AGL - agilon health: High Growth But Unsustainable Economics

2023-11-20 09:18:54 ET

Summary

- agilon health's full-year outlook caused its stock to fall sharply, raising concerns about the sustainability of its business model.

- While the company reported a 71% increase in revenue and a rise in Medicare Advantage membership, its gross profit growth doesn't hold up.

- A $5 billion market cap appears too high, considering agilon's low medical margins.

agilon health ( AGL ), a health care company focused on empowering physicians to transform health in communities, recently hit a 52-week low after lowering its full-year outlook during its Q3 earnings report. agilon health is a partner for physicians, offering a platform that enables them to provide care to patients. The company operates in the healthcare industry, specifically focusing on the Medicare Advantage and ACO REACH populations. agilon health aims to improve patient outcomes by strengthening its physician network and leveraging its platform capabilities.

The company strategically builds and strengthens its physician network, fostering a network effect. While the company's growth appears strong on the surface, agilon's missing profitability and low medical margins, spark concerns about the sustainability of its business model.

Earnings Snapshot

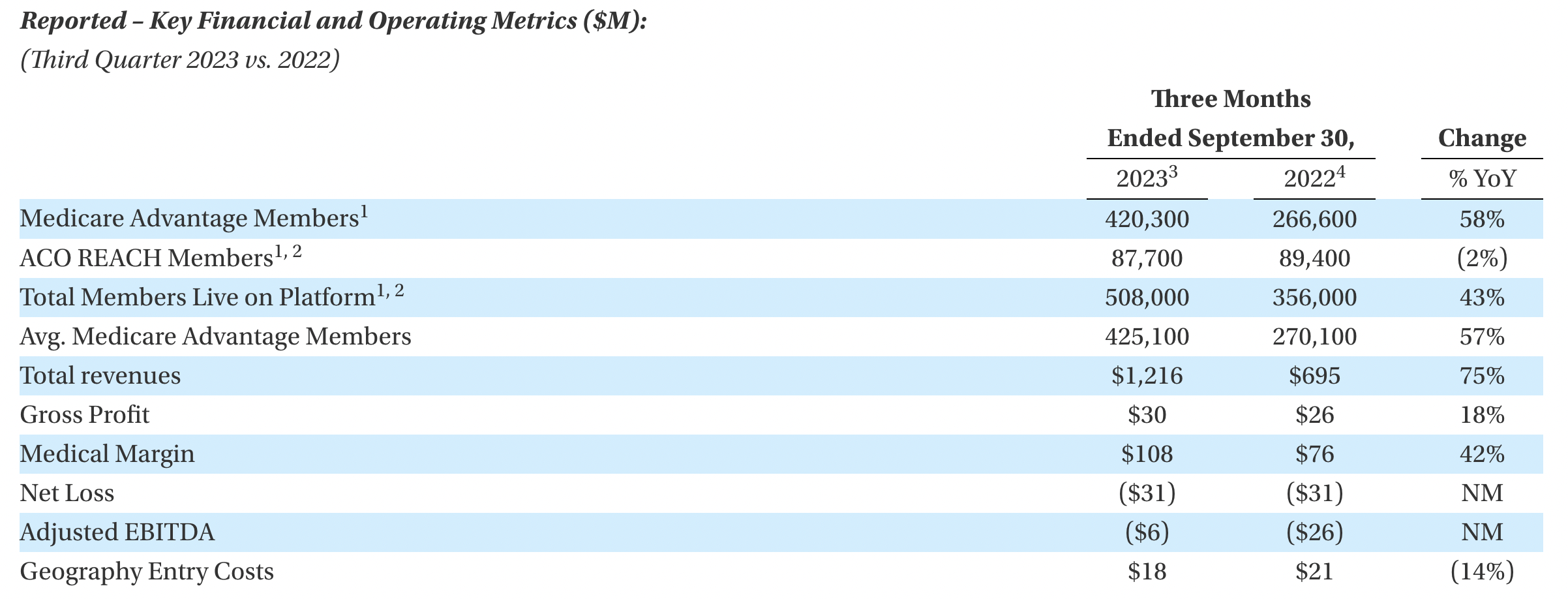

agilon health reported a 71% increase in revenue to $1.15 billion and a 57% rise in Medicare Advantage membership to 408,900, with total members on the agilon platform reaching 495,900. While its reported revenues exceeded expectations, agilon missed EPS estimates by 2 cents, coming in at -$0.08. This represents a net loss of $31 million in the third quarter 2023, compared to a net loss of $31 million in third quarter 2022.

{kind=link}

agilon health

Although, revenues increased by 75% year-over-year (YoY) in the quarter, its gross profit increased by only $4 million, or 15%, while its medical margin increased by $108 million, or 42% during the third quarter 2023. Ideally, these figures should increase relatively faster than its revenue growth, otherwise, the company isn't scaling effectively and will grow unprofitable revenue. Its total gross profit represents a mere 2.4% margin, much lower than the 3.7% gross profit margin reported in Q3 2022.

The company saw a significant improvement in adjusted EBITDA of only negative $6 million in the third quarter 2023, compared to a loss of $26 million last year. This may be interpreted positively and could demonstrate some signs of effective scaling after all, yet its adjusted EBITDA improvement is a result of various favorable factors during the quarter. Here, geography entry costs included $18 million, compared to $21 million in the third quarter 2022. While this only accounts for $3 million, adjusted EBITDA of -$9 million makes it seem as if agilon is further away from breaking even on an adjusted basis than the earnings suggest.

{kind=link}

agilon health

More important, however, is the fact that its ACO REACH segment contributed $18 million to Adjusted EBITDA during the third quarter 2023, compared to a $3 million loss in the third quarter 2022. ACO REACH (Accountable Care Organization - Rapid Evaluation and Adoption for Chronic Care) in healthcare refers to a program or initiative aimed at enhancing the delivery of chronic care services within the framework of an Accountable Care Organization. It focuses on rapidly evaluating and adopting strategies to improve the management of chronic conditions, ultimately aiming for better patient outcomes and cost-effectiveness. During the quarter, ACO REACH Members declined by 1.7 million, or 2%. If ACO is agilon's main profit driver, declining memberships in the segment is a warning sign, in my opinion, and leaves little room for further EBITDA contribution in the future.

{kind=link}

agilon health

agilon health also increased its full-year cost guidance by $90 million, representing lower medical claim margins for the rest of the year. Earlier this year, Healthcare giants reported rising costs due to an increase in surgeries among older adults. While insurers have been profiting from postponed non-urgent surgeries amid the COVID-19 pandemic and staffing shortages at hospitals, remarks from UnitedHealth ( UNH ) indicate that these advantages may be diminishing. Since larger healthcare and Medicare providers may have a lower medical loss ratio due to their significant scale, agilon's losses may further increase.

Valuation

agilon took advantage of a hot IPO market in 2021, driven by high valuations as a result of significant quantitative easing during the pandemic. The company went public at a valuation of over $11 billion and closed at nearly $30 per share. At a revenue run rate of just over $2 billion, this translated into a Price-to-sales ratio of over 5 times. Since then, shares have dropped nearly 60% and its valuation contracted significantly. Nevertheless, I believe its valuation is still way too high, considering its low-profit margins. Here, agilon holds just 4% gross profit margins, translating into over 29,4 Price to Gross Profit. A smaller competitor, Oscar Health ( OSCR ) generates more gross profit on an annual basis, and grows at a similar pace, yet has just 1/3 of agilon's market cap. Either way, Oscar is also deeply unprofitable and demonstrates no sustainable unit economics.

| Company |

| Price to Sales (P/S) |

| Gross Profit Margin |

| Price to Gross Profit ((TTM)) |

| agilon health ((AGL)) |

| 1.1 |

| 4% |

| 29.4 |

| Oscar Health ((OSCR)) |

| 0.32 |

| 19% |

| 1.7 |

| UnitedHealth ((UNH)) |

| 1.35 |

| 25% |

| 5.6 |

| Molina Healthcare ( MOH ) |

| 0.64 |

| 18% |

| 5.2 |

| Elevance Health ( ELV ) |

| 0.63 |

| 27% |

| 3.7 |

| Humana ( HUM ) |

| 0.6 |

| 18% |

| 3.4 |

| Cigna ( CI ) |

| 0.43 |

| 13% |

| 3.4 |

| Centene ( CNC ) |

| 0.26 |

| 16% |

| 2.3 |

| CVS Health ( CVS ) |

| 0.25 |

| 15% |

| 0.65 |

While one may argue that the large-cap healthcare giants listed above are no suitable comps, based on their larger scale and more mature business, it is crucial to note that large healthcare players such as Molina Healthcare ((MOH)) have been consistently profitable even at a comparable scale. Furthermore, healthcare providers may see a tougher future ahead, as the Biden administration is proposing cuts to Medicare Advantage. Private insurers receive a payment from the federal government for delivering Medicare-covered services to enrollees, determined by a statutory formula overseen by Centers for Medicare and Medicaid Services ((CMS)) related to Medicare Advantage ((CMS)). Recently, CMS finalized a rule altering the process of Medicare Advantage risk adjustment data validation (RADV) audits and issued the annual notice proposing changes to Medicare Advantage plan payments for the upcoming year. Such regulatory changes could drive down profit margins of the entire industry and make it even more difficult for smaller Medicare start-ups like agilon to reach scale.

Takeaways

agilon's member base expansion hasn't translated into a clear path toward profitability. Its revenue growth outpaces gross profit growth, relying heavily on leftover IPO funds for liquidity, making its balance sheet look sound on the surface. Established providers' insurer ties make it tough for startups to compete on reimbursement rates. Past attempts by healthcare startups like GoHealth ( GOCO ), SelectQuote ( SLQT ), and Clover Health ( CLOV ) ended in failure, and agilon might face a similar fate. Thus, short sellers like Citron Research may be right.

For further details see:

agilon health: High Growth But Unsustainable Economics