AFT - AFT: A Good Floater If The Market Is Wrong About Rates Or A Potential Hedge

2023-11-22 16:43:22 ET

Summary

- Apollo Senior Floating Rate Fund offers a high level of current income with a 12.36% yield, outperforming other debt funds.

- The AFT closed-end fund's focus on floating-rate securities allows it to avoid the impact of interest rate swings and maintain stable returns.

- The fund's holdings primarily consist of below-investment-grade securities, but the majority have a credit rating of B- or above, so we should not have default problems.

- The fund could work well as a companion to a traditional bond fund, as the market may be wrong about the direction of interest rates.

- The fund's distribution is fully covered by NII, and it trades at a very attractive discount on net asset value.

The Apollo Senior Floating Rate Fund ( AFT ) is a closed-end fund aka CEF that specializes in providing a very high level of current income for its shareholders. As of the time of writing, the fund boasts a 12.36% yield, so it certainly accomplishes the provision of income quite well. This fund's distribution also compares fairly well to other closed-end funds that specialize in investing in floating-rate securities:

| Fund |

| Current Yield |

| Apollo Senior Floating Rate Fund |

| 12.36% |

| Eaton Vance Floating-Rate Income Trust ( EFT ) |

| 11.55% |

| BlackRock Floating Rate Income Strategies Fund Inc ( FRA ) |

| 11.78% |

| First Trust Senior Floating Rate Income Fund II ( FCT ) |

| 11.65% |

| Pioneer Floating Rate Fund, Inc. ( PHD ) |

| 12.27% |

This is not especially surprising to see. Apollo is one of the largest alternative asset managers in the world, but it does not have the same recognition as some other fund houses among retail investors that ordinarily purchase closed-end funds. That could prove to be a very good thing for investors right now, as the fund's high yield provides an excellent opportunity for investors to obtain a substantial amount of income. This fund trades at a very reasonable price right now as well.

One of the defining characteristics of floating-rate securities is that they are not affected very much by swings in interest rates. This has allowed this fund to outperform most other debt funds over the past two years. For example, the Apollo Senior Floating Rate Fund has only lost 2.21% since the start of 2022 when we take the fund's distributions into account. The Bloomberg U.S. Aggregate Bond Index ( AGG ) is down 11.47% over the same period, once again after we consider the impact of distributions:

{kind=link}

It is important to consider distributions when evaluating debt funds. This is because debt securities deliver the overwhelming majority of their returns in the form of direct payments to the investors. The distributions received by the shareholders of this fund thus help to offset some of the share price declines, so including the distributions in our return calculations provides a much better idea of what investors in the fund actually received.

However, as many readers may be quick to point out, the market has recently begun to raise bond prices and drop long-term interest rates. In such an environment, a floating-rate fund like this will probably underperform a fund that invests in traditional fixed-income securities. Let us investigate and see if buying this fund today could make any sense.

(Please note that on November 7, 2023, an announcement was made that the Apollo Senior Floating Rate Fund, Apollo Tactical Income Fund Inc. ( AIF ), and MidCap Financial Investment Corporation ( MFIC ) will merge into a single entity. This merger has not been approved by shareholders yet, and there is no guarantee that it will be approved. As such, this article focuses its attention on how the Apollo Senior Floating Rate Fund looks today. The merger, if it ends up getting approval from shareholders, will not close until the end of the first quarter of 2024. As this potential event is still at least four months away and may not even happen at all, it will not be considered for our discussion today. As more information becomes available, updates will be published).

About The Fund

According to the fund's webpage , the Apollo Senior Floating Rate Fund has the primary objective of providing its investors with a very high level of current income while still ensuring the preservation of their principal. This is a very common objective for a debt fund, and in fact, most of them have a similar objective. However, this fund has a somewhat different strategy for achieving this goal than many other bond funds. As its management explains on the website,

Apollo Senior Floating Rate Fund Inc. is a diversified, closed-end management investment company. The Fund's investment objective is to seek current income and preservation of capital by investing primarily in senior, secured loans made to companies whose debt is rated below investment grade and investments with similar economic characteristics. Senior loans typically hold a first lien priority and pay floating rates of interest, generally quoted as a spread over a reference floating rate benchmark. Under normal market conditions, the fund invests at least 80% of its managed assets (which includes leverage) in floating rate senior loans and investments with similar economic characteristics.

Unlike most debt-focused closed-end funds, the Apollo Senior Floating Rate Fund does not invest in traditional bonds that pay a fixed coupon over their lifetimes. Rather, this fund invests in debt securities that have floating rates. The coupon is usually set as being a spread above some benchmark (such as 6-Mo. LIBOR+XXXX%, where XXXX is a percentage spread). The coupon payment that is received by investors will then vary based on market interest rates at the time of payment.

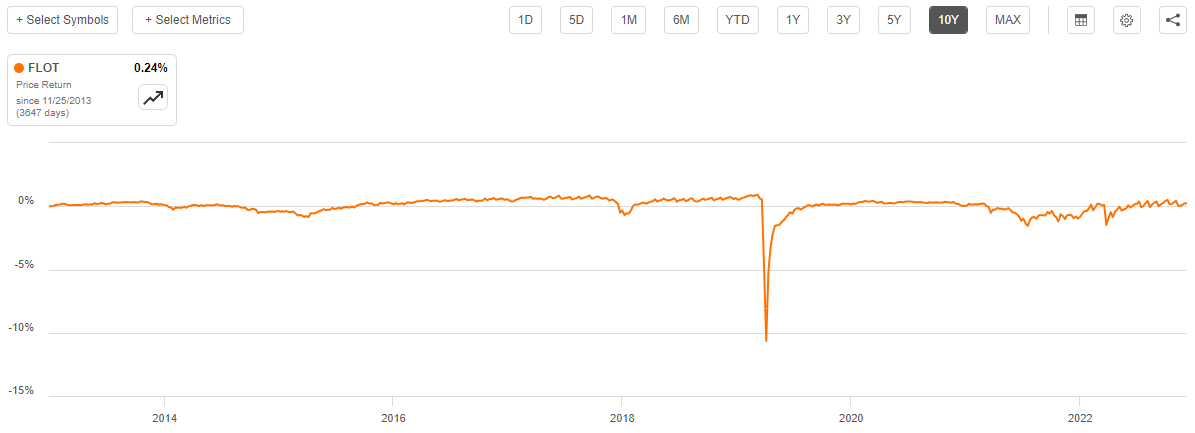

The floating-rate coupon payment allows these securities to avoid the biggest problem with bonds. As everyone reading this is likely aware, bond prices drop when interest rates go up. This is because a bond must always deliver a competitive yield to otherwise identical bonds that are being newly issued in the market. However, an existing floating-rate security will always deliver a competitive yield to brand-new identical securities because of the variable coupon. As such, these securities do not go up or down in price when interest rates change. In fact, the BBG US Floating Rate Notes 5 Yrs. And Less Index, iShares Floating Rate Bond ETF ( FLOT ) has been almost perfectly flat over the past ten years:

{kind=link}

As we can see, except for a temporary drop around the COVID-19 pandemic when investors were literally dumping everything in a panic, the index has not really budged at all over the past decade. That is much better than an ordinary bond fund that is significantly affected by both rising and falling interest rates.

As of September 30, 2023 (the most recent date for which data is available), the Apollo Senior Floating Rate Fund has 92.4% of its assets invested in floating-rate securities. The remainder of the fund's assets are invested in junk bonds:

Apollo Public Funds

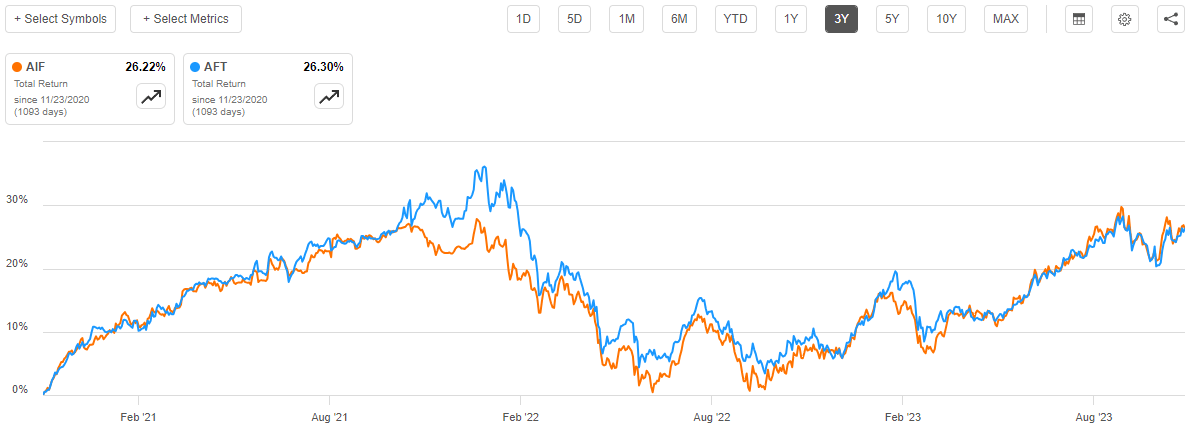

This is a much larger exposure to senior floating-rate loans than the Apollo Tactical Income Fund, which acts as something of a sister fund to this one and has gained a great deal of popularity with investors due to its strong performance throughout the current monetary tightening period. The two Apollo funds have actually delivered almost identical total returns over the past three years:

{kind=link}

We can see that the Apollo Senior Floating Rate fund did outperform its sister fund in late 2021 and early 2022. That was around the time that investors began to get nervous about the Federal Reserve potentially raising interest rates. We can see this in the fact that the S&P 500 Index ( SP500 ) peaked right about the same time:

{kind=link}

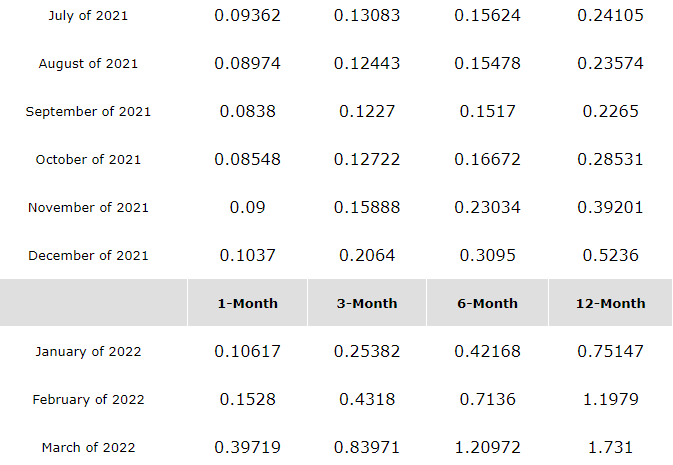

That could explain why the Apollo Senior Floating Rate Fund outperformed its sister around that time. The six-month and twelve-month LIBOR started to climb in earnest in October and November of 2021 compared to September 2021 levels:

{kind=link}

Notice how six-month LIBOR sat around 0.15% and twelve-month LIBOR sat around 0.23% until both numbers started climbing quickly in November. The rise in interest rates should benefit the Apollo Senior Floating Rate Fund more than its hybrid tactical cousin, as the traditional bond exposure of the latter fund would hold its returns down in comparison. That is exactly what we see by looking at the performance of the Apollo Senior Floating Rate Fund against the Apollo Tactical Income Fund.

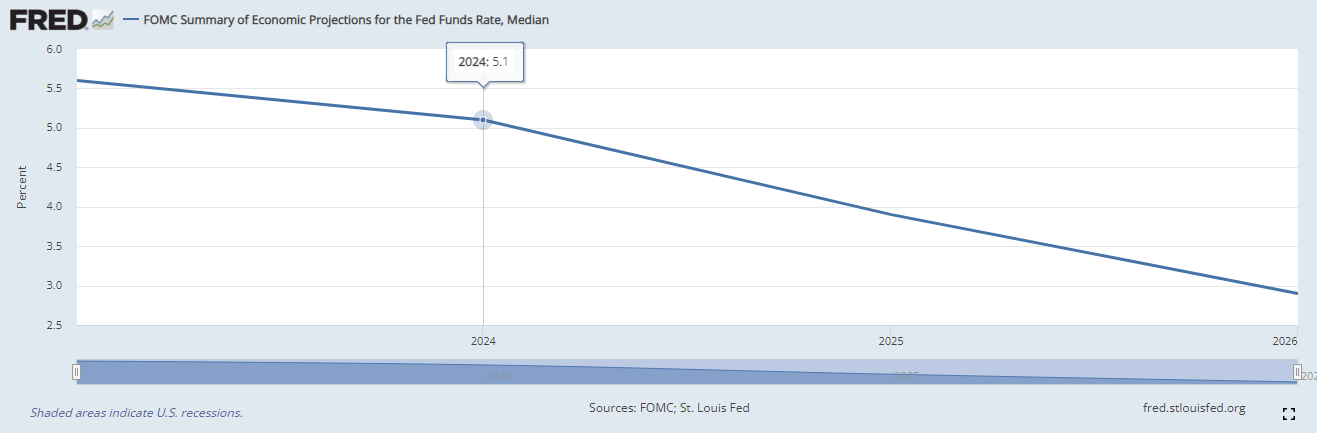

This could mean that the Apollo Senior Floating Rate Fund could be a slightly better holding for someone who expects that rates will go up further from here. I doubt that very many people, apart from a few fringe economists, believe that. As I pointed out in a few recent articles (see here and here ), the Federal Reserve seems content to hold the federal funds rate at its current level for now. The median prediction of the members of the Federal Open Market Committee is a single 25-basis point cut next year.

{kind=link}

However, the Federal Reserve has strongly implied that it wants long-term rates to be a lot higher than they are right now. It was seemingly more comfortable with the ten-year U.S. Treasury (US10Y) around 5% than it is with it at 4.383% as it is today. If the market keeps pushing long-term rates down, there is always a chance that the central bank might sell its own holdings of U.S. Treasury securities into the market or take some other action to push bonds down and rates up. That action would benefit the Apollo Senior Floating Rate Fund more than the Apollo Tactical Income Fund. However, that is simply speculation and, as with most predictions about the Federal Reserve's future activities, nobody knows for sure.

It may be a wise decision to pair something like the Apollo Senior Floating Rate Fund, which benefits from higher interest rates, with a junk bond closed-end fund in your portfolio. This way, you are basically in a good position regardless of interest rate movements and still collect the high level of income that is currently possible with these funds today.

As mentioned in the fund's description on the webpage, the Apollo Senior Floating Rate Fund invests primarily in securities issued by below-investment-grade companies. This is pretty typical for a floating-rate fund, as floating-rate loans are generally only made to companies that already have a substantial amount of debt ("leveraged loans") or are otherwise financially strained to the point that they are unable to issue fixed-rate bonds with an acceptable yield. After all, with a floating-rate loan, the borrower takes on the interest rate risk. The investor takes on the interest rate risk with traditional bonds. No company wants to take on interest rate risk unless they have no other choice.

The fact that this fund invests mostly in junk-rated securities may concern those investors who are worried about the preservation of the principal. After all, it is fairly well known that companies whose credit ratings are below investment grade have a much higher risk of defaulting on their debt and causing the investor to lose all of the money that was invested. Fortunately, we can derive a certain amount of comfort from looking at the credit ratings carried by the securities in the fund. The website includes an interactive chart that provides this information, but it is not suitable for inclusion in this article. As such, I have reproduced the information in this chart:

| Credit Rating |

| % of Total Assets |

| BB |

| 1.4% |

| BB- |

| 2.8% |

| B+ |

| 0.5% |

| B |

| 27.6% |

| B- |

| 34.3% |

| CCC+ |

| 5.3% |

| CCC |

| 3.0% |

| CCC- |

| 0.4% |

| Not Rated |

| 24.7% |

A junk bond is anything rated BB or lower, which clearly applies to everything in this chart. The only possible exception would be some of the unrated securities, which might be investment-grade securities. That seems very unlikely though, as any company that is capable of obtaining an investment-grade credit rating will almost certainly do so as it saves a considerable amount of money in interest over the life of the loan. Thus, we can assume that pretty much everything that is held by this fund is a junk bond or similar.

Fortunately, we can see that 66.6% of the fund's holdings have a credit rating of B- or above. This should provide a certain amount of comfort to those investors who are worried about the risk of default-related losses. According to the official bond ratings scale , any company whose securities have a BB or B rating has sufficient financial strength to carry its debt even in the event of a short-term economic shock. This could be important right now since the Federal Reserve has basically stated that it will not cut interest rates to the degree that the market expects unless a severe recession occurs in the next few months. The fact that most of the companies whose securities are held by this fund should be able to weather such an event without defaulting is something that should make it much easier to sleep at night.

Leverage

As is the case with most closed-end funds, the Apollo Senior Floating Rate Fund employs leverage as a method of boosting its effective portfolio yield beyond that of any of the underlying assets. I explained how this works in a number of previous articles. To paraphrase myself:

Basically, the fund borrows money and uses that borrowed money to purchase high-yield floating rate securities and junk bonds. As long as the yield of the purchased securities is higher than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, this will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not employing too much leverage since that would expose us to an excessive level of risk. I generally do not like a fund's leverage to exceed a third of its assets for this reason.

As of the time of writing, the Apollo Senior Floating Rate Trust has leveraged assets comprising 35.87% of its portfolio. This is a bit above the one-third level that I would like to see, but in this case, there should not be too much reason to worry. The biggest risk of running a leveraged portfolio is volatility, and as we have already seen, floating-rate securities do not have much volatility. Any risk that the fund is exposed to should the interest rate on its borrowings increase is offset by the fact that the securities in the fund are floating rate themselves. Thus, we probably do not need to worry too much about the fund's leverage.

Distribution Analysis

As mentioned earlier in this article, the Apollo Senior Floating Rate Fund has the primary objective of providing its investors with a very high level of current income. In order to achieve this, the fund invests in a portfolio that primarily consists of speculative-grade floating-rate securities that deliver most of their total return in the form of direct payments to the fund. The fund borrows money in order to control more securities than it otherwise could with only its assets, which has the effect of boosting its yield further to the extent that the yield on the purchased securities exceeds the rate that the fund pays on the borrowed money. The Apollo Senior Floating Rate Fund pools all of the money that it collects from the securities in its portfolio and pays it out to the shareholders, net of the fund's own expenses. It might therefore be expected that the fund's shares will boast a very high yield.

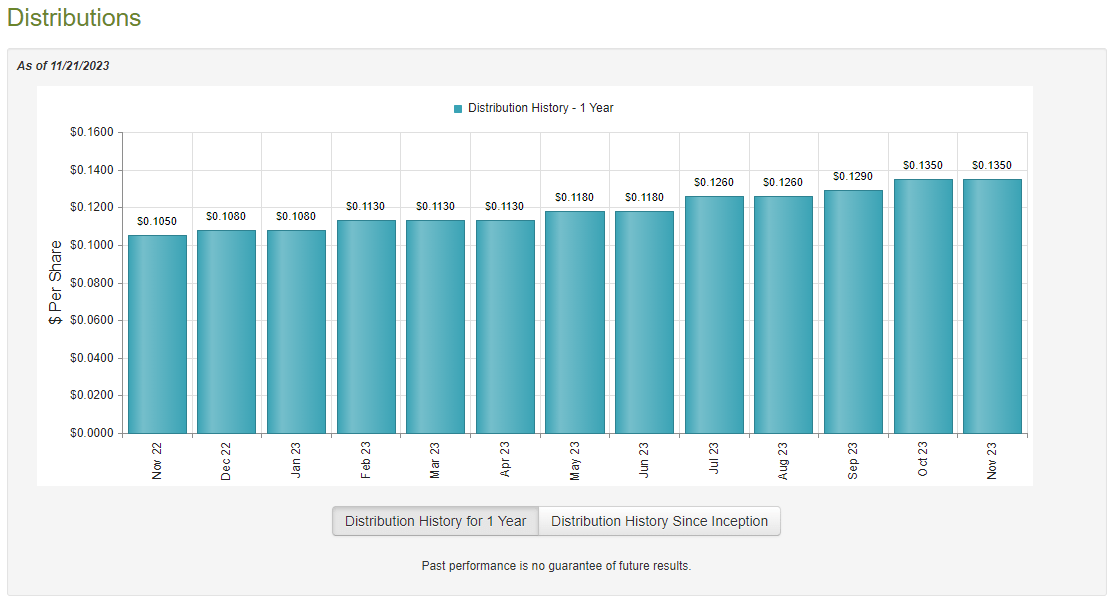

This is certainly the case, as the Apollo Senior Floating Rate Fund pays a monthly distribution of $0.1350 per share ($1.62 per share annually). This gives the fund a 12.36% yield at the current share price. Unfortunately, the fund has not been particularly consistent with respect to the distribution over time. In fact, the fund's distribution has varied significantly from month to month in many cases:

{kind=link}

This may be a bit of a turn-off for those investors who are seeking to receive a safe and secure income from the assets in their portfolios. That is a category that almost certainly includes many retirees. However, the fund has been consistently increasing its distribution over the past year, as it has delivered six distribution increases in the past twelve months:

{kind=link}

This sort of variability with respect to the distribution is exactly what we would expect from a floating-rate debt fund. This is because the securities in the fund pay out a higher coupon when interest rates go up, which increases the fund's income. The fund will naturally reward its shareholders by raising its distribution to ensure that its payments keep relatively on track with its income.

We should still examine the fund's finances, however. After all, we do not want the fund to be paying out more than it actually earns since such activity is destructive to the net asset value and may cripple the fund in the long term.

Fortunately, we have a relatively recent document available that we can consult for our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is a reasonably good period to analyze since it was generally characterized by a strong market that was very optimistic that interest rates would soon be cut. While that assumption was wrong, it still had an effect on asset valuations and the fund's ability to turn profits during this period. While floating rate securities tend to be very stable in terms of price, the market's interest rate expectations do play a role in how much income the fund's securities bring in, since some of them may have a coupon benchmarked against U.S. Treasury securities.

During the six-month period, the Apollo Senior Floating Rate Fund received $18,792,406 in interest from the securities in its portfolio. The fund did not have any other source of income, so this was also its total investment income during the period. The fund paid its expenses out of this amount, which left it with $12,237,296 available for shareholders. That was more than enough to cover the $10,636,751 that the fund paid out in distributions during the period. Thus, it appears that this fund is simply paying out its net investment income to its investors. This is generally what we would like to see from a debt-focused closed-end fund. Overall, the distribution should be sustainable as long as interest rates remain at their current level.

Valuation

As of November 21, 2023 (the most recent date for which data is available as of the time of writing), the Apollo Senior Floating Rate Fund has a net asset value of $14.90 per share but the shares currently trade for $13.10 each. This gives the fund's shares a whopping 12.08% discount on the net asset value at the current price. That is not as good as the 13.01% discount that the fund's shares have had on average over the past month, but as I have pointed out before, a double-digit discount is generally a reasonable price to pay for any closed-end fund. As such, the entry price seems to be okay here.

Conclusion

In conclusion, the Apollo Senior Floating Rate Fund is easily one of the best floating-rate debt funds available in the market today. The fund's distribution is fully covered by net investment income, which is nice, and the fund is trading at a fairly large discount on net asset value. The fact that the fund's securities provide a hedge against rising interest rates could be useful too, as the Federal Reserve wants rates to be higher than the market and it does have some tools that it could use to accomplish that goal. Investors may want to pair this fund with an ordinary junk bond fund to protect themselves from either rising or falling rates.

The possible merger is definitely a medium-term wildcard, but at the moment nothing is certain about that and anyone buying the fund today still has a few months to use it as a source of income until anything happens with respect to that event.

For further details see:

AFT: A Good Floater If The Market Is Wrong About Rates, Or A Potential Hedge