AGESF - ageas: A Buy For Its 8% Dividend Yield

2023-06-27 02:36:26 ET

Summary

- ageas is a Belgium-based insurance company with a high-dividend yield, making it a good income play in the European insurance sector.

- The company has a strong presence in Belgium, the UK, and Portugal, and is committed to growing its operations in emerging markets like Asia.

- ageas' dividend yield is considered sustainable, with prospects of becoming even higher in the coming years.

ageas SA/NV (AGESY), (AGESF) offers a high-dividend yield that is well covered by its own cash flow generation, making it a good income play in the European insurance sector.

Company Overview

ageas is an insurance company based in Belgium, being one of the largest European insurance companies based on about 45 million customers across several markets. Its current market value is about $7.5 billion and trades in the U.S. on the over-the-counter market.

Its operations are focused on both the Life and Non-Life segments, serving individual customers and small and medium enterprises throughout several distribution channels.

Geographically, ageas has a strong presence in its domestic market, where it owns 75% of AG Insurance, the Belgian insurance market leader, while the remaining is owned by BNP Paribas ( BNPZY ) insurance unit. Due to this partnership, the bank's retail network the main distribution channel for AG Insurance in Belgium. Beyond its domestic market, ageas also has strong positions in the U.K. and Portugal, while in other European countries it has smaller operations, such as in Turkey.

In Asia, where it has better growth prospects over the long term, ageas does not control its operations, being its activities organized through joint-ventures with local banking partners across several countries, including China, Malaysia, Thailand, India, beyond others.

Despite this diversified footprint, ageas' revenues are quite concentrated, with its domestic market generating about 65% of total premiums, while only about 5% are generated in Asia. Nevertheless, ageas seems committed to grow its operations in emerging markets, given that over the past three years it has made several acquisitions in China, Turkey, and India, thus the weight of international markets is expected to gradually increase within the group over the coming years.

Moreover, while the weight in the top-line is not great, Asia's contribution to the bottom-line is higher because ageas has non-controlling stakes in joint-ventures, thus its profits are accounted under the equity method while its premiums aren't consolidated. Due to this accounting treatment, Asia's weight on profits was nearly 25% over the past year, which is already a significant contribution to overall group profits, and due to better growth prospects over the long term, this region is likely to increase its contribution to profits over the next few years.

Indeed, ageas' strategic plan presented in 2021, is focused on strengthening its leadership position in existing markets, plus it also considers mergers and acquisitions to fuel its growth. Most recently, this has been performed in emerging markets, but the company does not rule out adding a new geography to complement its existing three 'core' markets (Belgium, U.K., and Portugal), even though ageas has not made a significant transaction so far to add another geography.

Regarding it main financial targets, the company aims to achieve earnings growth of 5-7% annually between 2021-24, maintain a solvency ratio of at least 175%, and distribute more than half of annual earnings to shareholders.

Financial targets (ageas)

Financial Overview

Regarding its financial performance, reflecting ageas' high exposure to mature markets, its top-line has been relatively stable between €8-9 billion annually over the past few years, while its net profit has been around €1 billion in recent years.

However, on an annual basis its results have some volatility, for instance the company's performance was negatively affected by the pandemic in 2020 especially in its non-life segment, which led to a significant drop in earnings. More recently, its performance has recovered, plus rising interest rates in Europe has also been a recent boost to its investment income and profits.

In 2022 , ageas' net result was slightly above €1 billion, an increase of 21% YoY, supported by a strong operating performance across all regions. Inflows during the year were quite strong, especially in Asia, where new business sales increased compared to the previous year.

Its life segment remained the largest one on total profits, accounting for more than 63%, even though earnings in this segment declined compared to the previous year due to higher volatility on the capital markets, which affected business margins in unit-linked products. In non-life, adverse weather in the U.K. was also negative for the company's combined ratio (96.5% in 2022 vs. 95.4% in the previous year), impacting negatively this segment earnings.

Despite some headwinds, the group's overall profit increased due to liability management related to legacy issues following the global financial crisis, namely the RPN mechanism that is related to hybrid instruments received by BNP Paribas Fortis and impact ageas' net income. While in 2021 the impact was negative in its accounts, over the past year the net effect was positive and the main driver of earnings growth in the year. This shows that ageas' operational performance was not impressive last year, and the RPN revaluation can have a significant impact on its bottom-line, which is not a desirable outcome.

RPN effect (ageas)

Nevertheless, its free cash flow generation was quite good given that its cash remittances from operational subsidiaries amounted to nearly €900 million, more than enough to cover holding costs of €200 million. Thus, its holding free cash flow was about €700 million in the year, which is the company's 'free' cash to perform share buybacks and distribute dividends. Investors should note that, like some European companies, ageas only reports annual and semi-annual earnings, thus the next update will be presented at the end of August, related to the first semester of 2023.

At the end of 2022, its solvency ratio, a key measure of balance sheet strength in the insurance sector, was 218% (vs. 197% in 2021). This ratio is well above the company's internal target of at least 175%, which means it has an excess capital position, and can distribute a large part of its annual earnings to shareholders.

Given this background, ageas has distributed some €700 million in dividends related to its 2022 earnings, through two dividend payments of €1.50 per share. This means its total dividend was €3 per share, an increase of 9.1% YoY, which at its current share price leads to a dividend yield of more than 8%.

A high-dividend yield can usually be a sign of some questionable dividend sustainability, but as I've analyzed previously the company's 'free' cash flow was also about €700 million in 2022, thus its dividend payment is covered by cash generation and can therefore be considered sustainable.

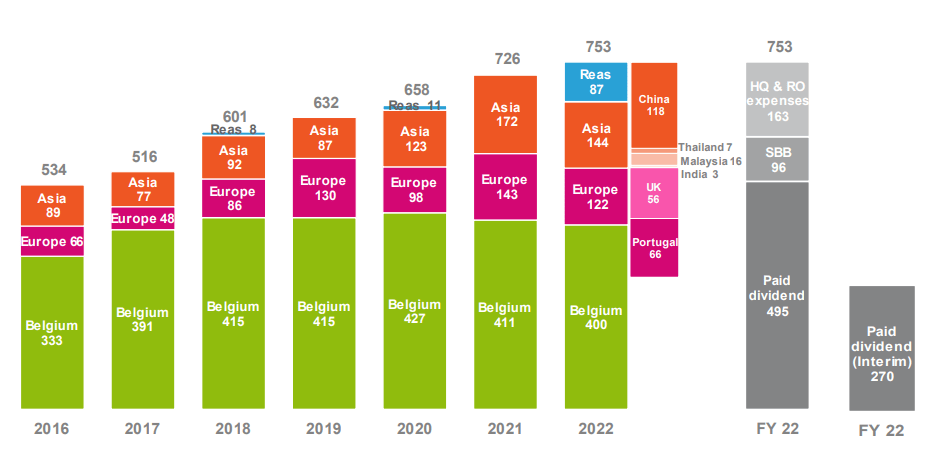

Moreover, ageas' cash generation has consistently increased over the past few years, as shown in the next graph, thus its management decision to increase the annual dividend is supported by the company's fundamentals, boding well for future dividend growth.

{kind=link}

Indeed, according to analysts' estimates , its dividend per share should maintain a growing trend over the next few years, increase to €3.60 per share by 2025, thus ageas offers a good combination of yield and growth for income investors.

Conclusion

The insurance sector is a mature one, but ageas' business profile is more attractive than compared to many European peers due to its exposure to Asia. Nonetheless, its investment case is highly geared to its high and sustainable dividend yield, which also has good prospects of becoming even higher in the coming years.

For further details see:

ageas: A Buy For Its 8% Dividend Yield