AGL - agilon health: Strong Value Proposition In The Industry

2023-04-06 00:55:53 ET

Summary

- agilon health hosted its 2023 investor day, with positive updates on new health system partnerships and favorable updates to 2026 targets.

- Post the investor day, I have further conviction on AGL's value proposition.

- With the CMS rates now finalized, there is a chance for FY24 guidance to be revised upwards.

Thesis

agilon health ( AGL ) hosted its 2023 investor day on 30 th March, which I had an overall positive takeaway. I was encouraged by the announcement of two new health system partnerships and favorable updates to 2026 targets. That said, I believe the share price reaction was largely due to a rebasing of investors' expectations, which apparently had a much higher expectation for FY24 and FY26. If we look at my initial model , I valued AGL stock at $21.32, which has been far surpassed to a high of $29.44. I believe my thesis was playing out and multiples have been shifting upwards as AGL is expected to generate positive EBITDA In FY23. At the height of $29.44, valuation was at 2.4x forward revenue, which was 50% higher than the 1.6x assumption I made, and I believe that valuation too much optimism despite the uncertainty with MA rates (which has now been cleared, discussed more below). Nonetheless, prices have dropped since the presentation, and I think it's important to zero in on the 2026 forecast. AGL raised 2026 targets despite taking a conservative stance on the potential rate headwind in 2024 (which has been better than expected), so the increase may not have been as strong as hoped (which I believe a revision is possible in light of the new CMS rates). Strong membership growth and a consistent medical margin trajectory across cohorts, in my opinion, also improve transparency into the attainability of 2026 targets. I stand by my recommendation to buy.

Long-term guidance

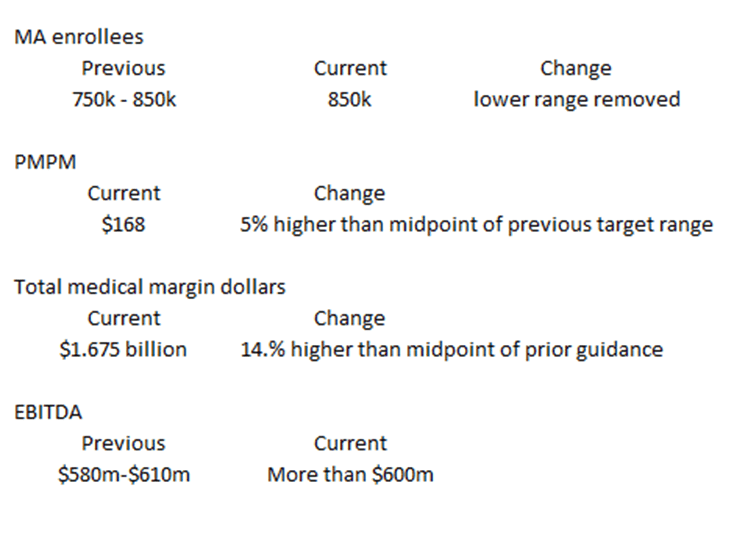

AGL's initial revenue outlook for 2024 was $5.5 billion, $200 million below consensus estimates. Management remarked that the guidance is based on the assumption that the proposed changes to the risk adjustment model will be implemented as written, and that the effect on AGL will be comparable to that of the industry as a whole. Given that the finalized rates are better than the proposed rates, I believe the FY24 now seems to be over conservative, and there is a chance for guidance revision. Importantly, management has also increased 2026 targets, albeit by a small amount. AGL's target range for Medicare Advantage enrollees has increased from a range of 750k to 850k to 850k, and the company's projected medical margin PMPM for FY26 has increased to $168. The new midpoint for medical margin dollars is $1.675 billion, up 14.5% from the previous guidance, and the new midpoint for adjusted EBITDA is over $600 million. In addition, management noted revised expectations around FFS trends, resulting in a decrease from $60 million to $35 million for the ACO REACH adj. EBITDA contribution in 2026. I still hold the belief that it is highly predictable to estimate AGL's medical margin and adjusted EBITDA in the long run, due to the steady performance of medical margin in various market classes and the expectation that more than 87% of the projected members in 2026 will have been using the platform for at least two years.

{kind=link}

Partnerships

Premier Health in Ohio and Holland PHO in Western Michigan launching as new health system partners for the class of 2024 is, in my opinion, a positive driver for growth going forward. As a result of this launch, management is expecting a greater increase in TAM and membership by the year 2024. To provide a better understanding of the situation, it should be noted that Premier Health and Holland PHO are the second and third health systems to partner with AGL, respectively, after the implementation of MaineHealth with the class of 2023. Furthermore, I believe it is significant that MaineHealth's performance thus far is in line with AGL's physician group partners, suggesting that unit economics are stable. The expansion of AGL's in-market TAM opportunity and the subsequent sustained growth of same-geography membership should result from the company's efforts to forge partnerships with health systems, in my opinion.

Value proposition

I also gained a deeper understanding of the AGL value proposition as a result of the investor day. At its most basic level, AGL's model provides doctors with tools to gain a deeper familiarity with their patient populations, especially those with chronic conditions, and to significantly enhance their performance and consistency. Care and quality metrics where AGL stands out from the MA industry as a whole were highlighted. For instance, compared to the industry average of 3 Stars, AGL has earned 4+ Stars on cancer screening and chronic condition management metrics. AGL also hosted a group of partner physicians to discuss the ways in which AGL model improves clinical outcomes, service to patients, and job satisfaction among doctors. The most crucial takeaway from the discussion was that AGL has superior data and analytics compared to its rivals, allowing doctors to more accurately risk-stratify patient populations, implement and match patients to clinical care programs, and discover ways to collaborate with specialists to reduce costs. All of these further reinforces my view that AGL can continue to penetrate this industry and grow over the long-term.

CMS rates

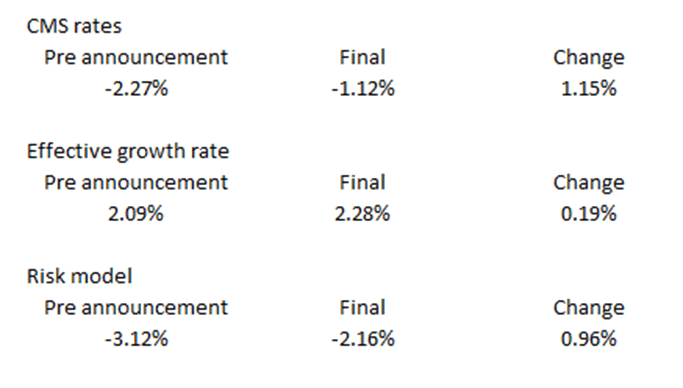

CMS has released the Medicare Advantage Rate Announcement for 2024, which shows better rates than the previously proposed rule, improving by approximately 115bps. In February, CMS published the Advanced Notice proposing a reduction of approximately -2.3% per member for 2024, which disappointed investors. However, with the final rates now set, CMS expects a decrease of -1.12%, which is about 115bps better than the proposed rule. This is due to the changes in the effective growth rate, which has increased from 2.09% to 2.28%, and the risk model revision, which has increased from -3.12% to -2.16%. These changes will be phased-in over three years, resulting in a smoother transition and allowing the industry time to adjust to the new model. Overall, I see these updates as favorable, and they are more consistent with historical rate patterns of modest improvement from advance to final rates. This is particularly beneficial for AGL, as a value-based care provider exposed to Medicare Advantage.

{kind=link}

Risks

AGL may have to give up more of their economics in order to compete in a market with more intense competition than I currently anticipate in order to attract new physicians and find anchor partners. Revenue and profits could also be negatively impacted if CMS reduced MA or direct reimbursement rates.

Conclusion

In conclusion, the 2023 investor day was an overall positive event, with the announcement of two new health system partnerships and favorable updates to 2026 targets. Although the share price reaction was due to a rebasing of investor expectations, AGL's multiples have been shifting upwards as it is expected to generate positive EBITDA in FY23. The increase in 2026 targets, the strong membership growth, and the consistent medical margin trajectory across cohorts, improve transparency into the attainability of 2026 targets. The partnerships with Premier Health and Holland PHO are positive drivers for growth, and AGL's value proposition as a tool for doctors to gain deeper familiarity with their patient populations was further reinforced. The CMS rates have been finalized and are better than the previously proposed rule, improving by approximately 115bps, making the outlook for AGL even more favorable. Overall, I stand by my recommendation to buy AGL.

For further details see:

agilon health: Strong Value Proposition In The Industry