AMTX - Aemetis Grows Pays Down Debt Promises More To Come In 2024

2023-12-06 11:52:48 ET

Summary

- Aemetis catalysts are starting to tip over like dominos, the first were Renewable Natural Gas related.

- Shorts are getting crushed by high borrowing costs and it appears a short squeeze has begun.

- The company's net asset value is around $1.5 billion by my calculations, but the market cap is under $300 million, despite the business being worth something too.

- Future revenues from over $7 billion in contracts and various tax credits suggest Aemetis could be the highest margin biofuels company in the world by 2025-6.

- I continue to rate Aemetis a strong buy for growth investors looking for a potential multi-bagger and have a $17-$22 price target range for around New Year.

Aemetis ( AMTX ) was my top growth stock of 2023 and is now a top small cap holding for me. In the name of originality, it will not be my top growth stock for 2024, but it could be if I weren't an original.

This week I had a conference call with Aemetis ((AMTX)) CEO Eric McAfee. He discussed progress and outlook for Aemetis with me and a large family office shareholder out of London I know. His group of four investors owns about one million shares in Aemetis.

In watching Aemetis progress the past few years, it is clear to me that they are well managed. The company is growing revenues fast, using that money for capex and to upgrade their balance sheet. With hundreds of millions in decarbonization related Investment Tax Credits and Production Tax Credits available, the company seems poised to join big oil in collecting massive margins.

Here's as brief of an update as I could write on Aemetis' progress.

CARB Decision On LCFS In January

The California Air Resources Board ((CARB)) is set to release its draft regulations for the LCFS - Low Carbon Fuel Standard by year-end. They will vote on the regulations January 20, if there are no further delays. They are about a year behind schedule.

The purpose of these regulations is to set the pricing mechanisms for the LCFS fuel credits for the next 20 years. That is of course of some importance.

If the regulations do not tighten up the market for the credits, then it will be a stretched out path to get to the maximum payments cap of $223 per metric ton of GHG (greenhouse gases) emissions. The current prices are around $70, down from around $200 a couple years ago.

What does that mean?

Aemetis fuels are carbon neutral to carbon negative. So, they create a credit to Aemetis. Companies that burn fossil fuels generate debits that must be offset. So, Aemetis wants a higher price per metric ton for selling those offsets. Pretty simple. Think of it as both sides of a ledger.

Right now, Aemetis is "storing" their LCFS credits looking to get a higher price in 2024 and 2025.

There are three likely outcomes from CARB.

- The regulations only tighten mildly and the price goes up slowly and in small increments.

- The regulations are tightened up in accordance with what has already been proposed and go up to around $200 by 2025.

- The regulations are tightened up a lot, for instances focusing on only California producers of credits (right now companies not in California can sell into California which is probably good nationally), and the price gets to the cap price of $223 quickly.

California Air Resources Board - LCFS Search

Here is a presentation that shows how much corporate firepower is behind outcome #2 above. It is possible that some entity or entities are pushing behind the scenes for outcome #3 and that they have the influence to make it happen. McAfee doesn't think so, but acknowledged it could happen.

Outcome #1 would be a win for a group of NIMBYs who are fighting the existence of cow herds in the Central Valley of California. Remember, California is the top dairy producer in the nation, so it's not like cows are new there. Nonetheless there is a group called the Association of Irritated Residents who fight most development in the Central Valley.

Basically, the Association of Irritated Residents are well off, but not as rich as corporations. They want to block most development in the valley. I'm not saying they don't have validity, I'm pointing out how these fights usually go in America, that is, to the corporations.

In this case, if climate change is in fact an existential threat (you know I believe that), then outcome #1 is a bad outcome. If climate change is not an existential threat, then outcome #1 is reasonable.

We'll know shortly which way the cow wind blows. I'll update when it happens.

Meanwhile, I think this article gives great context:

California climate policies: what you need to do to comply

If the CARB decision is #2 or #3, then I expect analysts to upgrade AMTX quickly as they would be a clear winner.

Preferred Debt Extinguishment

Shorts like to point to the financing deal in place to extinguish Aemetis $102.5 million left in Class B Preferred shares as an expensive financing arrangement. It's not cheap, but it's not out of line with most similar deals. The interest rate is Prime + 10% and a closing cost of $5.5m (which is a bit steep, about $2-3 million would be more normal).

Here's the thing, it's not likely to happen. Right now the Preferreds are carried at 8.5% by Aemetis. Third Eye, the lender, has no desire to trigger a taxable event this calendar year, which is what happens if the Preferreds are paid off with debt, i.e. it's a taxable event.

So, the Preferreds will be extended again, likely into Q2 sometime, which is when we will have clarity on a lot of things. There is a good chance the Preferreds are not extinguished until 2025.

The Preferreds are secured by the Investment Tax Credits that Aemetis receives for building dairy digesters for RNG that are financed largely by 20 year low cost loans from the USDA.

Those ITCs were $63 million so far on seven digesters. Aemetis just got approval for a 24 mile extension of their pipeline which will cover another 21 digesters, ten of which are in various stages of development. Anticipated ITCs are almost $200 million over the next two years, so paying off the Preferred A is simply a matter of calendar.

A side note is that Preferred A issued in 2007 was converted to a 126,008 shares of common today, which completely extinguished the Preferred A. The people who received the common may sell into the market and I think some did on December 5, however, it's literally a few hours of price pressure.

There was an S-1 filing on December 5 covering the Preferred A extinguishment, and I'm not sure why, but virtually every corporate event was linked from those documents. If you want to do the reading on everything about Aemetis, from how the company started to current executive contracts, it's in there in a very easy clickable format.

India, Biofuel And Tallow

One of the expansion projects in India, disclosed earlier, was a 50m/gallon Tallow refining facility. This is on the land they acquired in February 2022 in Kakinada, India.

As noted on the earnings call, their existing biofuels refinery on adjacent property was also expanded to 60 million gallons a year ahead of schedule and is being upgraded to 100 million gallons per year by 2025 or sooner. That expansion is being financed by India cash flow on their debt free refinery.

Aemetis Receives $150M Biodiesel Supply Allocation In India

Tallow is currently being used to produce biofuels that are not only being sold in India through their oil marketing companies, but they also have a partner in Europe that is buying other capacity. In other words, there is no shortage of demand.

Once the buildout in India is complete, then the company will be throwing off cash. That is the basis for a likely IPO of the Kakinada refinery on the India stock exchange.

In such a scenario, only a portion of the company would be floated and that would be a cash repatriation event for Aemetis. I expect that to happen in H2 2024, which is a quarter or two later than I originally believed, but monetary conditions have pushed a lot of financing events back around the world.

Quick Review Of Recent Developments

This is a quick bullet point list of what we learned from the Q3 earnings. I will cover the company more in depth again after the CARB decision.

- A big rise in revenues largely from $62 million in marketable tax credits.

- $50 million paid towards debt and preferred obligations.

- Better terms and interest rates on some debt.

- Continued development of RNG (renewable natural gas) dairy projects using favorable USDA 20-year low rate loans, which in turn, throw off more marketable investment tax credits.

- Expected 2024 ITC (investment tax credits) from RNG development is roughly enough to pay off $108 million in debt used to extinguish preferred stock obligations.

- In 2025 and 2026, marketable ITC on contracted RNG projects can be used to reduce Aemetis' debt, fund capex, reduce tax burden and generate free cash flow.

- The Keyes Ethanol plant is fully back online, after major upgrades to solar microgrid and Rockwell ( ROK ) AI production management system, and threw off free cash flow in September after restart and optimization.

- Discussions with potential joint venture partners on permitted Riverbank SAF and renewable diesel plant (which also benefits from tax incentives) being built to fulfill $3.8 billion of sustainable aviation fuel supply contracts with airlines, and a $3.2 billion renewable diesel supply contract with a national chain of travel stops.

- Expansion of their Kakinada, India refinery is a year ahead of schedule and being paid out of cash flow generated from the refinery.

- 2/3 of available capacity for the year beginning in October, 40 million gallons, at India refinery was allocated to India oil marketing companies for $150 million .

- Management is looking at monetization opportunities to float a portion of the India refinery in H2 2024 as a publicly listed company in India.

- Timelines on buildout of RNG, SAF and carbon capture are 2 to 3 quarters behind due to tighter conditions in the financial sector.

I have not completely covered the company's debt structure, but there are maturities in 2024 and 2025 that, along with capex, will soak up most cash generation. I will cover the debt profile in a separate piece, but potential buyers should do a complete analysis of the Aemetis 10-Q.

The short story on debt is that I believe it is manageable, however, if financial conditions stay tighter for longer, that would almost certainly have a material impact on the company.

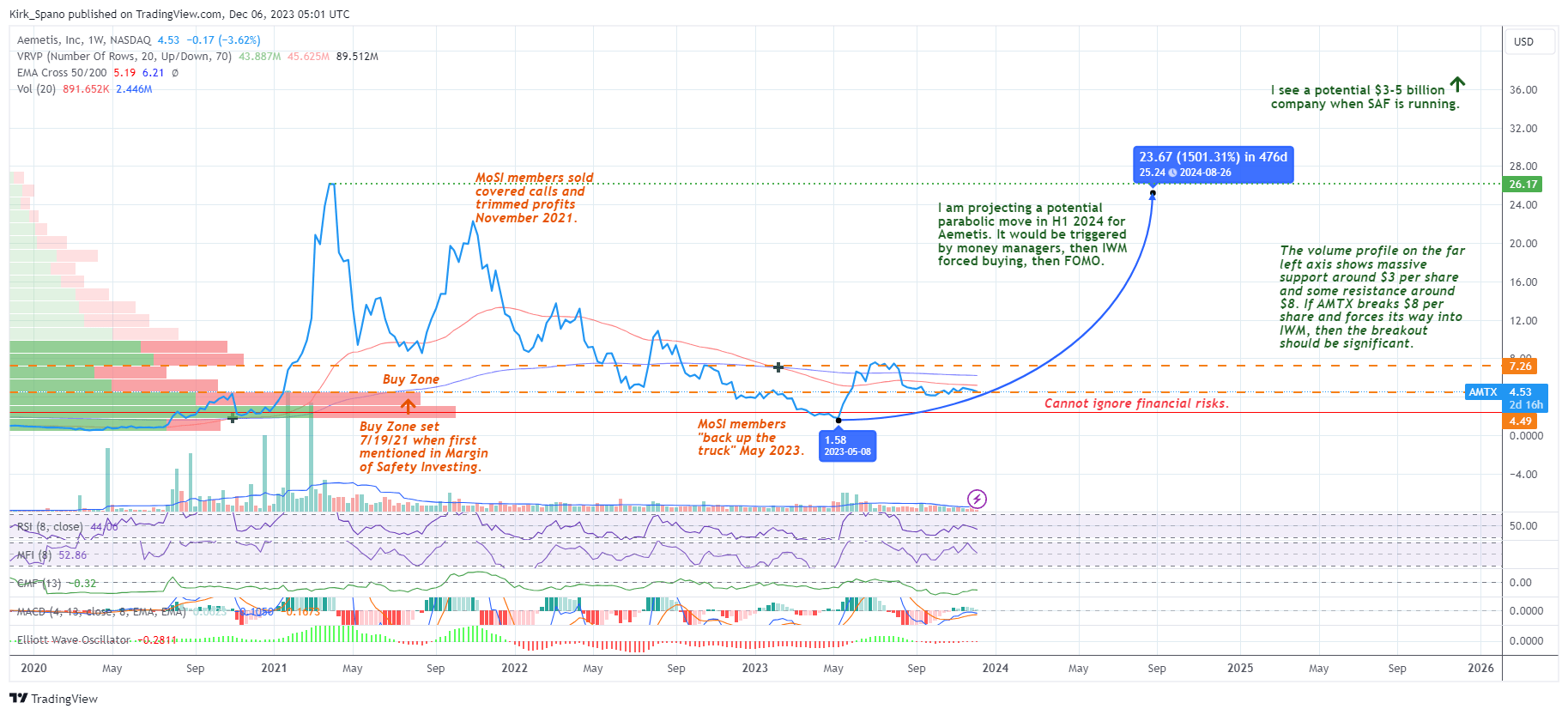

Microcap To IWM

Aemetis was removed from the Russell 2000 last spring and the related index tracking ETFs like the iShares Russell 2000 ETF ( IWM ) .

That removal was known ahead of time by traders and they punished the stock with massive shorting into forced selling by the ETFs that sold off around 3 million shares or about 10% of the common stock at the time.

It was that sell-off that we bought into heavily during May and June at around $2 per share. We might have partially triggered the following rally and now with the excitement as the stock peaked at $8.99. AMTX has settled in the $4s for a few months now and is exhibiting a nice consolidation.

{kind=link}

If Aemetis catches some upward momentum on business developments, then they are likely close to being included back into the Russell 2000. That would trigger forced buying by ETFs.

There is a very active hedge fund community that looks for such trades which could create a self-fulfilling prophecy.

In 2022, the smallest company on the Russell 2000 was $240 million. In 2023 it was $159 million as the Russell 2000 was down over the past year. Aemetis' market cap is $178 million today.

Any upward momentum at all would likely drive more upward price momentum in my experience, which would cause inclusion in the Russell 2000 and the forced buying by those ETFs I mentioned above.

The Russell 2000 linked index ETFs would have to buy 3-4 million shares based on about 40 million shares outstanding (up 4 million the past year from financing related dilution) to fill their allocations.

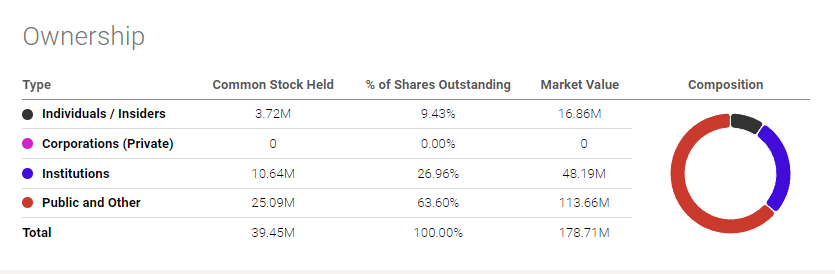

That's a substantial amount of not only total shares outstanding, but of the float that institutions and insiders don't already own.

{kind=link}

For what it's worth, I know where about 3 million shares are among what I consider relatively strong hands - me, my clients, readers, a few family offices, several hedge funds and at least two Registered Investment Advisory firms. There's no guarantee they're in it for the long run, but, they don't seem like the trader types.

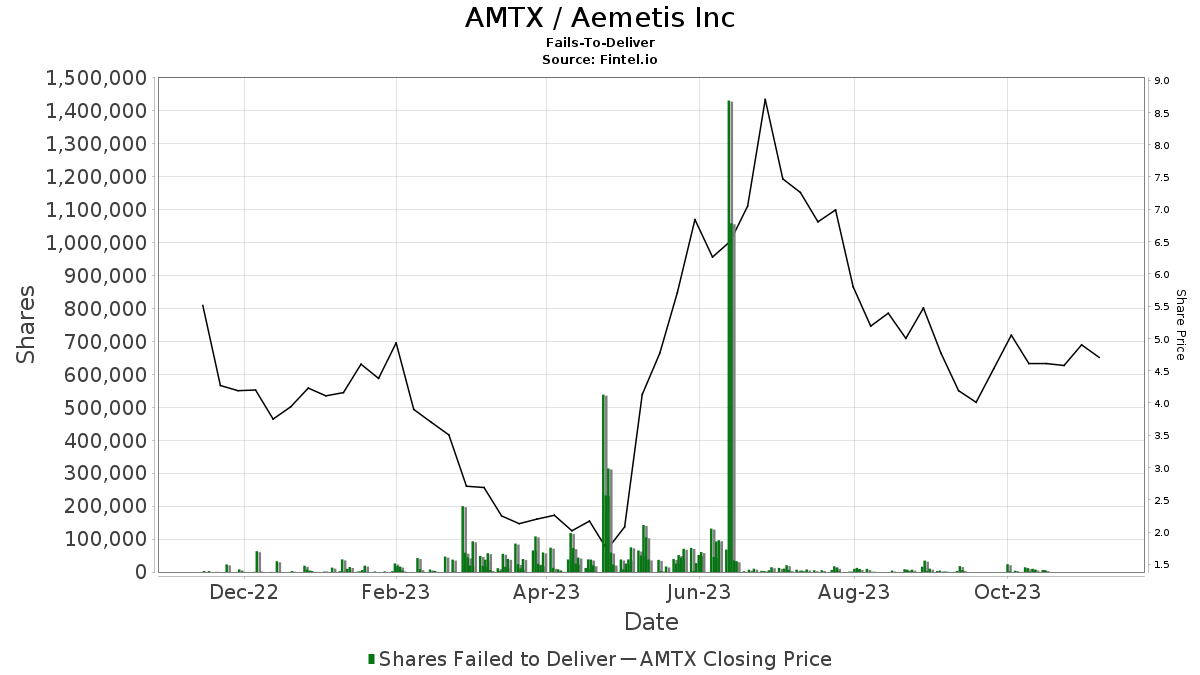

That "spin up" scenario in share price is without considering that AMTX is a heavily shorted stock with 16% sold short. Failures to deliver have not fallen to normal low levels, indicating there is naked shorting going on.

{kind=link}

We are aware that the SEC is cracking down on that with recent regulations. In addition, a recent court ruling against CIBC World Markets held brokerages liable for damages from naked shorting.

Naked shorting involves the selling of shares that the seller does not actually own or have borrowed and available to own. While technically illegal, there has been no regulatory requirements to track and prevent it. Essentially a law without an enforcement mechanism. That seems to have just changed as both a regulator and a court have put their foot down.

We'll see how that plays out in the broader micro and small cap space which are both suffering from massive failures to deliver which indicate naked shorting.

Fintel's quantitative analysis rates Aemetis shares as 170th most likely out of 4400 stocks to see a short squeeze soon.

Investment Quick Thoughts

I continue to hold a triple weight in Aemetis ((AMTX)) shares in appropriate accounts. I also have been selling the AMTX $5 April puts where appropriate, though my put selling activity has slowed as premiums decreased and my allocation reached its limits.

I am also starting to build a position in long AMTX calls for April at various strike prices.

My calls for AMTX $7.50 January calls, which I sold 1/3 of at very profitable prices, are languishing between 15¢ and 20¢, slightly below what I bought them at. Given I took profits at $2 and $3, as reported, I am happy to let these ride and simply build out the April position.

I will close my January position the best I can sometime in January. If the share price is very close to $7.50, I may take delivery of some or all of the shares.

Remember, with long calls, you do not ever want to pay for long time duration as that is very expensive and puts the calendar against you as time value erodes. It is cheaper to buy a new batch of calls every few months, than buy LEAPs.

Think of what you want as an option seller. You want the opposite as an option buyer. Hopefully that makes sense.

I am very long AMTX and rate it as a strong buy for growth accounts. It is the rare triple position for me which is around 12% (+/- depending on the day's price).

Accounts that have a growth sleeve but are oriented towards income should stick to a starter or half position and selling cash-secured puts that are in line with your asset allocation limits.

For further details see:

Aemetis Grows, Pays Down Debt, Promises More To Come In 2024