AEG - Aegon: Transamerica Transformation Needs Time (Rating Downgrade)

2023-08-30 06:01:27 ET

Summary

- Aegon has successfully executed its 2020 strategy and is now moving on to the next phase of its transformation.

- The company's focus will be narrowed to the UK and US markets, with a goal of growing strategic assets and reducing exposure to financial assets.

- AEG's valuation lags behind its US peers, but the company aims to improve this by consistently delivering strong performance and increasing shareholder returns.

- Yet, the presence of the largest shareholder Association Aegon will prevent the company from achieving a valuation in line with its US peers.

Aegon (AEG) (AEGOF) has shown strong performance over the last years and is now focusing on the next chapter in its transformation. Although shareholders are treated to a large share buyback and growing dividend, the stock has traded in a bandwidth between US$4-6 since 2021. It seems management needs to convince investors further before it can match the valuation of US peers.

Strategy delivery

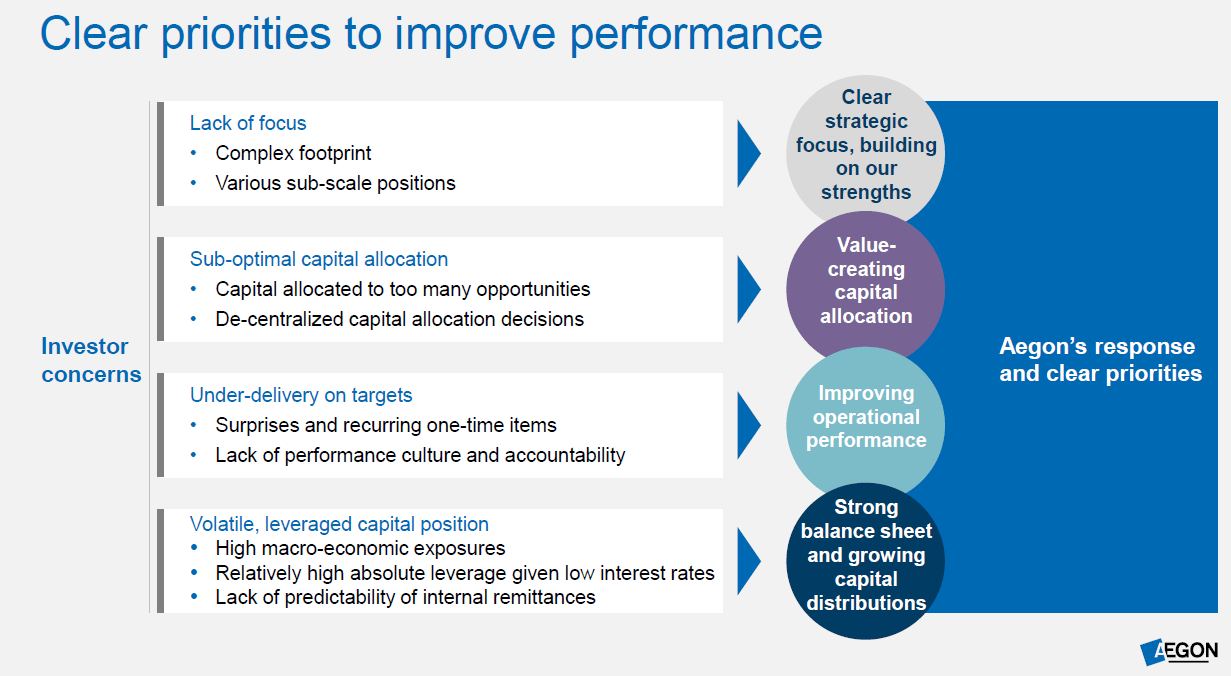

Nearly two years ago I covered Aegon and a lot has happened since. At the 2020 Capital Markets Day CEO Friese cut to the chase and gave a straightforward assessment of the state of affairs at Aegon, see figure 1.

Figure 1 - Investor concerns, CMD20 (aegon.com)

{kind=link}

Clearly, the previous CEO, Alex Wynaendts, who served on the board of Aegon from 2003 till 2020, hadn't been able to create value for investors and the figure states why. To be frank, it can be assumed many investors felt relief with the new CEO taking the bull by the horns. In this sense, the directness and straightforwardness of the Dutch Lard Fries can be seen as a positive.

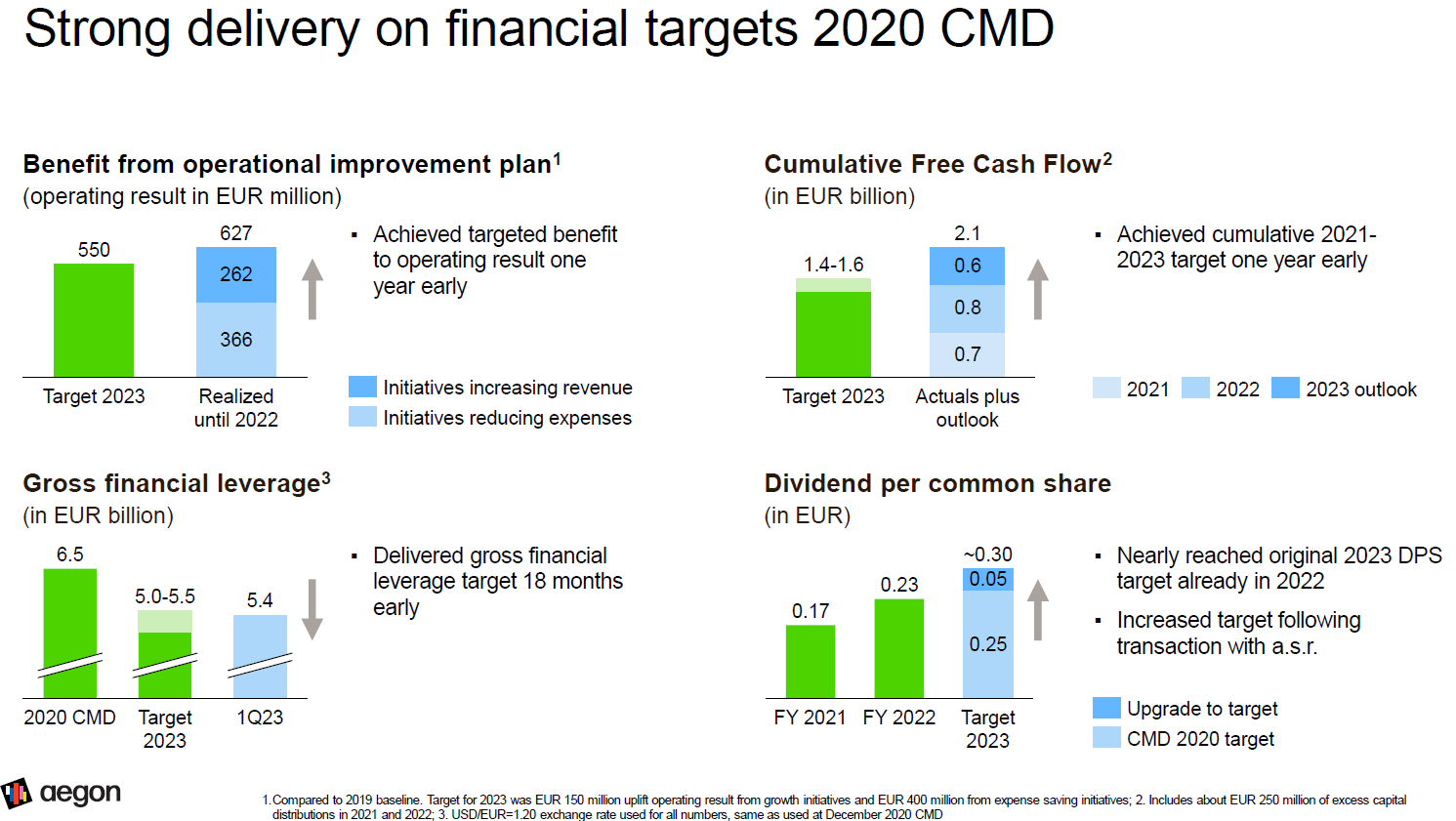

At the 2023 Capital Markets Day, the company gave an update on the execution of the 2020 strategy, see figure 2. In brief, management delivered on the strategy approximately a year early. From a shareholder point of view it's important to note the turnaround did not come at the expense of returns, the dividend was actually increased although the share price remained trading sideways in the US$4-6 price range.

Figure 2 - Strategy delivery, CMD23 (aegon.com)

{kind=link}

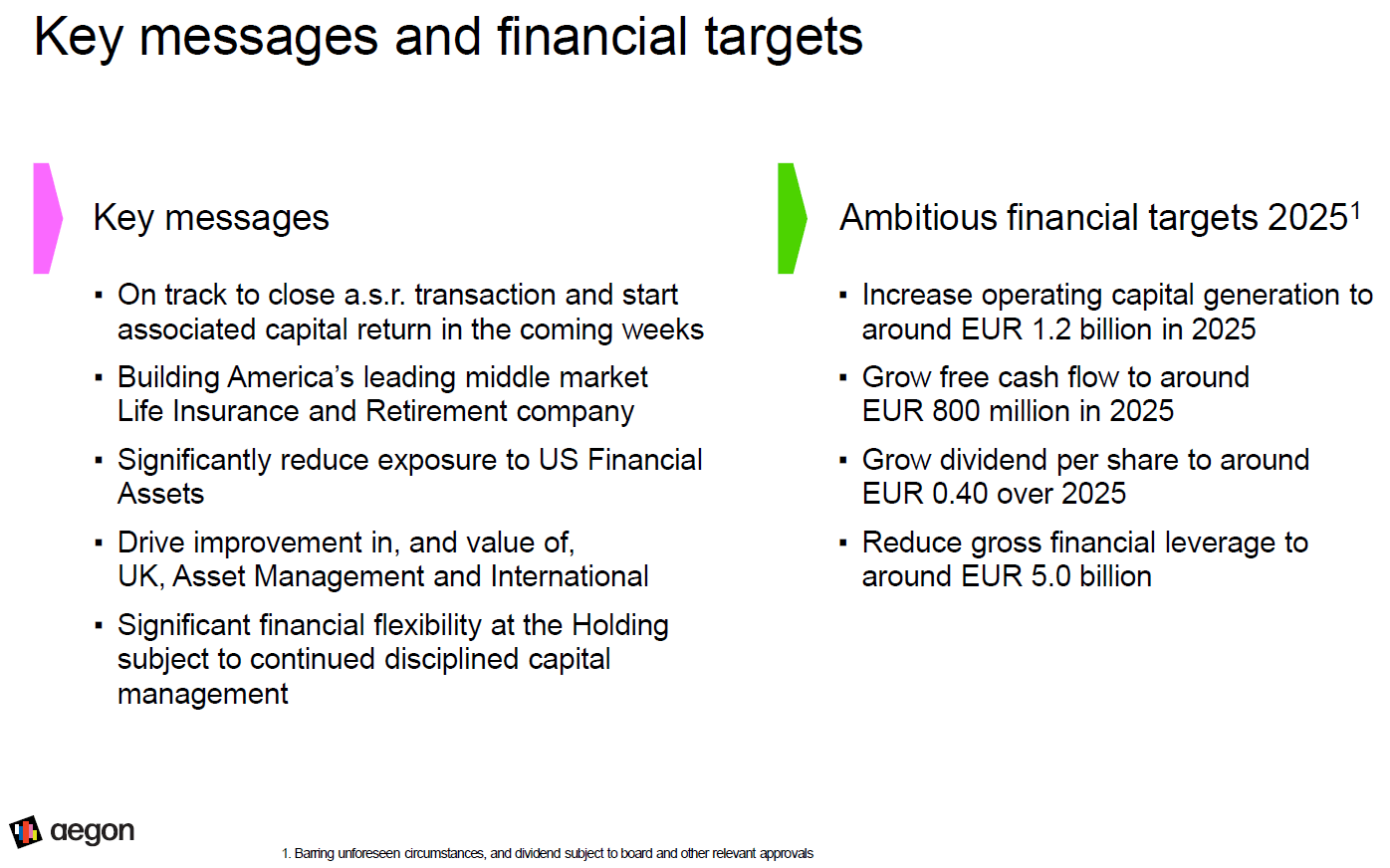

The 2021-2023 strategy is designated Chapter 1 by the company. With the delivery it now moves to Chapter 2 . The priorities and targets of this second chapter were neatly summarized at the 2023 Capital Markets Day, see figure 3.

Figure 3 - Aegon 2025 strategy and targets, CMD23 (aegon.com)

{kind=link}

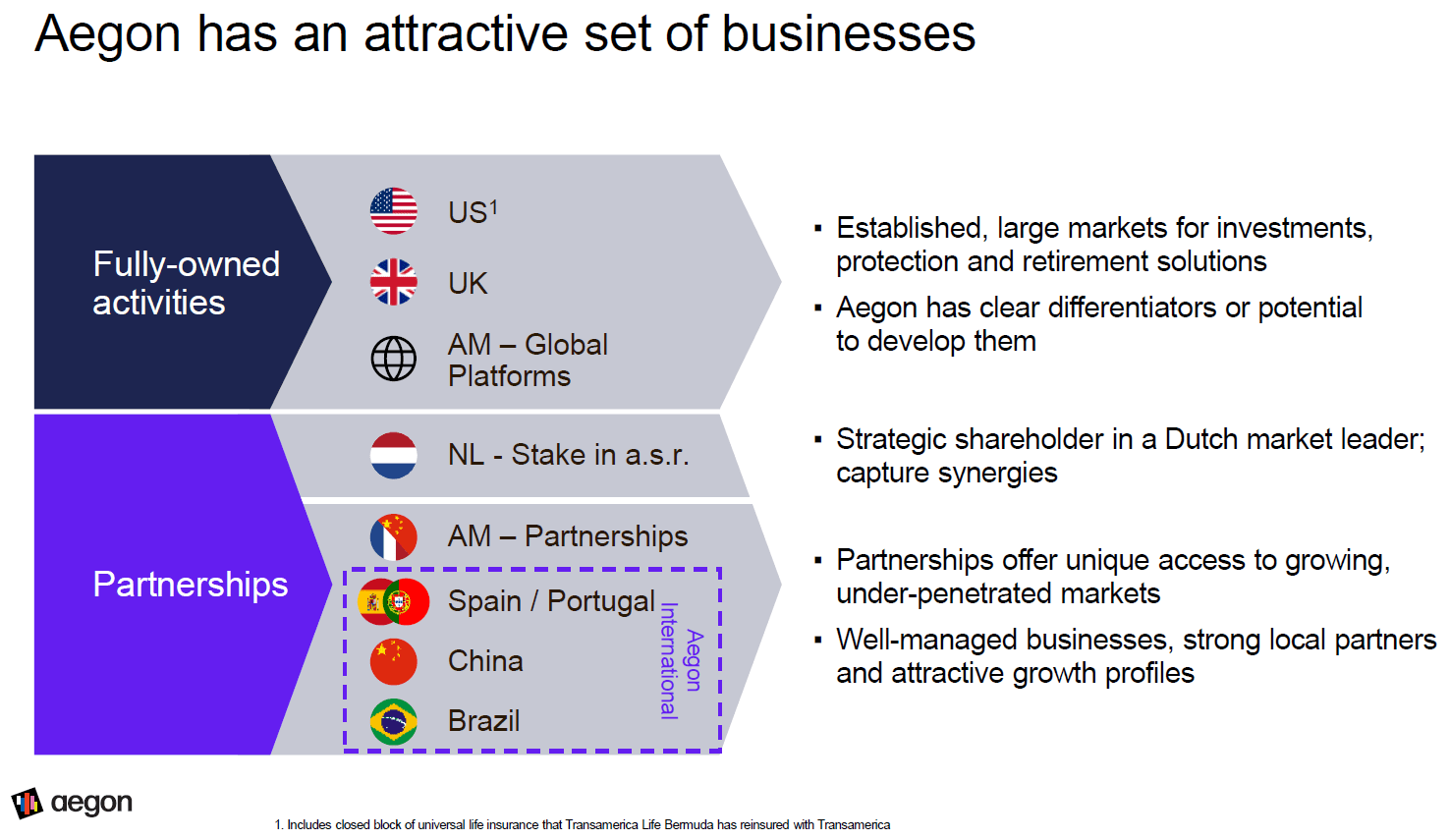

The main focus of the company will be narrowed to the UK and US while the company will operate in a selection of the geographies to gauge potential for its products. Again, a picture says more than a thousand words, so reference is made to figure 4 for the overview.

Figure 4 - Aegon overview, CMD23 (aegon.com)

{kind=link}

Quick wins

With the disposal of the Central and East European businesses and Aegon NL , the quick wins have been achieved. Therefore, going forward, it will be harder to create value and the targets reflects this line of reasoning.

Starting with free cash flow, the 2025 target aligns with the 2022 result, see figure 2. The divestments will affect FCF, but the 2023 outlook still indicates a value of €0.6Bn is expected to be achieved. Moreover, it's surprising how much the actual cash flow exceeded the previous 2020 target. Even so, management designates the US$0.8Bn FCF target as ambitious.

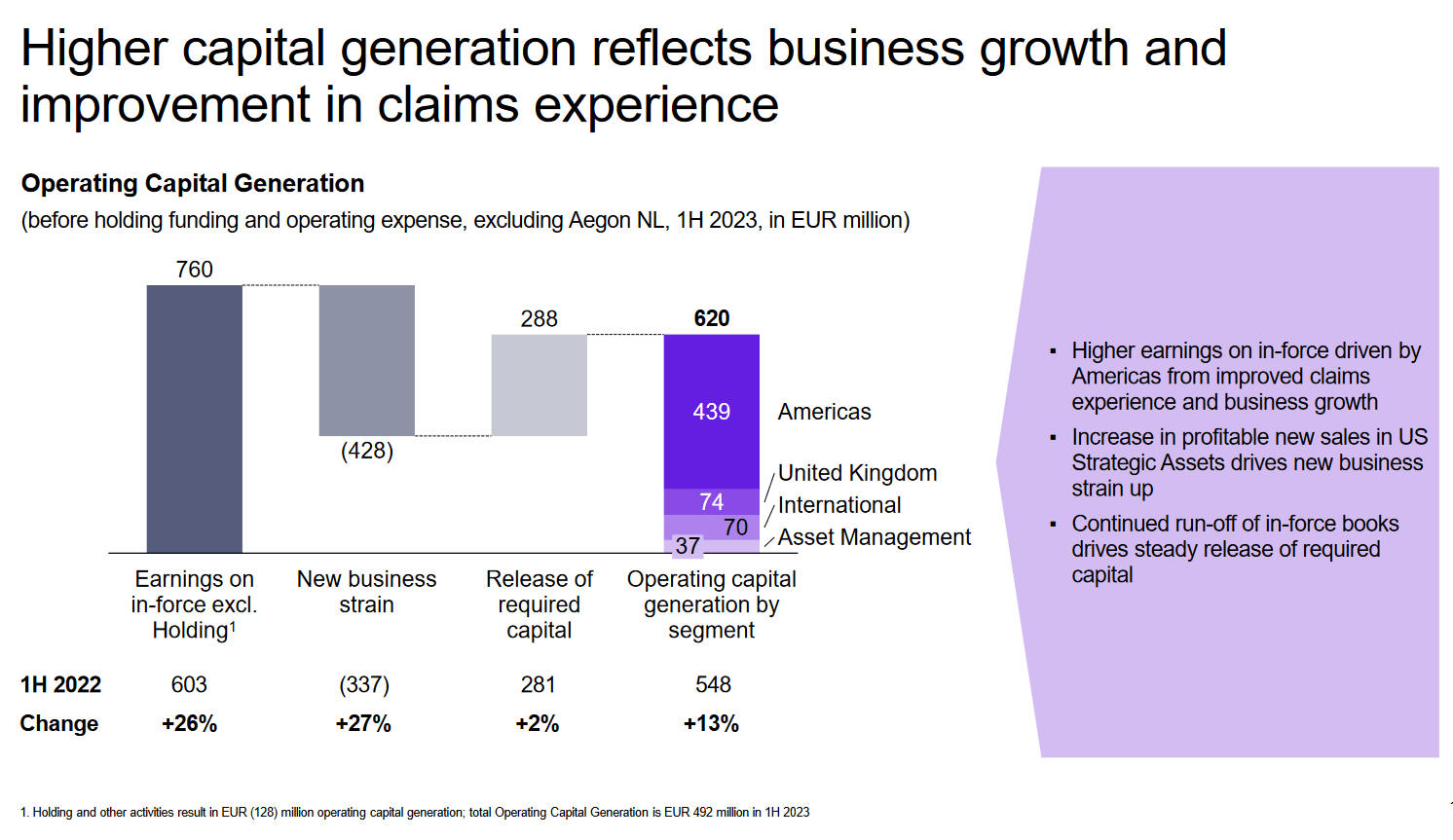

At the 1H23 results presentation the status regrading operating capital generation was shared, see figure 5. In the first half of 2023 Aegon generated €0.6Bn in operating capital, excluding Aegon NL. For the entire year management expects it can meet €1Bn in operating capital generation, meaning the 2025 target is not far away.

Moreover, the target for financial leverage (€5Bn) has been sharpened, but still aligns with the lower bound figure of the previous target for 2023 (€5-5.5Bn). In this respect it must be noted €0.7Bn received from the transaction with ASR will be used to reduce leverage .

Figure 5 - Capital generation, 1H23 results presentation (aegon.com)

{kind=link}

Another point laid bare by figure 5 is the increased relevance of the American market. Whereas the market share regarding earnings was around 40% before the sale of the Dutch activities, the Americas now count for 70% of the operational capital generation. Comparing earnings to capital generation is not the cleanest way, but it gives an idea regarding relative importance of the different geographies.

If Aegon wants to grow, it will need to be driven by the American business. Therefore the management team intends to grow Strategic Assets and reduce exposure to Financial Assets. The definition of these assets was shared in the 2022 annual report:

Strategic Assets are those considered to have a greater potential for an attractive return on capital and growth. In Individual Solutions, Transamerica focuses on select life insurance and investment products, including term life insurance, final expense whole life insurance, indexed universal life insurance, mutual funds, structured index-linked annuities and certain variable annuities with limited interest rate sensitive guarantees.(…)

Financial Assets are capital intensive assets with relatively low returns on capital. In Individual Solutions, these are traditional variable annuities (VAs) with significant interest rate-sensitive guaranteed living benefits and death benefits; standalone individual long-term care ((LTC)) insurance; and fixed annuities.

Basically, the company will invest to grow the Strategic Assets which are less sensitive to interest rate fluctuations while the rate sensitive capital tied up in existing Financial Assets needs to be released. Effectively, a large chunk of the business has been sold (Aegon NL) and the majority of what remains (Transamerica) needs to be transformed. And transformations take time which is reflected in the targets.

Association Aegon

After Aegon sold the Dutch (insurance) business, it could not be subject to the oversight of the Dutch National Bank anymore as stipulated by the Solvency II rules. The company moved the legal domicile to Bermuda, but is shifting the focus towards the US;

Aegon will continue to report under IFRS accounting standards. Aegon is exploring the implementation of US GAAP in the medium term, in addition to IFRS, so as to allow for better comparison against US peers, and provide long-term strategic flexibility for the Group.

The focus on the US was further highlighted in the Capital Markets Day presentation where virtually the entire presentation evolved around the plans for Transamerica. This focus does raise some questions concerning the stake in ASR and especially the position of the largest stakeholder Vereniging Aegon (Dutch for Association Aegon).

Clearly, the position in ASR is considered a partnership as demonstrated in figure 4. Moreover, the partnership has a distinct position as Aegon is a shareholder and as such has limited control even though it has two seats in the Supervisory Board. Ever since the sale of Aegon NL, it has been speculated what the intention of management is in relation to the 29.99% stake in ASR. Based on the relationship agreement between both parties, Aegon has the ability to reduce its stake even though in some cases it needs the consent of ASR. Nevertheless, Aegon management may wait until the transition of the Dutch business has been completed, by 2026 the latest .

In the event Aegon will want to sell the ASR stake, the question is what the position of the largest shareholder, Vereniging Aegon (Association Aegon), will be. After a potential sale Aegon won't have any business or shareholding anymore in the Netherlands. Therefore, the listing on the Amsterdam stock exchange likely will be dropped. In that case the question becomes what the function of the association, the largest shareholder will be. The current function, or purpose, is clearly stated in the articles of association :

The purpose of the Association is a balanced representation of the direct and indirect interests of Aegon N.V. and of companies with which Aegon N.V. forms a group, of insured parties, employees, shareholders and other related parties of these companies. Influences that threaten the continuity, independence or identity of Aegon N.V., in conflict with the aforementioned interests will be resisted as much as possible.

Basically the association acts as safeguard against a hostile take-over. Even though the association has been voting in favour of the proposals from Aegon management, including the move to Bermuda, the purpose is still the same. Constructions like these typically put on a discount on the share price as the likelihood of a take-over, and the corresponding premium paid to shareholders, is non-existent.

Competitors

So far, Aegon has been viewed as a European insurance company, but that designation is not correct anymore. Therefore, rather than comparing the valuation against European peers, a comparison against US peers may be more accurate. As the company is currently restructuring, a fair comparison to peers is difficult to make. As stated before, parts of the business have been divested, impairments have been taken and buybacks have been executed.

Nevertheless, an assessment of the price to book value is used to gauge where the company currently stands. As references Unum (UNM) and Manulife (MFC) will be used. The choice for Unum is based on the fact that both companies originate from the 1840's and the market cap is very similar. As a second peer, Manulife is used as this company has exposure to the American market through John Hancock which it acquired in 2003, a move that resembles Aegon's 1999 acquisition of Transamerica. Finally MetLife (MET) has been added as it is among the largest US life insurance companies.

Figure 6 gives and overview of the P/B ratio over the last five years. Without a doubt Aegon is lagging its US peers even though the gap recently narrowed as a results of divesting the Dutch business.

Figure 6 - Price to book value against peers (seeking alpha, Ycharts)

On a positive note, assuming Aegon will achieve an American P/B ratio of about 1.1, one could argue a 20% gain in stock price could be realized. Obviously, this is a very rudimentary approach and the move of Aegon to the US will not happen overnight, implying it will take several years to achieve this full valuation. Therefore, continued focus and consistent performance while growing shareholder returns will be the way to support the stock price.

Dividend and buybacks

In that respect, management has committed itself to a DPS of €0.40 in 2025. The 2022 dividend was €0.23, meaning it will have a CAGR of about 20% until 2025. On top of this, Aegon started it's €1.5Bn (US$1.65Bn) share buyback program on the 6th of July 2023. At first glance such figures are alluring, but these figures must be placed in context.

At the time of writing Aegon's market cap is US$9.9Bn, implying about 16% of the shares outstanding will be retired within a years' time as the buyback program is expected to be finalized in June 2024. On top of this, ASR already announced mid-to-high single digit dividend growth per annum until 2025 .

Without elaborately explaining the math here, the buybacks and expected dividend growth of ASR already allow Aegon to raise the dividend to approximately €0.30 per share. For this estimate it is assumed ASR will grow the dividend by 7% annually.

If the €0.30 dividend is taken as a start, the growth to €0.40 implies a CAGR of 10%. This target seems manageable and given the outlook shared by management the company will be able to cover dividend by free cash flow.

Yet, besides the performance of the company, non-European investors have to make a trade-off between the dividend yield and exposure to the USD/EUR exchange rate. In this respect, Manulife currently offers a 6% yield, the exchange rate does not play a role and, according to my knowledge, the company does not have a construction in place to protect its independence.

Conclusion

Aegon delivered a year early on its 2020 strategy in which the quick wins were booked. The second part of the transformation will prove more difficult which is reflected by the targets which are less ambitious than management presents.

The investment proposition appears appealing, but in spite of management lavishly rewarding shareholders, the stock has traded in a bandwidth between US$4-6 since 2021. With the quick wins executed, it may be expected management will focus on the execution of the new strategy which basically evolves around the transformation of Transamerica.

In addition, in spite of selling the Dutch operations, Association Aegon, the safeguard against a hostile take-over, is still the largest shareholder. As long as such a safeguard remains in place, it will be difficult to compete with US peers in terms of valuation.

For further details see:

Aegon: Transamerica Transformation Needs Time (Rating Downgrade)