DE - AGCO's Challenge To Deere: The Green Tractors Battle

Summary

- AGCO needs to grow its North American market share.

- The company is putting a lot of effort in expanding its premium German brand Fendt to steal market share from Deere.

- In this article, I would like to go over the "green tractors battle" to assess if it can offer an interesting opportunity for investors.

- Of course, the analysis will be supported by charts and graphs that paint a picture of relevant aspects of the North American farming equipment market.

Introduction

AGCO ( AGCO ) wants to challenge Deere ( DE ) on a very clear battleground: large agriculture and precision agriculture equipment in North America.

The reason? North America is the largest high-margin market on the planet.

How will AGCO pursue this goal? Through strengthening its brand Fendt, pushing new sales. The fight is clear: AGCO wants to eat a larger portion of the pie of North American premium tractor sales.

In this article, I would like to go over this strategy to see if the company can reasonably expect meaningful improvement and how it will benefit AGCO.

This time, I will share my reasoning starting from the company and then moving on to spend a few words on the economic environment to see if there is reason to believe AGCO can achieve its goal.

Summary of previous coverage

Last year, although I always thought AGCO to be a buy, I pointed out that the company seemed to be lagging behind CNH Industrial ( CNHI ) and John Deere in terms of margins. In fact, AGCO struggled to reach a double-digit margin. This was also due to its weakness in North America compared to the other two competitors. In fact, the company's main market is still Europe, where high-energy prices and the war in Ukraine seemed to depress consumer spending and sentiment.

At the end of Q322, AGCO was however able to finally reach its double-digit margins, as I pointed out in the article: AGCO: Turnaround Quarter Has Come. The company reported that Fendt performed particularly well.

An overview of AGCO's sales

AGCO provides investors with a regional net sales results slide, useful to grasp at a glance what is going on. As we can see from the latest available report, AGCO's net sales in North America increased their weight on total sales by 2 percentage points, with a strong acceleration in Q3 where sales were up 44% YoY (up 19% YtD).

{kind=link}

The company has made it clear to investors that part of its future success comes from growing in North America by pushing Fendt to play a larger role in the market. Just to get an idea, during the last earnings call, Fendt's name was mentioned 21 times. Fendt is currently Germany's most popular brand tractor. This is already a good sign, as Germany is a very demanding market, where products - especially machinery - are expected to offer high-quality, precision and reliability. I have seen it many times: once a product is accepted in Germany, it has the quality to please customers all around the world.

I think it is important for SA readers to go quickly through the main points that were disclosed about AGCO's strategy, to help everyone know what the management is thinking.

Mr. Hansotia, AGCO's CEO and the other members of the management team, clearly stated Fendt needs to be taken global:

The first focus area is taking our Fendt full line brand global. We are working to grow the business along two vectors. The first is expanding the Fendt product line beyond tractors in the combines, planters, and sprayers, where we have top-performing products across the board. The second is taking the Fendt full line products global.

How is the company doing this? It has worked on upgrading Fendt's offerings to the market, coupled with efforts to grow Fendt dealerships throughout the continent. Just to get an idea, since AGCO began investing in 2018 in its dealership network, it was able to add in 2 years - from 2018 to 2022 - 80 new locations for a total of 206 dealers in 2020 (this is the last available data I was able to find).

At the same time, AGCO focused on expanding Fendt's product portfolio, as we heard during the last earnings call:

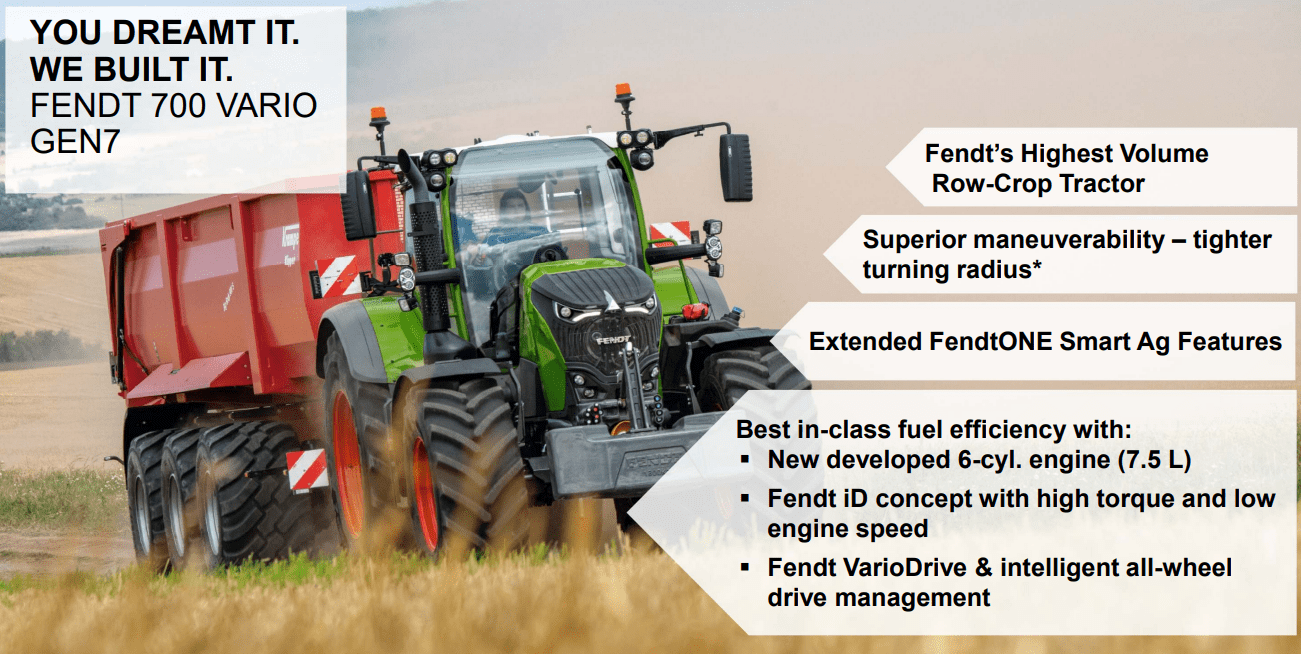

One of the ways we are growing our premium Fendt business is by continuing to expand and upgrade our product offerings. During the third quarter, we had a global launch event for the Fendt 700 Series. This high tech tractor ranges from 200 horsepower to 300 horsepower and is the highest volume row-crop tractor Fendt sells.

We can see the Fendt 700 Vario Gen 7 here below. A side note, the tractor was awarded the "Farm Machine 2023" title in the 180-280hp tractors category. Tractors of this category are a key to success, since here goes a big portion of large agriculture equipment demand.

{kind=link}

Success of this new model is thus quite important for Fendt's strategy to play out. Unfortunately, the company doesn't disclose some numbers about Fendt's performance in this key market. However, during the earnings call, AGCO's managers felt confident to say:

We are seeing excellent demand for the technology-rich Fendt full line up of equipment, our Precision Planting solutions and replacement parts. [...] Interest is growing in our premium Fendt product lines in both North and South America. Our Fendt and Challenger combined sales in North and South America are expected to double in 2022 compared to 2020. Our ambitious target is to double them again over the next five years to seven years.

Although we are lacking some numbers, Fendt's growing market share seems to have caught Deere's attention already two years ago, when Deere was reported offering strong incentives to its dealers to take in Fendt tractors.

Market Outlook

Besides investing to increase production, I think AGCO can rely on a few aspects to see its strategy turn out successfully.

First of all, farmer net income is expected to remain high as corn and other crops are still trading at historically high prices while inflation and - in particular - energy price are cooling off.

Secondly, take a look at this chart. It shows how the acres where corn was harvested in the U.S. are trending downwards.

USDA, National Agricultural Statistics Service

Now, this may look worrisome, since we all know about the growing need for corn and other crops as a consequence of the war in Ukraine and of the fast development (and growing hunger) of many countries around the world.

However, let's zoom out and look at the last century. In this following chart, we see the harvested area in the U.S. to be more or less the same as 100 years ago.

USDA, National Agricultural Statistics Service (U.S. corn area and yield)

However, the yield (measured as bushels per acre) has dramatically increased more than three times. This is thanks to fertilizers and technological innovations. And here is my point: AGCO is a leader in precision agriculture. The need for a growing yield, in a time where fertilizers are quite expensive, has to be met by technological innovations. This is also creating a new and prolonged equipment replacement cycle that must be seen as a strong tailwind for the company.

But why should AGCO benefit more than its peers from this trend? For two reasons: AGCO is not well-established in the continent and, more importantly, demand is greater than the supply the market leader - Deere - offers. This last reason necessarily leads many farmers to look at other manufacturers that can provide premium tractors.

We must not forget that in every earnings call we heard from CNH Industrial, Deere and AGCO, the building of pent-up demand for new farming equipment was often reported and highlighted. Supply chain bottlenecks have done nothing other than hindering further this huge demand, filling order books with orders that extend well into Q3 of 2023. In the meantime, the existing fleets age, creating additional future replacement demand while generating a lot of new streams of revenue for the spare parts business of these companies.

Let's look at a chart I already shared in my last article on Deere. Here we see the situation in Canada: unfilled orders are still high. In other words, companies such as AGCO have a lot of incoming revenue from their order books.

Farm Credit Canada (FCC)

To this situation, we have to add another fact: inventory levels for 4wd tractors and combines - the top tier products - are still far from recovering their pre-Covid highs. Actually, projections believe inventories to remain rather tight through the end of 2024.

Farm Credit Canada (FCC)

The more I look at these data, the more I am prone to think Deere unlikely to be able to satisfy North America demand for premium large ag tractors and combines. We are in a situation that should last at least for two years, and we will inevitably see some demand for Deere's products shift towards other solutions. Not everyone can wait for a Deere. Where will this demand go? Some of it has turned to CNH Industrial, which is the second-largest player in the industry. However, the company doesn't own a premium brand like Fendt. This is why I believe AGCO should benefit from the situation in North America. Investors will be able to see if this turns true by looking at the overall operating margin. If it regularly comes in at double-digits, I think it could be a sign of Fendt's success in the new continent.

Valuation

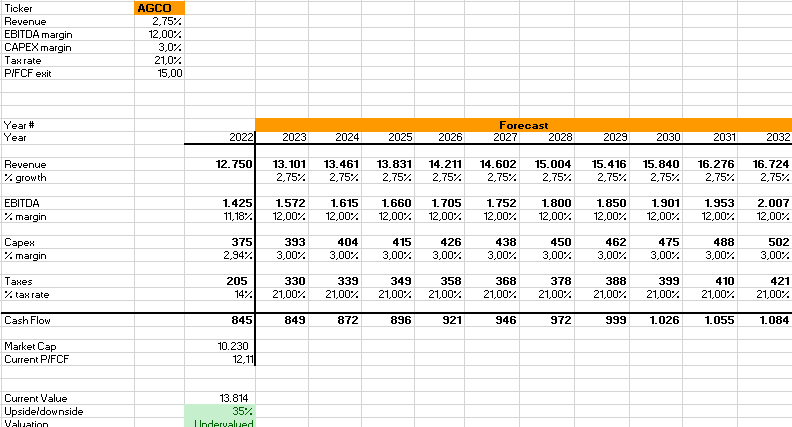

Some readers may be familiar with this table I usually share to get a rough idea of what I can expect from future cash flows of a company. I lowered my average rate for revenue growth to consider one or two mild recessions in the next decade. However, I brought the EBITDA margin up to 12% so that we consider the Fendt impact. I then use a price/free cash flow exit multiple to get an idea of the current valuation.

{kind=link}

The result confirms what I have been saying for a while. Though near ATHs, AGCO's valuation is still interesting (SA rates it with a C+) and it offers some upside. Over the past year, AGCO has beaten the S&P500 by a large extent (+20% vs. -8.6%) and it still isn't trading at inflated valuations, given its 11.5 PE or its 8 EV/EBITDA. However, what I really believe can make AGCO a good investment is not only its current valuation, but, rather, the way its strategy in North America will play out. I think this can significantly swing the needle, making the company more profitable and, as a consequence, right now cheaper than what it seems.

For further details see:

AGCO's Challenge To Deere: The Green Tractors Battle