AES - AES Corporation Has Become Too Cheap To Ignore

2023-10-19 03:15:35 ET

Summary

- AES Corporation has underperformed in the market due to the surge in treasury yields and its high debt load.

- AES is not likely to have any problem servicing its debt.

- The company has been growing its clean energy portfolio at a fast pace.

- The stock is trading at only 8.1 times this year's earnings and only 6.6 times its expected earnings in 2025.

AES Corporation ( AES ) has dramatically underperformed the broad market this year, as it has plunged 51% whereas the S&P 500 has rallied 15%. The reason behind the vast underperformance is the surge of treasury yields to a 16-year high. AES Corporation has a high debt load and hence the surge of treasury yields and the expectations for high interest rates for a longer period than previously anticipated are likely to take their toll on the results of the company.

However, AES Corporation has nearly all its debt at fixed rates and does not have any debt maturities before 2025. Given its reliable growth trajectory, the company is not likely to have any problem servicing its debt. In addition, its stock has been punished by the market to the extreme, as it is currently trading at a forward price-to-earnings ratio of only 8.1x . Thanks to its exceptionally cheap valuation and its reliable growth prospects, the stock is likely to highly reward investors whenever interest rates begin to moderate.

Business overview

AES Corporation owns and operates power plants that use various types of fuels, such as natural gas, diesel, coal, and renewable energy sources. It has operations in 14 countries and has more than 100 power plants, with an installed power in excess of 32,300 megawatts.

A key characteristic of AES Corporation is its resilience to recessions, as demand for energy hardly decreases even under the most adverse economic conditions. The company proved resilient throughout the Great Recession, which was the worst financial crisis of the last 90 years. AES Corporation also proved immune to the coronavirus crisis, as it posted record earnings per share in 2020, 2021, and 2022. The defensive business model of AES Corporation is important, particularly given the global economic slowdown this year.

The other key characteristic of AES Corporation is the excessive room for future growth. The global transition from fossil fuels to clean energy sources has remarkably accelerated during the last three years, especially after the fierce global energy crisis experienced last year due to the war in Ukraine. In order to avoid a future energy crisis, most countries are now investing in renewable energy sources at full throttle.

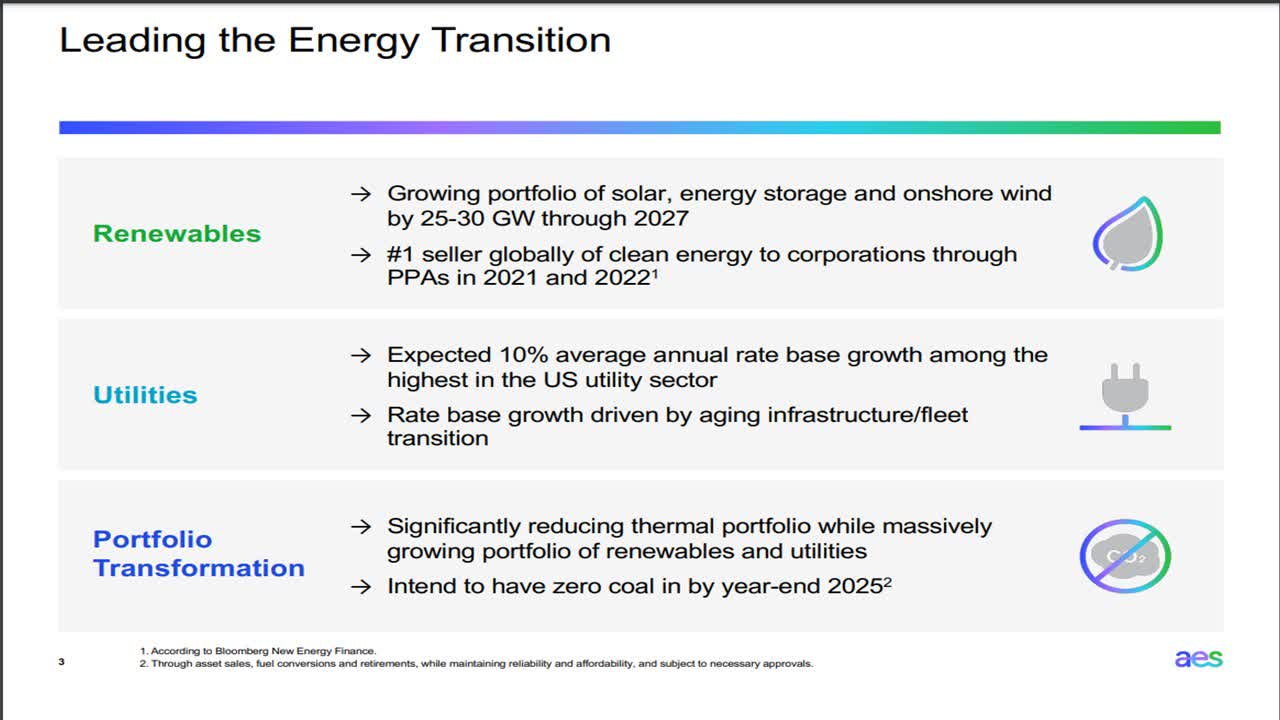

AES Corporation is ideally positioned to benefit from this trend and is investing in the expansion of its business at a breathtaking pace. To be sure, the company expects to eliminate coal from its portfolio by the end of 2025 and grow its portfolio of solar energy, energy storage and wind power by 25,000-30,000 megawatts by the end of 2027.

{kind=link}

This means that AES Corporation will nearly double its installed power over the next four years. The company also expects a 10% average annual growth of its rate base in the upcoming years. This growth rate is one of the highest in the entire utility sector.

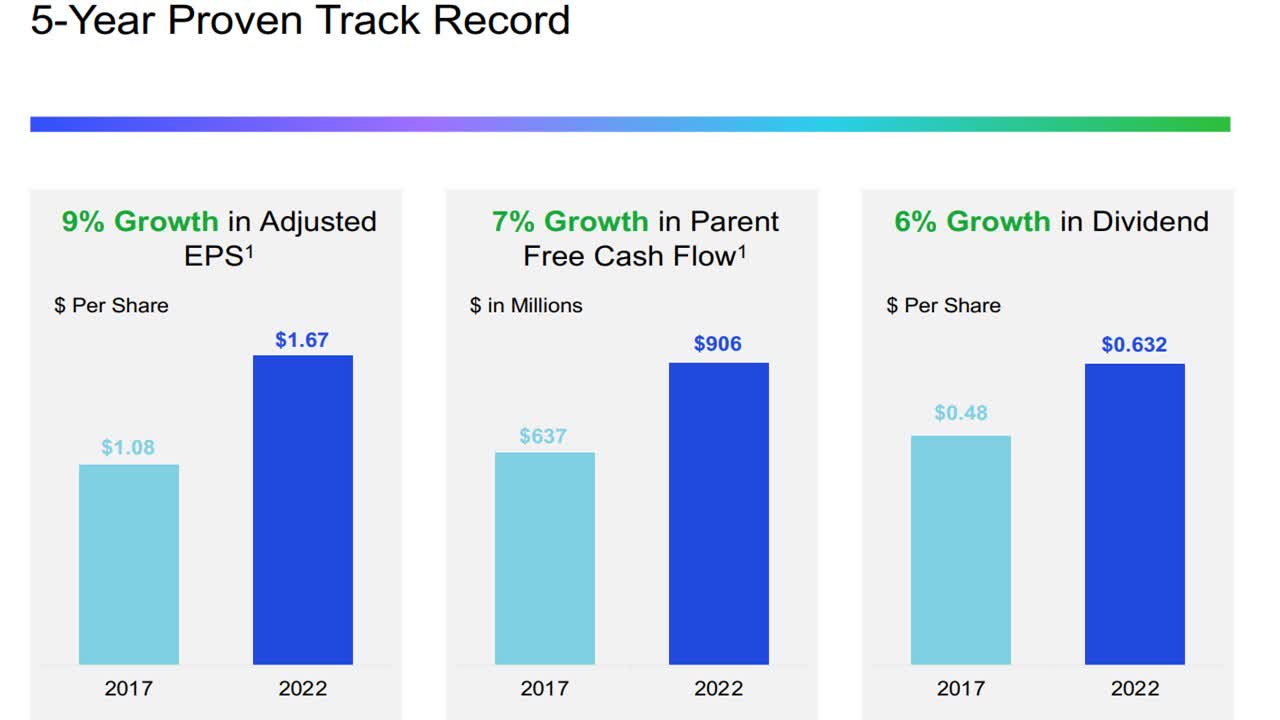

Some investors may claim that the fast expansion of installed capacity may not translate into high earnings growth. However, AES Corporation has exhibited consistent earnings growth over the last five years.

{kind=link}

During this period, the company has grown its adjusted earnings per share, its free cash flow and its dividend at an average annual rate of 9%, 7% and 6%, respectively. It is also important to note that the company has grown its earnings per share for six consecutive years. The consistent performance is indicative of a reliable growth trajectory. Indeed, analysts expect AES Corporation to grow its earnings per share by 11% in 2024 and by another 10% in 2025, from $1.69 this year to a new all-time high of $2.08.

Valuation - Debt

Due to its 51% plunge this year, the stock of AES Corporation is currently trading at a nearly 10-year low price-to-earnings ratio of 8.1x. This earnings multiple is a nearly 10-year low valuation level, much lower than the 10-year average of 11.5x of the stock. It is also remarkable that the stock is trading at only 6.6 times its expected earnings in 2025. This is undoubtedly an extremely cheap valuation level.

The depressed valuation of the stock has resulted from the surge of treasury yields to a 16-year high, which is likely to burden AES Corporation, given the weak balance sheet of the company. Its net debt (as per Buffett's formula, net debt = total liabilities - cash - receivables) is standing at $32.4 billion. This amount is more than three times the current market capitalization of the stock ($8.8 billion) and approximately 30 times the annual adjusted earnings of the company. Therefore, the debt load of AES Corporation is excessive, based on these metrics.

However, net interest expense consumes only 32% of operating income. Moreover, the vast majority of the debt of the company is at fixed rates while there is no debt maturity before 2025. This is critical, as the company has managed to avoid an increase in its net interest expense over the last three years, in sharp contrast to most indebted companies, which have incurred a steep increase in their interest expense during this period.

Furthermore, AES Corporation enjoys much more reliable cash flows than a typical company thanks to the essential nature of its business and the multi-year contracts it signs with its customers. It is also on a reliable growth trajectory and hence it is likely to improve its financial metrics in the upcoming years. Management recently stated that it expects to improve the leverage ratio (Net Debt to EBITDA) until 2027. To cut a long story short, AES Corporation is not likely to have any problem servicing its debt thanks to its low interest expense, its resilient business model and the fast growth of its business.

Dividend

Due to its depressed valuation, AES Corporation is currently offering a nearly 10-year high dividend yield of 4.8%.

The stock has a payout ratio of only 42% and hence its dividend has a meaningful margin of safety. It is also worth noting that the company has raised its dividend every single year since it initiated its dividend, in 2012. AES Corporation has grown its dividend by 5% per year on average over the last five years and over the last three years. Given its healthy payout ratio and its promising growth prospects, AES Corporation is likely to continue raising its dividend at a modest pace for many more years.

Risk

The recent surge of treasury yields to a 16-year high is a negative development for AES Corporation, which may be forced to refinance some portions of its debt at high interest rates when they mature, after 2025. If interest rates remain high for several years, they will almost certainly take their toll on the earnings of AES Corporation. However, even in such an adverse scenario, thanks to its fixed-rate debt and its laddered debt maturities, AES Corporation is not likely to be severely hurt by high interest rates over the next few years.

Moreover, the Fed has repeatedly stated that it will exhaust its means to drive inflation to its long-term target range of 2.0%-2.5%. Thanks to its aggressive stance, the central bank has already reduced inflation from last year's peak of 9.2% to 3.7% now. Whenever the Fed accomplishes its goal, most likely in 2024 or 2025, it will probably begin reducing interest rates. When that happens, the stock of AES Corporation will probably begin recovering toward its historical valuation levels.

Final thoughts

As long as interest rates remain around their 16-year highs, the stock of AES Corporation is not likely to retrieve its recent losses. Therefore, the stock is suitable only for patient investors, who can maintain a long-term point of view. On the other hand, whenever interest rates begin to normalize, the stock is likely to highly reward investors thanks to its depressed current valuation level and its solid earnings growth potential.

For further details see:

AES Corporation Has Become Too Cheap To Ignore