock and analysts were disappointed, analysts are still expecting Adyen to increase revenue at a high pace in the next few years. Between fiscal 2022 and fiscal 2023, analysts are expecting revenue to grow with a CAGR of 18.68% and although we don't have estimates for earnings per share, we can expect the bottom line to grow (at least) at a similar pace.

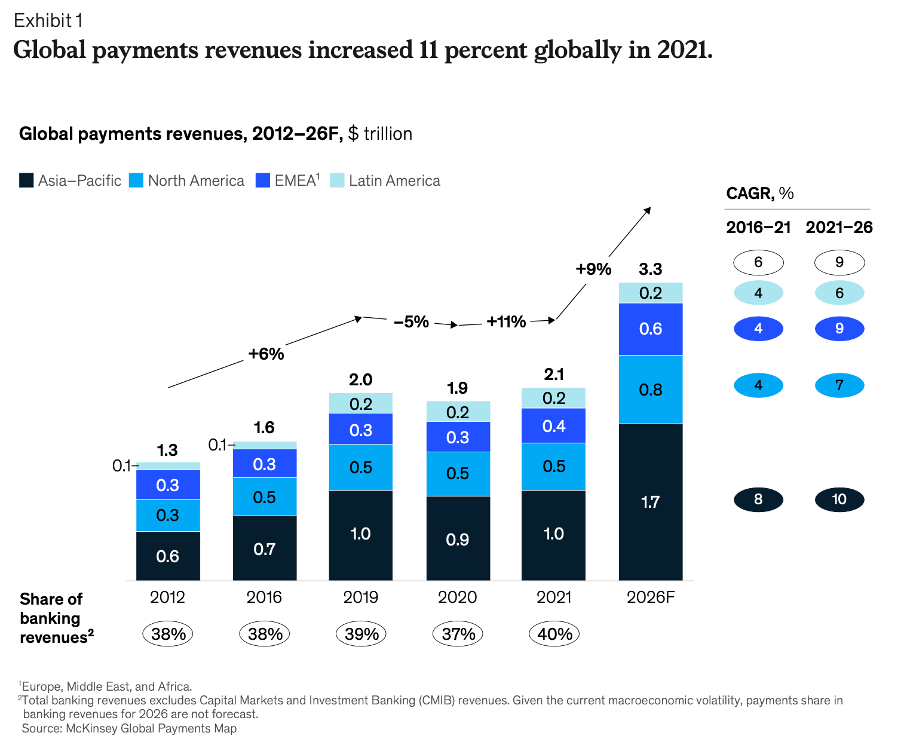

Not only are management and analysts optimistic about Adyen - the entire payment and fintech industry is still expected to grow at a high pace. In my last article about PayPal I already wrote about the growth of the global payment sector (and fintech industry). According to the 2022 McKinsey Global Payments Report , global payments revenue is expected to grow with a CAGR of 9% in the years to come.

{kind=link}

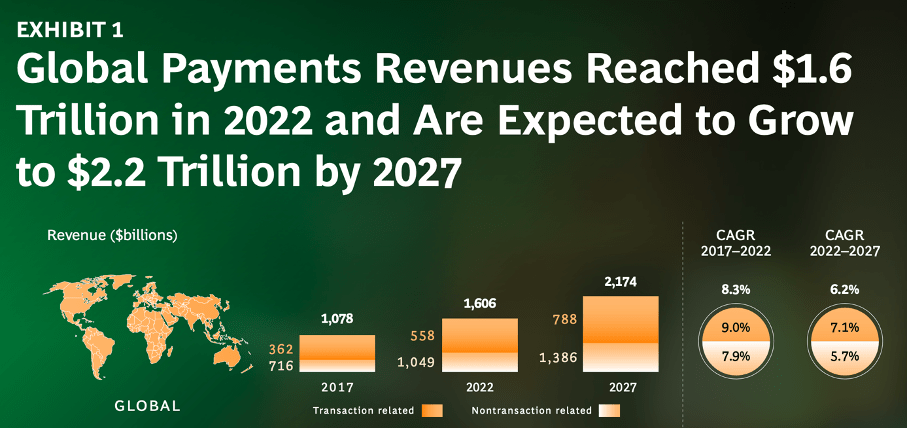

According to the Boston Consulting Group , global payments revenues are expected to grow with a CAGR of 6.2%.

{kind=link}

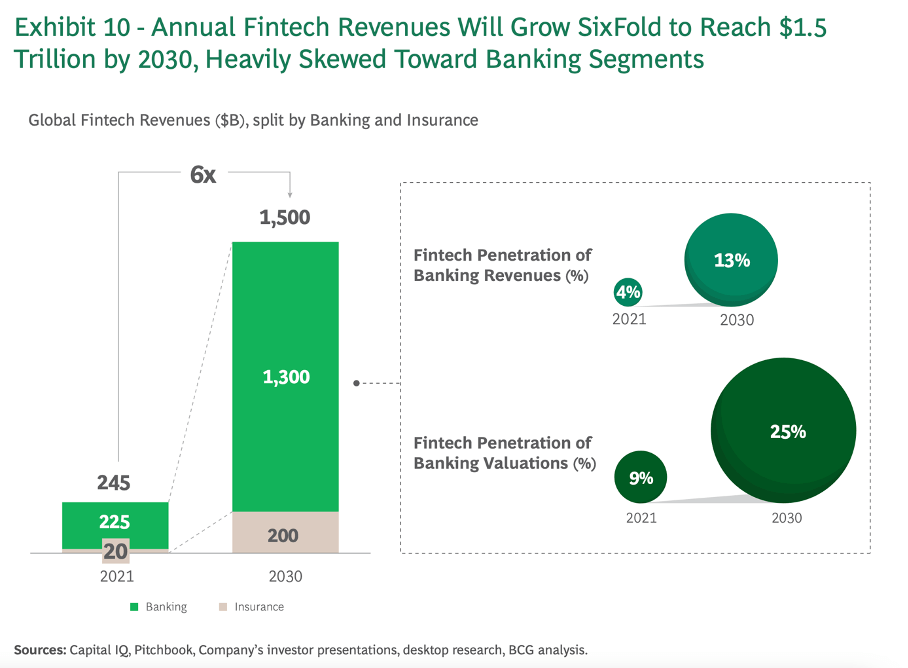

Different studies about the overall market growth are also reasons for optimism and sound rather bullish. But especially fintech and online payments are expected to grow at a higher pace while other forms of payment will decline. The fintech penetration of banking revenue is expected to grow from 4% in 2021 to 13% in 2030 with fintech stealing market shares from traditional banking and therefore growing at a much higher pace than the total payment sector.

{kind=link}

And when focusing especially on the Merchant Banking Services Market, in which Adyen is operating, we see an expected CAGR of 16.7%.

Short-term risks

While the long-term growth potential for Adyen seems to be gigantic and there is plenty of reason to be long-term bullish on Adyen, the company is facing short-to-mid-term risks.

At this point, it seems like the economy in several countries is headed towards a recession, especially several European countries are at a high risk with Germany already being in a recession And in such an environment consumer spending will decline with disposable income not only declining but people also trying to save money and postpone any investments and purchases which are not absolutely necessary. As a result, the processed payment volume will most likely be lower and this has a measurable effect on Adyen's business. Growth is already slowing down at this point for Adyen, and it might slow down further in the next one or two years.

On the other hand, we see positive signs in the United States. The number of initial unemployment claims is declining again (when looking at the 4-week average). And consumer sentiment (according to the University of Michigan) is constantly improving since June 2022 (although clearly lower than before the COVID-19 crisis). In an article published in mid-August I looked at several bullish and bearish aspects. Management also commented on the situation during the last earnings call:

This cycle presented shifting economic dynamics as the macro landscape evolved, we saw North American digital businesses increasingly prioritized cost optimization. We know that growth is not always linear and continued progressing towards our sizable opportunity while meeting our customers' ever-evolving needs."

And aside from consumer sentiment probably shifting, Adyen is also seeing lower growth due to competitive pressure:

If you look at online where we started the company, we see lower growth than what we hoped for. And the reason for that is that we have seen increasing competitive pressure in North America, and that's, to my view, related to a higher interest rate environment, more companies are looking at the bottom line, and that's an environment in which they try to see if cheaper alternatives work.

Overall, we can be optimistic about Adyen growing at a high pace in the next decade, but in the next few quarters we should be rather cautious.

Intrinsic Value Calculation

I wrote above that Adyen's stock declined about 80% since the previous all-time high and after such a steep decline one might often assume that a stock is undervalued now. But Adyen is still trading for high valuation multiples at this point. At the time of writing, Adyen is trading for 37 times earnings. Compared to about 280 times earnings about two years ago this might sound like a bargain, but a business still must grow at a high pace to justify 37 times earnings.

The stock is also trading for 25.8 times free cash flow, which seems more reasonable than the P/E ratio. Additionally, in the past few years, the price-free-cash-flow ratio was not as extreme as the P/E ratio, and I would always argue that the price-free-cash-flow ratio is the more important metric.

But most simple valuation metrics have some short comings, and a discount cash flow calculation is often the better choice. As basis for such a calculation we need to make several assumptions. For starters, we need to assume a free cash flow as basis and I think we can use the free cash flow of fiscal 2022, which was €607 million. Additionally, we calculate with 31.01 million outstanding shares. Free cash flow conversion was 83% - in the previous year the free cash flow conversion ratio was 90%.

To be fairly valued right now, Adyen must grow 11% annually in the next ten years followed by 6% growth till perpetuity. And when looking at the growth assumptions mentioned above and especially the growth rates Adyen could report in the last few years, these assumptions seem more than reasonable.

The difficult question is what growth rates for Adyen are realistic in the years to come. And of course, we can argue for such a young company if higher growth rates than 6% in ten years from now are realistic and if we should calculate with higher growth rates. But as I have often argued in the past, I never calculate with a higher growth rate than 6% for perpetuity (which is already optimistic considering that we don't know how the world will be in 20 or 30 years from now).

We will calculate with different assumptions - 10% growth in the next ten years, 15% in the next ten years and 20% in the next ten years. Each assumption is followed by 6% growth till perpetuity.

| 10% growth |

| 15% growth |

| 20% growth |

| Intrinsic Value |

| €649.51 |

| €922.67 |

| €1,303.43 |

| Adding cash on balance sheet |

| €856.28 |

| €1,129.44 |

| €1,510.20 |

When looking at cash and cash equivalents on the balance sheet, we have about €207 per share, which we can add to the intrinsic value. The company can use the cash on its balance sheet to acquire other businesses or use the cash to repurchase shares.

We can argue that Adyen is undervalued at this point, but the stock might not be such an extreme bargain as one might expect after an 80% decline. Adyen was so extremely overvalued before that the 80% correction was rather the reversion to the mean and not so much leading the stock into deep bargain territory. Nevertheless, I would argue that Adyen should be at least worth €1k at this point and the stock is undervalued.

Conclusion

Adyen is certainly a great business, and we can argue the company has a wide economic moat around its business. Despite short-term headwinds we also have reason to believe in double-digit growth rates in the years to come and Adyen might be undervalued at this point. However, to assume the stock is clearly undervalued, Adyen must grow at a high pace and assuming high growth rates for a long time is always a risky assumption.

For further details see:

Adyen: Another Fintech Company That Is Undervalued