HNRG - Aegis Value Fund H1 2023 Portfolio Manager's Letter

2023-12-06 03:05:00 ET

Summary

- Aegis Value Fund is a Small-Cap Deep Value fund with a high Active Share managed by a research team with significant co-investment in the Fund.

- Aegis Value Fund underperformed its benchmark in the first half of 2023, with tech-focused stocks driving the S&P 500's gains.

- The banking system showed strains due to rising interest rates, leading to bank failures and losses on investment portfolios.

- The Fund's top performer was Bank of Cyprus, which benefited from its position in higher interest rates and reduced non-performing assets.

Table 1: Performance of the Aegis Value Fund as of June 30, 2023

| Six Month |

| One Year (Annualized) |

| Three Year (Annualized) |

| Five Year (Annualized) |

| Ten Year (Annualized) |

| Since Inception (Annualized) |

| Aegis Value Fund ( AVALX ) |

| 5.69% |

| 17.19% |

| 28.37% |

| 13.69% |

| 9.63% |

| 10.98% |

| S&P Sm. Cap 600 Pure Value Index ^ |

| 6.66% |

| 14.32% |

| 27.55% |

| 5.46% |

| 7.77% |

| N/A |

| S&P 500 Index |

| 16.89% |

| 19.59% |

| 14.60% |

| 12.31% |

| 12.86% |

| 7.67% |

| Morningstar Percentile Ranking * |

| 15 |

| 4 |

| 1 |

| 9 |

| Funds in Small Value Category |

| 450 |

| 433 |

| 420 |

| 388 |

| * Morningstar Percentile Ranking is based on total return. ^Available performance data for the S&P SmallCap 600 Pure Value Index prior to the December 16, 2005 inception date of this Index cannot be shown as display of pre-inception Index performance data is not permitted. Performance data quoted represents past performance and does not guarantee future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value will fluctuate so that upon redemption, an investor’s shares may be worth more or less than their original cost. For performance data current to the most recent month end, please call us at 800-528-3780 or visit our website at www.aegisfunds.com. The Fund has an annualized gross expense ratio of 1.48% and a net annualized expense ratio, after fee waiver and/or expense reimbursement and management fee recoupment, of 1.50%. Under the waiver, the Advisor has contractually agreed to limit certain fees and/or reimburse certain of the Fund’s expenses through 4/30/2024. |

Dear Aegis Investors:

The Aegis Value Fund returned 5.69 percent during the first half of 2023, underperforming its primary deep-value small cap benchmark, the S&P SmallCap 600 Pure Value Index, which gained 6.66 percent. The largest, tech-focused members of the S&P 500 were the stand-out performers, driving the index to a 16.89 percent gain over the period as the S&P 500 recovered from last year’s rout.

Banking System Began to Show Strains Under Higher Interest Rates

In the first half of 2023, the unusually rapid pace of Fed tightening claimed its first significant victims as the economy grappled with the biggest bank failures since the Global Financial Crisis, with Silicon Valley Bank and Signature Bank both failing in March, followed by First Republic Bank in May. Losses on investment portfolios from rising interest rates appeared to be the culprit. Many banks have been struggling in 2023 as the market value of their intermediate and long duration investment-grade bond portfolios slid lower with each Fed rate hike, often sparking deposit flight as account holders sought higher interest rates and more institutional stability.

The Fed reacted quickly, offering new liquidity programs to banks that were experiencing financial pressures. The Fed also slowed its rapid-fire pace of rate hikes, even pausing in June after hiking 500 basis points at the previous ten consecutive meetings. By mid-year, while many banking stocks were showing signs of recovery, banks remained some of the worst performers of the first half, with the KBW Bank Index dropping 20.47 percent.

Yet the Aegis Value Fund’s top first half performer was a bank

Fortunately, the Aegis Value Fund was well positioned for the bank rout, entering the year with a single bank stock in the portfolio: a 2.1 percent position in Bank of Cyprus (BOCH-L). Somewhat ironically, despite the bank industry turmoil, this position turned out to be the Fund’s strongest first-half performer, adding 1.59 percentage points to returns as shares in Cyprus’ largest bank climbed by 88 percent. As opposed to many of the troubled domestic banking institutions poorly positioned in long-duration debt bought during the recent period of ultra-low interest rates, Bank of Cyprus was much better positioned for the upturn in interest rates. The company, having recently reduced non-performing assets to normal levels, was instead holding extraordinary amounts of liquidity on deposit at variable rates at the European Central Bank. With rates soaring in the Eurozone, Bank of Cyprus’ position paid off handsomely, with interest income rapidly resetting higher, sending profit margins surging. With the bank finally turning the corner on its asset disposition program and its earnings beginning to surge with higher rates, investors began to re-rate the stock higher, narrowing its previously substantial discount to tangible book value. Despite the strong recent gains, we continue to maintain our position in Bank of Cyprus, and project a good probability for additional future gains given the stock still trades at a material discount to book value and at less than four times 2023 analyst earnings estimates.

We’re Looking at Banks, but Haven’t Found a Compelling Investment

With banking turmoil roiling the market in the first half, a significant number of bank equities are now hitting our watchlist. Resultingly, we allocated additional research focus on bank stocks in the first half. However, we have yet to make any additional capital allocations of significance into banks. Often, upon investigation, we have found that the equity book value for so many of the bank stocks on our watchlist are overstated, most notably on account of the so-called “held-to-maturity” investment securities. These securities portfolios are interestingly allowed to be carried on the books of banks at the purchase price pending eventual maturity, despite significant interim declines in market value that may have been incurred as interest rates increased – an accounting convention that allows the balance sheets of many bank equities to appear more robust than they might be in reality.

While banks with strong deposit franchises may be able to fund these impaired and low-yielding assets to maturity by paying depositors sub-market interest rates for extended periods, overall banks have had a significantly more challenging time than anticipated holding the line on increases in deposit rates. The so-called “deposit betas” of banking institutions have turned out to be substantially higher than many bank investors had hoped as depositors have proven more willing to shift deposits to a new institution for incremental interest than presumed. In the era of cell-phone bank connectivity, many banks have resultingly been forced to rapidly reset deposits to higher interest rates or risk losing the critical deposits that funds their assets. The outcome has been depressed banking margins and lower earnings expectations, or even losses at these institutions.

Significant Losses in Commercial Real Estate and Private Equity Could Also Materialize

Many banks are also highly exposed to commercial real estate, a sector that is now struggling with post-Covid occupancy challenges as well as rising inner city hollowing-out concerns centered around crime and city-center quality of life. A recent survey by global consultant McKinsey & Co. of nine large global cities suggested that remote working is likely to lead to a massive $800 billion decline in commercial real estate values in just these cities by 2030. Commercial borrowers, many having purchased urban buildings in recent years at top dollar values buoyed by low interest rate loans, are now also among the first to experience the impact of higher rates, courtesy of the shorter five to seven-year bullet maturities on these loans, as opposed to the longer 30-year maturities typical of fixed rate residential mortgages. With rates having surged over the last 18 months, we are now witnessing rising levels of commercial real estate defaults as nearly $2.5 trillion low-interest rate loans are slated to hit maturity over the next five years, leading to the prospects of forced asset liquidations and potentially significant increases in bank losses.

Bank loans were also liberally made in recent years to lever-up middle-market companies that funded high-priced private-equity buyouts and cash-out refinancings. These loans may now also be facing significant risk of loss as interest rates roll to today’s much higher levels, pressuring company liquidity. While both these sectors, as well as the banks that fund them, may prove to be fertile future hunting grounds for distressed and deeply undervalued equities, for the moment our Fund has remained on the sidelines, as we believe it is quite possible that the accelerating defaults we are witnessing may be just the tip of the iceberg as these sectors struggle to reprice lower under the weight of higher interest rates.

Technology Stocks Defied the Gravity of High Interest Rates and Skyrocketed in the First Half

With rates pushing still higher in the first half, and with skeletons now starting to tumble out of the economic closet in banking and commercial real estate, the big surprise was the massive surge in technology stocks. Speculators, apparently unconcerned with interest rates, and fully captivated by Chat GPT’s “artificial intelligence” capabilities, managed to blast the tech-heavy The Nasdaq Composite Index to a blistering 39.4 percent first half gain, its best first-half return in 40 years. Bitcoin skyrocketed an even higher 83.3 percent. Market gains in the S&P 500 Index over this period of 16.89 percent were also overwhelmingly driven by the strong performance among a narrow subset of mega-cap technology stocks, including Apple Computer, Amazon, Google, Meta, Microsoft, Nvidia, and Tesla. Dubbed by the media as the “magnificent seven,” these stocks today comprise a hefty 27.3 percent of the S&P 500 Index.

Tech Gains Driven by Multiple Expansion are Likely to End in Pain

Investors either directly invested in the magnificent seven or those indirectly, and perhaps unknowingly, exposed to the companies through their S&P 500 Index funds may not realize just how high in altitude the valuations have soared. As can be seen in Table 1, price-to-earnings valuation multiples of these stocks recently jumped higher in the first half of 2023 as share gains materially outpaced the growth in analyst forward earnings expectations. As a result, by mid-year, these stocks were trading at an average of 39.4 times forward analyst estimates and at an even more puzzling 109.2 times trailing GAAP earnings levels so high that multiple future years of extraordinarily strong and historically rare earnings growth rates are already fully priced into the equities. Furthermore, with the gravitational pull of today’s high interest rates bearing down heavily on all valuations, we would judge these price levels as simply unsustainable, with a strong likelihood of tears next in store.

Table 1: The Multiple Expansion of the “ Magnificent Seven ”

| 12/31/2022 |

| 6/30/2023 |

| Ticker |

| GAAP Trailing Twelve Months P/E |

| Next Twelve Months P/E # |

| GAAP Trailing Twelve Months P/E |

| Next Twelve Months P/E # |

| AAPL |

| 22.0x |

| 20.5x |

| 32.9x |

| 30.1x |

| AMZN |

| NEG |

| 46.7x |

| 312.6x |

| 62.0x |

| GOOGL |

| 19.4x |

| 16.9x |

| 26.6x |

| 20.3x |

| META |

| 14.0x |

| 14.7x |

| 35.6x |

| 21.5x |

| MSFT |

| 26.7x |

| 23.1x |

| 36.9x |

| 30.9x |

| NVDA |

| 62.1x |

| 34.4x |

| 242.8x |

| 47.8x |

| TSLA |

| 34.0x |

| 22.3x |

| 77.2x |

| 63.6x |

| # Next Twelve Months P/E is based on Analyst’s expectation. Source: FactSet |

The Aegis Value Fund Continues to Hold Significant Energy Sector Investments – Which Dragged in the First Half

Our Fund has instead chosen to maintain significant investment in a number of energy equities, with energy-sector holdings representing approximately 32.5 percent of Fund assets at mid-year. Our energy positions decreased Fund performance by approximately 2.3 percentage points in the first half, primarily stemming from declines in coal companies holdings Hallador ( HNRG ) and Peabody ( BTU ) as well as a drop in International Petroleum ( IPCO:CA ). In each case, we view the declines as temporary and continue to hold our positions in anticipation of future share price recovery and appreciation.

In stark contrast to the tech giants, energy stocks have generally been in the doldrums this year as NYMEX crude prices dropped 12 percent in the first half and Henry Hub natural gas prices plunged 37.5 percent. The weather certainly did not cooperate for energy investors, with the northern hemisphere experiencing one of the warmest winters on record. The unseasonable weather greatly reduced prospects of near-term global energy shortages arising from Russian energy export embargos and hurt trading sentiment. Furthermore, with energy markets increasingly plagued by fears of near-term demand destruction from an economic “hard landing,” worries over China’s slow pace of emergence from Covid lockdown, and concerns over fossil-fuel obsolescence, the wind was clearly blowing in the face of energy investors in the first half.

Energy Stocks Appear Well Positioned for Strong Returns

We continue to be constructive on traditional energy investments for a number of reasons. Energy has been a sector that has screened cheaply for some time with many companies comparatively undervalued in the equity markets relative to both asset values and cash flows. The energy sector offers cash flow yields that are among the highest available in the equity capital markets today. Many of the Fund’s energy-sector holdings have financially de-risked, using the strong cash flows generated in the last few years to significantly pay down debt, and leaving these companies very well positioned to weather a higher interest rate environment.

With stronger cash flows, many of our energy portfolio companies have increased shareholder returns, paying out solid dividends, or even more interestingly, using the cash flow to repurchase shares at what we calculate are bargain prices in transactions that are extremely accretive to long-term shareholder value. Our substantial holdings in Canadian heavy oil producers such as Meg Energy Corp ( MEG:CA ), International Petroleum ( IPCO:CA ) and Athabasca ( ATH:CA ) have valuable steam plant infrastructure in place and decades of oil reserves located in a politically friendly jurisdiction. Additionally, oil egress from Western Canada is likely to improve significantly early next year when the Trans Mountain Pipeline is expected to come on-line, taking heavy crude to west coast markets.

The Probability of Higher Oil Prices is also Good

Our energy holdings generally appear poised to deliver strong returns over time, with many generating excellent cash flow yields at today’s energy prices. Moreover, we believe the case for increased energy pricing, driving even better returns, is also quite strong. Despite all the talk of global recessionary fears and a slow China re-emergence from lockdown, oil demand remains robust, with the International Energy Agency (the IEA) in July reporting global oil consumption was still projected to climb by 2.2 million barrels per day this year to a record 102.1 million barrels per day.

It is important to note that demand for crude has remained surprisingly robust during recessions, with 2020’s Covid driven downturn being a notable recent exception. Generally, oil demand has been dominated overwhelmingly by long term consumption growth trends in Asia, as China, India and other developing countries relentlessly increase their per capita oil consumption. Such trends are also quite likely to continue well into the future, despite the multitude of political narratives de rigueur against fossil fuels, as 7 billion people on earth who consume an average of 3 bbls/yr desire to live like the other 1 billion who consume an average of 16 bbls/year. Increased use of low-cost, fossil fuel energy remains critical to the alleviation of poverty and a more inclusive global economic development, with fossil fuel energy demand unlikely to easily or inexpensively be supplanted by alternatives through government fiat. Goldman Sachs’ commodities analyst Jeff Currie recently pointed out that $3.8 trillion in investment in renewables has been spent over the last 10 years. These expenditures have been financed to a large extent from taxpayer handouts and through other government market distortions. However, despite all these costly expenditures over the last 10-years, the share of total global energy consumption met by fossil fuels has only dropped by one percent, from 82 percent to 81 percent.

Oil Supply Constraints are Setting up For Potentially Strong Future Returns

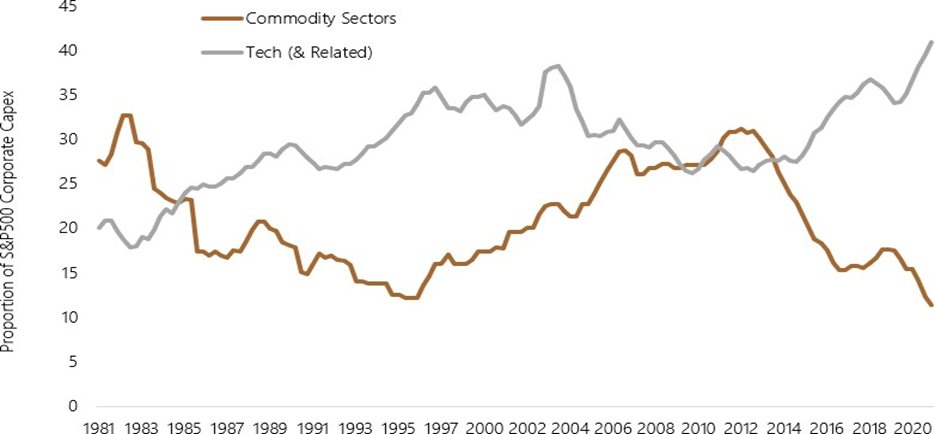

At the moment, the oil supply picture also appears opportunistically constrained, with many banks and institutional investors restricted from capital investment in fossil fuel enterprises, under ill-conceived and often politically-oriented investment mandates. These mandates have acted to choke off capital investment in oil production growth in the western world. The largest oil majors also appear increasingly distracted from their historical role funding the growth of low-cost energy supplies in the hunt for oil, and are increasingly allocating capital instead to the development of high-cost, speculative renewables in the hunt for green energy-related taxpayer hand-outs and subsidies. A case in point appears to have been BP’s decision to acquire Archaea, a high-cost bioenergy company, for an astounding $4.1 billion in late 2022, which managed to top Chevron Corp’s $3.15 billion purchase of high-cost biodiesel maker Renewable Energy Group earlier in the year. As can be seen in Figure 2, commodity sector investment, which of which energy is a large portion, has been at a 40-year low as a percentage of S&P 500 corporate capital expenditures (Capex). At the same time, tech expenditures have ballooned.

While constrained capital investment in recent years has certainly suppressed oil supply growth, the US government has been recently sheltering consumers from the adverse impact of these policies by selling oil into the world market from the country’s Strategic Petroleum Reserve (SPR), in what appears to be a political effort to suppress energy prices. With strategically important SPR reserves now plumbing multi-decade lows, the runway for further extension of this artificial supply appears to be fairly limited. Furthermore, production out of the US shales has been leveling off – a function of the plateauing drilling efficiencies and the exhaustion of top tier drilling locations in maturing fields.

Figure 2: Capex: Commodity Vs Tech

{kind=link}

Growth in production from US shale, which has added more than 7 million barrels per day to global supply over the last 12 years, has been instrumental in meeting world demand growth. However, with future shale growth looking substantially more subdued, it is unclear where the supply will now be found to meet future demand growth. Factor in the recent OPEC+ cartel production cut of 1 million barrels per day along with the long-term negative supply impacts facing Russia, given its isolation, and it certainly appears probable a strong environment for energy investment returns could be setting up.

The Aegis Value Fund’s Largest Purchase Was Natural Gas Services

The Fund heavily purchased energy-sector holdings in the first half of the year. The largest Fund purchase overall was Natural Gas Services (NGS), a Texas-focused energy logistics company that fabricates, rents, and maintains compression equipment for oil & gas companies. Shares in the company, which trade at a 45 percent discount to tangible book value, have been under selling pressure as executive turnover, rising debt-loads and descending gas prices have apparently generated some selling pressure in this historically sleepy stock. Fortunately, despite all the management transition noise, we were pleased to see that Steven Taylor, a former Halliburton executive who has been instrumental in successfully and conservatively steering the company over many years, was re-assuming the CEO role. Although the $125 million market-cap company has seen debt increase from de-minimus levels to just over $60 million in just the last few quarters, we were pleased to see that the increase was made to fund a material expansion in larger horsepower compression rental equipment, the overwhelming majority of which has already been committed to multi-year contracts at strong rates to high quality customers.

Furthermore, several competitors to NGS have been highly levered and are now facing rising interest expense and financial pressure as they endeavor to de-lever. As a result, these competitors have not been able to take full advantage of the strong compression market and expand their own rental fleets. Fortunately, NGS was well positioned with a debt free balance sheet and has been capturing profitable share. With significant debt capacity at the company to put new equipment on profitable, long-term leases, NGS is planning to spend $150 million in capital expenditures this year. With new equipment requiring about six months from purchase-order payment to rental installation and with much of the ramp-up in business having occurred since late 2022, investors have not yet seen the cash flow impact in reported results, which has resulted in distorted cash flow valuation multiples. Normalized, we see free cash flow FCF returns on market value of the company in excess of 20 percent once the newly ordered equipment is fully installed, which we suspect could lead to a nice stock re-rating. With large investor representation on the company’s Board of Directors and high share ownership by the Chief Executive Officer, we believe corporate governance at the company is strong. At quarter end, the Fund held a 2.4 percent position in Natural Gas Services.

The Fund’s Gold Positions Performed Well in the Quarter

At mid-year, the Fund continued to maintain significant investment in a number of precious metals mining equities. These positions, in aggregate, added an estimated 1.93 percentage points to first half Fund returns as spot gold gained 5.23 percent. Interestingly, despite gold’s first half price rise, the MVIS Global Junior Gold Miners Index was actually down by 0.12 percent as the industry’s primary performance benchmark for junior miners underperformed the metal. The Fund’s strongest gains came from Equinox Gold (EQX-TO), which alone added 1.25 percentage points to Fund first half returns as the company’s Greenstone gold project continued to progress both on-time and on-budget. We suspect the positive update at Equinox may have surprised the market following significant cost over-runs and delays at recent projects in North America by Argonaut and IAM Gold.

Centerra Gold also added 0.62 percentage points to first half Fund performance. The Turkish government finally approved the restart of the Oksut mine following completion of the required mercury abatement retrofit to the adsorption/ desorption and recovery (ADR) plant after an unfortunate mercury leak forced a shut-down and dented the value of the stock. Worst performing was the Fund’s position in Minera Alamos, a Mexico-focused mining start-up. Production at the company’s new Santana heap-leach project start-up was plagued by water well and pad permitting delays, impacting the Fund by just under one percentage point. We continue to hold our position, with confidence that Minera Alamos’ issues are teething pains and believe the management team will manage to get the business back on track in the next few quarters.

Precious Metals Miners Are Well Priced and Positioned for Gains

We continue to believe that our Fund’s precious metals miner holdings represent excellent value relative to the broad market. These investments offer ownership in gold projects with return profiles that we judge to be excellent in the context of today’s gold prices. Furthermore, we believe these holdings also offer some unique characteristics, performing particularly well in certain investment scenarios where the Fed, perhaps on account of political influence, chooses to pivot and loosen monetary policy prior to a full retrenchment of inflationary pressures. With nearly 40 percent of the $32 trillion of US Government debt outstanding coming due for interest rate repricing in the next 24 months, and with fiscal deficit federal spending already adding an incremental $1.5 trillion to the annual tab, we think the Fed may soon find itself under substantially increased government pressure to debase and depreciate the value of the dollar in order to lessen the debt burden on the Federal Government. Under these kinds of inflationary scenarios, our mining holdings could potentially deliver very strong returns.

{kind=link}

We’re Trying to be Well Positioned for Whatever the Fed Decides to Throw at Us

As we sit today, the Fed appears quite hawkish despite large sectors of the economy, such as real estate, private equity and banking, appearing to have already arrived at the cutting edge of the Fed’s high interest rate buzz saw. We have endeavored to position the Fund with an effort to avoid situations that put us in the direct path of the saw, a positioning of particular value should the Fed continue to keep rates elevated, and especially so if the tight policy is maintained in the face of increased market turmoil.

More specifically, we have worked diligently to limit our exposure to debt within our Fund holdings. When taking on investments that do have meaningful financial leverage, we have worked to ensure that the corporate debt structure is sufficiently robust such that substantial periods of illiquidity and high interest rates can be successfully navigated. While inflation appears to have been on the decline in recent months, it remains an open question as to whether inflation will soon dim substantially enough to allow the Fed to successfully cut rates without reigniting inflation. We must admit we have our doubts. Far more likely, to our thinking, is a premature Fed pivot. Should the Fed succumb to the increasing political pressure and turn more dovish, we believe the Fund is very well positioned with substantial holdings in precious metals mining, energy, and basic resources.

The Broad Markets are Overpriced, But Unusual Market Dispersion Offers Good Investment Opportunities

Overall, the broad US equity markets do not appear to be particularly attractive. With the recent surge in prices, valuation levels on the large cap, technology stock-laden S&P 500 are now, in fact, looking quite vulnerable, particularly in the context of today’s significantly higher interest rates. Furthermore, we must not forget that historical recessions have knocked as much as 20 percent off prior levels of S&P500 earnings. Technology valuations today are way too high, in our view, and intense regression to the mean appears to be a strong probability, particularly should valuations spend more time under the suppressive gravity of higher interest rates.

Figure 4: Aegis Value Fund, Russell 2000 Value and S&P 500 Index Historical Price-to-Book Ratio

Source: Aegis Financial Corp and Bloomberg (Data from 9/30/1998 to 06/30/2023)

Figure 5: Number of Stocks Selling Below Tangible Book Value (Market Cap. Greater Than $70 Mil)

Source: U.S. public equity market statistics from Stock Investor Pro (Data from 4/30/2002 to 06/30/2023)

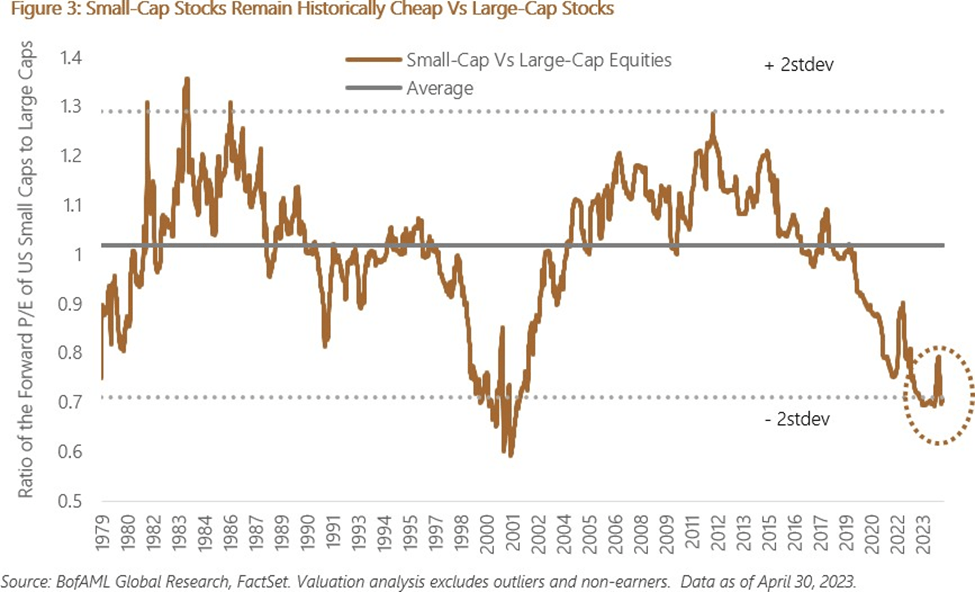

Fortunately for us, markets today have also once again become unusually bifurcated, with large portions of the market having not participated in the massive run-up in valuations seen in the technology sector. As a result, the valuation disparities between the cheapest and most expensive stocks in the market are unusually high today, and many smaller stocks today trade at valuation levels that offer good value. In fact, as seen in Figure 3, small-cap US equities have recently traded at some of the biggest price-to-earnings discounts relative to their U.S. large-cap peers. We can also observe some evidence of this bifurcation in the increased valuation differentials between the S&P 500 and the Russell 2000 Value Index, as seen in Figure 4. Our Fund continues to trade at a significant discount on price-to-book relative to both indices. As can be seen in Figure 5, the number of stocks on our watchlist has also increased materially in recent quarters, with the number of investment prospects now oddly reaching the high levels set during the Global Financial Crisis in 2008/2009 and the Covid crisis of 2020.

Overall, we continue to hold a portfolio of carefully researched stocks offering what we believe are among the best risk/ return profiles available to investors in the equity markets today. Aegis employees and their families own in excess of $48 million of Fund shares. We continue to carefully monitor our Fund portfolio for emerging risks. Should you have any questions, our shareholder representatives are available at (800) 528-3780. You are also welcome to call me personally at (571) 250-0051.

Sincerely,

Scott L. Barbee, Portfolio Manager, Aegis Value Fund

| Please see the following page for important information. The Aegis Value Fund is offered by prospectus only. Investors should carefully consider the investment objectives, risks, charges and expenses of the fund. The Statutory and Summary Prospectuses contain this and other information about the Fund and should be read carefully before investing. To obtain a copy of the Fund’s Prospectus please call 1800-528-3780 or visit our website www.aegisfunds.com, where an on-line version is available. Mutual fund investing involves risk. Principal loss is possible. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. Investments in smaller and mid-cap companies involve additional risks such as limited liquidity and greater volatility. Investment concentration in a particular sector involves risk of greater volatility and principal loss. Value stocks may fall out of favor with investors and underperform growth stocks during given periods. The Fund’s top ten holdings are Amerigo Resources Ltd., Interfor Corp., Hallador Energy Company, MEG Energy Corp., Kenmare Resources, International Petroleum Corp., Orezone Gold Corp., Equinox Gold Corp., Algoma Steel Group Inc., and Peabody Energy Corp. As of June 30, 2023, the stocks represent 6.2%, 5.5%, 5.4%, 5.1%, 5.0%, 4.4%, 4.1%, 3.3%, 3.2%, and 3.1%, of total Fund assets respectively. Fund holdings are subject to change and should not be considered a recommendation to buy or sell a security. Current and future portfolio holdings are subject to risk. Morningstar Rankings represent a fund’s total-return percentile rank relative to all funds that have the same Morningstar Category. The highest percentile rank is 1 and the lowest is 100. It is based on Morningstar total return, which includes both income and capital gains or losses and is not adjusted for sales charges or redemption fees. © 2023 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results. Price to Book: A ratio used to compare a stock's market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter's book value per share. Book Value: A company’s common stock equity as it appears on a balance sheet. Price-to-Earnings The P/E ratio is the measure of the share price relative to the annualized net income earned by the firm per share. S&P 500 Index: An index of 500 stocks chosen for market size, liquidity and industry grouping, among other factors. The S&P 500 is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe. Cash Flow: A revenue or expense stream that changes a cash account over a given period. MVIS Global Junior Gold Miners Index: The modified market cap-weighted index tracks the performance of the most liquid junior companies in the global gold and silver mining industry. The S&P SmallCap 600 Pure Value Index: An index maintained and selected by the S&P Index Committee. It contains companies with market caps in the range of US$ 300 million up to US$1.4 billion and with public floats of at least 50% and with strong value characteristics. NASDAQ Composite Index: A market-capitalization weighted index of the more than 3,000 common equities listed on the Nasdaq stock exchange. The types of securities in the index include American depositary receipts, common stocks, real estate investment trusts (REITs) and tracking stocks. The index includes all Nasdaq listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds ('ETFs') or debentures. Russell 2000 Value Index: measures the performance of small-cap value segment of the U.S. equity universe. It includes those Russell 2000 Index companies with lower price-to-book ratios and lower forecasted growth values. Tangible Book Value: The net asset value of a company, calculated by total assets minus intangible assets (patents, goodwill) and liabilities. Basis Point: One 100th of one percent. US Strategic Petroleum Reserve: The world’s largest supply of emergency crude oil. It was established primarily to reduce the impact of disruptions in supplies of petroleum products and to carry out obligations of the United States under the international energy program. KBW Bank Index: consisting of the stocks of 24 banking companies. This index serves as a benchmark of the banking sector. New York Mercantile Exchange (NYMEX): is the world's largest physical commodity futures exchange. U S Strategic Petroleum Reserve: The world's largest supply of emergency crude oil. It was established primarily to reduce the impact of disruptions in supplies of petroleum products and to carry out obligations of the United States under the international energy program. Free cash flow ('FCF') represents the cash that a company is able to generate after laying out the money required to maintain or expand its asset base. The European Central Bank (ECB) manages the euro and frames and implements EU economic & monetary policy. Its main aim is to keep prices stable, thereby supporting economic growth and job creation. GAAP (generally accepted accounting principles) is a collection of commonly followed accounting rules and standards for financial reporting. The International Energy Agency (The IEA) is at the heart of global dialogue on energy, providing authoritative analysis, data, policy recommendations, and real-world solutions to help countries provide secure and sustainable energy for all. The Organization of the Petroleum Exporting Countries Plus (OPEC+) is a loosely affiliated entity consisting of the 13 OPEC members and 10 of the world's major non-OPEC oil-exporting nations. Diversification does not guarantee a profit or protect from loss in a declining market. An investment cannot be made directly in an index. Earnings growth is not representative of the Fund’s future performance. Dividends are not guaranteed and may fluctuate. Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice. References to other investment products should not be interpreted as an offer of these securities. Quasar Distributors, LLC is the distributor for the Aegis Value Fund. |

Editor's Note: The summary bullets for this article were chosen by Seeking Alpha editors.

For further details see:

Aegis Value Fund H1 2023 Portfolio Manager's Letter