AFT - AFT: Grow Your Income With This 11% Yielding CEF

2023-09-07 03:20:40 ET

Summary

- Apollo Senior Floating Rate Fund focuses on senior secured leveraged loans, with a portfolio mainly consisting of single 'B' rated collateral.

- The fund has performed well, generating a total return of over 13% in the past year, benefiting from higher rates.

- The fund trades at a discount to NAV, which is expected to persist, but it has a low discount beta and is a good option for buy-and-hold investors.

Thesis

Apollo Senior Floating Rate Fund ( AFT ) is a closed-end management investment company that focuses on fixed income. As per its literature:

The Fund’s investment objective is to seek current income and preservation of capital by investing primarily in senior, secured loans made to companies whose debt is rated below investment grade and investments with similar economic characteristics. Senior loans typically hold a first lien priority and pay floating rates of interest, generally quoted as a spread over a reference floating rate benchmark.

The CEF comes from Apollo, a behemoth in the asset management business. To that end, it is interesting to see UBS now trying to re-negotiate the sale of the legacy Credit Suisse securitization business to Apollo. This asset manager is very well versed in credit lending, both in terms of origination as well as management.

It is surprising to see though that the top names in the fund are not Apollo sponsored deals:

Holdings (Fund Fact Sheet)

Both Solera and Gainwell are companies taken private by Veritas Capital , rather than Apollo. The way private equity works is via a public to private takeover concurrent with debt issuance. To that end, if a private equity fund identifies a company that is undervalued, they basically make an offer to buy the equity (at a premium) and then finance the entire take-over via debt. Debt is usually in the form of senior secured loans and unsecured debentures. The private equity entity then retains the equity portion, and thus the upside for the deal for when an eventual IPO/exit occurs. It is very customary to see large private equity sponsors like Apollo sprinkle the debt issuance for their own deals in their private label funds.

AFT focuses on senior secured loans which are floating rate, and thus have a light duration profile when compared to fixed rate bonds. However, what holds this fund back a bit is its large 'B' allocation, which brings in a large credit spread component. Fund has a rough 68% allocation to single 'B' credits, which brings its overall portfolio weighted average spread at 4.79%:

Risk Statistics (Fund Fact Sheet)

So on average, the loans in this portfolio pay SOFR + 4.79%. While SOFR is floating and thus has no duration (it is the index itself), the higher the credit spread, the higher the duration impact. It is akin to owning fixed rate bonds at 4.79%. The pure fixed bonds in this portfolio have a weighted average coupon of 7.47%.

With rates peaking as we speak, the duration aspect becomes less important, with the high yield generated by the fund becoming key:

{kind=link}

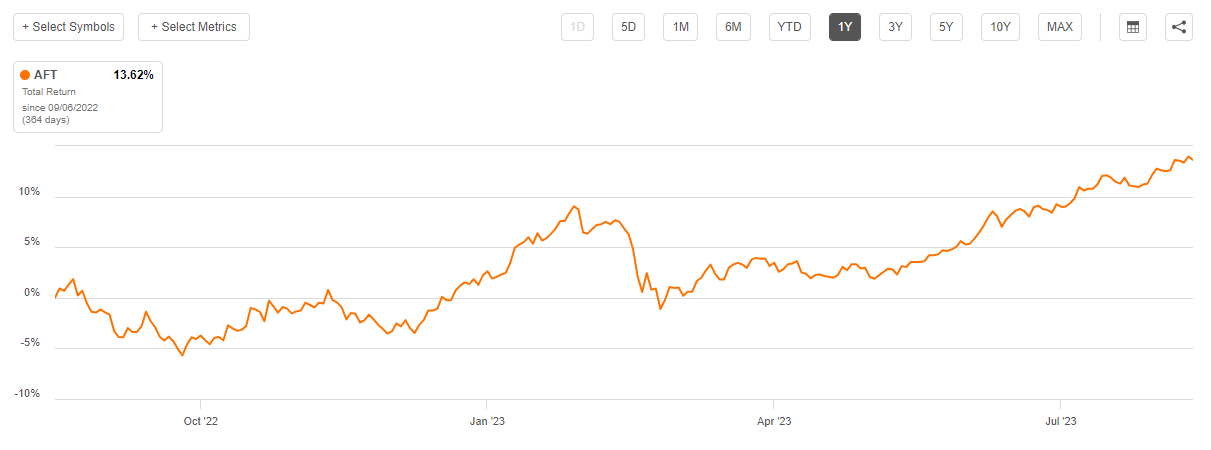

In the past year, the CEF has been able to generate a total return in excess of 13%, which is head and shoulders above many other asset classes. As long as rates stay high, this fund will deliver outsized returns due to the floating rate nature of the underlying collateral and high credit spreads.

Analytics

- AUM: $0.2 billion.

- Sharpe Ratio: 0.75 (3Y).

- Std. Deviation: 6.7 (3Y).

- Yield: 11%.

- Leverage Ratio: 35%.

- Discount to NAV: -12%

- Z-stat: 0.72

- Composition: Fixed Income - Leveraged Loans

- Expense Ratio: 2.63%

Premium / Discount to NAV

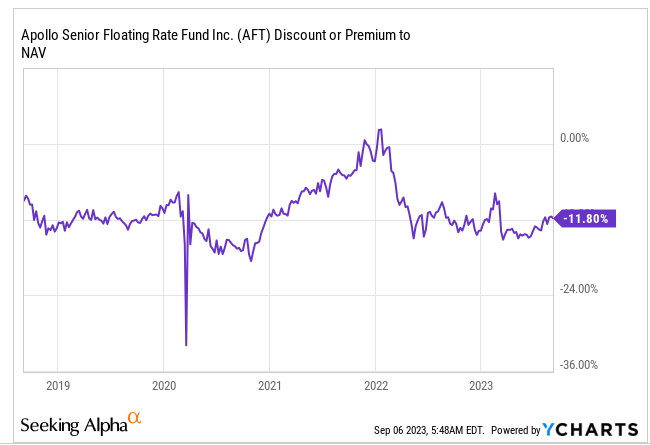

The fund usually trades at a discount to net asset value:

{kind=link}

We can see that historically the name has traded around the -11% discount mark, with large fluctuations driven by the rates environment only. During the zero rates period of 2020/2021, the fund actually moved to being flat to NAV, although the all-in yield was low.

Today the fund is back at trading at its usual discount, but to note that this figure is sticky. Do not expect this fund to generate an additional +11% return from the normalization of the discount. Not in 2024 or 2025 for sure. However, the bright side here is that the discount has a low beta - i.e. it does not fluctuate much. And that is a big positive for buy and hold investors. You want your holdings' returns to be driven by fundamental factors, rather than market perception and pricing of CEF shares.

Holdings

The fund contains 93 issuers, and has a weighted average rating of single 'B':

Fund Details (Fund Fact Sheet)

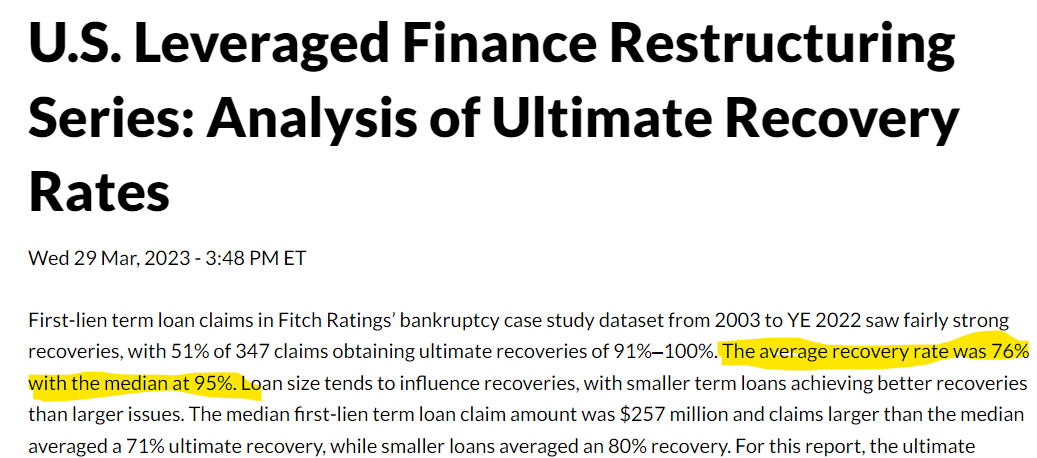

Although we are in the riskier territory here for junk debt, it is worth noting that leveraged loans are senior in the capital structure with a high historic recovery ratio. So if any of the issuers were to default, the equity contributed by the sponsor would be gone first, followed by any debentures, and then senior loans:

{kind=link}

In effect, based on a recent Fitch study, recoveries have been even better than historic norms, with average recovery rates at 76%. However, if there is a recession and the economy deteriorates, recovery rates will go down. There is a close correlation between bankruptcies and recoveries. The higher the bankruptcies, the lesser the capital that is going to look to inject new money and thus recovery rates go down.

The portfolio is made up almost entirely by floating rate leveraged loans, with a small fixed rate bond sleeve:

Portfolio (Fund Fact Sheet)

We can see that around 91% of the collateral is made up of loans, with 8.4% of the underlying being high yield bonds, while there is a small bucket for equity holdings.

Conclusion

AFT is a CEF from Apollo. The fund focuses on senior secured leveraged loans which make up around 91% of its portfolio. The collateral pool is mainly single 'B' rated, with an average spread over SOFR of 4.79%.

The fund has done very well in the past year, being up more than 13%, its floating rate collateral being able to pass to investors at higher rates. Expect this trend to continue. Until the Fed starts cutting rates (priced in mid-2024 by the forward Fed Funds market) AFT will be able to deliver outsized yields.

With a high recovery rate due to their position in the capital stack, leveraged loans remain an asset class to own. The CEF has a -11% discount, but do not expect this to narrow. Outside of the zero rates 2020/2021 period, this fund has always traded at a very similar discount to NAV. Expect to receive the current yield for another 12 months here. We like Apollo as a manager and this CEF in today's high rate environment, and thus are a Buy here.

For further details see:

AFT: Grow Your Income With This 11% Yielding CEF