AGL - agilon health: Strong Sales Growth Lacks Remaining Value Drivers

2023-09-13 18:00:00 ET

Summary

- The company's stock has been on a volatile journey since December, currently selling at previous lows.

- A secondary offering of common shares by a selling stockholder saw the market react violently.

- Despite solid performance, via growth in sales and memberships, economic drivers are absent, with thin gross returns on assets employed.

- Net-net, reiterate hold.

Investment Briefing

Since the last publication , there have been numerous updates in the agilon health, inc. ( AGL ) investment debate that must be discussed in further detail. The company's equity stock has been on quite the journey since the December publication.

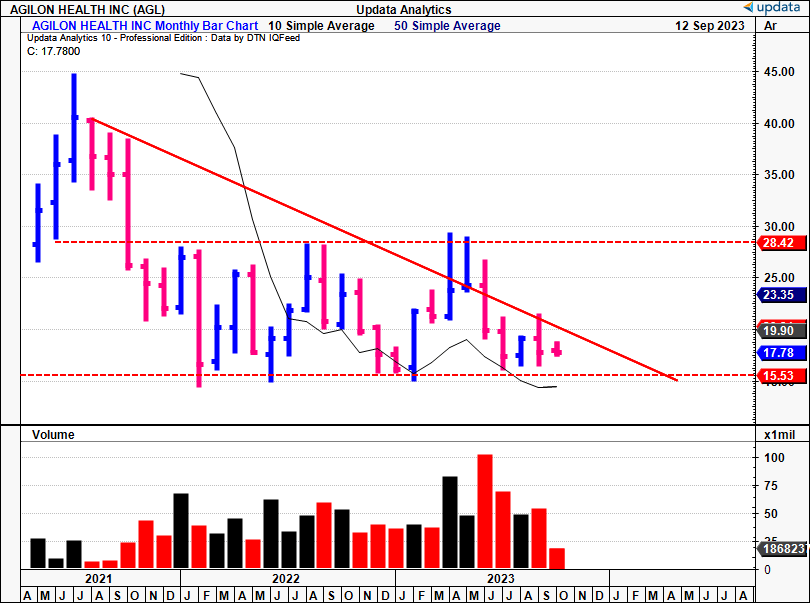

This report will unpack the moving parts in the debate, with particular focus on the economic levers that are impacting AGL's stock price from my perspective. As seen in Figure 1, the stock has sold within a broad range, failing to break key levels at each end of the channel. It now sells back at previous lows, and I'm not attracted to these valuations of just 1.6x forward sales and little-to-no profitability to speak of. Net-net, reiterate hold.

Figure 1. AGL Monthly Returns Since Listing

{kind=link}

Recent developments

- Secondary offering of common shares-but no proceeds gained?

In May, AGL completed a secondary public offering of ~87mm of its common shares. Specifically, the deal involved 86,884,353 common shares being offered by "a selling stockholder" (more on this in a second) at a price of $21.50/share. The selling stockholder was CD&R Vector Holdings LP ("CD&R"). The deal's underwriters were granted the option to acquire 10.5mm shares, and could purchase an additional 7.7mm shares on discretion as part of the transaction.

Critically, AGL did not receive any proceeds from the secondary offering. This boils down to the fact the follow-on was made by a selling stockholder (CD&R in this instance). If you didn't know, this shareholder could be an insider, an early investor, or any other entity that has previously acquired shares of the company. The company does not issue new shares in this type of offering. These shares are typically already in circulation.

Usually, the selling stockholder is an original investor, an employee who received stock options or grants, or an early stakeholder who wishes to collect profits on their investment by selling their commitments on the open market. In this kind of secondary offering, the proceeds of the sale of shares go to the selling shareholder and not to the company itself. This is in contrast to a typical secondary or follow-on offering, where the company raises proceeds to finance growth operations. The company may also help with the logistics and compliance requirements of the secondary offering, but again, it does not gain any direct financial benefit from the sale of shares by the selling shareholder.

There was about to be ~87mm of new supply in AGL's stock on the secondary market with this deal. So, it opted to buy back $200mm worth of stock (~9.6mm shares) from the underwriters, funded by its existing cash on hand. This reduced supply by that amount, and the underwriters could purchase another 18mm or so shares. CD&R in turn agreed to a lock-up agreement, where it wouldn't sell 100mm of its AGL shares for at least 900 days following May 15th. After the dust settled, CD&R now owns ~26.5% of AGL's equity.

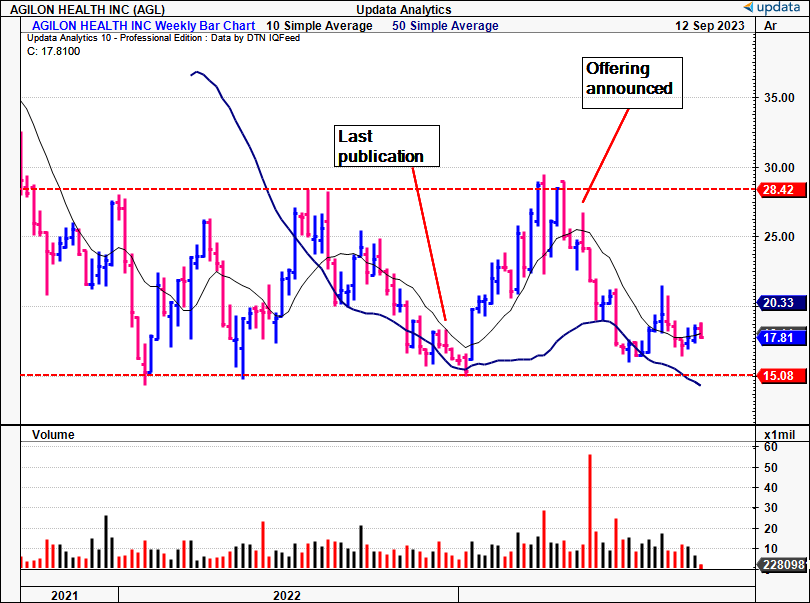

The market did not like this transaction, at all. You can see in Figure 2 the share price evolution last 2 years. After the December publication, AGL caught a strong bid, rallying from ~$16 to $28.

But the secondary offering saw investors dump the stock and send it back to former lows. I must admit a struggle to understand the economic rationale of this deal. Sure, it "creates strong long-term alignment between our key stakeholders" , as put by management on the Q2 earnings call . And sure, the buyback does reduce the float, per share metrics, etc., etc. But surely there is a more reasonable use of the capital, a $200mm 'investment', when the company's economics (discussed later) don't offer shareholders accretive value in the first place. The market certainly agreed with this sentiment.

Figure 2.

{kind=link}

Critical fundamental, economic factors

1. Breakdown of Q2 numbers

AGL had a strong financial performance in Q2 , growing sales 71% YoY to put up $1.15Bn. It's also grown revenues up by 73% to $2.29Bn this YTD. Growth was underscored by an increase in membership in both new and existing markets.

Given the revenue upsides in H1, management raised its FY'23 membership and revenue projections, and now expects total revenues of $4.5Bn at the lower range, up from the previous forecast of $4.4Bn. It expects core EBITDA of $0-$23mm on this. However, the company has moderated its medical margin outlook by ~$30mm, now forecasting a range of $500mm-$530mm.

Back to the quarter, positives from the top-line breakdown are as follows:

- Revenue per member per month ("PMPM") was up by 11%, primarily due to benchmark updates and membership composition. This includes higher benchmarks in several of its new markets. The medical margin PMPM increased by 9% to $113, compared to $103 in the previous year. H1 FY'23 medical margin PMPM was up 60% in dollar terms, and by 42% on a PMPM basis, reaching $166.

- Its Medicare Advantage ("MA") medical margin increased by 69% YoY to reach $138mm during the quarter. AGL's YTD figures were equally notable, posting medical margins up by 78% to $300mm. The growth in medical margin is good evidence of how mature AGL's markets and member cohorts in terms of lifetime customer cycles.

- Meanwhile, MA membership was up 57% YoY, tallying 409,000 members. This was on revenue growth of 71% to $1.15Bn. This exceeded the company's guidance and was supported by the successful onboarding of new primary care physicians ("PCPs").

- I'd also point out that AGL's Q2 medical margin included a $7mm net headwind from prior-year claims and revenue. Overall, this comprised $16mm from prior-year claims, offset by $9mm of prior-year revenue.

2. Economic growth levers

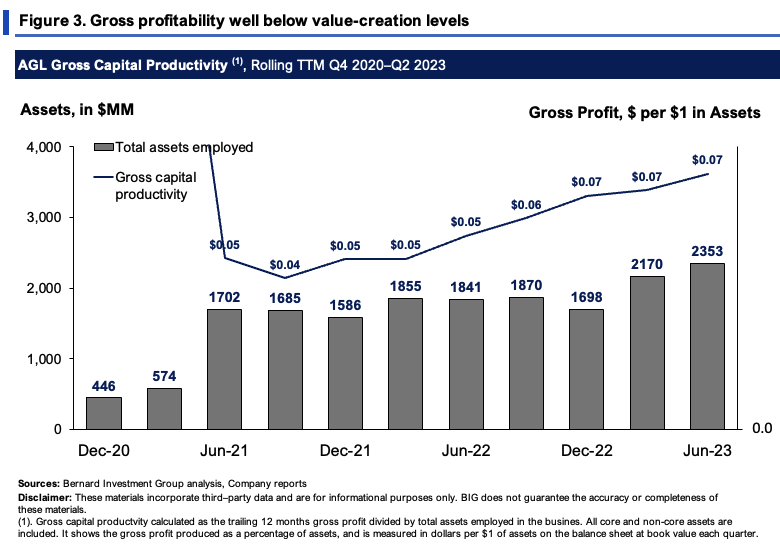

Asset values have been lumpy these last 2 years, as seen in Figure 3. The image shows the gross profit produced on these assets employed on a rolling TTM basis. Given AGL's lack of bottom-line fundamentals, this is a cleaner measure to observe accretions to corporate value.

The company is rotating back just $0.07 in gross for every $1 in assets employed. This is exquisitely low. A number of $0.33 is high, $0.7 exceptional. At $0.07 on the dollar, it doesn't suggest AGL is a lower-cost provider, nor does it have the propensity to send income further down the P&L, not in my view.

{kind=link}

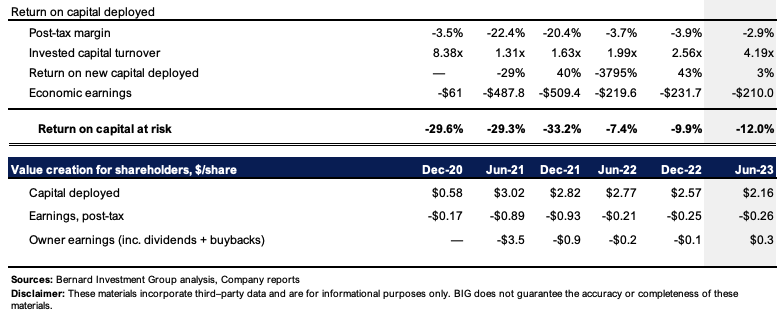

Regarding the deeper economics of the business:

- Post-tax margins are negative for the company and have been so since 2020 at least.

- But as a positive, it is turning over capital at very efficient rates. Each $1 of capital invested brings in $4.19 in sales, quite an attractive proposition. Problem is the new sales aren't profitable revenues. They are actually a drag on equity performance because it isn't meeting the capital charge required by most investors (in the realms of ~10-12%).

- It's acutely difficult to advocate buying a company that produces a $0.26/share loss on $2.16 of capital invested, with no change in this trend observed to date. By all measures outlined here today, these trends are likely to continue going forward in my view.

Figure 4.

{kind=link}

Valuation and conclusion

The stock sells at 1.6x forward sales and trades at an EV/Invested capital of 8x as I write. The latter is potentially attractive as it suggests the market values its investments very highly. But it needs profitability to back this up. Ongoing losses aren't going to cut it, even at the 1.6x forward. Further, the growth is seen in accounts receivable for AGL as it grows the business. In the last 2.5 years, every new $1 in sales has required an additional $0.26 in NWC, mainly from the receivables account, with fixed asset intensity up just $0.09 on the dollar. This will continue eating into cash flows going forward in my view.

Two other points to consider:

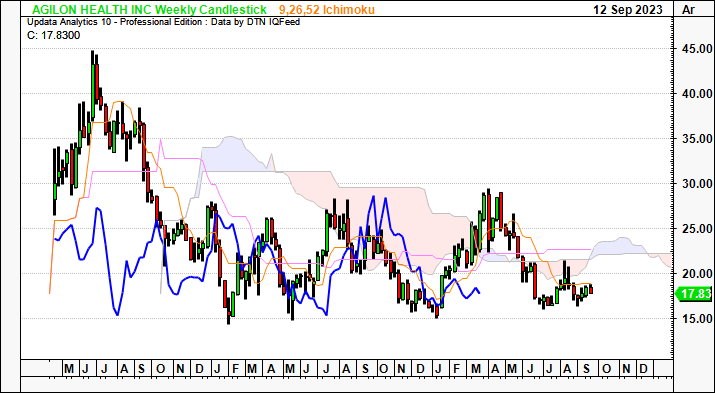

- The stock trades below major trend markers, shown in the cloud chart on Figure 5. It is a weekly chart, looking to the coming months. Both price and lagging line are below the cloud by some distance, showing the flat sentiment currently in AGL's stock.

- We also have downsides to $13.50 and an upside target to $19.75 on the P&F studies in Figure 6. The risk-reward on this flat, just ~$2/share in upside, but ~$5.20 in potential downsides if using these targets as gospel.

Both of these factors support a neutral view in my opinion, in line with the points on valuation.

Figure 5.

{kind=link}

Figure 6.

Data: Updata

In short, there are multiple hurdles for AGL to overcome at its current level of operations. The company is growing its top line at a reasonable clip, and unit economics are all favorable. But none of this carries below the top line. Asset intensity is high, more so relative to gross and net operating profits produced on capital used to run the business. These are factors that I cannot overlook based on our core investment tenets and the requirement of somewhat predictable, stable cash flows into the future. I just can't get there with AGL at this point in time. Net-net, reiterate hold.

For further details see:

agilon health: Strong Sales Growth, Lacks Remaining Value Drivers