AES - AES Corporation Is In The Bargain Bin And Its Future Is Green

2024-01-02 23:09:58 ET

Summary

- Clean energy stocks have underperformed due to rising interest rates, creating a buying opportunity for investors in AES.

- AES exceeded market expectations in Q3 earnings and raised its 2023 EPS forecast.

- AES is focused on decarbonization, aiming to exit coal entirely by 2025 and has a strong position in renewable energy.

- Patient investors could see rewards as AES executes its plans and grows earnings and cash flow in alignment with the long-term trend toward decarbonization.

Clean energy stocks have been underperforming this year, partly due to rising interest rates. This has created an attractive buying opportunity for investors to leg into AES ( AES ). AES' recent quarter showed strength and exceeded market expectations in Q3 earnings. AES has upped its 2023 EPS forecast to the upper range and secured significant renewable contracts, aiming to reach at least 5 GW of new PPAs by year-end. To ensure financial stability, AES is expediting its asset sale program, intending to avoid the need for new equity until at least 2026. They anticipate minimal impact from higher interest rates, with a 100 bps shift affecting less than a cent in 2024 and between 3 and 4 cents in 2025.

The Latest Quarter Showcased Operational Strength and Financial Flexibility

AES's adjusted EPS of $0.60, surpassed consensus estimate of $0.54. Looking ahead, AES now anticipates achieving EPS in the upper half of its 2023 guidance range of $1.65 to $1.75.

AES confirmed their targeted adjusted EPS annualized growth of 7-9% until 2025 from a 2020 base year. Furthermore, AES maintains its annualized growth target for adjusted EPS of 6-8% through 2027.

To ensure financial stability, AES is expediting its asset sale program, aiming for over $3.5 billion (previously $2.7-3.0 billion) to avoid requiring new equity until at least 2026. The company forecasts equity issuance of $500-1,000 million in 2027, as opposed to the previously planned $1.6-$1.9 billion for the full 2023-2027 period. Despite this, management expects to meet or exceed credit downgrade thresholds next year due to the accelerated asset sale program.

AES' backlog, which includes projects with signed contracts but not yet operational, stands at 13,138 MW, with 5,761 MW currently under construction. As of YTD 2023, AES has completed construction or acquisition of 1,314 MW of wind, solar, and storage, with plans to complete a total of 3.5 GW by the end of 2023. In the same period, the company has signed contracts for 3,740 MW of new renewables and is on track to sign at least 5 GW by the year's end.

A Compelling Proposition Focused on Decarbonization

AES has shown robust 9% EPS growth over the past five years while notably reducing coal generation from about 60% to under 30% of total generation. Their aim is to exit coal entirely by 2025, establishing a strong position in renewable energy. They've been a top seller of clean energy to corporations, securing 2.8 GW of new PPAs in 2022, which accounts for approximately 7% of their total.

AES faces its most significant risk in its current backlog of infrastructure projects. If these projects fall short of meeting their financial targets, it could adversely affect the company's valuation. Nonetheless, the established safeguards governing pricing and costing offer some assurance and mitigate this risk to an extent.

Recent Weakness Presents a Buying Opportunity

Over the period of 2018-2022, AES significantly outperformed its renewable peers with a 166% price appreciation compared to the range of -15% to +114% among its peers and 36% for utilities.

{kind=link}

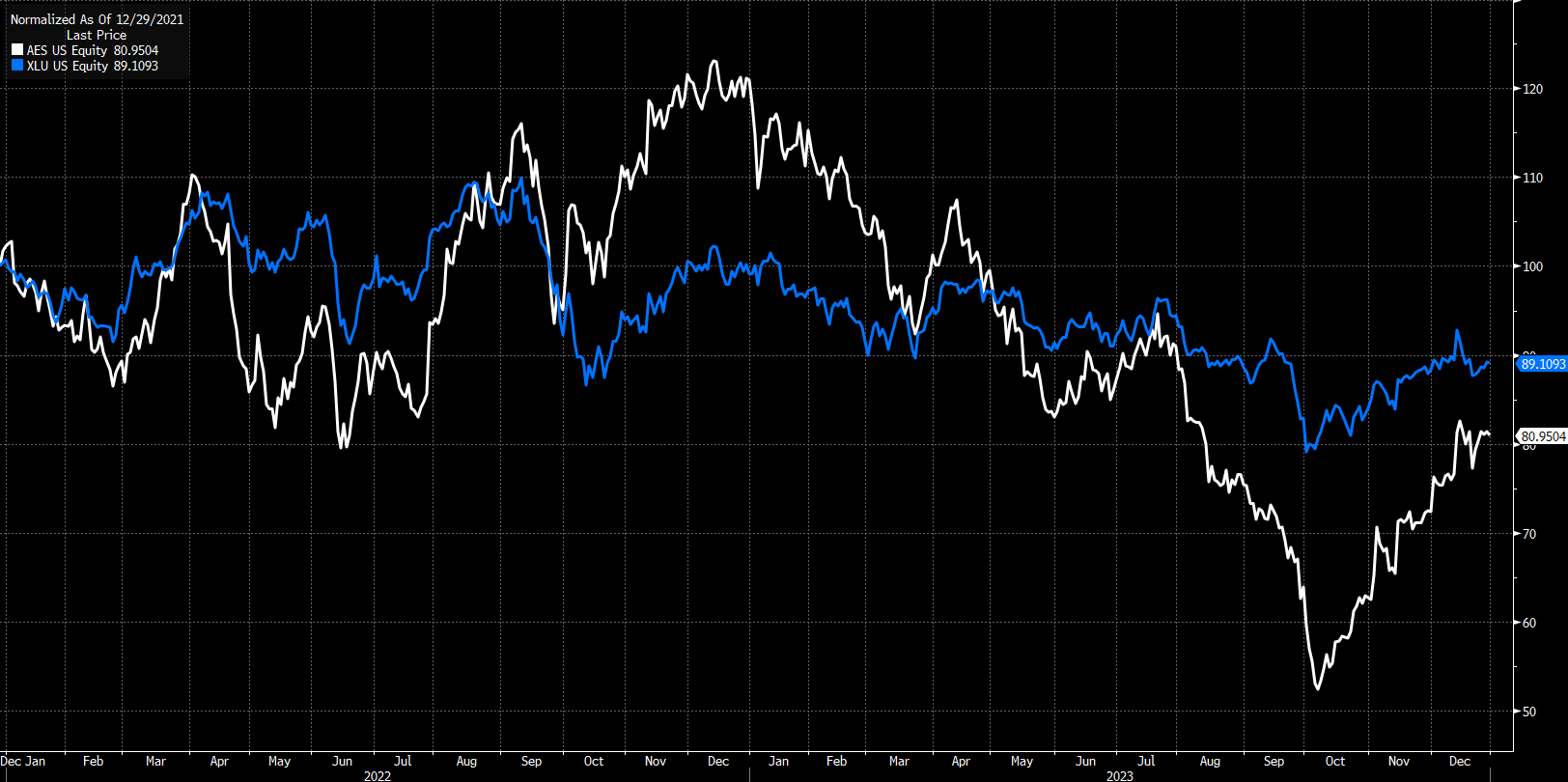

AES was a notable outperformer versus the XLU ETF in 2022, rising 21.7% vs 1.4% for XLU. However, despite being one of the top performers in 2022 AES has underperformed through 2023, declining 30.9% through the year against the XLU which has declined 7.2%. This dip is partially attributed to rising interest rates, and a newly issued EPS growth forecast of 6-8% annually for 2023-2027 at the May 8th Investor Day, disappointing investors.

Nonetheless, AES reaffirmed its previous target of 7-9% annual growth through 2025. The decrease in growth rate is linked to the company's strategy to exit coal by 2025, which accounts for almost a third of AES' 2022 EPS. Most importantly, I believe investors should look beyond the medium term because AES anticipates double-digit growth post-2025, following the reset from coal assets.

{kind=link}

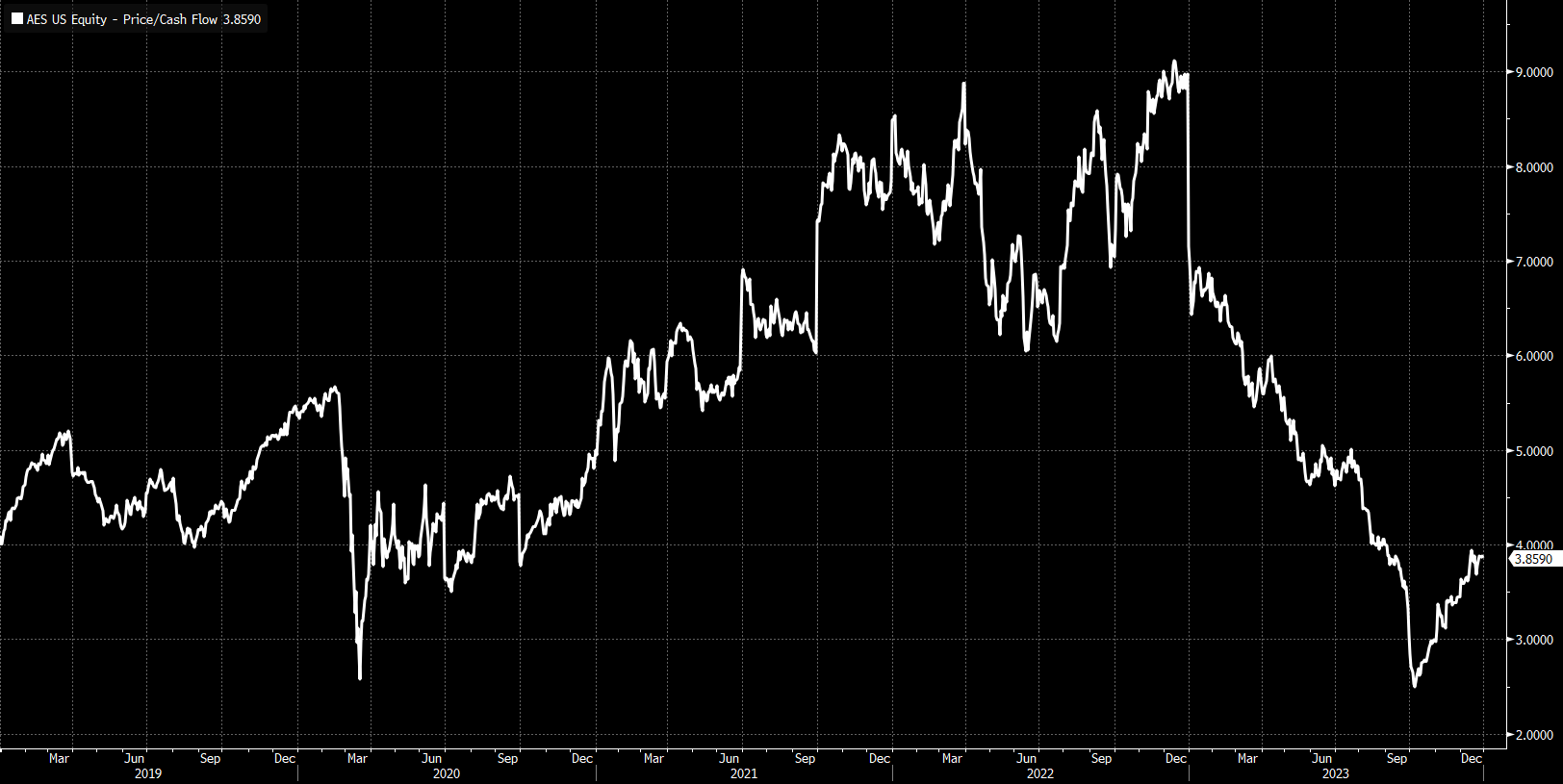

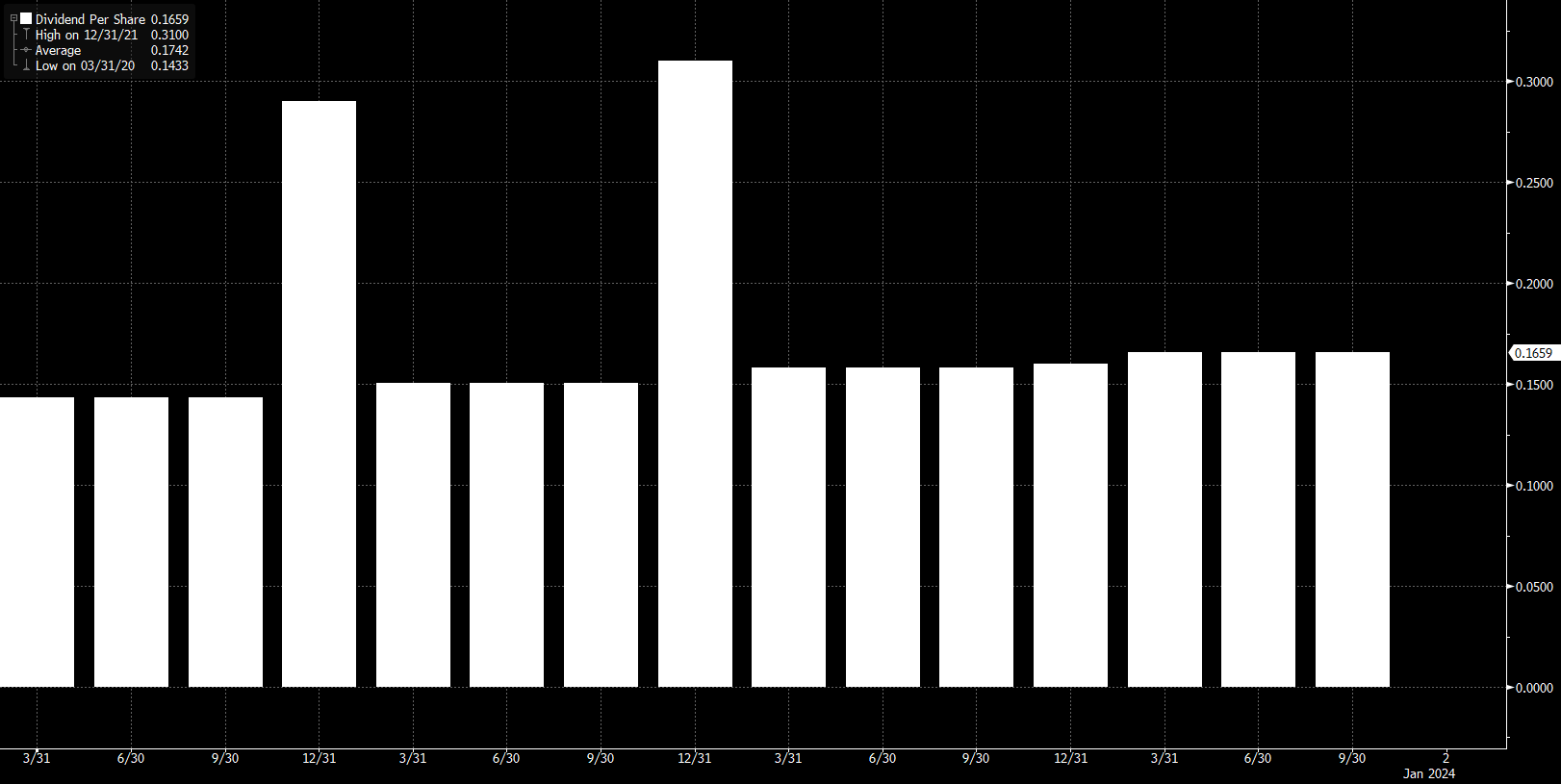

The recent bout of underperformance has brought AES valuations into the bargain territory. AES currently trades at 3.85x P/CF, which is steeply discounted to 5 yr average of ~5.4x. While AES transforms itself into a green energy company, you also get paid to wait. AES will not screen as a high dividend payer, however, the stock does carry a ~3.6% yield which isn't something to sneeze at. Despite the company being in the midst of a transformation, the dividend itself is well covered. The payout ratio on AES' dividend is ~40% at the time of writing. Over the past four years, AES has also increased its dividend four times and also paid out two special dividends along the way.

{kind=link}

Conclusion

Despite short-term challenges, AES remains positioned as a top beneficiary of the ongoing decarbonization trend, especially with the potential impact of policy changes. Patient investors could see rewards as AES executes its plans and grows earnings and cash flow in alignment with the long-term trend toward decarbonization.

For further details see:

AES Corporation Is In The Bargain Bin And Its Future Is Green