ASLE - AerSale Corporation Q3: Latest Earnings Miss Signals Overvaluation

2023-11-19 00:25:02 ET

Summary

- AerSale has consistently missed earnings expectations in the past 9 months, with the stock cratering at every earnings release.

- The company's lack of visibility in the market and high levels of inventory pose significant risks.

- AerSale is trading at a higher valuation compared to its competitors, and after adding all concerns we derive a fair price of $10, with a downside of 30%.

During the past 9 months, AerSale ( ASLE ) missed all three of its last quarters' expectations. The stock cratered each and every time, and this prolonged weakness is sending a clear message to the market: the company’s results may be harder to forecast than initially thought. This is not something that is being remunerated by the market during this period of contracting valuations and high interest rates, and investors should rightly expect multiples contraction going ahead.

We feel neutral to lightly bearish on AerSale and are comfortable assigning a fair price of around $10, with a downside potential of 30%.

The company and the last quarters: what’s going on

AerSale is a supplier of aftermarket aviation components, from aircraft and engines to OEM and other components. The company also provides proprietary technical solutions that are internally development such as software. Their sector is cyclical as demand is highly dependent on demand coming from a cyclical industry, which is airlines. They have exposure to both passenger and cargo airlines as they provide solutions and components to both. They generate revenues through three main segments: (1) product sales, (2) leasing, and (3) services. The first one of the three experienced a boom in growth as shortages and delays in the overall aircraft industry fueled price increases across this equipment.

The latest earnings release has been quite disappointing for various reasons. We believe that the company (1) failed to meet guidance expectations, and (2) gave poor visibility on inventory movements. The company actually met Q3 expectations as they reported revenues of $92 million which was around $22 million below consensus (per Seeking Alpha data), and EPS of $0.03, $0.18 below consensus. On top of this miss, the guidance for the full year seems to imply flat revenue growth YoY, with around $400 million of total revenues guided against $408 million for FY2022. And then there are concerns around inventory, which we presented below.

So to wrap up, a booming market, and booming revenues, fueled an amazing stock price increase in the last years. Revenues of AerSale are still growing some 80% YoY in the last quarter reported, and they are guiding between $400 and $420 million of revenues for FY 2023.

ASLE Revenues (Seeking Alpha)

Revenues reached a new high last year, and 2023 should also be close. However, the earnings miss, and more cautious than expected guidance during earnings calls, is opening up to the possibility of not-so-great numbers going forward.

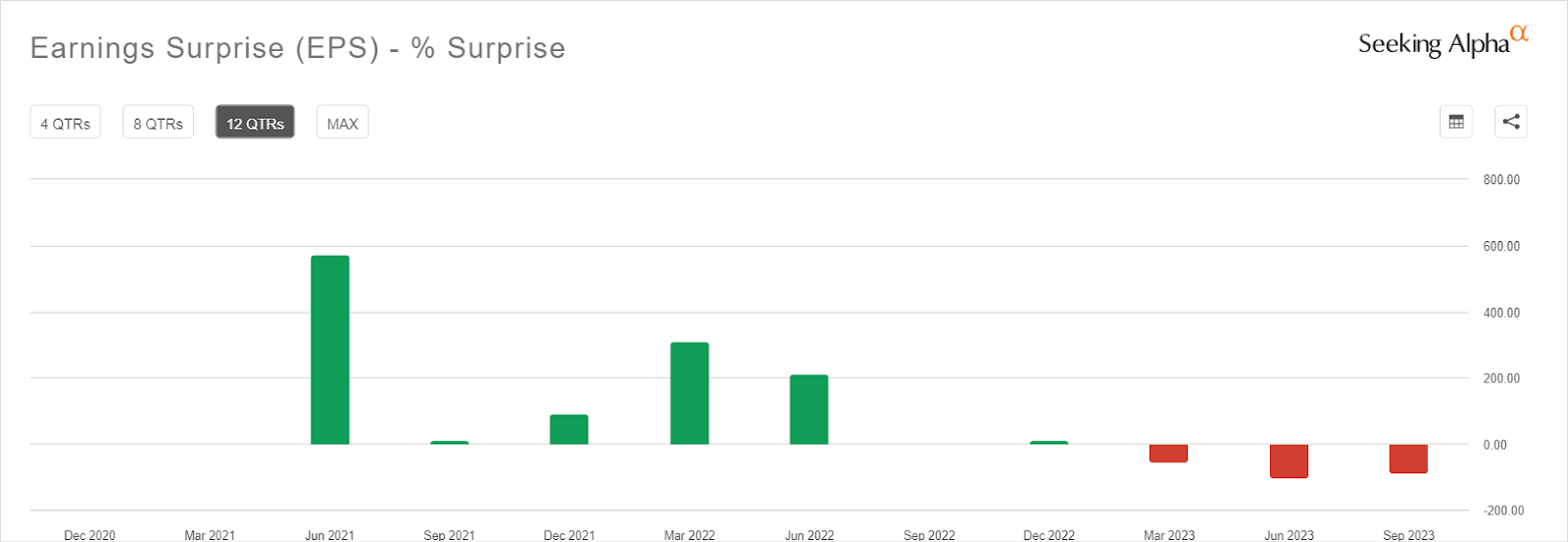

ASLE - Earnings surprises (Seeking Alpha)

{kind=link}

These are the earnings surprises for the last 12 quarters. ASLE was doing great during the 2021-2022 period, with both top line and bottom line numbers coming well above expectations. But in 2023 things changed. In particular, the air freight recession lowered rates and is causing delays in cargo-related sales by ASLE. From the latest earnings call:

Consistent with our communication last quarter, given the current end market conditions, we anticipate these will take longer to place than originally forecasted at the start of the year, and expect a higher mix of aircraft will be leased instead of sold

This is just an extract, but the overall sentiment is that the company lacks visibility due to current market conditions. This weighs on the valuation as at every earnings release, the market realizes that things are worse than expected, and the stock tanks.

We believe that the current situation poses a significant risk of losses given: (1) extremely high levels of inventory compared to the historical average, and (2) limited visibility on market conditions.

ASLE - Inventory (Seeking Alpha)

In the last months, despite worsening macroeconomic conditions and in particular a deep recession in the air cargo market, the company went all in with new “opportunistic” purchases. It is clear from the analysts' questions in the latest earnings call that this is a significant concern if paired with the second point: lack of visibility. The company uses historical disposition rates to compute how much of that they are going to sell, but what if they are not representative of this environment? The answer is significant losses, negative EPS, and depressed topline and cash flows.

A spectrum of valuations: AerSale is more expensive than its competitors

We also want to highlight some concerns on a relative valuation basis. AerSale competes with various similar providers of aircraft equipment and leasing services. However, we find that ASLE is more expensive than its peers, and the concerns expressed before are not helping.

ASLE - Valuation (Seeking Alpha)

The company is trading at an EV/EBITDA (forward) multiple that is almost twice the median sector value. We believe this is not justified by any expectations of future growth rate as the market itself lacks visibility on the sales/inventory conversion environment. This is a result of pure overvaluation fueled by past positive results that are not representative of the current environment.

We like to use ASLE’s own guidance to try to price the stock at a reasonable level of fair price per share.

Finally, moving to our updated guidance for 2023. We now expect to generate revenue of $400 million to $420 million and adjusted EBITDA of $40 million to $45 million in 2023

This means that for FY2023 we should use a multiple applied on a top estimate of $45-50 million. To be conservative in our bearish view, we will apply a $50 million EBITDA figure to include possible beats in Q4. By applying the market average multiple of around 11x, get to a fair EV of $550 million, and a fair price per share of around $10. This would represent a downside potential of around 30% compared to the current price of $14.

Wrapping up: how things may play out for ASLE

We think that not everything might be lost for ASLE. As other Seeking Alpha authors pointed out, the company is also on the verge of launching a relevant new product that is set to get approval from the FAA. It’s the Enhanced Flight Vision System “AerAware”, which can be deployed on Boeing 737 and MAX aircraft.

The overall view is a product on both the concerns of an unstable environment and excessive inventory and a possible recovery from the successful launch of this product plus improvement of market conditions.

However, the current valuation is still too generous and biased on the upside scenario rather than accounting for all the possible risks. Given that there is no track record to benchmark the imminent launch of this software, we are not sure about revenue velocity and customer perception. It would be nice to judge this 3 to 6 months from now and only then draw positive conclusions, before then, we remain highly skeptical especially when adding the concerns.

We think what the market is really missing is that we cannot properly evaluate a company that has little to no visibility on its cash flows 3 months from now, and now the stock price is biased towards recent positive results. In the last three years, analysts have seen skyrocketing revenues and EPS that were the results of exceptional market conditions, and these are simply not here anymore.

Conclusion

We believe that AerSale is overvalued as the company is navigating a highly uncertain business environment with an incautious capital structure and asset allocation decisions. On top of this, the stock also appears overvalued compared to the median sector valuation considerably lower.

We believe that any price above $10 should be considered not attractive as the concerns clearly outweigh any possible benefits.

For further details see:

AerSale Corporation Q3: Latest Earnings Miss Signals Overvaluation