AEGOF - Aegon Continues To Be A Buy

2023-05-19 14:59:23 ET

Summary

- Aegon is progressing on its portfolio optimization and is on track to close the a.s.r. transaction.

- Cash holdings are in the upper half of the operating range.

- Ongoing buybacks and solid balance sheet mean Aegon is a solid buy, also thanks to the a.s.r. cash procedure upside.

Here at the Lab, following the US regional bank crisis and Credit Suisse-UBS development, we decided to take advantage and increased our rating on Aegon (NYSE: AEG ). Why? First of all, the Dutch insurer has limited exposure to CS's AT1 bonds . Secondly, the company is moving on with a transaction (a merger with ASR ) that will be extremely beneficial for shareholders' remuneration, cash proceeds used for deleveraging, and combined synergies - you can have a look at our previous publication titled ' Deal To Benefit All '.

{kind=link}

After having reviewed Aegon Q1 results and participated in the Q&A analyst call, here at the Lab, we could not be more than satisfied. Before going into the company's details, and reporting on our Zurich Group's latest publication , we positively view the insurance sector for the following macro reasons:

... in a world with negative interest rates, insurance companies have focused on cost optimization. If we are looking to the past, insurer players were recording cash surplus on investment activities and reinvestment yield; however, since rates significantly declined their aim moved to the core operating activities. The lower the combined ratio the more profitable is the insurer. Currently, here at the Lab, we are confident in the sector thanks to a double benefit 1) stable combined ratio and 2) higher reinvestment yield.

Going to the investment buy case recap on the micro level, we are confident that Aegon 1) will sustain a solid cash organic generation, 2) will deleverage for about €700 million following the ASR deal, 3) and more importantly, will remunerate shareholders with a higher dividend per share, an ongoing buyback and a potential additional special dividend or higher share repurchase announcement for a total consideration of approximately €1.8 billion which is equivalent of 21% of the company's today market capitalization.

{kind=link}

Source: Aegon Q1 results presentation

Q1 results

Related to the ARR transaction, Aegon is making the right progress to move on with its transformation agenda plan. The company is on track for the merger combination closing which is expected to be completed in 2023's second half. Reporting the CEO's words, Aegon is making " good progress with the disentanglement of Aegon the Netherlands from the group ". And he also explained how the Dutch player is confident to achieve the necessary regulatory approvals.

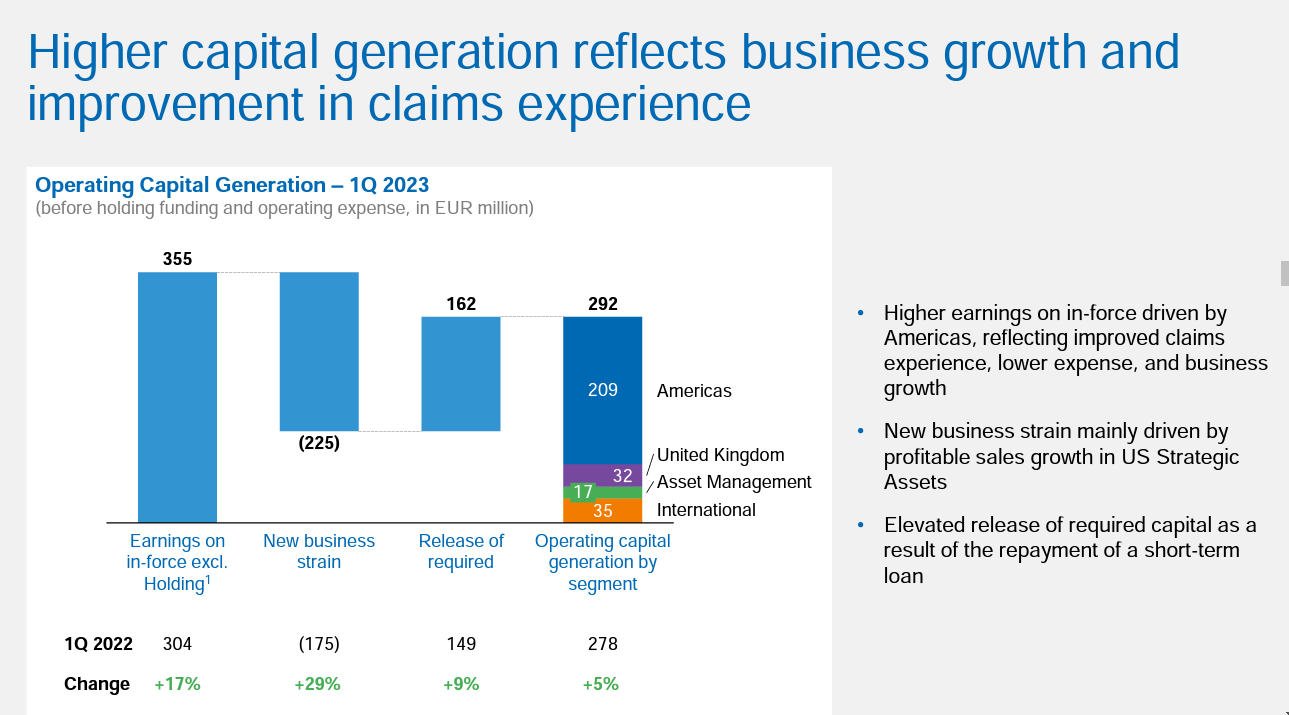

Going back to the core financials ratio, Aegon recorded a good start to the year. The company's organic capital generation increased by 5% to €292 million versus Q1 2022. This was driven by business growth, higher pricing power, and combined ratio improvements. Aegon turnover significantly grew in the US Strategic Assets , and a positive performance was also recorded in the life insurance businesses in Brazil and China. On a negative note, we should recall a lower sales momentum in the company's asset management division; however, we should not be surprised. After having analyzed Allianz and Zurich , capital market conditions were not giving any favor to the insurance sector and Aegon net outflows recorded $1 billion and $159 million in Variable Annuities and Fixed Annuities respectively.

{kind=link}

The CR was not disclosed; however, the company mentioned that there was an improvement in claims and achieved lower expenses. As a reminder, the combined ratio is the sum of incurred losses and expenses divided by the earned premium and multiple per 100. The lower the ratio is, the more profitable is the insurer.

{kind=link}

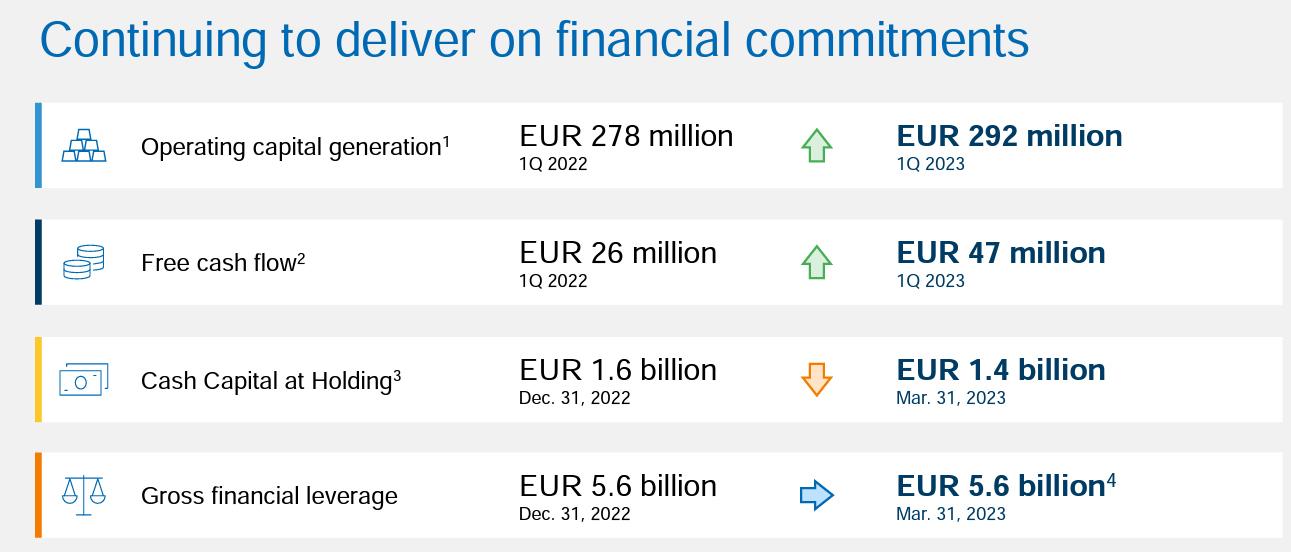

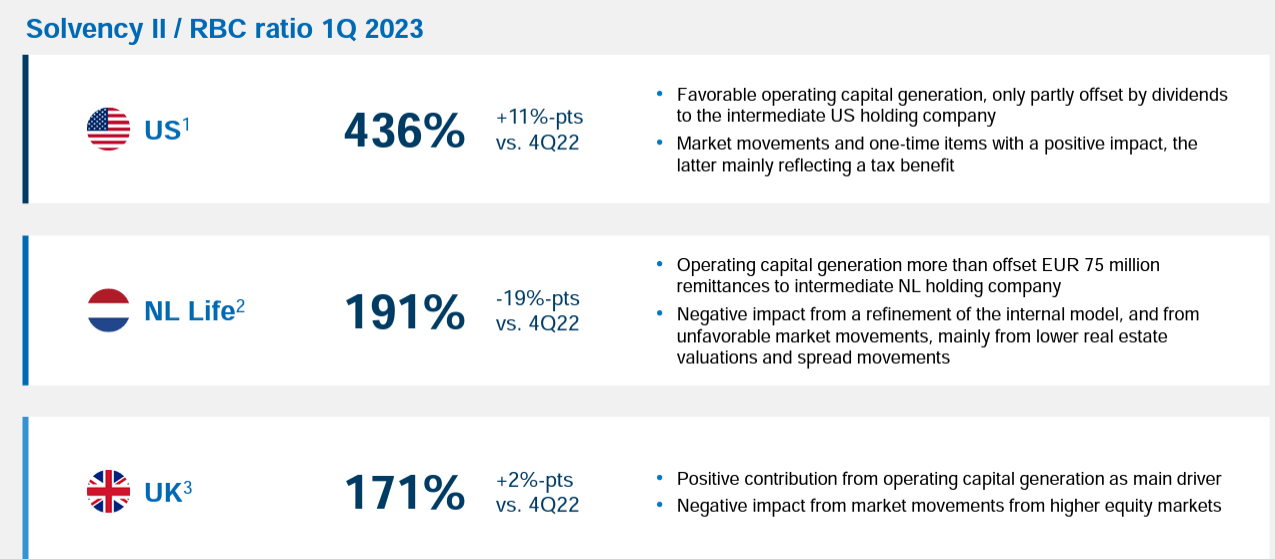

Looking at Aegon's capital solidity, the three main capital ratios remained above their respective regulatory requirements. In detail, the group Solvency II ratio increased to 210% from 206% at 2022 year-end. Despite an unfavorable equity market environment, the capital positions remain highly above operating levels. For the above reason, Aegon is progressing on the €200 million buyback and the cash at Holding decreased to €1.4 billion (still in the upper range of the company's internal targets).

{kind=link}

Conclusion and Valuation

Looking at the Q1, the cash capital is still in the upper half of the operating range and the company confirmed its DPS payment (it goes ex-dividend next week). At today's price, Aegon is yielding almost 7% with 21% in additional shareholder's remuneration. Therefore, we are not implementing any changes in our twelve months numbers forecast and we see Aegon more solid on a balance sheet level. 2023 guidance was also confirmed, and so we decided to confirm our buy with a TP of €5.7 (and $6.1 in ADR).

For further details see:

Aegon Continues To Be A Buy