AFT - AFT: Senior Loan CEF Double-Digit Distribution Yield And Discount

2023-09-14 09:16:38 ET

Summary

- Senior loans offer some of the highest yields in the market today.

- AFT is a particularly strong senior loan CEF, with a growing 11.5% yield, and large 11.3% discount. Both are strong on an absolute basis, and higher than average.

- An overview of the fund follows.

I've written several articles on senior loans and other variable rate securities in the recent past, due to their strong, growing dividends. I've focused on ETFs, as I tend to do. This time I thought to write an article on CEFs instead, as these sometimes offer investors particularly strong yields at cheap prices and wide discounts. Of these, the Apollo Senior Floating Rate Fund (AFT) seems to be a particularly compelling, strong choice.

As is the case for most senior loan funds, AFT offers investors a strong, growing 11.5% dividend yield, and very low interest rate risk. AFT's total returns are stronger than average, on both a NAV and price basis. AFT's 11.3% discount is higher than average for its peer group too, and higher than the fund's own historical average. AFT's growing 11.5% yield, strong performance, low interest rate risk, and high 11.3% discount, make the fund a buy.

AFT - Basics

- Investment Manager: Apollo

- Expense Ratio: 2.63%

- Management Fee: ~1.40%

- Distribution Yield: 11.50%

- Discount to NAV: 11.33%

- Total Returns CAGR 10Y: 5.26%

AFT - Investment Thesis

AFT is an actively-managed CEF focusing on senior loans. AFT's investment thesis is quite thorough, and rests on the fund's:

- Strong, growing 11.5% yield , underpinned by its investments in high-yield senior loans

- Significant 11.3% discount to NAV , which boosts distribution yields, and could lead to sizable capital gains

- Very low duration and rate risk , of particular importance during a hiking cycle

- Above-average total returns , with the fund generally outperforming its peers and benchmark on both a NAV and price basis

AFT's many benefits combine to create a strong fund and investment opportunity, albeit one which is broadly inappropriate for more conservative, risk-averse investors. Let's have a look at each of the points above.

Strong, Growing 11.5% Yield

Some context first.

AFT focuses on senior loans, which are senior secured variable rate loans from non-investment grade corporations. These securities account for 91% of the fund's assets.

AFT

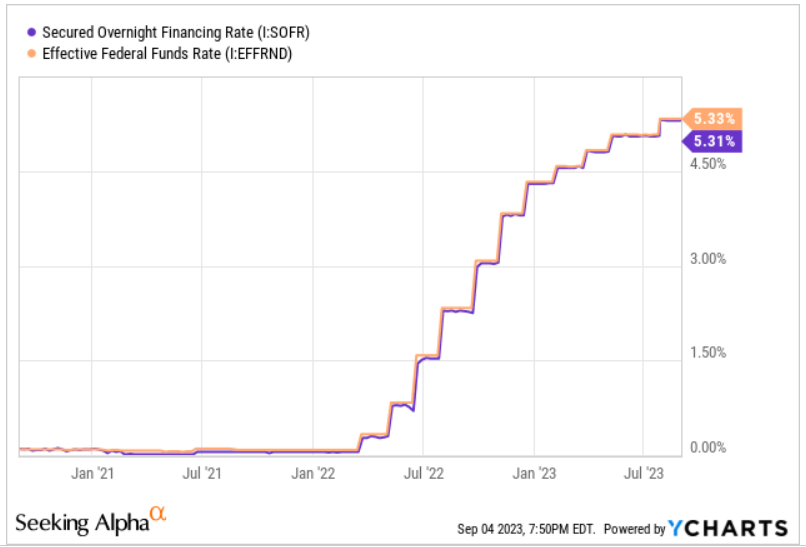

Senior loans are almost always variable rate loans, indexed to specific benchmark rates, and so see higher coupon rates when interest rates rise. Most are indexed to SOFR, a benchmark interest rate which closely tracks the federal funds rate.

{kind=link}

Rates are reset at specific intervals, generally quarterly.

So, simplifying things a bit, we can say that senior loans see higher coupon rates when the Federal Reserve hikes rates, and the Fed has hiked very aggressively these past few years. As can be seen above, rates have increased by around 5.3% since early 2022, leading to around 5.4% in higher rates for senior loans (other factors accounted for the extra 0.1%).

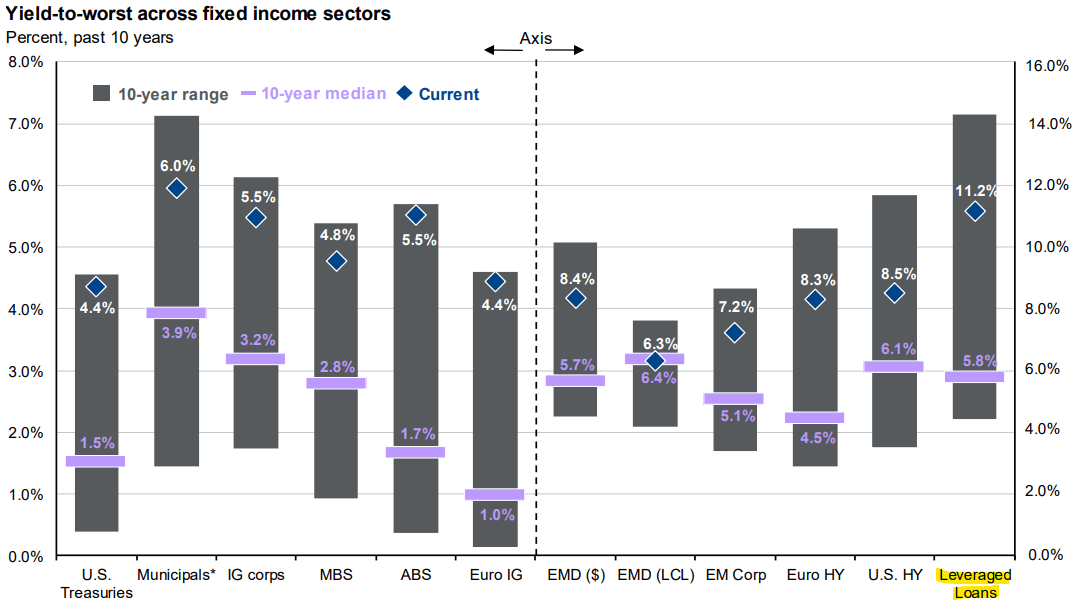

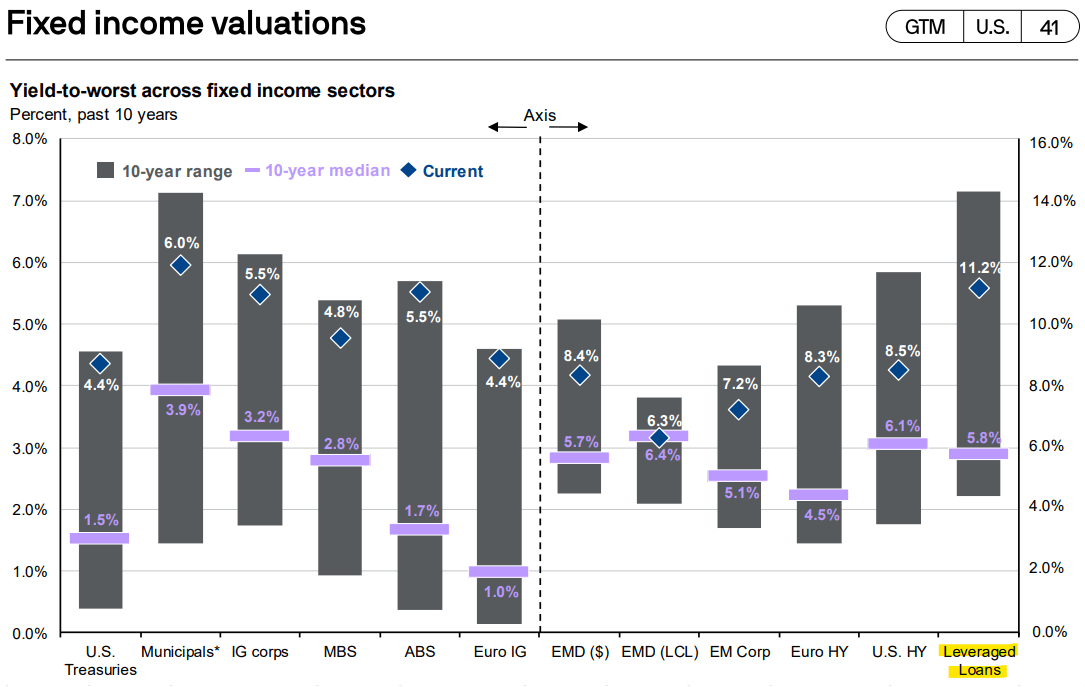

Due to these hikes, senior loans currently yield more than most other bonds and fixed-income securities, and by very healthy margins. Data as per J.P. Morgan ( JPM ), senior loans are referred to as leveraged loans in graph below.

{kind=link}

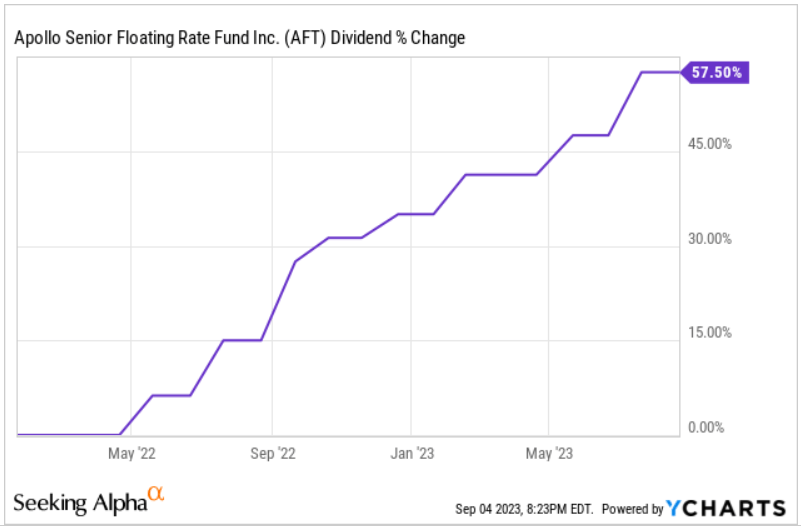

AFT focuses on senior loans, and so has benefitted from recent Fed hikes too. Dividends have grown by 57.5% since early 2022, a very strong figure.

{kind=link}

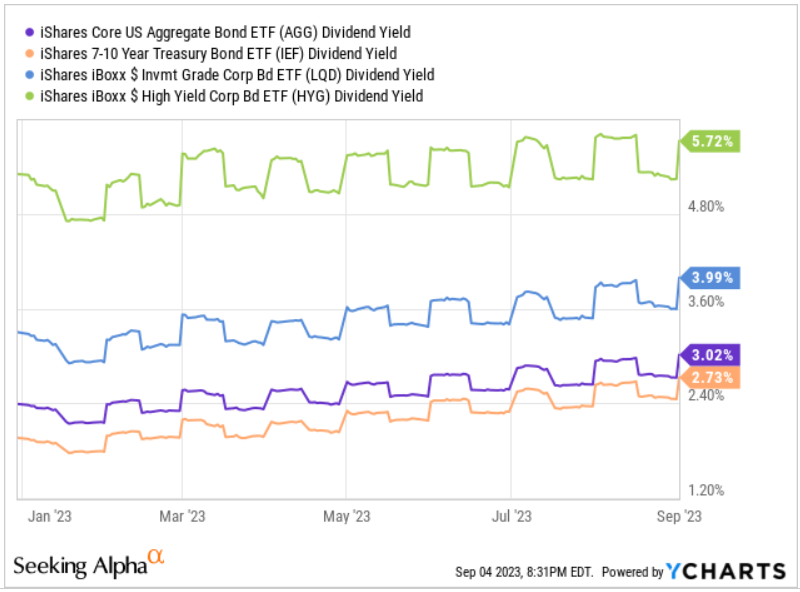

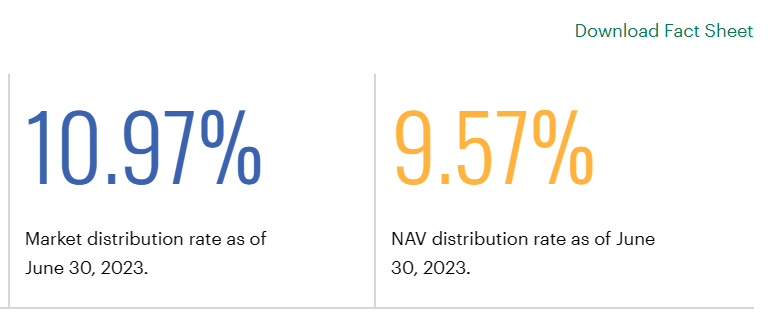

Yields themselves are also quite strong, with the fund currently sporting a 10.5% TTM distribution yield, and a 11.5% forward yield. Both are strong figures, and higher than those of most relevant bonds and bond sub-asset classes.

{kind=link}

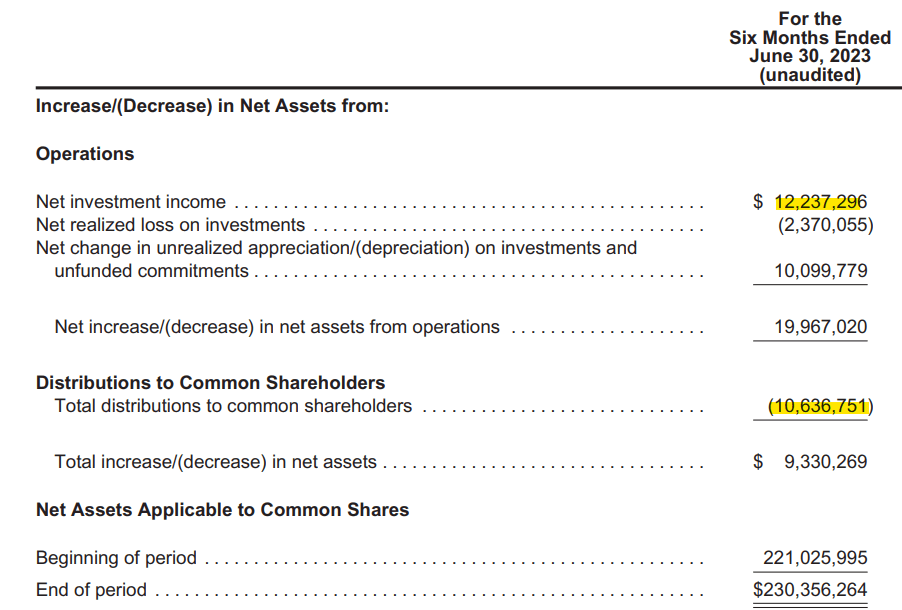

AFT's distributions are more than fully covered by underlying generation of income. In fact, as per its latest semi-annual report, the fund generates around 15% more in income than it distributes to shareholders. Under these conditions distribution hikes are exceedingly likely, as have occurred in the recent past.

{kind=link}

AFT's strong distributions are mostly the result of focusing on senior loans, the highest-yielding bond or income securities right now. Distributions are further boosted, by around 36.1%, by the fund's use of leverage.

AFT

Distributions are further boosted by the fund trading with a sizable 11.3% discount. Remember, higher discounts mean lower share prices, and hence higher yields. As per management, the fund's discount boosts its distribution by 1.4%, but these figures are somewhat outdated.

{kind=link}

AFT's leverage and discount to NAV means fund distribution yields are higher than those of most senior loan ETFs, including the benchmark Invesco Senior Loan ETF ( BKLN ).

AFT's strong, growing, fully-covered 10.5% distribution yield is a significant benefit for the fund and its shareholders, and core to its investment thesis.

Significant 11.3% Discount to NAV

AFT currently trades with a 11.3% discount to NAV. It is a significant discount on an absolute basis, and quite a bit higher than the fund's long-term average. It is also around twice that of the average senior loan CEF, as per CEF Connect data.

AFT's discount benefits investors in two key ways.

First, and as previously mentioned, higher discounts means lower share prices, and hence higher yields. AFT's double-digit discount boosts distribution yields by around 1.4%, as per management data.

A second benefit of high discounts is that these could potentially lead to capital gains, assuming discounts normalize. Discounts have normalized YTD, leading to sizable gains during the same timeframe. Discounts and returns have been both quite volatile, however.

Data by YCharts

Potential capital gains from narrowing discounts are at the whims of the market and might fail to materialize. Higher yields, however, are not dependent on the whims of the market, and are a much more certain, much likelier benefit. Investors will almost certainly receive higher distribution yields from investing in AFT at a sizable discount, regardless of what the market thinks or does.

AFT's significant discount to NAV boosts yields and potential capital gains, two important benefits for the fund and its shareholders.

On a more negative note, the fund's discount was higher in prior months, and at roughly the same level since mid-2022. Z-scores are highly positive at the 1Y mark and lower. AFT's discount does remain high on an absolute basis, and relative to the fund's long-term average.

CEF Connect

Very Low Duration and Rate Risk

AFT focuses on senior loans, securities with negligible duration and rate risk. The fund has small investments in high-yield corporate bonds, with low duration, and notional investments in other securities. The result is a portfolio with very low duration and rate risk. Expect small, below-average losses during hiking cycles, as has more or less been the case since early 2022. AFT has posted positive NAV returns since said date, slightly outperforming expectations, but negative price returns, due to widening discounts.

Data by YCharts

AFT's very low duration and rate risk is a benefit for the fund and its shareholders. As the Fed has significantly slowed down/paused hiking, this is unlikely to provide any tangible short-term benefit for investors, but it remains an important long-term benefit.

As an aside, the fund's management has estimated the fund's duration at 3.5 years. Said figure is inconsistent with the fund's holdings or performance (too high). I think there is either a data issue, or some technicality around the fund's leverage or portfolio weights. Still, I thought to mention the figure in the interest of full disclosure.

AFT

Above-Average Total Returns

AFT's performance track-record is quite strong, with the fund consistently outperforming most bonds and bond sub-asset classes on both a NAV and price basis since inception. Returns have been particularly strong in the recent past, due to higher rates. AFT has outperformed benchmark senior loan funds too, due to leverage and, perhaps, management alpha.

Seeking Alpha - Chart by Author

The fact that AFT's total returns have been stronger in the recent past, weaker long-term, merits an explanation. Senior loans currently yield 11.2%, broadly in-line with the fund's 11.5% yield.

Senior loan yields have averaged 5.8% for the past decade, a bit higher than AFT's 10Y 4.6% NAV CAGR. The fund has somewhat underperformed expectations long-term, in part due to a recent widening of credit spreads.

{kind=link}

From the above, it seems clear that AFT's future returns are strongly dependent on interest rate and senior loan yields. Double-digit returns are likely if rates remain elevated. Returns should decrease to the high single-digits if the Fed cuts rates slightly. Returns should decrease to the mid single-digits if rates go back down to zero. Lots of assumptions in these figures, so take them with a grain of salt. Still, the broader point remains.

AFT's strong performance track-record is a straightforward benefit for the fund and its shareholders.

What About the Fed?

Federal Reserve cuts would mean lower senior loan coupon rates, directly reducing AFT's generation of income and almost certainly leading to distribution cuts. Significant cuts would almost certainly lead to higher prices for most fixed-income securities, not for senior loans, resulting in AFT underperformance.

Although the above is more or less true, the magnitude and timing of these matter too, as does market expectations. Right now, the market is expecting around 2.0%-3.5% in rate cuts , so senior loan performance should be reasonable enough if Fed cuts are in-line with expectations.

Looking at senior loans themselves shows similar expectations to the above. Senior loans generally yield about the same as high-yield corporate bonds, very slightly less, as these have similar credit risk. Right now, senior loans yield around 2.7% more, as the market expects around 2.7% in Fed rate cuts in the coming years.

Another way of interpreting the above is that senior loans would still yield more than all of its peers if the Fed were to cut rates by less than 2.7%. Senior loan spreads to high-yield bonds would reach historical average with 3.0% in cuts. Senior loan yields would reach long-term historical averages with 5.4% in cuts, meaning the Fed cutting to zero. The Fed has a lot of room to cut without jeopardizing senior loan rates.

In my opinion, the Fed is unlikely to cut rates at the required speed and magnitude to lead to senior loan underperformance. More dovish investors might disagree.

Why AFT?

In my opinion, senior loans are a buy, as are most senior loan funds. AFT itself does have two advantages relative to its CEF peers: above-average returns and discount to NAV. Data as per CEF Connect.

CEF Connect - Chart by Author

In my opinion, and considering the above, AFT is a somewhat stronger investment opportunity than the average senior loan CEF. Nevertheless, the fund does not significantly differ from its peers, and I'm broadly bullish on the sector/investment niche as a whole.

Conclusion

AFT's growing 11.5% yield, strong performance, low rate risk, and high 11.3% discount, make the fund a buy.

For further details see:

AFT: Senior Loan CEF, Double-Digit Distribution Yield And Discount