AGL - agilon health: Improved Member Growth And Economies of Scale May Imply Undervaluation

2023-09-13 23:31:44 ET

Summary

- agilon health expects positive adjusted EBITDA in 2023 and is experiencing double-digit net sales growth.

- The company's growth is driven by an increase in the number of members and partnerships with local physicians.

- Economies of scale, marketing efforts, and potential M&A could lead to significant free cash flow generation.

agilon health ( AGL ) is delivering double digit net sales growth driven by increases in the number of members, and also expects positive adjusted EBITDA in 2023. I think that economies of scale, further investment in marketing to add new members, and M&A efforts could result in significant FCF generation. Even considering failed predictions from management, failed M&A, or lower member growth than expected, I believe that the company is trading a bit undervalued.

agilon health: The Company May Deliver Positive EBITDA In 2023

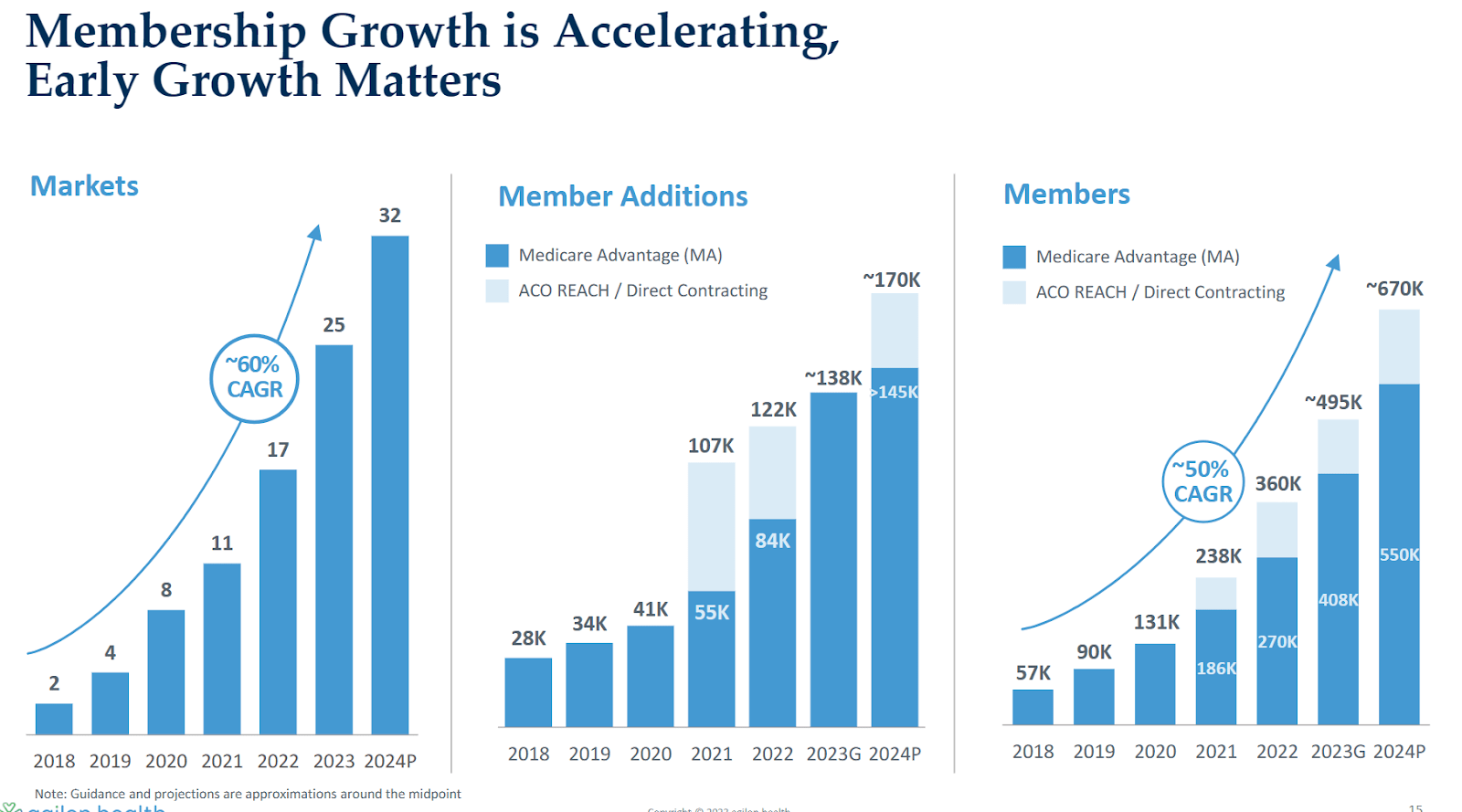

Since its founding in 2016 and its inaugural partnership in 2017 with an anchor physician group, the company has experienced rapid growth in local communities. In a period of five years, it has managed to expand to 32 different geographies and 14 states.

Source: Investor Presentation

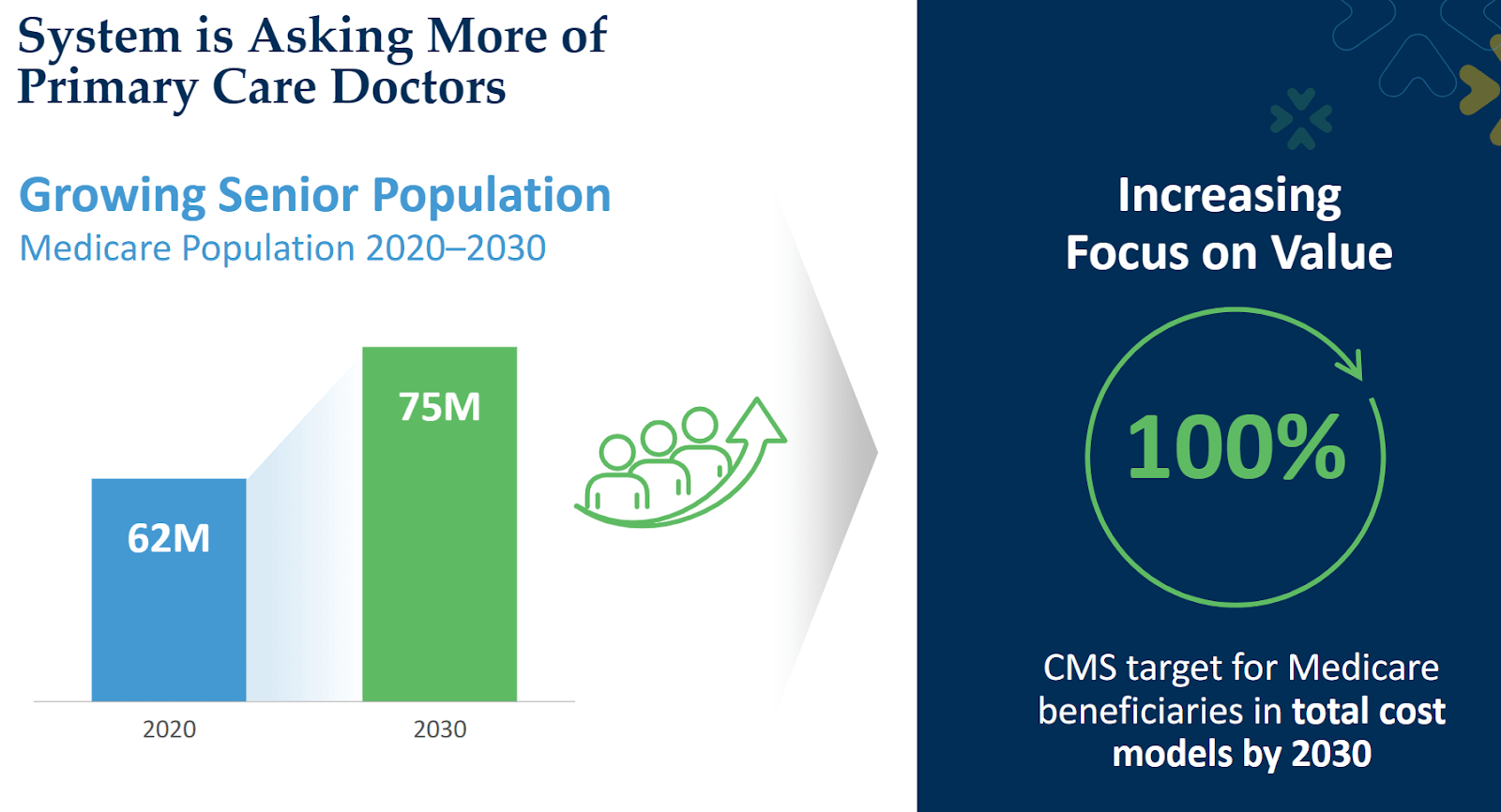

In my view, the growing senior population and the facilities given to the independent local physicians are the main assets of agilon. Thanks to its platform, from the end of 2021 to the end of 2022, total membership increased by 45%, and revenue increased by 48%.

{kind=link}

As of December 31, 2022, PCPs on their platform provide care to approximately 269,500 members of Medicare Advantage and 89,000 Medicare Fee-for-Service beneficiaries through eight direct contracting entities in their participation in the CMS Innovation Center Direct Contracting Model. In the last presentation given to investors’ member additions, market growth was expected to grow at the double digit.

{kind=link}

With that about the previous and expected growth, management also reported its expectations for the year 2023. I believe that the most appealing is that agilon, for the first time, could be delivering positive Adjusted EBITDA in 2023 after positive quarterly Adjusted EBITDA delivered for the quarter ended June 30, 2023.

Source: Investor Presentation

Expectations From Other Analysts

Other analysts expressed impressive expectations for the future. 2025 Net sales is expected to be close to $7.853 billion, with net sales growth of about 28%, 2025 EBITDA of $276 million, net margin of 21%, and 2025 free cash flow of close to $135 million. I used some of these figures in my cash flow models, so I believe that investors may want to have a look at them.

Source: Market Screener

Balance Sheet And Contractual Obligations

As of June 30, 2023, agilon health reported cash worth $190 million, restricted cash and equivalents of about $10 million, and marketable securities close to $389 million. The total amount of cash is quite impressive. The net debt is in fact negative. It means that agilon may have a significant amount of liquidity to finance future marketing developments as well as to hire new personnel.

The company also reported receivables of about $1.417 billion, 184% more than that in 2022, with prepaid expenses and other current assets of $37 million, 10% more than that in 2022. Total current assets stood at $2.044 million, and the current ratio is larger than 1x. Besides, with property and equipment of $24 million, total assets were equal to $2.352 billion. The asset/liability ratio is larger than 1x. In sum, I believe that the balance sheet stands in a good place.

Source: 10-Q

The list of liabilities does not seem worrying at all. Medical claims and related payables stood at $1.099 billion, with accounts payable and accrued expenses close to $257 million. It means that doctors seem to be financing the activities of agilon health. The company does not seem to need a significant amount of debt to operate. Total liabilities were equal to $1.473 billion.

Source: 10-Q

In February 2021, the company agreed to a credit facility that included a $100 million secured term loan and a $100 million secured revolving credit facility. These funds were used to refinance outstanding debt and general corporate purposes.

As of December 31, 2022, the company had $43.8 million outstanding under the term credit facility and $38.8 million available under the revolving credit facility. The credit facilities are guaranteed by subsidiaries of the company, and contain covenants that include financial restrictions and requirements. The weighted average effective interest rate of the term credit facility was 6.04%. I believe that this figure is quite relevant for the investors running DCF models.

{kind=link}

First FCF Catalyst: More Partnerships Will Most Likely Bring Net Sales And FCF Growth

The business model focuses on establishing partnerships with existing medical groups in local communities to provide quality, patient-centered healthcare. Working closely with its physician partners, the company integrates its practices into a common platform and network, sharing best practices and fostering a collaborative approach.

Source: Corporate Website

The marketing team is responsible for developing customized brand strategies for each region, creating communication and educational materials to help patients make informed decisions about their Medicare coverage. The growth strategy is based on a dedicated focus on business development and building a strong network of like-minded physicians. Its approach is based on forming local partnerships and empowering physicians to effectively manage the health and medical needs of their Medicare patients. Under my cash flow, I assumed that further marketing efforts will most likely lead to further net sales growth.

FCF Margin Growth: Platform Support Costs Will Likely Lower, And Economies Of Scale May Lead To Higher FCF Margin Growth

I believe that we may see further improvements in Adjusted EBITDA margin and FCF margin as the number of physician partners increases. As a result, economies of scale may play a major role in reducing the costs per client. In this regard, agilon health made a comment about how platform support costs could lower.

Our platform support costs, which include regionally-based support personnel and other operating costs to support our geographies, are expected to decrease over time as a percentage of revenue as our physician partners add members and our revenue grows. Our operating expenses at the enterprise level include resources and technology to support payor contracting, clinical program development, quality, data management, finance, and legal functions. Source: 10-Q

Acquisitions Like That Of My Personal Health Record Express, Inc. Could Also Accelerate Growth

Considering the current amount of cash in hand, under my DCF model, I assumed future acquisitions. In this regard, it is worth noting that agilon health is ready to acquire smaller competitors. In 2023, the company acquired My Personal Health Record Express, Inc. or mphrX for ~$44 million.

On February 28, 2023, the Company completed the acquisition of My Personal Health Record Express, Inc., a leading provider of value-based care technology and interoperability solutions for cash consideration of $44.4 million, net of cash acquired and subject to certain post-closing adjustments. Source: 10-Q

Cash Flow Expectations

My expectations include net declining sales growth from 2023 to 2033 and a gradual increase in the ratio of net income/ sales from close to 0.4% in 2024 to 5.3% in 2033. 2033 Net sales would stand at $21.237 billion, with a net income of $1.129 billion. The net sales growth revenue used and the net income/sales are, in my view, conservative assumptions.

{kind=link}

The adjustments to reconcile net loss to net cash used in operating activities that I used were pretty much in line with previous figures reported by agilon health. I included 2033 depreciation and amortization close to $10 million, with stock-based compensation expense worth $130 million, but no loss on debt extinguishment, or no losses from equity method investments.

Besides, with changes in operating assets and liabilities including receivables of -$445 million, prepaid expense and other current assets of about -$94 million, and medical claims and related payables worth $464 million, I obtained 2033 CFO of $1471 million, 2033 capex close to -$95 million, and 2033 FCF of $1.377 billion.

Source: Cash Flow Expectations

By adding cash of $190 million, restricted cash of $10 million, and marketable securities of $389 million, and with current debt close to $5 million and long-term debt of $36 million, net debt would be close to -$550 million. With these figures, a WACC ranging from 7% to 12%, and a terminal EV/FCF of 15x-25x, the implied forecast would be around $26 and $56 per share. The IRR would be close to 3.9% and 20%.

With that about my sensitivity analysts, I believe that a conservative valuation of agilon health would be closer to $34-$41 per share, which is way above the current market price.

Source: DCF Model Source: DCF Model

Risks

The company has experienced significant net losses in previous years, and has a significant accumulated deficit. Expenses are expected to increase in the foreseeable future, which could result in further losses as the company invests in business growth, expands the management team, establishes relationships with physician and payer partners, develops new services, and meets requirements of being a public company. These expenses may be higher than anticipated, and difficulties, delays, and other unknown factors could arise that would adversely affect the business. There is a risk of failing to grow revenue sufficiently to offset these expenses, which could impact current and future profitability.

Management may also be making errors in assessing future Adjusted EBITDA growth, and the guidance given may be far from reality. Besides, I made many assumptions in my cash flow models, which may also be failed forecasts. If the company delivers lower net sales than expected or lower FCF margin than expected, I believe that the stock price would decline.

Competition

In the highly competitive and fragmented healthcare industry, the company faces competition in all aspects of its business. Primary competitors include ChenMed, Oak Street Health, Optum and VillageMD, and numerous local provider networks, hospitals, and health systems. Additionally, large, well-funded payers can offer managed services at reduced prices, or expand their relationships with other physicians or physician networks.

Other competitors may offer specialized services, such as data analytics or disease-based programs. Although some competitors use elements of the globally capitated risk model, the company believes that none captures all elements of agilon model. Key competitive factors include physician relationships, quality of care, payer relationships, and strength of economic model. The company relies on its platform, partnership, and network model to compete favorably.

My Opinion

In my opinion, the company has experienced significant growth in recent years, expanding its geographic presence and increasing its membership and revenue. However, it has also incurred net losses. Competition in the healthcare industry is intense, and the company faces established and diverse competitors. While confident in its business model and platform, the company must remain competitive and overcome financial challenges to achieve profitable long-term results. With all these risks being mentioned, I believe that the guidance given, potential economies of scale, and further addition of members could imply a valuation of more than $34 per share. The company appears a bit undervalued.

For further details see:

agilon health: Improved Member Growth And Economies of Scale May Imply Undervaluation