ASLE - AerSale: Stock Has Probably Already Priced In FY24 Earnings

Summary

- There are plenty of airplanes that are going to retire over the next few years.

- ASLE has a tailored operating model which maximizes profitability.

- ASLE’s FAA rating can be considered as a competitive advantage.

- It is not an attractive share price to go long currently.

Summary

I recommend staying neutral on AerSale Corporation ( ASLE ). I expect ASLE to benefit greatly from the surge of fleets retirement in the near-term due to the COVID disruption, which would boost profits and earnings to an all-time-high. However, this seems to be already priced in by the market (as such it is trading at a trough multiple today). This pricing in would also mean additional risk to an investor in that, if ASLE misses estimates, the stock could take a nose-dive as the market resets expectations.

Company overview

The aviation products and services of AerSale Corporation are for sale and maintenance. Aftermarket commercial jet aircraft, engines, and OEM used serviceable materials, as well as maintenance services, are services the company offers to airlines transporting both passengers and cargo, as well as government agencies, leasing companies, multinational original equipment manufacturers (OEMs), and independent Maintenance, Repair, and Operations (MROs).

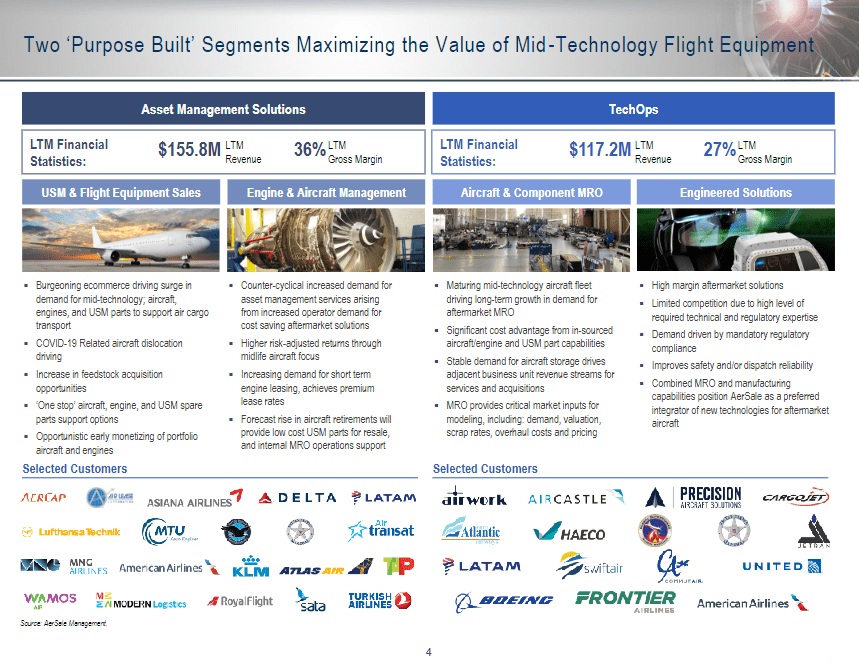

ASLE operates two segments: Asset Management Solutions (68% of FY21 revenue) and Tech ops (32% of FY21 revenue)

{kind=link}

Plenty of airplane retirements coming up

ASLE's core business is providing Flight Equipment MRO services and supplying used serviceable material [USM] for commercial transports in both civilian and military service.

The aviation aftermarket is largely driven by global macroeconomic factors and the success of airlines transporting both passengers and cargo. The demand for aviation products and services is affected by a wide variety of variables, such as the age of the fleet, the price of fuel, the type of aircraft in use, and aircraft utilization rates. Aircraft utilization, a key factor in MRO demand, is affected by many of these factors. In addition, these variables are directly associated with the need for USM replacement components for aircraft with finite service lives.

Midlife aircraft, which require more frequent maintenance, have traditionally been sold or leased to lower-tier airlines as newer, more modern planes are delivered to the world's top airlines. Historically, these secondary-level operators have depended on third-parties more than their primary-level counterparts for MRO and equipment spares support. In my opinion, this is a promising industry to enter because there is a detectable pattern of recurrent demand, and the ASLE operating model is structured to meet the requirements of this growing market.

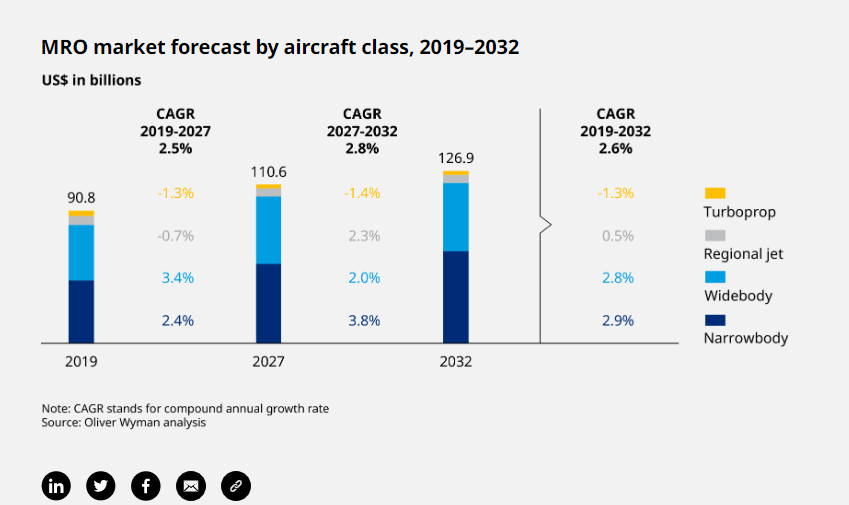

I believe that as the world becomes more globalized and travel returns to pre-covid levels and beyond, demand for aircraft will continue to rise. This means that an increasing number of aircraft will be retired. According to Oliver Wyman , the global fleet will grow to 38,189 by 2032, up from 27,844 in 2020.

In the run-up to COVID-19, the market value of midlife aircraft for the models that AerSale seeks out skyrocketed, making them unfeasible for early retirement or conversion into freighters. Due to the introduction of new fleets, I anticipate that AerSale's Asset Management and TechOps departments will soon be able to acquire a large number of midlife aircraft at bargain prices. I also think there could be a significant uptick in the demand for leased and used exchange engines to back up operational fleets.

Consequently, I also believe the MRO industry will grow along with the world's fleet. This is supported by Oliver Wyman's forecast, which predicts that the MRO market will expand by the low single digits until 2032, totaling $126.9 billion.

{kind=link}

Tailored operating model to maximize profitability

The focus of ASLE's institutionalized processes is to maximize the value of flight equipment in the second half of its life cycle, which is where the company really shines compared to the competition. In my opinion, ASLE's data-backed approach and unique set of analytics serve as a competitive edge against competition in the aviation aftermarket.

ASLE's ability to offer low-priced options for flight equipment is essential for the company's profitability and ability to create value. ASLE's comprehensive range of products and services gives it an advantage over competitors as a one-stop solution for its target market. The integration of these services also presents ASLE with numerous opportunities for cross-selling between its different business units, as many clients use both segments. Overall, ASLE is better able to meet the needs of its customers thanks to the depth and breadth of these capabilities, which allow for greater fleet adaptability and less maintenance downtime. All of these features also help ASLE save money on its own Flight Equipment. At the same time, MRO and USM parts investment decisions are informed by market intelligence gleaned from upstream aircraft and engine transactions, which in turn gives important actionable insight into operating fleet market trends.

As a trusted supplier, ASLE gives clients a more affordable option to buying new OEM parts. The main idea here is that by sourcing cheap USM parts, ASLE can make a profit off of airplanes and engines that have little value as a whole operating asset. Additionally, many parts and systems utilized by the USM can be kept operational for longer thanks to ASLE's component MRO services. In this way, ASLE can boost USM return to service yield, cut costs associated with return to service, and reap additional profit from the sale of USM parts. It is also able to reduce the amount it spends on repairing and maintaining its planes and engines.

FAA rating can be considered as a competitive advantage

ASLE, in my opinion, has a leg up on the competition in the MRO space thanks to its ability to maintain FAA "unlimited" repair station ratings (not many MRO players have this qualification). Most importantly, the FAA no longer provides these detailed ratings (according to the S-1). With this rating, ASLE can move quickly to implement selected MRO capabilities through a "self-certification" process that has already been approved by the FAA. By skipping the standard FAA repair station capability certification process, this drastically shortens time-to-market.

Expand geographical footprint to extend growth runway

In my opinion, the expanding global aviation market presents a fantastic opportunity for the company to broaden its clientele by capitalizing on its existing capabilities. As international fleets in both developed and developing markets continue to grow in size and age, I expect ASLE to play an increasingly important role in providing its expertise to developing markets that lacks the necessary capabilities to do so.

Diving deeper into the Government segment

ASLE serves a wide variety of commercial and military customers, and many of the aircraft and engines that they support are also used by civilian and military government bodies. Because funding from the government is reliable and less cyclical, I believe this market has significant growth potential. ASLE, in my opinion, can best leverage this developing trend by emphasizing the signing of new MRO service contracts and the sale of USM replacement parts. If this were to happen, it would almost certainly extend ASLE's growth runway by expanding the TAM that the company serves.

Valuation

I believe ASLE is fairly valued as this point as my model indicates that ASLE is worth $16.65 in FY23. Which is about 4% above current share price.

My model assumption is based on my belief that the ASLE will benefit from the surge of retired fleets in the near-term due to the COVID disruption. Alongside the growth, margins should expand as ASLE takes advantage of the spread.

ASLE is currently trading at 6.5x forward EBITDA, which makes sense as the market is pricing in ASLE "peak" earnings in FY23/24 as mentioned above. I believe this is the right way to value ASLE and as such have used the same valuation multiple.

Own calculations

Risks

2nd derivative impact from commercial aviation industry

Because of ASLE's position as a supplier to the commercial aviation sector, the company's profits are generally affected by the sector's economic climate. Historically, the commercial aviation industry has been cyclical, experiencing downturns due to macro factors. Airline capacity cuts, either domestic or international, as a result of such macro weakness would also be bad for ASLE. A weak credit market would also be bad as airline clients will face trouble when trying to make large purchases like maintenance services, Flight Equipment, and new planes.

Conclusion

Due to an increase in fleet retirements as a result of COVID-related disruptions, the company is likely to see significant growth in the near future, which could drive profits and earnings to record levels. However, it appears that the market has already factored in this potential growth, as the stock is trading at a trough multiple. This adds to the risk for investors, as missing estimates could result in a significant drop in stock price as the market adjusts its expectations.

For further details see:

AerSale: Stock Has Probably Already Priced In FY24 Earnings