VT - AGD: A High Fee Closed-End Fund To Avoid

2023-11-24 23:45:04 ET

Summary

- The abrdn Global Dynamic Dividend Fund aims to provide investors with high current dividend income, with a focus on qualified dividend income.

- AGD has performed poorly on both an absolute basis and historical basis relative to global equity capitalization weighted index funds.

- AGD has a very high total annual operating expense ratio of 1.16%.

- While AGD trades at a substantial discount to NAV, the fund lacks any near-term catalysts which would suggest this discount will narrow.

- I believe investors should avoid AGD and instead consider index funds such as ACWI or VT.

Closed-End Fund Overview

The abrdn Global Dynamic Dividend Fund ( AGD ) seeks to provide investors with high current dividend income with more than 50% being qualified dividend income. The fund also focuses on long-term growth of capital as a secondary investment objective.

AGD is an actively managed fund and benchmarks itself against the MSCI All Country World Index.

Currently, AGD has ~$246 million in net assets and has a total annual operating expense ratio of 1.16%. Fund characteristics include 2% leverage, a market distribution rate of 7.34%, and a NAV distribution rate of 8.41%.

AGD has performed poorly on both an absolute and risk adjusted basis historically compared to capitalization weighted global index products. AGD charges a very high management fee and is positioned in a market category which has proved especially challenging for active managers. While AGD is trading at a substantial discount to NAV, there are no catalysts which suggest this will narrow anytime soon. For these reasons, I believe investors should avoid AGD and instead consider low fee global equity index products.

High Management Fee

AGD has a very high expense ratio of 1.16%. To put that into context, the average expense ratio for an actively managed equity mutual fund is ~0.66% and the average equity ETF expense ratio is ~0.16%. Comparably, the iShares MSCI ACWI ETF (ACWI) charges an expense ratio of 0.32% while the Vanguard Total World Stock ETF ( VT ) charges an expense ratio of just 0.07%.

Per Morningstar research , as of June 30, 2023, just 10% of World Large-Blend funds have outperformed their benchmarks after fees suggesting that this space is relatively efficient and not an easy category for active fund managers to add value.

Historical Performance

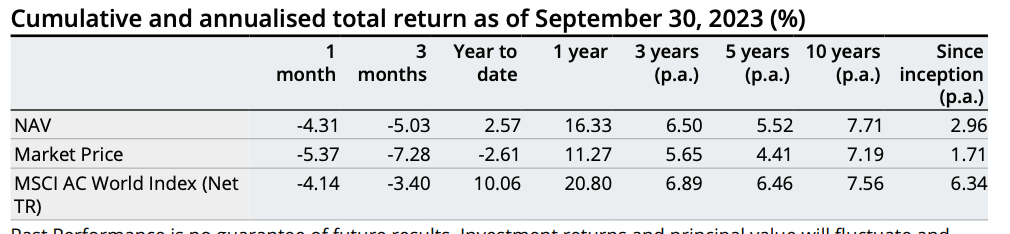

AGD launched in July 2006 and has significantly underperformed its benchmark, the MSCI All Country World Index. As shown below, as of September 30, 2023 AGD has delivered an annualized return of 2.96% compared to an annualized return of 6.34% for the MSCI All Country World Index.

Since the inception of the MSCI ACWI ETF ( ACWI ) in March 2008, AGD has delivered a total return of just 17.9% compared to a total return of 163% for ACWI.

In addition to performing significantly worse than ACWI on an absolute basis, AGD has also performed significantly worse on a risk adjusted basis. As shown by the chart below, AGD has realized an average 30 day volatility of 20.9% compared to 17.4% for ACWI.

One reason why AGD has experienced additional volatility is due to the added volatility related to the level of discount to NAV.

{kind=link}

Discount to NAV

AGD is currently trading at 13.9% discount to its NAV. This represents a significant discount on an absolute basis and a modest discount to AGD's historical norm.

Over the past 10 years, AGD has traded at an average discount to NAV of 11.7%. However, closed-end funds are generally trading at above-average discounts to NAV currently. According to BlackRock, the median closed-end fund is now trading at a discount of 10.7% compared to a 5-year median discount of 7.4%.

Given the relatively liquid nature of AGD's holdings, it might be surprising that the fund trades at such a high discount to NAV. However, AGD is not an easy fund to implement an arbitrage strategy with as positions are actively managed. Moreover, there are not currently any catalysts such as an activist fund holder campaign which would provide investors a way to agitate for changes which could result in a reduced discount to NAV.

For these reasons, I am not convinced that the discount will narrow in the immediate future.

Holdings Analysis

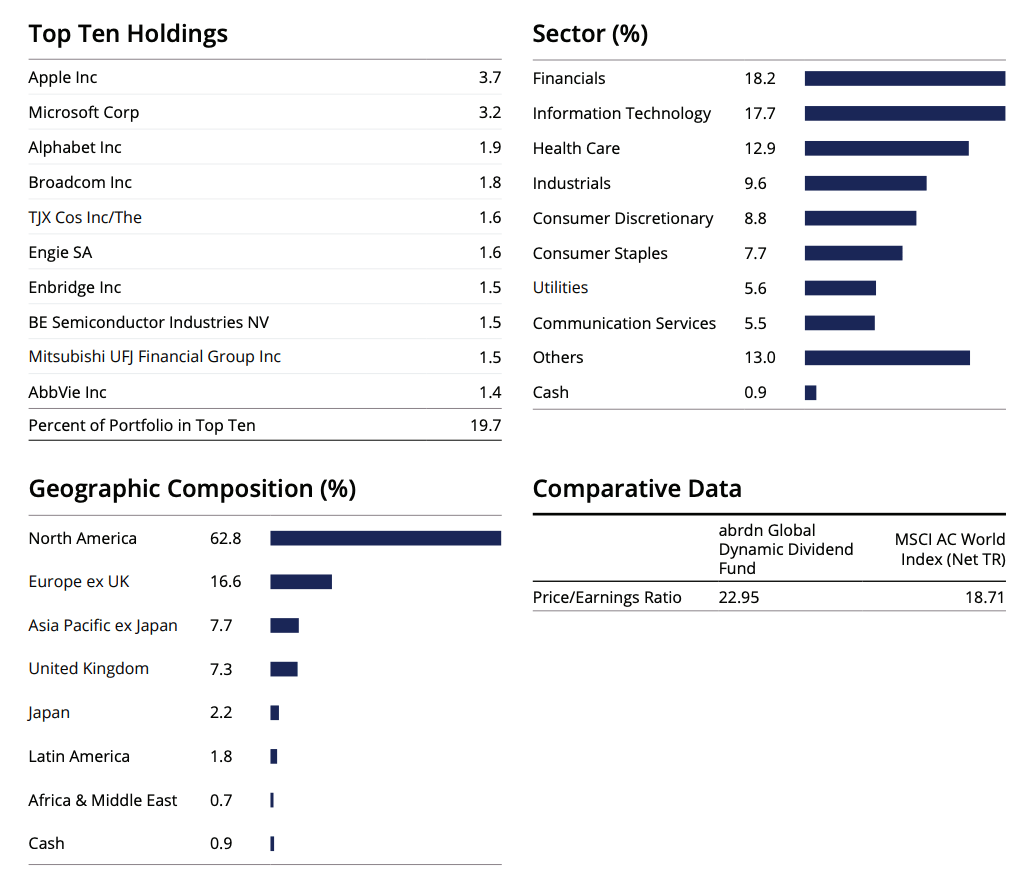

As shown by the table below, as of September 30, 2023, AGD is well diversified with its largest holding being Apple ( AAPL ) which accounts for 3.7% of the fund. Comparably, AAPL accounts for 4.7% of ACWI.

AGD's top 10 holdings account for 19.7% of the fund. Comparably, the top 10 holdings of ACWI account for 18.9% of that fund.

One thing to highlight is that AGD's top holdings are not particularly high yielding companies as one might expect due to AGD's fund name. AAPL pays a dividend of just 0.50%, Microsoft pays a dividend of just 0.79%, and Alphabet currently does not pay a dividend.

On a portfolio basis, AGD's portfolio has a weighted average dividend yield of 3.42%. Comparably, ACWI has a yield of 1.81%. Thus, despite the fact that top holdings are not high yielders the fund as a whole does have a bias towards higher yielding stocks.

In terms of sector exposure, AGD is generally similar to ACWI. AGD's most significant underweight is to technology (17.7% compared to 22.9% for ACWI.) AGD is modestly overweight financials (18.2% vs 15.6% for ACWI) and Utilities (5.6% vs 2.6% for ACWI.)

In terms of geographic exposure, AGD is fairly similar to ACWI. U.S. exposure accounts for 62.8% of AGD compared to 62.4% for ACWI. One significant country overweight for AGD is the U.K. which accounts for 7.3% for AGD vs 3.6% for ACWI. This overweight is offset in part by an underweight to Japan (2.2% compared to 5.4% for ACWI).

{kind=link}

Forward-Looking Outlook

I believe AGD will continue to underperform lower cost global equity ETFs such as ACWI and VT going forward over the long-term. However, I believe the degree of underperformance will be moderate considering the fact that AGD is invested similarly to index products such as ACWI in terms of geographic and industry exposure. Thus, assuming AGD maintains similar exposures going forward, a significant portion of divergence vs ACWI will be due to stock selection.

AGD charges a very high expense ratio of 1.16%. This fee is a major headwind which AGD must overcome just to match a low cost ETF such as VT or ACWI.

While AGD currently trades at a significant discount to NAV on an absolute basis, the current discount is close to the fund's historical average discount over the past 10 years. Moreover, closed-end funds are generally trading at above average discounts to NAV right now. For these reasons, I do not believe AGD's discount to NAV is poised to narrow in the near-term.

Conclusion

AGD has failed to deliver strong risk adjusted results historically compared to lower fee index products such as ACWI.

AGD currently trades at a significant discount to NAV but there is no immediate catalyst to suggest this will narrow anytime soon. Additionally, AGD's discount to NAV is only modestly higher than its historical average over the past 10 years.

While AGD clearly has a bias towards higher yielding stocks, its geographic and industry exposures are broadly inline to capitalization weighted index products such as ACWI. For this reason, assuming exposures remain somewhat similar going forward, AGD's relative performance will be driven by single stock selection.

AGD carries a very high expense ratio of 1.16% which will be difficult to overcome. Additionally, AGD operates in a market category which has proved very difficult for active managers historically suggesting the market is fairly efficient.

For these reasons, I rate AGD a sell and believe investors looking for global equity exposure should favor low cost index funds such as ACWI or VT.

For further details see:

AGD: A High Fee Closed-End Fund To Avoid