AGCO - AGCO: Compelling Valuation For One Of The Market Leaders

2023-11-07 10:13:48 ET

Summary

- AGCO Corporation is challenging Deere in the North American agricultural machinery market.

- AGCO is becoming a precision ag leader, as its recent JV with Trimble shows.

- AGCO currently trades at a steep discount.

Introduction

AGCO Corporation ( AGCO ) has still not found a place in my portfolio. And yet, it is a company I look a close eye on for two reasons. The first one is that I am overall bullish on the industry . The second one is that AGCO has committed itself to seriously challenging Deere ( DE ) in North America, declaring what I have previously called " The Green Tractors Battle ". In addition, though I have often liked CNH Industrial ( CNHI ) more - especially after its Iveco Group ( IVCGF ) spin-off - AGCO seems to be catching up with its peers in terms of margins.

Since AGCO recently reported earnings, it is time to go over this company for two reasons: see if its turnaround is moving at the right pace and understand what to expect from the upcoming reports of its two main peers.

The industry

Industrials usually trade at low valuations because they discount high competition, low margins and low returns on capital, and, above all, one of the biggest enemies for investors, aka cyclicality.

And yet, some industries within this broad sector are a bit different. One of these agricultural and farm machinery manufacturing. The market was estimated at $182 billion at the end of 2022 and it is expected to reach around $300 billion by 2032, at a CAGR above 5%.

Furthermore, it is highly consolidated, with a few big players taking the lion's share of total sales. This means that few manufacturers have to meet most of this huge demand. The consequence is clear: this is an industry where the leaders have more pricing power and higher margins compared to other industrial companies.

Mordor Intelligence

The market sees Asia with a 43% share, North America comes in second place with 31%, Europe is third with 19%, while Latin America has around 4% of market share. Not only is Asia the leader, but it is also the fastest growing region in the world. In addition, favorable macrotrends are helping the whole industry grow: increasing world population, the need for precision agriculture before a reduction of arable land due to urbanization, governments around the world seeking to shorten their food supply chains by bringing the producers closer than they are now.

AGCO

Here is where AGCO comes into play and stands out as a very interesting pick. The company, in fact, is a leading manufacturer of agricultural equipment, such as tractors (59% of sales), combines (5% of total sales), self-propelled sprayers, hay tools and forage equipment, seeding and tillage equipment, implements, grain storage and protein production systems (9% of total sales). In particular, it owns well-known brands such as Fendt, Massey Ferguson and Valtra. The first of these three - Fendt - is widely recognized as a premium brand, able to compete directly with the industry leader John Deere. Currently, AGCO has grown the Fendt market participation in North America from about 40% market coverage to 70-75% market coverage with a step-by-step dealer expansion that was described during the last earnings call . AGCO still expects to grow up to 90-95% in a couple of years both in North and in South America.

AGCO is strong in Europe, but it wants to penetrate North America, particularly through Fendt. This will help the company's margins and pricing power, making it able to close the gap at least with CNH Industrial , the second largest player in the industry.

Financials

Let's take a look at the general picture dating back from the beginning of the millennium. In purple we see AGCO's revenues, in orange its operating margin.

The cyclical nature of the business immediately stands out, affecting both its top-line and its margins. And yet, cycle after cycle, the business grows and so do its margins, showing how the company is turning more and more profitable as years go by.

Nowadays, AGCO is a business with a quarterly revenue above $3 billion and an annual revenue above $14 billion at the end of FY 2022. This year, current consensus sees AGCO's revenues coming in at $14.7 billion, but I would not be surprised to see the company come close to $15 billion.

In terms of profitability, AGCO scores an A- on Seeking Alpha . with a gross margin of 26% and a net income margin of 8%. But, most importantly, it has a high return on total capital of 18%.

The real question many investors have is this: how do I understand what part of the cycle AGCO is in? Clearly, the ideal buy would be at a trough in order to anticipate the future peak of the upcoming cycle. Usually, one of the key metrics used to answer is inventories. When inventories rapidly increase, it is a sign of a peak.

It is what is happening right now. It is not that difficult to deny this, once we think about what happened in the past three years. After the pandemic, we saw huge government spending, which is usually a tailwind for machinery. In addition, international conflicts such as the war in Ukraine put pressure on agricultural commodities, such as wheat. Together with soaring inflation, this created optimal conditions for farmers' net income.

Farmers have had purchasing power in the past few years. In addition, supply chain bottlenecks created pent-up demand, which lead to an even faster increase in inventories, where unfinished vehicles could not be delivered at the right time. This year, order books were full and machinery manufacturers have had quite a time trying to ship all the equipment that had been ordered.

In the meantime, demand is slowing down. So, we are seeing high revenue growth because of past pent-up demand. In particular, the company reported that large equipment is seeing increased sales, while smaller equipment is already declining YoY. This is clear. Larger equipment takes more time to be manufactured than smaller equipment. Therefore, with larger equipment, AGCO is still dealing with a lot of pent-up demand that has already been fulfilled when considering smaller equipment.

We are also seeing margin growth because of pricing (8% for AGCO this year) and cooling inflation. Yet, all of these things suggest that next year won't keep up with these strong trends. In addition, this year's projected farmer income will see a reduction from the $183 billion of 2022 to $143 billion and, if corrected for inflation, it will be below the 2021 level, but above the levels of every year between 2014 and 2020. This doesn't mean 2024 will be an awful year for these companies. It just means we are going towards a more normalized time.

Now, looking at two metrics from the cash flow statements, we can see an interesting thing about AGCO. Cash from operations has a cycle during the year, with the first quarter usually being negative. This is because during Q1 a company like AGCO buys most of the parts that will be assembled in its products through the year. Because of this, as the year unwinds, we see a growing amount of cash from operations towards the second half of the year, especially in Q4.

At the same time, capex is well under control, remaining pretty stable at $120 million per quarter.

As we can see from this slide taken from the latest results presentation, Ytd FCF is still negative, though only by $155 million, but it is expected to come in above $900 million, which is over double the FCF seen in 2022. Once again, this highlights how Q4 is usually the most important for FCF generation because inventories are sold down.

AGCO Q3 Results Presentation

Latest Results

A few days ago, AGCO reported its Q3 results .

Net sales hit a new record of $3.5 billion (+10.7% YoY). Europe and Middle East was up 14.2%, North America was up 3.4%, South America increased 26%, but Asia decreased 17%. Pricing was the primary contributor to higher sales.

Operating margin was 12.3%, a new high for the company and up 190 bps YoY. In particular, in South America the operating margin was 20.8%, while in North America it was 14.9% and in Europe 12.6%. This is the fifth consecutive quarter with operating margins above 10%, which is a significant threshold among machinery manufacturers.

EPS came in at $3.74 vs. $3.18 in Q3 2022.

However, these words stated by Mr. Hansotia, AGCO's CEO, need to be noted:

Increased crop production in the Northern hemisphere and strong yields in Brazil are driving higher grain inventories and weighing on commodity prices. While still at supportive levels, the lower commodity prices and a fleet age that is now trending younger are causing farmers to become more selective about their equipment and technology investments.

It is the first time in years I see a CEO noting how fleets are finally trending younger. So far, everyone was pointing out how fleets were aged and this was creating the perfect environment for sustained demand. This means many farmers have by now received their new and more technologically advanced equipment.

Now, up until a few years ago, the end of a replacement cycle would have been very bad news for a company like AGCO. However, though what Mr. Hansotia said seems to confirm the assumption we are near the peak of the current cycle, we have to factor in something new. In particular, farming is requiring more and more precision agriculture and autonomous solutions due to land and labor scarcity. These are high-margin segments that also carry along a lot of services: from spare parts to personalization and software. Therefore, it is a segment that also generates recurring revenue.

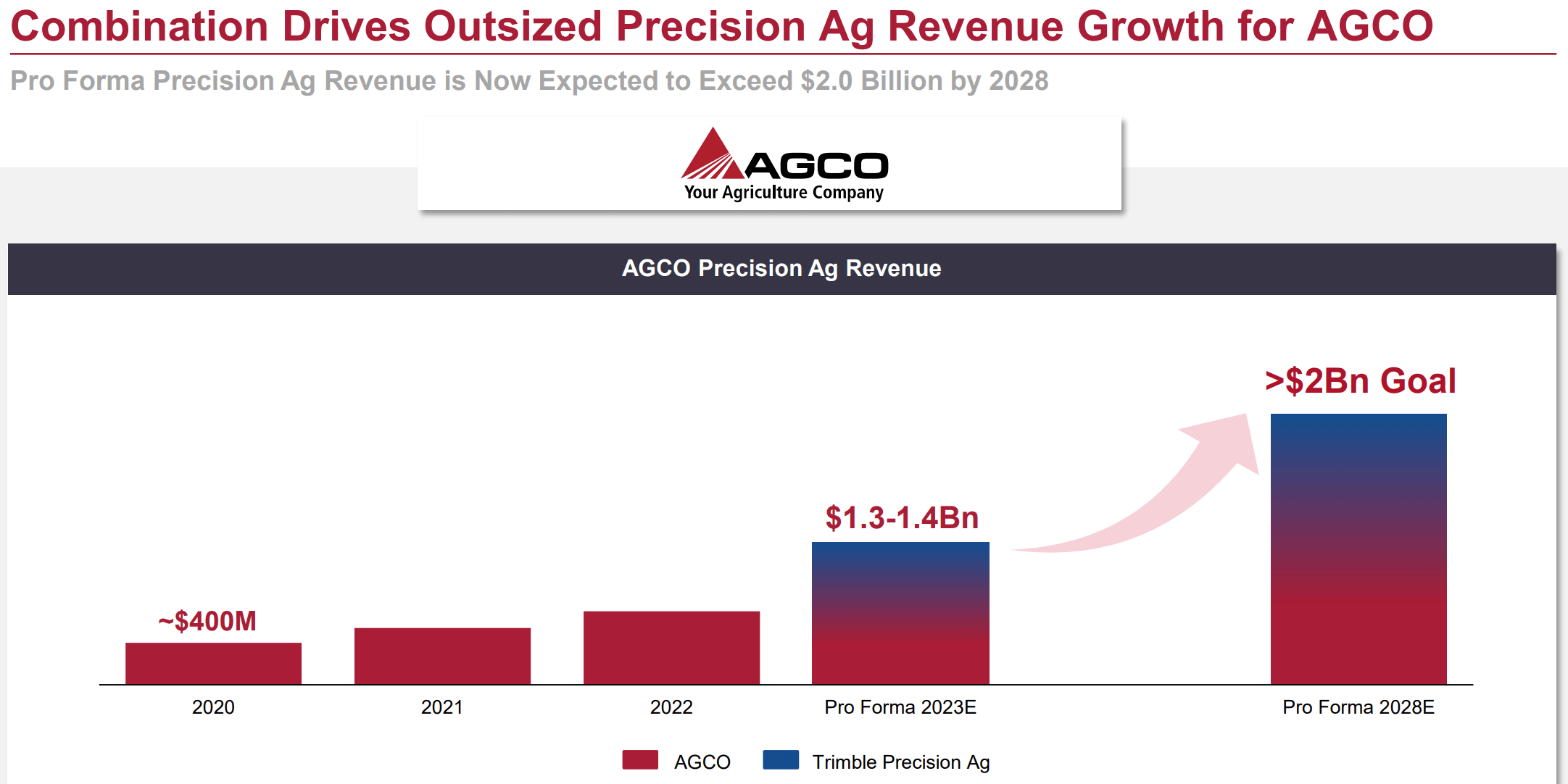

In addition, AGCO recently announced its joint venture with Trimble, a leading precision agriculture provider that designs, engineers and distributes hardware, software and cloud-based platforms for farmers. Trimble currently makes $535 million in revenue, with and EBITDA margin of 32%. Thanks to the combination of its business with Trimble, AGCO expects to see its Precision Ag revenue goal of $2 billion reached in five years, more or less a 50% increase from the 2023 expected revenue.

{kind=link}

While demand may be softening, this is a trend that won't go away and that will impact the next cycle for sure.

In the latest report, a few concerning trends were revealed:

We continue to limit order intake on some products to improve our on-time delivery rates, though other products are returning to a more normal order bank management. We currently have approximately seven months of order coverage for both large and small ag.

(Earnings Call Transcript)

Valuation

Currently, the stock has seen some weakness and it is trading at a market cap of $9 billion which is just 4x its TTM EBITDA. A 4x EBITDA multiple is very low and this is why AGCO's valuation grade is currently a B+ , dragged down from an A only by its dividend yield (on which we should spend a few words because, though it is 0.88%, it doesn't factor in that AGCO often pays a special dividend in the second quarter; this year, for example it paid $5 per share, which is a 4.2% yield alone, not counting quarterly dividends).

If we look at traditional metrics such as Fwd PE, Fwd EV/EBITDA or Fwd P/FCF, we have compelling metrics: Fwd PE of 7.9, Fwd EV/EBITDA of 5.2 and Fwd P/FCF of 6.3.

For a company with premium products such as the ones AGCO has and with a growing high-margin business set to drive sales and profits up in the next few years, these are very low metrics, especially considering Agco is improving its profitability at a quick pace.

I personally think a 4x EBITDA multiple is too low for a company such as AGCO. Even a 7x would still be low, but, assuming investors want to highly discount the cyclical nature of the business and thus use a single-digit multiple, we would be before a potential market cap of $14.2 billion, which is a 57.8% upside from the current levels.

This is why I rate the stock as a buy and I am adding it to my watchlist in order to monitor it closely in the upcoming weeks.

For further details see:

AGCO: Compelling Valuation For One Of The Market Leaders