UBS - Aegon: Little Impact From AT1 Bonds Tied To Credit Suisse Crisis

2023-04-03 12:44:10 ET

Summary

- The wipeout of AT1 bondholders before shareholders shocked the markets.

- Sticking to facts, AT1 bonds allow for this but many parties have shielded against this by prudent diversification and risk assessment.

- AT1 bondholders getting wiped out should most definitely not be seen as a template for saving banks.

The banking crisis has been raging, but we do see that markets now have somewhat stabilized. Whether this is the silence before the storm remains to be seen. In my opinion it’s more the fear that drove down the market rather than an actual banking crisis that would happen, but that's how most crises start. Not so much a fear-driven element, but a rethink on the risk profile that spread throughout. Besides that, the way the Swiss government acted and the continued rate hikes from central banks are not helping. In this report, I show that the exposure to the doomed junior bonds which got wiped out in the takeover of Credit Suisse are not having a material impact on Dutch banks and insurers. In fact, Aegon ( AEG ) is the only insurer which detailed the numbers.

Shocking The Debt Market

The way the Swiss government orchestrated the takeover of Credit Suisse ( CS ) by UBS ( UBS ) definitely does not deserve a beauty prize. The deal was finalized during the weekend giving shareholders no possibility to sell, even though I do believe that shareholders were given an opportunity and reason to sell in the days and months before the takeover. Beyond trapping shareholders, there also was the problem with wiping out AT1 bondholders before shareholders which did shock the bond market. Even though the AT1 bonds were structured such that this could happen, it sent a message to the market that the hierarchy of some bonds and actual stocks were different than perceived before.

Continued interest rate increases while also implemented to show support to the strength of the banking system initially also did not look like a real support as it was perceived as a sign that no matter what central banks would continue hiking rates to fight inflation, and it wouldn’t stop until the big banks would start collapsing which is hardly a positive sign or stabilizing mindset.

Dutch Exposure To Doomed Credit Suisse Bonds

What should be clearly separated is what is perceived and what's the actual reality of things. We can fear the AT1 bonds exposure as a vehicle for the banking crisis to spread apart from the higher rates pressuring banks, but if we look at the AT1 bonds exposure for instance for Dutch banks and insurers, we see that it's fairly limited. Dutch bank ABN Amro ( OTCPK:AAVMY ) has no AT1 exposure at all while ING did not comment .

Switching to insurers, Nationale Nederlanden did say its exposure to AT1 bonds is negligible and they did not hold any AT1s of Credit Suisse. Aegon has an exposure of €3 million and that is really a small number.

{kind=link}

Aegon

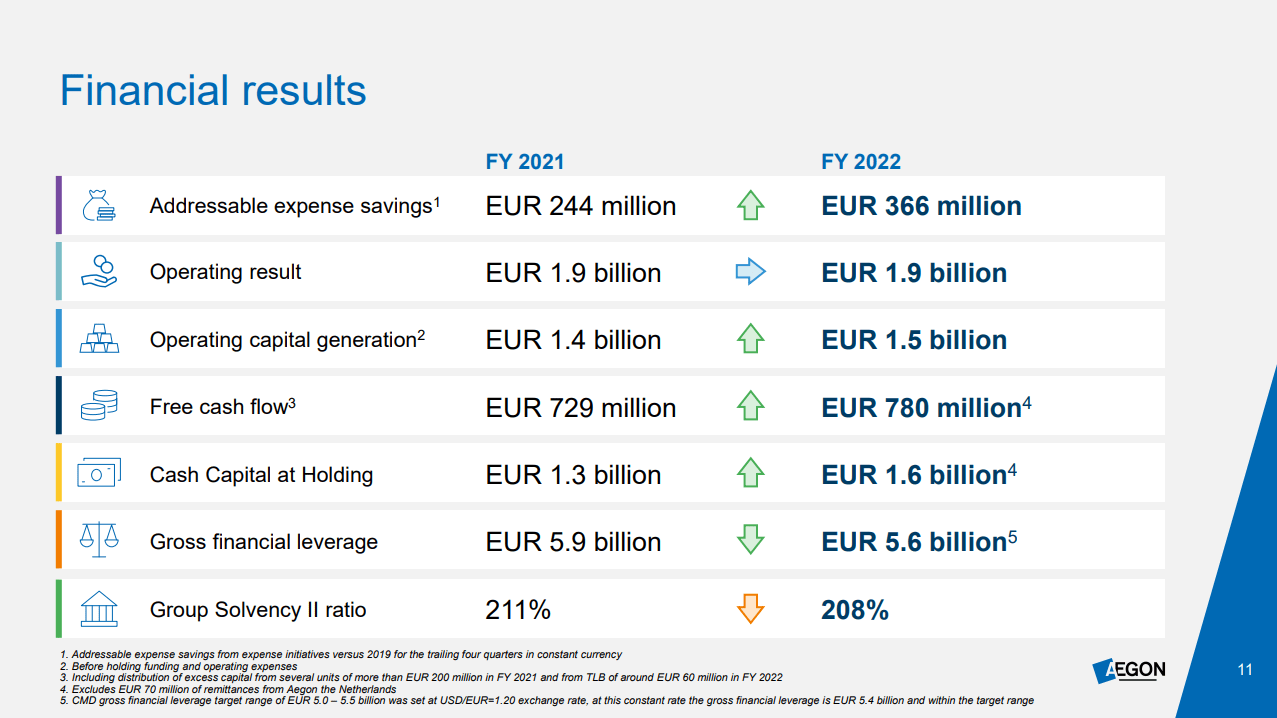

If we look at Aegon’s 2022 financial results, we can only conclude that the €3 million exposure is close to nothing. With an operating result of €1.9 billion, the exposure to CS AT1 bonds is less than 0.2%. In 2022, Aegon booked €36 million in impairments. So, the AT1 exposure is really not resulting in a big fallout and that's the way it's supposed to be. Some banks saw the risks of AT1 bonds and did not hold them and some did hold AT1 bonds but not to the extent it could significantly harm the business and the exposure to Credit Suisse AT1 bonds was even smaller. So, the domino effect is most definitely not running through the lines of the AT1 bonds even though the Swiss government shocked this subclass of assets.

Conclusion: Diversified Exposure Limits AT1 Bonds Pain

There without doubt are parties that have exposure to the doomed AT1 bonds of Credit Suisse, but viewed in the bigger picture we seen an overall healthy diversification which also means that a domino effect on the bond market is unlikely to happen. That does not take away the shock that the Swiss government brought upon stock and bondholders, but the risk profile of bondholders were in many cases such that the exposure was limited and that is also what should be kept in mind. In a fear-driven market, we also have to look at the facts and the facts are that the exposure for many parties is limited and AT1 bondholders getting wiped out most definitely is not a template for saving a bank. It was the questionable template the Swiss government adopted.

For further details see:

Aegon: Little Impact From AT1 Bonds Tied To Credit Suisse Crisis