AGG - AGG And TLT: Real Yields Near ATH Reveal The Opportunity

2023-09-01 10:34:11 ET

Summary

- Long-duration bonds are great winners after the Fed's pause, based on historical evidence from the latest cycles.

- The outcome is different for soft or hard lending; however, both narratives tend to be bullish for bonds in the very first months after a Fed pause or cycle end.

- Nominal yields had been driven by the increase in real yields as a result of "higher for longer" mantra and the resilient economy, which is probably not so resilient.

- The market sees a higher probability of a Fed pause than a hike, which does not change the strategy.

- Fed Funds Rate > Core inflation. As a result, I see the inflation path on a solid downward track.

I believe there are numerous reasons to own long-term US Treasury bonds such as ( TLT ) and ( AGG ). While I will concentrate primarily on these three: Firstly, historical evidence is fairly plain and provides a straightforward perspective on what will occur with bonds following a Fed pause. I am persuaded that we are near or possibly behind peak rates. In this regard, I share the market's my perspective. Second, the real yield is eminently close to long-term astronomically high levels not seen in more than 10-15 years, thereby constituting an absolute catalyst for robust long-term opportunity. Thirdly, the Effective Fed Funds Rate is higher than core inflation in the United States, while inflation is declining sharply. When FFR > inflation, it is sufficiently restrictive to reach the inflation target. I am confident that inflation will continue to return to the target level, also as a result of the base effect, based on the numerous leading indicators that I have been suggesting in recent months. However, the greatest hazard is almost uncontrollable fiscal spending combined with QT. There must be fresh purchasers. On the basis of the current attractive position, I believe there will be purchasers, so I consider these rates to be very attractive.

Real yields are primary driver of nominal yields

There are several crucial reasons why I chose the AGG and TLT for further analysis. As you can see in the table below, these are predominantly long-term bonds whose real yields have settled near their highest levels in the past 10 to 15 years, indicating my attraction to such a selection. AGG has a weighted average maturity of 8.52 years, an effective duration of 6.13 years, and a positive convexity of 0.65, according to iShares .

Due to the extremely long duration of TLT, every rate increase would be especially vulnerable. In spite of the fact that the weighted average yield to maturity is 25.21 years, the effective duration is 16.89 years and the convexity is positive at 3.8. Due to the positive convexity, a further increase in interest rates would be less painful than gains, providing the advantage to the long position based on a risk-reward approach.

While I was once bullish on TLT (down -7% from the previous analysis, based on total return), I must confess that I was a little bit premature, despite being correct about inflation. However, the narrative of being long TLT was too speculative because I did not believe the Fed could raise as much as it did at the time. However, that is precisely what transpired, but we will investigate the most significant contributors to nominal yield to identify potential opportunities.

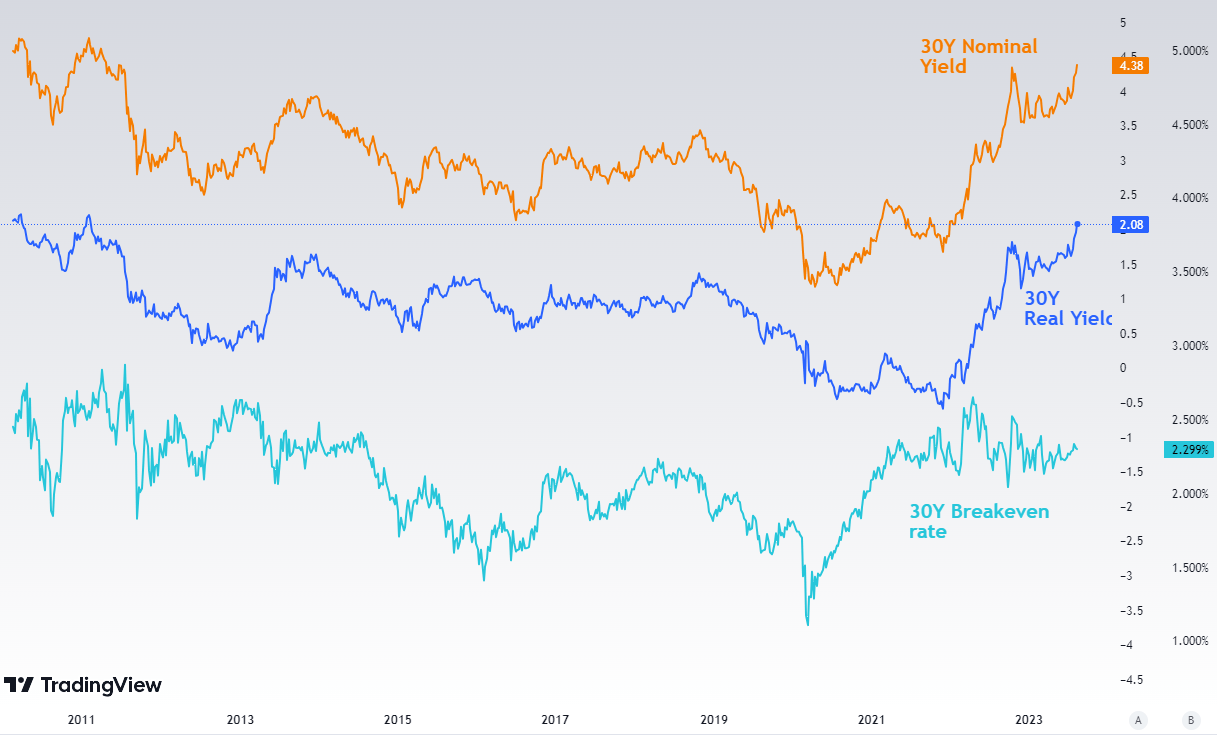

You can see the contribution of nominal US30Y below, as well as the 30Y TIPS yield (real yield) and 30Y breakeven rates (market expectations for the annualized inflation rate for 30 years). As can be seen, real yields were the driving force in recent months, while inflation expectations remained relatively stable. Real yields are nearly at all-time highs, reflecting the greatest investment opportunity in years. Inflation expectations for 30 years are approximately 2.29 percent, which is above the long-term inflation target of about 2 percent.

The comparison of 30Y yield, real yield and breakeven (Lucid Vision via Tradingview.)

{kind=link}

Considering 20-year and 10-year real yields, it appears that we are close to 2008 and 2009 levels. Currently, rates are pricing the "higher for longer" theme. Nevertheless, the Mr. market is always subject to change, as real yields have been extremely volatile. Despite the risks involved, I believe it presents a wonderful opportunity from this perspective.

Resilient economy or not

Taking into account the upcoming round of inflationary pressures, the Fed may decide to raise rates again. Here are the possible drivers:

- "Resilient" economy based primarily on the services sector,

- with stronger expenditure and wage pressures,

- tight labour market,

- and the rebound from commodity prices.

Also as a result of these narratives, the Altanta Fed GDP model now predicts that the annualized GDP for the third quarter will increase by 5.8%.

Atlanta Fed GDP model for Q3 (Atlanta Fed)

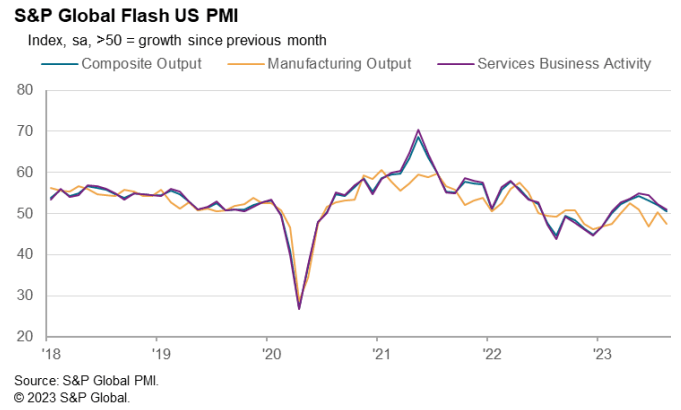

These factors are also responsible for the rapid growth of real yields. The latest flash PMI (S&P) from last week's Wednesday may indicate that the service sector is beginning to be less resilient than anticipated, along with the composite index as a whole. After the release of the data, real yields fell considerably across the curve, with 20-year real yields falling from a local high of 2.04% to 1.88%. Very impressive change in just a few days. However, the overall result differs from the ISM PMI, indicating a much more negative outlook.

{kind=link}

Fed Pause is a massive bullish driver

The charts below from JPMorgan illustrate the most evident behavior of US10Y before and after the Fed Pause. However, it is always an estimate as to when the last rate hike will occur, so we must take into account current market expectations. Although not always accurate and subject to drastic change, it is the most objective indicator of what Mr. Market believes. If not, we could perform our own projections. In the following chapter, we will also examine current market pricing and provide my insights on it.

The graph below depicts the behavior of 10-year US yields following a "Fed pause" during non-recessionary tightening cycles. The majority of dates indicate that long-term yields tend to decline. The exception is cycle Dec 1966.

10y UST before and after the last fed hike: non-recessionary (JPMorgan, X)

When delving deeper, it can be somewhat different when examining the cycles that the recession followed. After a few days of the "Fed pause," yields tended to decline in five of seven cases, but in the majority of cases, yields recovered. On the other hand, due to rising risks and instability, market behavior was fundamental and conventional. Currently, or let's say since 2008, the monetary "normal" is nowhere to be found due to QE and balance sheet expansion. Now, central banks are attempting normalization, but its success will be determined in the future. Assuming a soft landing, the risk-reward profile of owning long-term bonds supports the optimistic narrative.

10y UST before and after the last fed hike: recessionary (JPMorgan, X)

Long-durations bonds are clear beneficent

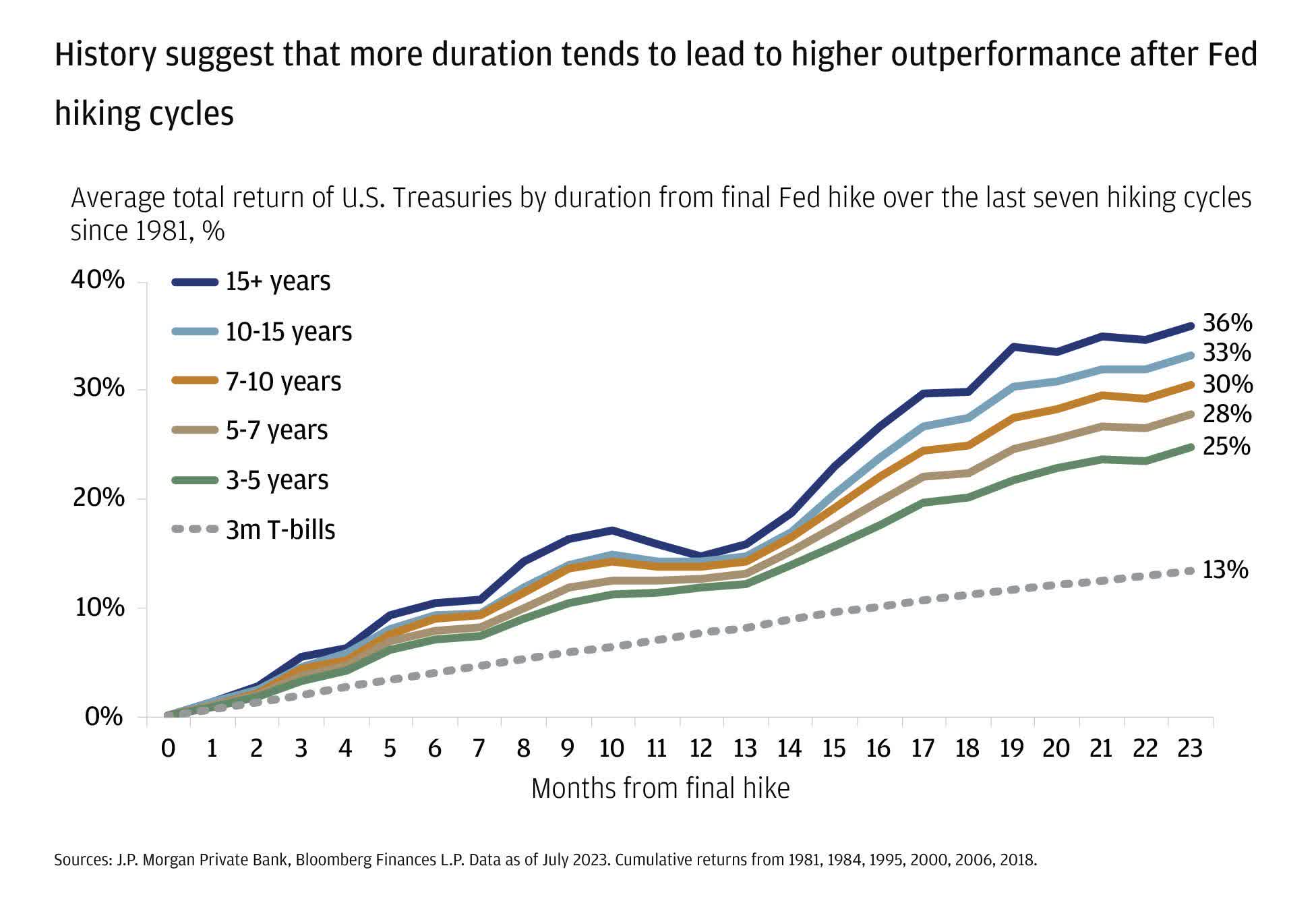

The "average" development of long-duration bonds since 1981 from JPMorgan (via Twitter ) in the last seven cycles indicates that long-duration bonds are clearly advantageous, based on history and the event of the most recent fed hike. In my opinion, we may take one more hike and then be finished, or we may not even see that. According to J.P. Morgan's calculations, a bond with a duration of 15 years or more has an average move in the next 23 months following the last Fed rate increase accumulated a 36% gain. And even short-term bonds performed admirably. TLT and AGG are excellent matches for this.

Avg total return of US treasuries by duration from final Fed hike over the last seven hiking cycles (JPMorgan, X)

{kind=link}

Inflation is cooling

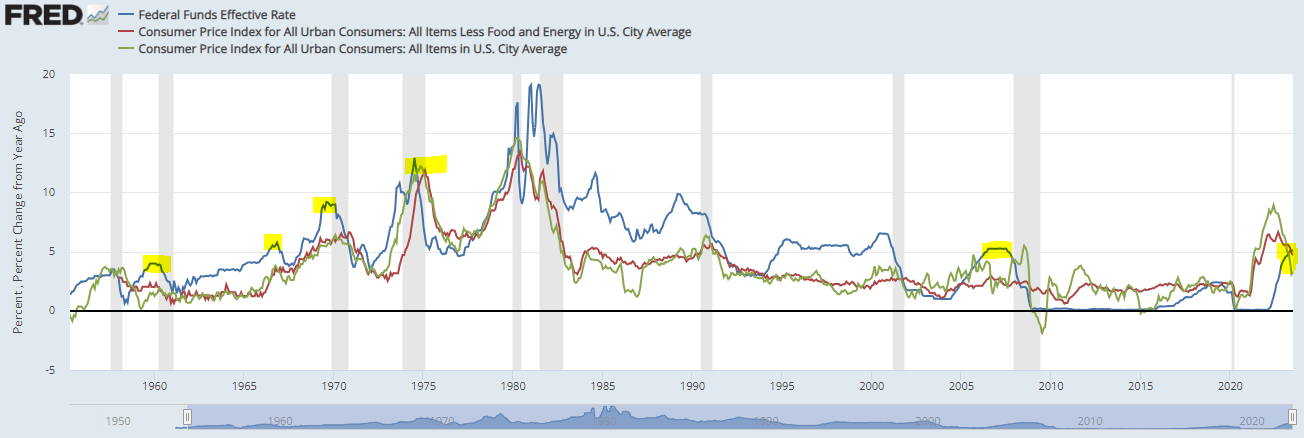

Perhaps you are wondering why I am so confident in my opinion. As FFR is higher than YoY Core Inflation, I believe the Fed has tightened enough. While FFR may be in place for some time, I am confident that it will be sufficient to tame inflation. Most of the time, when FFR exceeded Core inflation, it was sufficient to pacify it. However, it is crucial not to reduce interest rates as quickly as policymakers did in the 1970s.

Fed Funds Rate vs. Core Inflation (FRED)

{kind=link}

These assumptions simply lead me to believe that the Fed is likely finished with rate adjustments. On the other hand, there are risks associated with a robust economy and solid expenditure, or there are leading indicators indicating that services are becoming less resilient and manufacturing is continuing to decline. Inflation is below 0.2% m/m for the second consecutive month, which is below the 10-year monthly average and annualized below 2%, thus below the Fed's inflation objective. Yes, as I mentioned, there are dangers to the upside, but a number of leading indicators point to a greater risk to the downside. Nevertheless, an indicator of economic activity and food suggest inflation could rebound.

Market rates expectations

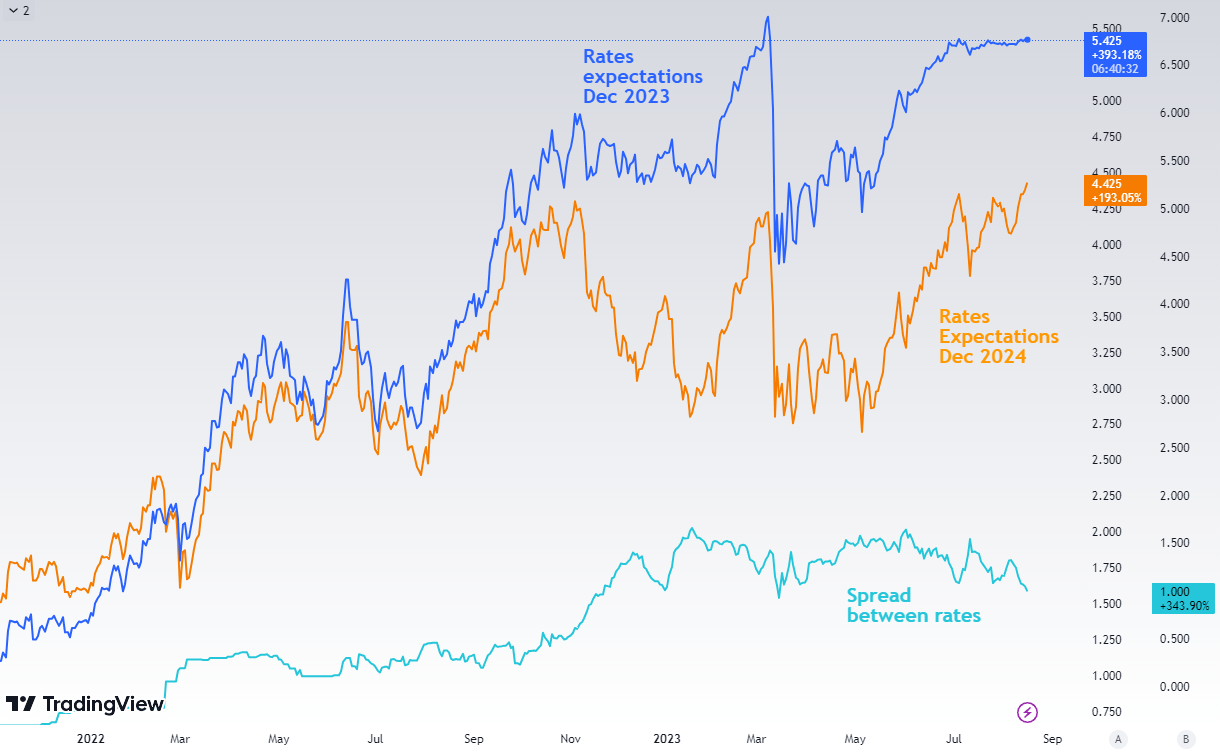

While there are upside inflation risks, which were extensively discussed at the most recent FOMC meeting and Jackson Hole, I prefer to concentrate on market rate measurement by Fed Funds Futures. Simply stated, market participants anticipate rates in December 2023 to be close to 5.43 and in December 2024 to be close to 4.48, implying a probability that the Fed will raise rates by 25 basis points under 40%. The spread between specified futures reflects the market's expectation of a 100 basis point (bps) rate cuts from peak rates through the end of December 2024. Obviously, these expectations alter over time and in response to events, such as last week's Jackson Hole.

FFF rates expectations Dec23, Dec24 (Lucid Vision via Tradingview)

{kind=link}

Nonetheless, if this pattern of rate cuts materializes, it could be a strong positive driver for bonds with maturities of 7 years or more and reduce real yields. Assuming that the fight against inflation could be effective, real yields and inflation expectations could be positive drivers for lowering nominal and real yields. Fed Funds Futures rate expectations imply peak rates in December and November, giving us a slightly less than 40% chance of a 25 basis point rate increase at one of the next two meetings.

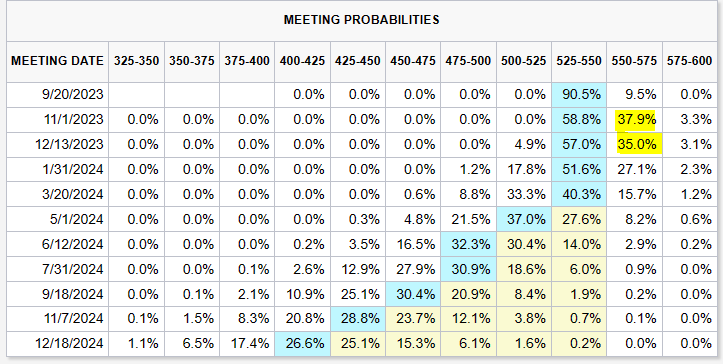

CME Meeting probabilities (CME via Fed Funds Futures)

{kind=link}

Summary and risks

While I have provided clear evidence of how the market behaved in analogous situations, there is no assurance of the market's future behavior. I see limited upside risks in real-yields rising by an additional 30-50 basis points or more (from local yield highs), which could be close to all-time highs. In my opinion, the likelihood of record-breaking real yields is extremely unlikely, though not entirely impossible. However, real yields premiums could spike if enormous fiscal debt issuance and almost out-of-control spending occurred, which could increase inflation expectations and exacerbate the supply-and-demand imbalance.

If demand is insufficient, continued fiscal emissions could lead to an increase in nominal yields if they continue. As a result of the Fed's quantitative easing (QT), it may be more difficult for the market to curb such massive emissions. I believe mitigating factors exist. However, such yields are ideal for asset managers and also attractive for retail investors. Imagine the following long-term yields: 4.24 percent for 10 years, 4.55 percent for 20 years, and 4.33 percent for 30 years. These are the levels that investors and many analysts believed would never be reached again. Levels last seen in 2009. Nonetheless, this threat persists. From a timing perspective I believe, there could be a little bit spark up by 10-20 bps from current yields, which could pull down the AGG and TLT down. This could be solid opportunity.

Jackson Hole - The most important message

Powell attempted to be as hawkish as possible, but the market was not surprised. Fed Chairman confessed that the Fed is prepared for additional tightening if necessary, until it is evident that the inflation target is being met:

We are prepared to raise rates further if appropriate, and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.

There is also a significant comment that must be addressed:

Additional evidence of persistently above-trend growth could put further progress on inflation at risk and could warrant further tightening of monetary policy

Powell has just disclosed that the still-expanding and resilient economy, as indicated by the robust labor market and robust economic expansion, could threaten the efforts of central bankers. Primarily due to the constrained labor market, because, in my opinion, a tight labor market solely creates wage pressures, which drives the price of services. Powell is aware of this inflationary pressure, which is why the FOMC always seeks to soften the labor market, especially in times such as the present.

However, the most recent data from this week - JOLTs Job Openings in the US economy (non-farm) - showed a significant decline, totalling 8.827 million compared to expectations totalling 9.465 million. Nonetheless, the trend remains considerably above pre-pandemic levels, confirming that the labor market remains tight. Nonetheless, it is softening rapidly.

The Fed's decision to halt tightening could be precipitated by a labor market that is easing but remains tight, a manufacturing sector that is continuing to weaken, and a service sector that is starting to weaken. Thus, whether or not we see one more increase is less significant for this strategy than the emergence of global and downside risks.

Regarding the economy's resilience in relation to higher bond yields, I have one suggestion. Despite the fact that the Atlanta Fed GDP model released a very strong piece of forward-looking GDP for Q3, I'm becoming more cautious as the most recent Flash PMI reveals weaker service numbers, following many months of resilience. The monetary policy delayed effect began to materialize.

However, I believe that long-term bonds have an extremely favourable risk-reward ratio, which is influenced by duration and convexity. From a risk perspective, it is much more advantageous to initiate fairly severe DCA at this point. This also correlated with historical evidence, but even historical evidence is never a guarantee of future returns. Before investing, do your own due diligence. Feel free to review my assessment of the technology sector from July, which is ahead of September, the most negative month from a seasonality perspective, or my most recent ideas, lithium producers that are significantly undervalued with excellent growth prospects and with high margin of safety (from my point of view).

For further details see:

AGG And TLT: Real Yields Near ATH Reveal The Opportunity