AGGH - AGGH: A Bond Fund That Comes With Covered Calls And Hedging

2023-08-18 10:25:41 ET

Summary

- Simplify Aggregate Bond PLUS Credit Hedge ETF uses a complex strategy involving bonds, covered calls, protective puts, option spreads, and credit default swaps.

- The fund's performance has been slightly better than its benchmark during the bond bear market, but its protection measures could drag its performance down during a bull market.

- The fund pays monthly dividends with a current annual yield of almost 11% boosted by options selling.

- Some people might find the fund's approach overly complicated while others might prefer its approach.

Simplify Aggregate Bond PLUS Credit Hedge ETF (AGGH) is an interesting fund from Simplify, the same company that runs some well-known funds such as SVOL ( SVOL ) and CTA ( CTA ). This fund uses a combination of holding bonds (more like bond funds), writing covered calls, buying protective puts, option spreads and buying CDX (credit default swaps) as insurance in order to protect from a possible black swan event. While some people will find the fund's approach unnecessarily complicated, others might like it.

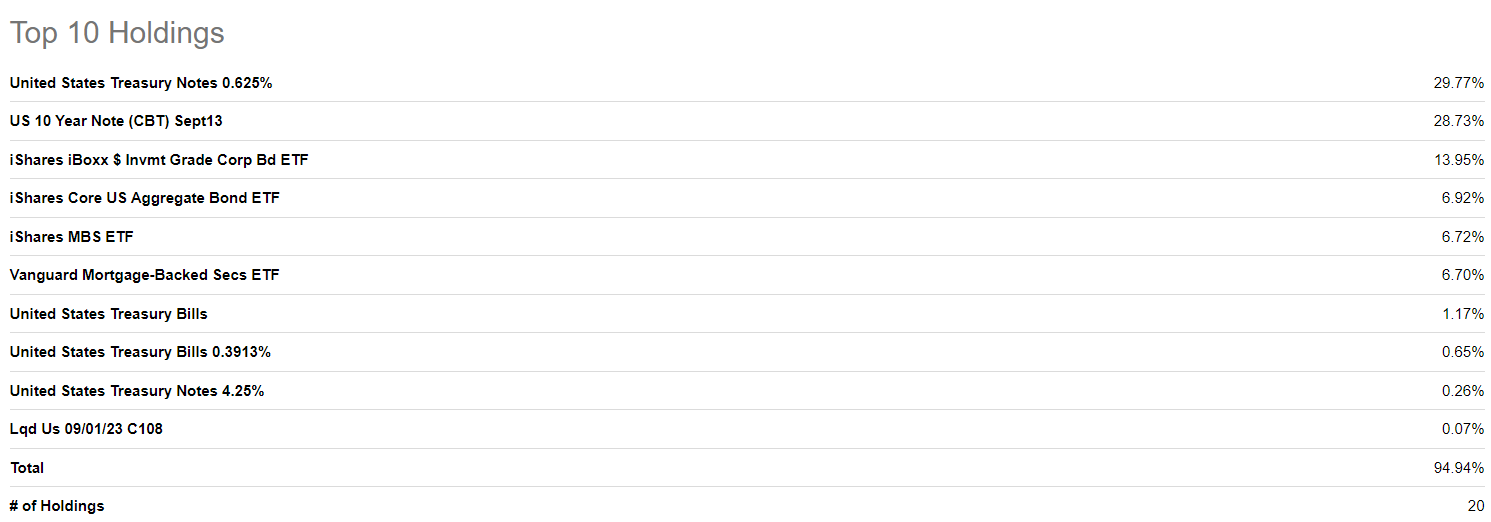

The fund's top holdings include some well-known and highly liquid bond ETFs such as iShares Investment Grade Corporate Bond ETF ( LQD ), iShares High Yield Corporate Bond ETF ( HYG ), iShares 20+ Year Treasury Bond ETF ( TLT ) and iShares Core U.S. Aggregate Bond ETF ( AGG ). The fund has also written some covered calls against each of these positions such as $108 calls for LQD, $99 calls for TLT, $76 calls for HYG and $104 calls for AGG. When I look at the fund's top holdings I don't see credit swap contracts but the fund's prospectus claims that it invests in them as insurance.

{kind=link}

The fund has been around for less than a year and so far its total return is a negative -6%. This looks bad but it's slightly better than the fund's benchmark which is Vanguard Total Bond Market ETF ( BND ). The benchmark was down -9.9% during the same period. Since this fund applies multiple measures to hedge its bond positions, we are not surprised to see that it fell less than its benchmark during a bond bear market but we would have expected a better protection than a mere 3% from a fund that's applying different kinds of hedges.

We can also expect this fund to underperform when bonds are in a bull market because of the drag from all those hedges it has in place. The fund's management says that these hedges are in place to protect investors not necessarily from a bear market in bonds but an actual credit event like what we saw in 2008 but I don't know if I agree with this 100% because the fund doesn't hold individual bonds. It holds a basket of bond ETFs each of which hold hundreds of bonds so the fund shouldn't suffer too much if there is a credit event unless it's something extremely drastic like the US government defaulting on its debt.

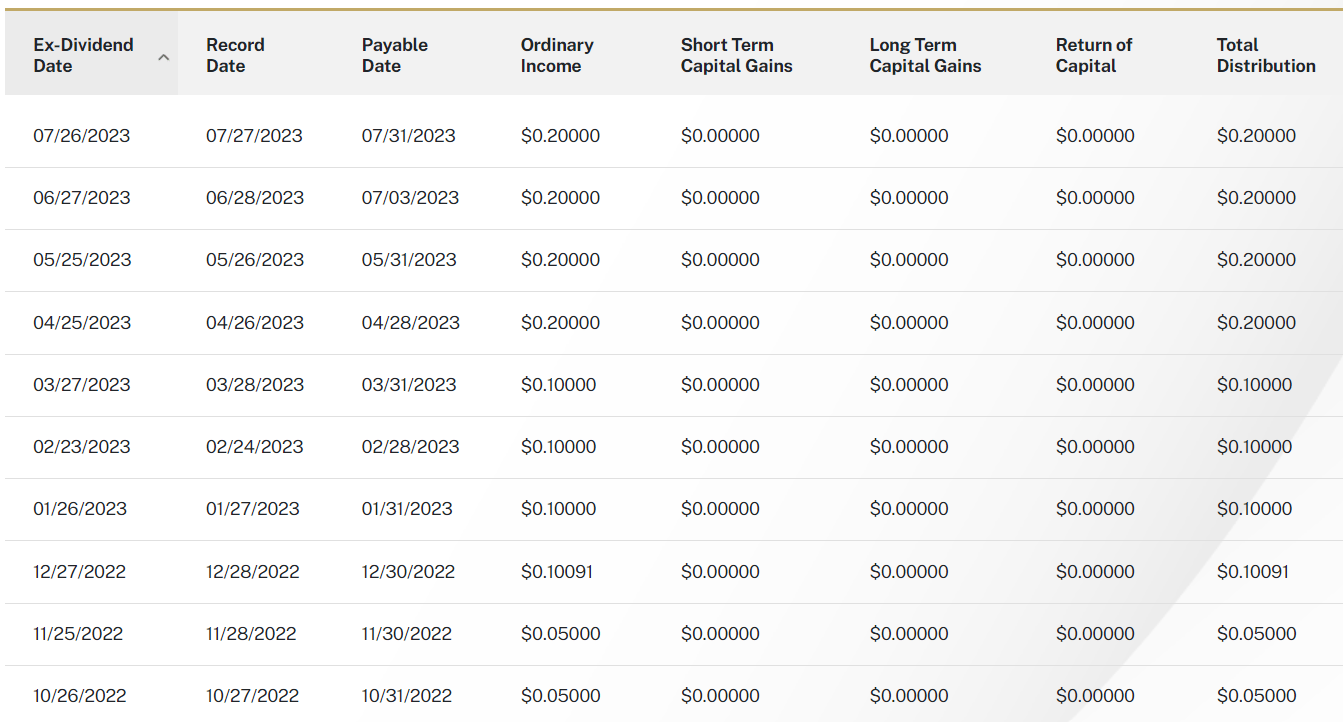

The fund pays monthly dividends. It was originally paying about 5 cents per month but raised it to 10 cents in December and further raised it to 20 cents in April. So far all distributions are marked as "ordinary income" which means it doesn't have the same tax benefits one would see from qualified dividends or long term capital gains not to mention return of capital which doesn't get taxed. Ordinary dividends are taxed at the same rate as one's income bracket which means someone with high income might end up in a disadvantage.

{kind=link}

The current rate of monthly distributions of 20 cents translates into an annual rate of $2.40 which gives us an annual yield of almost 11% considering that the current share price (at the time of writing this article) is $22. Most of the fund's holdings don't pay a yield anywhere near that though. For example TLT yields 3.3%, HYG yields 5.8%, AGG yields 3.0% and LQD yields 3.9%. The rest of the yield will come from fund's covered call sales which are often a few percentage points out of money.

This fund's approach of selling covered calls on bond funds reminds me of similar funds such as TLTW ( TLTW ) which writes covered calls on TLT, HYGW ( HYGW ) which writes covered calls on HYG and LQDW ( LQDW ) which writes covered calls on LQDW. Typically these funds write calls very close to the money and they don't use any kind of special hedging. Since all these funds are also new, we don't have long term performance comparisons but below is a comparison of how each of these funds performed this year so far. We see that HYGW performed the best with being up almost 6% year to date followed by LQDW which was up 4% in total returns. AGGH came behind these funds with 3% total return so far. Perhaps its performance was dragged down by its complicated hedges.

Bond markets have been in a bear market since the beginning of 2022. Even the safest bonds that are seen as virtually risk-free such as US government bonds or government backed mortgage securities are down significantly because risk-free doesn't mean bond's value can't drop. Risk-free simply means that it is extremely unlikely that the bond will have a default event but as investors found out last year and this year, bond prices can still fluctuate wildly and they can still post large unrealized losses. Some regional banks (and mortgage REITs) even found out that overleveraging on "risk-free" bonds makes them not so risk-free anymore.

We don't know how long this bear market of bonds will last. Bond market is still trying to figure out what inflation rate will be in the next couple years and how to price it accordingly. Bond markets are also trying to figure out what the Fed will do with short term rates moving forward and there seems to be a lot of uncertainty in the system even though the Fed has been very clear, open and consistent in its messaging all years. The Fed will not cut rates until inflation comes down to levels below 2% in a sustainable fashion and stays there for a while. Still, markets try to price in different scenarios and different what ifs which gives us the volatility in bond markets.

Having said that, bond markets aren't likely to be stuck in a bear market forever. We can see bonds stabilizing later in the year when inflation numbers come in and market participants finally start digesting what the Fed has been communicating for over a year. If investors are looking for income from a basket of bond ETFs boosted by covered calls and hedged with different vehicles this can be the fund for you. Some people might find this fund's approach to be unnecessarily complicated though and I wouldn't argue with them very hard either.

For further details see:

AGGH: A Bond Fund That Comes With Covered Calls And Hedging