ANYYY - Aena: Entering A New Growth Cycle

2023-07-17 08:26:40 ET

Summary

- Aena, the world's largest airport operator, is expected to see significant earnings and cash flow growth due to a rise in unregulated commercial revenue.

- Aena offers around 17% upside.

- The investment offers unique exposure to a network of high-quality assets and is attractive from a thematic perspective as it is a play on the rise of tourism.

We present our Long thesis on Aena, an airport operator with a natural monopoly on Spanish air traffic, in the light of significant earnings and cash flow growth driven by unregulated commercial revenue growth, higher traffic, and in the mid-term a new regulatory framework which will allow higher returns on RAB and more flexibility.

Company Overview

Aena (ANYYY) is the world's largest airport operator by passenger volume. Aena owns and operates 46 airports and 2 heliports in Spain, with an estimated capacity of 335 million passengers, and has a natural monopoly on Spanish air traffic. In addition to its Spanish portfolio Aena has a significant presence outside Spain with interests in 23 international airports including a 51% stake in London Luton , a 100% stake in the Northeastern Group of Airports in Brazil, and a stake in Grupo Aeroportuario del Pacifico (PAC). Aena was listed in the stock exchange in year 2015 and it currently has a market capitalization of ca. €22 billion.

Over the last decade, Aena has invested heavily to create a top-flight modern infrastructure. Currently, the network has the capacity to absorb traffic growth and capex needs have declined sharply. Moreover, the network benefits from a stable regulatory network, which we will analyze later. We would like to note that the Government of Spain owns 51% of the group.

Aena has 4 divisions. The Aeronautical division collects revenue from airlines for landing, passengers, security, cargo, and other services. The tariffs are regulated by a framework that takes into regard traffic, capex, fixed and operating costs, and cost of capital. The Commercial division includes revenue from shopping, restaurants, and advertising i.e., rental income from operators; this division is out of the regulated perimeter. The Real Estate Services division includes car parks, rent for infrastructure, and undeveloped real estate. The International division includes the stake in Luton, Brazilian Airports, and a series of other minority stakes.

Regulation

Aena is regulated by the Spanish Civil Aviation Authority and the Competition and Markets Commission. The latter is tasked with monitoring the implementation of the tariff regime. The most important principle of the regulatory framework is the recovery of operating costs plus an appropriate return on capital. Its monopolistic position in the Spanish airport sector would have otherwise given Aena considerable bargaining power with airlines, but this is not a driver of earnings growth as revenue is regulated. The commercial segment is unregulated since 2018. Moreover, Aena like its peers in Paris ( AEOXF ) and Frankfurt (FPRUF), fully owns the assets i.e., is not concession based, hence the duration is unlimited.

Before And After The Pandemic

Before the pandemic, Aena had been overearning: regulated EBIT was €200+ million in excess of the regulated limit, and commercial revenue was higher due to minimum annual guarantees. However post-pandemic, the situation has changed sharply. The decrease in traffic and considerable cost inflation have caused the return on the Regulated Asset Base to decline to levels below 6%. In addition, there is an unwinding of rent accruals that are not going to be paid. As per the company's guidance that amounts to a reported value of €200 million in this fiscal year. This is solely a reported value and doesn't have a cash impact.

Capital Markets Day

On its Capital Markets Day in November last year, Aena announced a positive mid-term outlook that was well received by the markets. It forecasts around 300 million passengers by the year 2026, MAGs at 65% by 2026, and expects to reach its 2019 EBITDA levels by 2025. It also reiterated its commitment to capital returns policy with an 80% payout ratio.

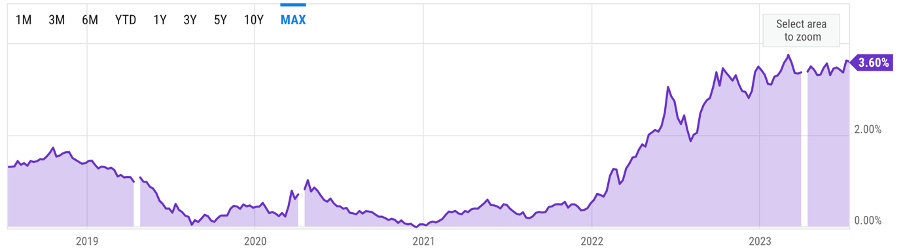

Share Price Performance

Due to lower inflation protection than peers and a period of overearning, Aena's share price stagnated post the vaccine bounce, and underperformed in Q2-Q3 2022. This was reversed after the CMD and a good print of FY and Q1'23 results, and Aena is up 17% year-to-date

Investment Thesis

The regulatory authority is going to announce the new regulatory framework in 2026 i.e., DORA III, which will be implemented in 2027 as DORA II expires. Given the rise in interest rates, as per our estimate, Aena should be earning between 8% and 9% on RAB vs the current 6%. The risk-free rate was around 50-60bps when the previous framework was announced; now the Spanish 10-year bond yield is currently higher than 3.5%. Regulated EBIT should almost double vs current levels. Moreover, the price cap expires in 2026, and Aena will be able to increase airport fees that have been set by the regulator.

{kind=link}

What we find most exciting however is the unregulated commercial revenue which consists of revenue-indexed rents and rising fixed rents. This income is determined by traffic growth, inflation, and new tenders and has a high rate of cash conversion. Duty-free tender results came out strong with bids implying c.30% higher revenue than current levels for the tendered lots; this translates to €100 million + of additional revenue. Commercial revenue remains at lower levels vs European peers, and we believe there is significant catch-up to do. In addition, we like the improving earnings mix as unregulated "higher quality" revenue from the commercial division grows and we believe Aena should trade at a higher multiple.

{kind=link}

Valuation

As per our forecasts, Aena's sustainable mid-term FCF should be in excess of €1.5 billion or ca. €10 / share, implying a 7% FCF 2026e yield and ca. 6% dividend yield.

We value Aena using a one-year forward multiples analysis. With a 30% increase in Commercial Revenue in 2023, followed by 4% growth annually and an EBIT margin of 75%, we arrive at an EBIT of ca €1.3 billion by 2025 for the Commercial division. We believe the Commercial division should be valued at 15x EBIT 2025 given the growth and quality of earnings or at €19.5 billion. We value the Aeronautical division at 1.1x RAB at a value of €11 billion. We value Real Estate at 15x EBITDA and International at 10x at-equity-income, at €1bn. Subtracting net debt and making EV adjustments we arrive at an equity value of €25.3 billion, or a share price of €165 or $185 implying 17% upside.

Risks

Risks include but are not limited to lower traffic growth, general cost inflation, higher energy expense, unfavorable changes in the regulatory regime, lower commercial revenue and worse-than-expected commercial tender results, and inappropriate capital allocation including value-destructive M&A activity.

Conclusion

Given the favorable fundamentals and the appealing valuation, we recommend building a long position in Aena shares. The investment offers unique exposure to a network of high-quality assets with growing earnings. We also find it attractive from a thematic perspective as it is a play on the rise of travel and tourism in Spain. Aena is one of our top picks amid European infrastructure large-caps.

For further details see:

Aena: Entering A New Growth Cycle