ASLE - AerSale Stock: Why I Bought More

2023-05-15 14:34:40 ET

Summary

- AerSale results missed analyst expectations.

- Year-over-year decline is driven by one-off sales.

- Southwest Airlines is most likely the launch customer for AerAware.

- On the prospect of AerAware, I am upgrading to strong buy.

In a previous report , I marked AerSale ( ASLE ) stock a buy on its attractive business segments and the prospects of AerAware. Its leasing segment is not what radiates strength to me, but I like the fact that the company provides MRO services and buys feedstock and decides what is economically more viable. So, the company can buy an airplane for parting, leasing, refurbishing and sale or conversion and the company continues looking at its feedstock in that way and even if an airplane is on lease it can decide to sell the airplane at attractive prices. So, the company is constantly weighing what is best for the business in a very prudent way. Besides that, I continue to believe the AerAware product will do great things for the business and its customers.

AerSale Q1 2023 Financial Results

{kind=link}

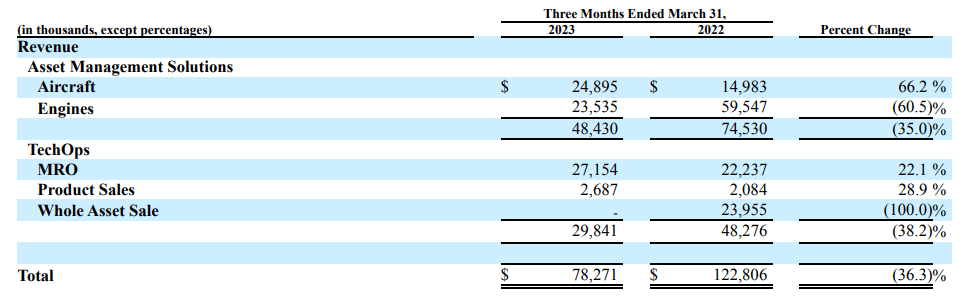

Looking at the revenues, we see that revenues were down 36.3% missing analyst estimates by $5.1 million. That might look like a dramatic drop, but it is caused by the $24 million sale of the X AerAware demonstrator in the comparable period last year. Absent of this asset sale, TechOps would have seen 23% in revenue growth. Year-over-year, we see that the segments within TechOps are up 20 to 30 percent.

In Asset Management Solutions, aircraft revenues were up 66.2 percent driven by a $10.3 million higher asset sale figure, while leasing revenues went down. During the quarter, the company decided to sell a Boeing 737-400 that was on lease and that demonstrates why the lease revenues are under pressure but also demonstrates how AerSale looks asset by asset what makes most sense from a profit perspective. Engine revenues were over 60% lower, primarily due to lower engine transactions and lower rental income on engines.

What is currently affecting the business is actually more a comp issue. Compared to last year, transactions are more backloaded this year on asset sales and AerAware also warns on these kinds of fluctuations, indicating that its results can be better assessed on annual basis. Excluding one-offs and the lumpy sales on wholesale, results would have improved by 8%.

I could do a detailed discussion of the profits, but those mostly reflected the lower sales and a less favorable composition of the asset sales. So, it is really a trickle through effect.

What Are The Growth Drivers For AerSale?

My view on the growth drivers has changed little. While AerSale is not really showing growth where I'd like to see it, namely in the leasing business, I am not negative on the company for investment, but one should keep in mind the risks. If you want lease revenue exposure, I believe there are other names such as AerCap ( AER ) and Air Lease Corporation ( AL ) to consider.

The Boeing 757 passenger-to-freighter conversion program or P2F is a growth opportunity for the company. Currently, there are delays in the conversions and there was some headwind in H2 2022 for feedstock availability. With airplane shortages which are not getting much better given the Airbus delivery and program delays and Boeing's most recent problems with the Boeing 737 MAX , acquiring feedstock at attractive prices can be a challenge, but this year should be better and with airplane shortages, there are also opportunities for MRO as airlines are keeping airplanes in the fleet longer requiring more maintenance activities than initially planned for. Overall, with the cargo demand cooling it is harder to sell these airplanes but leasing is an option as well.

What I liked about AerSale is that the business provides an integrated solution. With feedstock, the company can either decide to lease the airplane to an operator, part it out or convert it. So, the company always has a solution for its feedstock. The Boeing 757 offers opportunities as an airplane in the express logistics chain for e-commerce growth, but there are also risks. Engine availability could drive up costs and cost of conversion could in the current inflationary environment also be higher while macroeconomic headwinds could reduce demand for the converted airplanes as we are already seeing currently.

So, that is something that should be kept in mind. Either way, even with lower P2F demand in the current environment where airplanes are higher in demand than OEMs can supply, AerSale has some flexibility to optimize its on-airport MRO business and let the conversions be done by subcontractors. This basically means that the capacity for conversions is being subcontracted so that the MRO business can focus on servicing in-fleet airplanes.

What makes AerSale a highly interesting name to consider for investment is its AerAware product, which consists of some airplane modifications in the radome and a wearable heads-up display for a pilot which improves situational awareness through improved vision in low-visibility conditions. Initially developed for the Boeing 737NG or Boeing 737 MAX, the Enhanced Flight Vision System provides AerSale with a big addressable market for a product that should be high margin. The only drawback is that the commercial roll-out of this product is one that is unknown. AerSale is going through the certification of the product now, but the process of cumulating flight hours has been rather slow. So, it is a project that is promising, but its revenue generation depends on certification, though I do believe that we are closing in on commercialization. No AerAware sales have been projected for 2023, but that is not because no sales are expected at all but because AerSale does not want to conduct issuing forecasts which include products that are not yet certified.

AerAware Progress Looks Promising

I started buying shares of AerSale by the end of April and the only reason why I am buying is the prospect of AerAware. I think otherwise I would not be a buyer. So, AerAware is also what I want to hear more about every call, and we got some very useful information. For 2023, 100 AerAware kits were targeted and the company is already at 55 after Q1 with a production rate of 15 per month now. So, it seems that actual production this year could be closer to 200 than to the 100 and that really does provide some positive light on the ability to supply in large quantities as some operators have large fleets that will not activate the AerAware product until a significant portion of its fleet is equipped.

Right now, one more set of flight tests is required, which would finalize the flight test campaign if everything goes smoothly. Currently, a small modification is being worked on and once that is finalized, the final sets of tests should be happening which will only take a week, and then it should take 30 days to obtain the STC (Supplemental Type Certificate). It is not the case that from that point on there will be a huge flow of kits going to customers, since there is an installation effort as well as a training effort involved. The company also remains confident that its intended launch customer will still be the launch customer. It is a US domestical airline with several hundred Boeing 737s in the fleet. So that is either Alaska Airlines (ALK) or Southwest Airlines ( LUV ) and I am inclined to say it is the latter.

Is AerSale Stock A Buy?

The short answer is: Yes. I entered some fundamental data for AerSale and expectations for AerSale into a valuation tool for aerospace and airline companies that I will be launching for subscribers of The Aerospace Forum next week. And based on the results from that dynamic model, we get a price target of $21 for AerSale providing 32% upside and that leaves a significant undervaluation as compared to the industry and does not take into account the prospects that AerAware has in terms of scalability over a long term period for the Boeing 737 and future platforms.

Conclusion: AerSale Is An AerAware Buy

My overall conclusion does not change after the first quarter results. Selling converted freighters might be a bit tougher, and overall, the leasing revenues are under some pressure as AerSale in many cases opts for a more rewarding solution of selling the asset. The big thing for AerSale is going to be AerAware without doubt and I saw some very positive signs during the first quarter earnings call and couple with my valuation I believe this is a strong buy.

It will have a high margin and a big addressable market for the Boeing 737, which can be expanded towards other airplane models. AerAware should become the next big thing for AerSale and makes AerSale Corporation stock a buy in my view

For further details see:

AerSale Stock: Why I Bought More