ADYEY - Adyen Simplified

2023-10-19 11:00:28 ET

Summary

- I recently came across some TAM and market share data that has acted as a key pillar of our investment thesis in Adyen.

- I would say that this data, in some sense, *is* the thesis. It reveals everything we need to know about our ownership of Adyen.

- Adyen's valuation is considered attractive, especially considering its capital efficiency and potential for future share repurchases.

- From the nature of the Adyen platform to its future growth prospects, this one piece of data certainly packs a thesis-buttressing punch.

- In short, with 20%+ annualized growth likely for the next 10 years, ~$1.8B in cash alongside no long-term debt, ~45%+ free cash flow margins, a 3.4% free cash flow yield (it really keeps getting better!), and a differentiated platform that has sustainably captured market share for the last decade, I like Adyen quite a bit at these levels.

Brief Intro

I recently produced an in-depth review of Adyen's (ADYEY) (ADYYF) H1 2023 report as well as a review of the business and investment thesis broadly. You may read that via the link below:

- Adding To Adyen

While I feel I was as comprehensive as possible in my review, I recently came across market share data that has been in my mind over the years for Adyen, but which I've been unable to locate. As I mentioned in the introductory bullet points, this data is, in some sense, the entire thesis.

Specifically, this data illustrates a few key aspects of the Adyen investment thesis:

- Its vertically integrated, single source of coding acquiring and issuing platforms will continue to capture market share in a highly competed, low differentiation total addressable market populated by legacy vendors from the 20th century.

- In this vein, Adyen has a very long runway for growth still ahead of it. There's massive opportunity, in the former of market share, which translates to gross profit and free cash flow, for Adyen to capture.

- With both of these ideas in mind, Adyen's elevated/attractive free cash flow yield, relative to its future growth prospects and ability to grow at management's guided 25-30% annually, represents an exceptional opportunity.

Adyen Grows Its Operating Income From $45M to $700M in The Last Eight Years Based on Points 1 And 2 (Is This Likely To Mysteriously Stop?? I Am Incredulous)

YCharts

With these ideas as our platform, let's begin this abridged version of my Adyen thesis.

Valuation: Attractive

As I've shared in the past, Adyen could likely be considered to be the best FinTech on earth presently. Perhaps, it could be argued that Stripe (STRIP) holds this crown, but, as the data in the concluding thoughts of this note will reveal, Adyen is a vastly more capital-efficient business relative to Stripe, while growing at essentially parity and while having fielded a platform at essentially product and feature parity.

Additionally, as the TAM data that I will share with you in a moment demonstrates, Adyen has a very long runway for growth.

So we have a fantastic combination of quality and capital efficiency, alongside elevated growth prospects.

With these ideas in mind, let's turn to a review of Adyen's valuation.

| Key Metrics |

| Values |

| 2023 Net Revenue |

| ~$1.6B |

| Long Run EBITDA Margin |

| "Greater than 65%" |

| Tax Rate (Netherlands) |

| ~26% |

| Long Run Free Cash Flow Margin (conservative) |

| 45% |

| Current Pull Thru Free Cash Flow (45% fcf margin) |

| ~$720M |

| Shares Outstanding |

| 3.1B |

| Net Cash |

| ~$1.8B |

| Enterprise Value |

| $20B |

| Free Cash Flow/Enterprise Value Yield |

| 3.4% |

For a company that could grow sales, and, by extension, free cash flow per share, at 20%+ (which would be below management's guidance) annualized for the next 10 years, a 3.4% free cash flow yield is quite fantastic.

And this does not include future share repurchase programs, which its legacy peers, such as Fiserv ( FI ), have executed with brilliant success.

To add just a bit of extra information here by which you may become a more educated investor, Adyen's 3.4% yield is quite attractive in light of its growth prospects and in light of the reality that it is likely the best FinTech on earth. This yield is vastly, vastly more attractive than the sub 2% yield investors were offered historically.

Additionally, the rise of Adyen's yield is not mysterious.

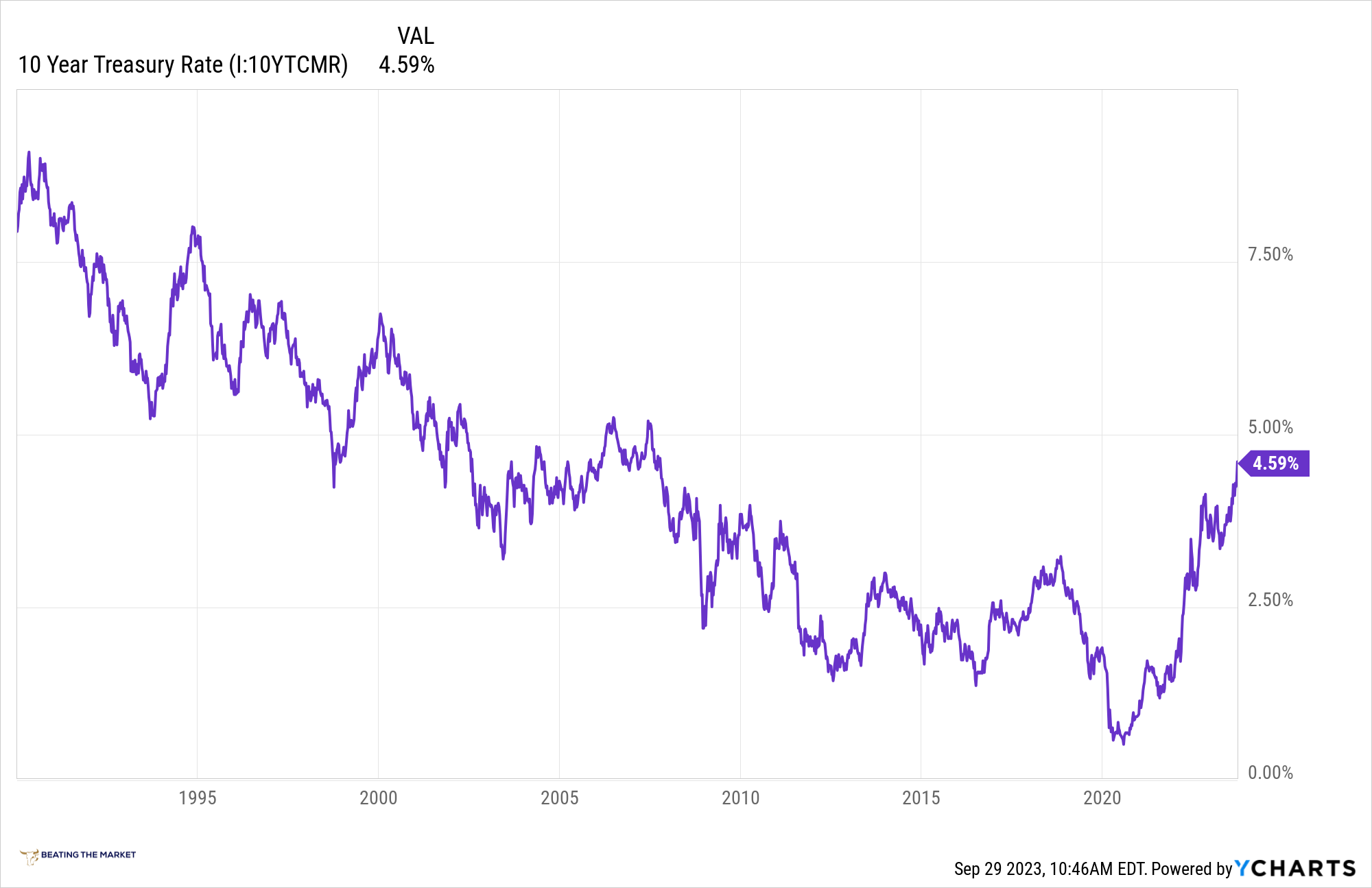

On the heels of the fastest interest rate hiking cycle in American history, the 10 year treasury yield, against which Adyen's yield principally competes for investor capital (the result of which influences supply and demand for Adyen's security; therefore, share price), now finds itself at about 4.6%.

10 Year Treasury Yield

{kind=link}

Academic finance suggests that Adyen should trade such that we get the risk free rate + risk premium, which would suggest that Ayden should trade with a free cash flow yield of 5%+.

For current owners, this likely sounds like a scary prospect, but for prospective owners, such a valuation would likely yield 25%+, or quite likely more, annualized returns in the decades ahead, as the company grows at 20%+ and begins repurchasing shares.

All of this being said, Adyen does not offer a risk premium, nor does its yield trade at parity with the 10 year treasury yield, and I believe this makes sense: While investors in the 10 year will only receive 4.9% per annum, granted they hold to maturity, investors in Adyen will witness the free cash flow yield (note not actual yield) on their investment grow very materially in the decade ahead, especially if Adyen begins repurchasing shares with its excess free cash flow, which it likely will at some point in the decade ahead.

TAM: Growing Within An Inverse Bubble

The principal impetus behind crafting this abridged version of the Adyen thesis was my recent receipt of the TAM data that has eluded me for the last couple of years or so.

Adyen, like essentially all of our businesses, has grown within a giant TAM populated by legacy incumbents and a diverse set of point solutions.

Adyen has vertically integrated the aforementioned point solutions into one acquiring platform tech stack, and it has done so on a single source of code. This has resulted in a more feature-rich, cost-effective, and versatile platform (especially for global, multi-national enterprises), which has afforded Adyen the market share capture we can see in the chart below.

Acquiring Platforms Market Share

Credit Suisse

Additionally, we can see the highly fragmented nature of this industry, within which Adyen continues to grow due to the nature of its platform. That is, its growth within this fragmented TAM has been a byproduct of the nature and configuration of its platform, which you may review below:

Understanding The Adyen Platform

Adyen S-1

Adyen is a quintessential example of a business that fits within my Inverse Bubble Framework (a term I coined), as well as our first and third foundational investment frameworks.

1. Vertically integrated product; capture market share in stagnant mature industry: We target businesses that have created a fully vertically integrated product, within a fragmented, low NPS, and mature industry, whereby that vertically integrated product offers 10x better value; therefore, it captures significant market share rapidly. [This is very clearly and quintessentially what the above data represents.]

3. Quality cultures that breed innovation within the larger conglomerate: We've often explored the Spawner framework (I'm working on a different name), which entails a company's ability to launch, or spawn, new successful business/product after new successful business/product, creating a nucleus of explosive, compounding sales growth. This is the idea that a business creates a culture in which its employees create new products successfully. With multiple products growing rapidly simultaneously, the business overall grows more rapidly and more durably. Some of my favorite examples that fit within this framework are Axon (AXON), Monday (MNDY), Adyen (ADYEY) , Sea (SE), Tesla (TSLA), Amazon (AMZN), and MercadoLibre (MELI). Indeed, many of my businesses possess this incredible cultural structure, and that is why we've chosen to own them.

Concluding Thoughts

As I mentioned towards the introduction of this note, Adyen is arguably the best FinTech on earth at present, and the financial data below confirms this reality in my mind:

@kouroshshafi

As we can see, Adyen's leadership has demonstrated a vastly greater aptitude for capital allocation relative to the leadership of Stripe.

Adyen has grown faster with vastly less required capital, and Adyen and Stripe are effectively at product parity today.

To close, some have told me they do not like FinTech; to which I would respond, "Fair, but have you seen the returns of legacy FinTechs from whom Adyen or Marqeta continue to capture market share?"

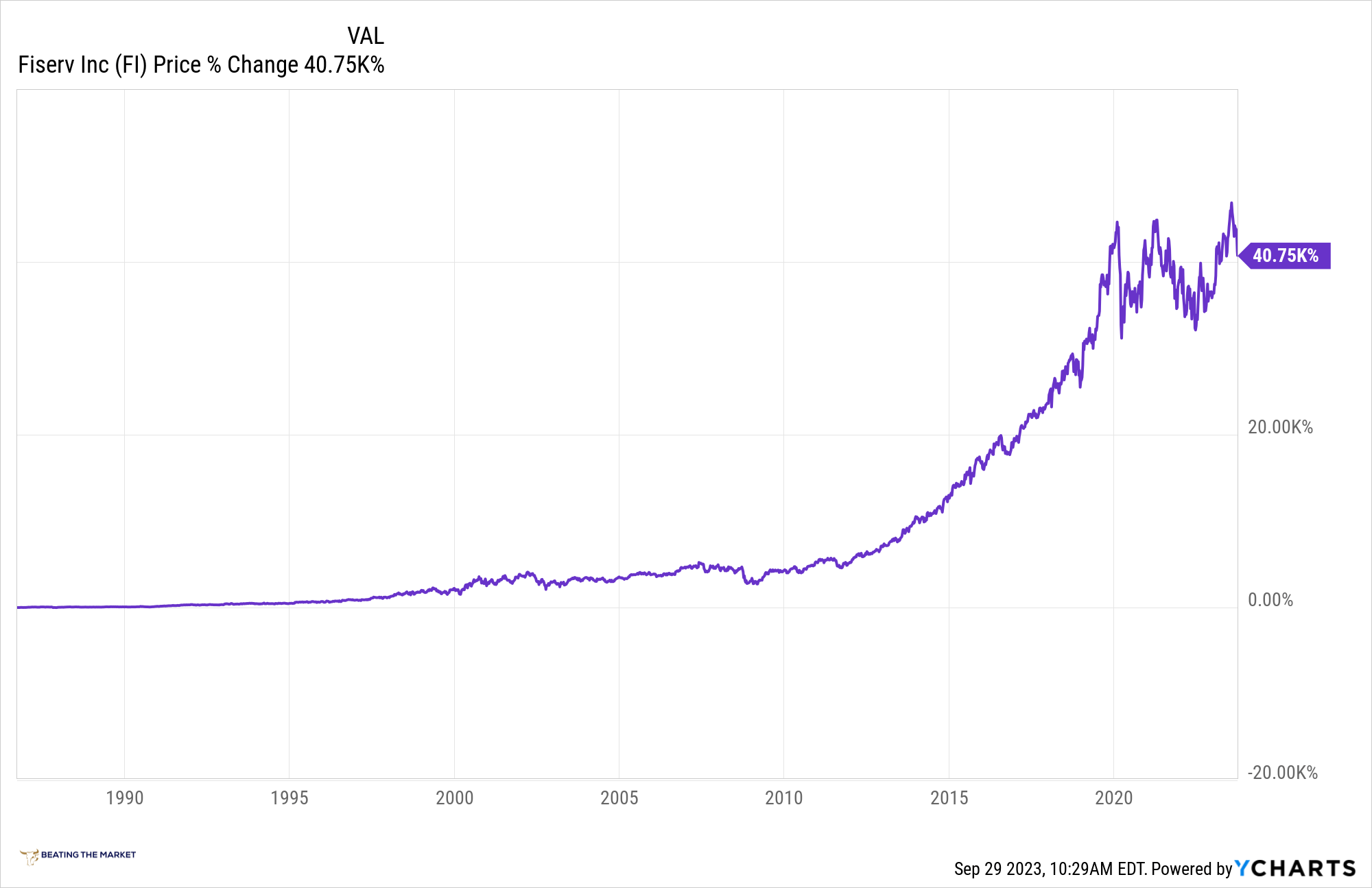

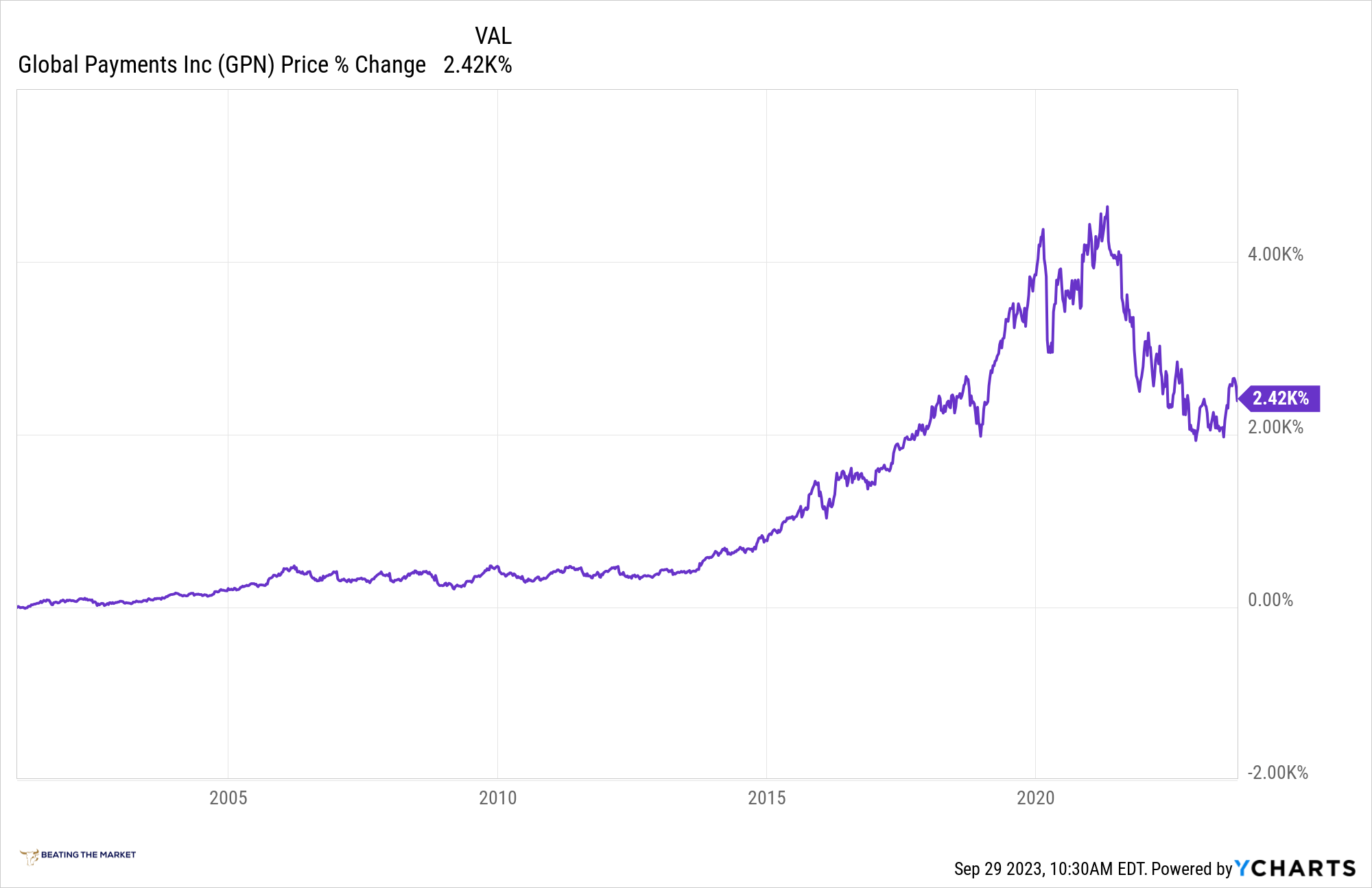

Below, we can see the returns of Fiserv and Global Payments over the last 40 and 20 years respectively.

Fiserv Returns ~40.75k% Returns In 40 Years

{kind=link}

Global Payments Returns ~2.42K% Returns In 20 Years

{kind=link}

Today, we have the opportunity to buy the very, very best FinTechs on earth at value ( OTCPK:ADYEY ) to deep value ( MQ ).

Both of these businesses have truly giant cash hoards and no debt, as well as very profitable unit economics and long runways for growth.

Thank you for reading, and have a great day.

For further details see:

Adyen Simplified