V - Adyen: Buy Now As The Dust Settles

2023-10-04 00:34:17 ET

Summary

- Adyen's stock price has declined around 50% from its highs in August, prompting questions about whether the company is undervalued or if the earnings report justified the decline.

- Adyen is a global payment provider that offers businesses a single solution for accepting payments via mobile, point-of-sale, and e-commerce.

- The company has experienced a slowdown in revenue growth, particularly in North America, due to changing economic conditions and increased competition. However, Adyen's management stays optimistic and plans a revenue growth rate of ~30% and an EBITDA margin of 65%.

- Within our Bear and Bull Case scenarios, the company looks attractively valued.

Adyen ( ADYYF , ADYEY ) is down around 50% from its highs in the middle of August. The company's stock price declined almost 40% in one single trading day - after declaring earnings for the first half of 2023. This poses the question if the company could be undervalued right now or if the earnings report justified such an excessive decline.

The Business

Businesses are able to accept payments via mobile, point-of-sale, and e-commerce using Adyen, a worldwide payment provider. It was established in 2006 and has its headquarters in Amsterdam, the Netherlands. Adyen offers a single solution to take payments using a variety of methods globally. It is renowned for its smooth and effective service, which makes it possible for both customers and businesses to conduct transactions without any hiccups.

Adyen primarily generates revenue by charging transaction fees to businesses that use its payment platform. These costs typically consist of a predetermined fee per transaction plus a modest percentage of the total transaction amount. Depending on the nation, the Adyen platform accepts a wide range of payment options, including credit cards, debit cards, and other local payment options.

To get a better understanding of the market position, I summarized the different market participants of the payment market:

-

Merchants : These companies make use of Adyen's payment processing services. Small and medium-sized businesses to huge global corporations are among them. Retail businesses, e-commerce websites, and subscription services are a few examples.

-

Customers : These are the people or organizations that pay merchants using the several payment methods provided by Adyen.

-

Payment Networks : These are the companies that run the networks that Visa ( V ), Mastercard ( MA ), and American Express ( AXP ) use to handle credit card transactions. Adyen engages in communication with these networks to approve and complete transactions.

-

Banks and Financial Institutions : Customers receive payment cards from these organizations, and they also help retailers settle transactions with Adyen. By approving and executing transactions performed through Adyen's platform, they play a critical part in the payment process.

-

Regulators : Adyen communicates with regulatory agencies to guarantee compliance with laws pertaining to payment services, data protection, and anti-money laundering, among other laws, given that it operates in the financial services industry and is subject to several local and international rules.

-

Payment Service Providers (PSPs) and Payment Gateways : These organizations offer services that help customers and businesses conduct online transactions. By providing a full and integrated payment solution, Adyen competes with other PSPs and payment gateways and sets itself apart from them.

Here are some of the services that Adyen is offering:

Point of Sale Solutions : Allowing businesses to collect payments in person using hardware from Adyen.

E-commerce Payments : Providing online payment options for companies with an online presence.

Risk Management and Fraud Prevention : Giving retailers resources and assistance to reduce the risk of fraudulent purchases.

Currency and Conversion Services : Allows businesses to take payments in several currencies and convert them as necessary.

RevenueProtect : Adyen created an integrated risk management system to spot and stop fraud in real time.

Unified Commerce : Supplying businesses with a unified solution to manage payments across various channels (online, mobile, in-store), enabling them to provide a smooth consumer experience.

The company has achieved to amass some very high-quality customers, here is a list just to name a few:

Customers of Adyen (adyen.com/customers)

The Elephant In The Room - Decelerating Growth

Due to a noticeable slowdown in revenue growth in the first half of 2023 compared to the same time in the previous year, Adyen's shares saw a considerable decline. Adyen is currently positioning itself as a growth story, which is why it isn't surprising that investors reacted negatively to the company's slowing growth.

North America had a pronounced downturn, with net sales growth slowing to 23% year over year (YoY), down from 52% YoY growth in H1 2022. This slowdown in growth is significant since North America has recently been a major source of income. The trajectory in digital volume growth was similar, falling to 23% YoY from 55% in H1 2022. This was due to the big overlap of the North American and the Digital Payments Segment.

Development Digital Services (H1 2023 Shareholder Letter)

Unified commerce refers to the integration of several commerce channels into a single, coherent system that offers a consistent and customized consumer experience, and is used regardless of the channel or device used. In this segment, the growth also decelerated to 36% from 83% in the last time frame.

Development Unified Commerce (H1 2023 Shareholder Letter)

In Adyen's secondary key business division, Platforms, the performance seems to be the most concerning. Within this segment, there has been a significant deceleration in growth, plummeting from an impressive 53% to a mere 3%. Notably, a considerable portion of this decline can be ascribed to their major client, eBay. If we were to exclude eBay's influence on the numbers, the Platforms segment would have exhibited a remarkable 82% year-on-year growth. Management claims that the main reason for the slowdown in growth is because a sizable amount of eBay transaction volumes have already been absorbed and eBay is presently concentrating on improving certain payment options.

Development Platforms (H1 2023 Shareholder Letter)

In general, the company declared a net revenue of €739 million, which resembles a Year over Year growth rate of 21%. This is a considerable decrease in revenue growth if we compare this to the latest years:

2022 net revenue of €1.3 billion - 33% YOY Growth

2021 net revenue of €1.0 billion - 46% YOY Growth

2020 net revenue of € 648 million - 28% YOY Growth

2019 net revenue of € 496 million - 30% YOY Growth

2018 net revenue of € 349 million - 42% YOY Growth

Be careful here when you take a look at the metrics on your own, as most of the websites - including SA - state the gross revenue and not the net revenue. This however includes 'costs incurred from financial institutions' and is therefore not really a suitable metric.

H1 2023 Shareholder Letter (investors.adyen.com)

{kind=link}

This slow development was caused by a number of factors according to management, including altering economic conditions marked by inflation and rising interest rates. In the first half of 2023, many digital enterprises - especially in North America - put profit above growth and concentrated on cost reduction. Additionally, Adyen saw difficulties as a result of the tight labor market, which limited its hiring potential and had an influence on the size of its sales staff.

Therefore Adyen has increased its investments and hired 551 people, mostly for technical positions - this is an increase of ~16%. However, expenses related to team growth and inventory write-offs caused the company's EBITDA for the first half of 2023 to decline by 10% to €320.0 million ($348 million) from €356.3 million in the same period of 2022. Due to rising labor, payroll expenses, and greater amortization and depreciation, the EBITDA margin decreased to 43% from 59% in H1 2022.

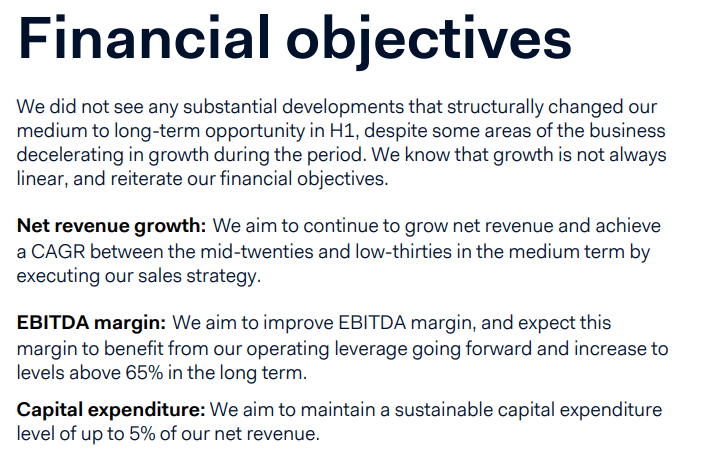

Investors were probably dumping the company's shares in light of these events due to worries about its slower growth rate, rising expenses, and constricted EBITDA margins, which are especially important given Adyen's stance as a growth firm. However, the corporation is planning to eventually increase its EBITDA margin to above 65% and maintain a revenue CAGR between the mid-twenties and low-thirties.

Financial Objectives Of Adyen's Management (investor.adyen.com)

{kind=link}

Valuation

We are now going to evaluate the company. To adjust for the above-mentioned decline and deceleration in operating metrics, we are going to take a look at two different scenarios:

- The Bear-Case: Growth and Margins stay "low"

- The Bull-Case: Growth and Margins are recovering

The Bear-Case

Europe is still lagging behind the US. Adyen is not able to compete with Stripe and establish a solid presence in the United States. The inherent competitive environment and market dynamics are hampering Adyen's development in establishing its footprint and securing market share in the robust digital payments landscape of the United States, despite the increased headcount, especially in North America.

The management doesn't manage to achieve its set goals. Revenue growth and margins remain to be rather low due to margin pressure and intense competition - major rivals like Stripe, and PayPal's ( PYPL ) Braintree pose serious obstacles. Within this scenario, we get the following assumptions:

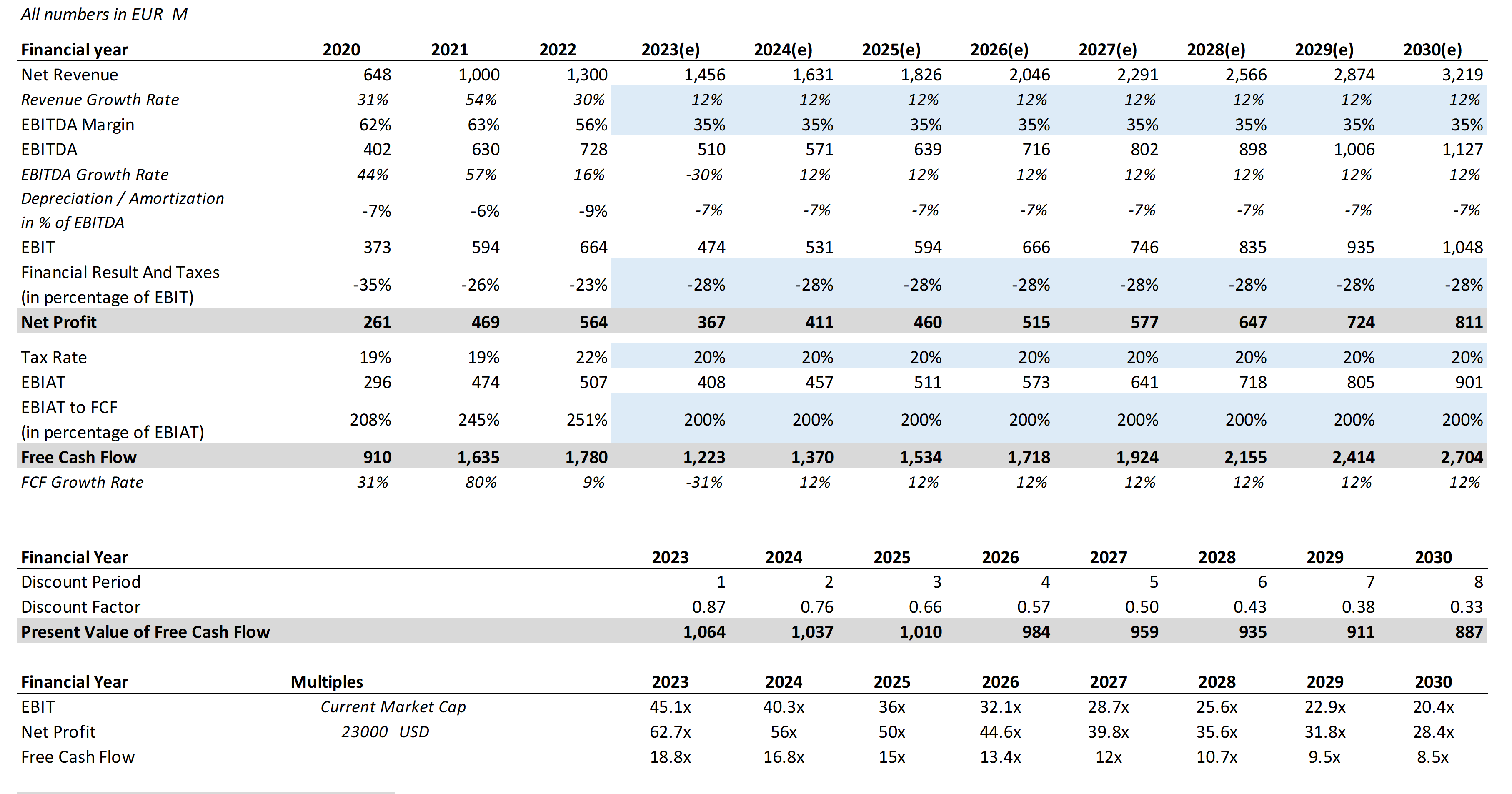

Revenue: For the revenue CAGR I assumed that the company will grow at a 12% growth rate over the next 8 years. Remember this is pretty conservative considering that the growth rate in H1 2023 of 21%, 2022 of 30%, and 2021 of a whopping 54%.

EBITDA: For the EBITDA Margin we took the assumption that the company manages to achieve 35% and it stays flat until 2030. This is once again a considerable decline compared to the latest years and last half year.

Depreciation and Amortization: Here I averaged out the last three years and used -7% to eventually calculate the EBIT.

Net Profit: From here on I used the average financial results and taxes of the last three years, -28%, and the aforementioned EBIT to determine the net profit.

Free Cash Flow: To get a suitable assumption for the Free Cash Flows, I firstly calculated the EBIAT. For that, I used the average Effective Tax Rate of Adyen for the last five years - 20%.

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| 2018 |

| Effective Tax Rate |

| 21.6% |

| 19.1% |

| 19.2% |

| 20.5% |

| 20.4% |

From there on I chose a suitable EBIAT to FCF ratio. The average of the last three years is ~235%. I used 200% to get an additional margin of safety.

WACC: For the WACC I used 13%, this is higher than Adyen's current WACC of 10% but I believe it is suitable as it provides us with an additional safety margin.

Perpetuity Growth Rate: Here I assumed a very conservative 2.5%.

Net Debt: According to SA, Adyen's net debt is currently at -€6.4 billion - meaning it currently has around 6.4 billion cash. In this metric, however, 'payables to merchants and financial institutions' is still included. For our DCF I adjusted the net debt to -2 billion by subtracting the payables to merchants.

Adyen DCF Bear Case I (seekingalpha.com; investor.adyen.com; own assumptions)

{kind=link}

Adyen DCF Bear Case II (seekingalpha.com; investor.adyen.com; own assumptions)

{kind=link}

With these assumptions, we get a fair price of ~€626, indicating that the company could still be overvalued by around 12%. However, keep in mind that this scenario factors in an additional decline in both EBITDA margin and revenue growth rate.

The Bull-Case

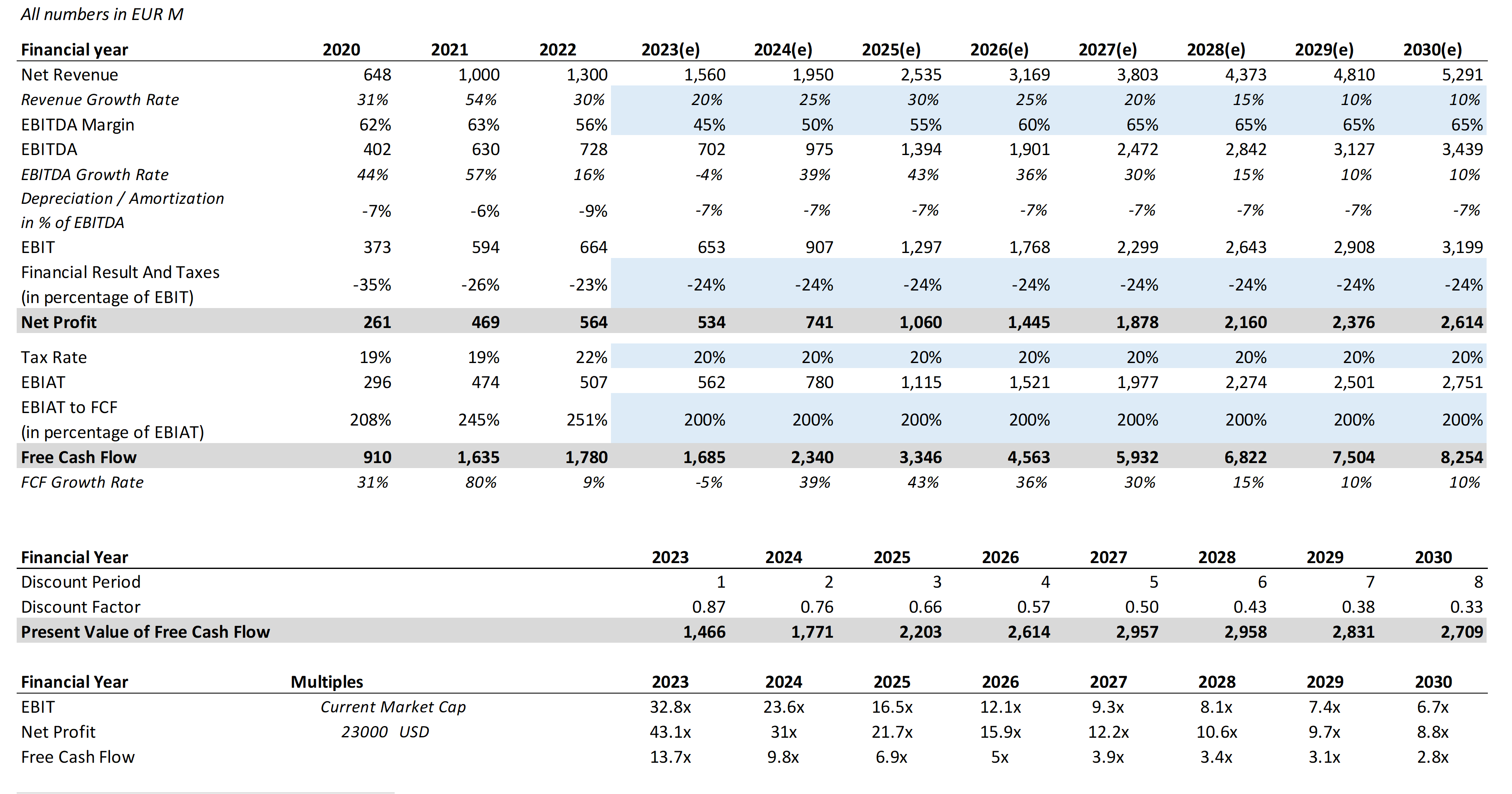

The company is seeing a return to its previous growth rates and management achieves its target for a revenue CAGR of ~30%. E-commerce continues to grow as normal, and the industry's upward trend is being maintained. The recent hiring spree leads to the desired growth in revenue and the EBITDA margins steadily grow to the long-term goal of 65%. In the Bull-Case we have these assumptions:

Revenue: The revenue growth stays at 20% in 2023, but is increasing steadily to eventually decline again:

| 2023(e) |

| 2024(e) |

| 2025(e) |

| 2026(e) |

| 2027(e) |

| 2028(e) |

| 2029(e) |

| 2030(e) |

| Revenue |

| 1,560 |

| 1,950 |

| 2,535 |

| 3,169 |

| 3,803 |

| 4,373 |

| 4,810 |

| 5,291 |

| CAGR |

| 20% |

| 25% |

| 30% |

| 25% |

| 20% |

| 15% |

| 10% |

| 10% |

EBITDA Margin: The company manages to steadily increase its margin to 65%:

| 2023(e) |

| 2024(e) |

| 2025(e) |

| 2026(e) |

| 2027(e) |

| 2028(e) |

| 2029(e) |

| 2030(e) |

| EBITDA Margin |

| 45% |

| 50% |

| 55% |

| 60% |

| 65% |

| 65% |

| 65% |

| 65% |

The other assumptions were the same for the Bull-Case scenario.

Adyen DCF Bull Case I (seekingalpha.com; investor.adyen.com; own assumptions) Adyen DCF Bull Case II (seekingalpha.com; investor.adyen.com; own assumptions)

{kind=link}

{kind=link}

With these assumptions, we get a fair price of ~ €1,630, meaning the company could be undervalued by a whopping 130%.

Conclusion

According to our scenarios, the company is currently miss-valued by -12% to 130%. Of course, the truth will probably lay somewhere in between, but the two scenarios show the - in my opinion - worst- and best-case scenarios.

With the historically very high EBITDA margin of 50% to 60%, the company has already proven that they are able to effectively manage the business. The aspired 65% margin therefore seems very achievable in my opinion. The current decline in the margin is largely caused by the hiring spree in North America of the company. I believe that this is exactly the right way, as Adyen has to expand its operations in NA further to stay competitive in the long run. In case of any uncertainties or slower-than-anticipated growth, the new employees can always be laid off, which should stabilize the margins. However, generally speaking, margins should normalize during expansion, and the decision to hire personnel shouldn't ultimately result in worse profitability.

With all this in mind, I currently rate the company as a 'Strong Buy' with an intrinsic value of €1,100.

For further details see:

Adyen: Buy Now As The Dust Settles