AGNCO - AGNC: Better Preferreds Elsewhere Except For AGNCL

2023-11-03 10:22:01 ET

Summary

- We discuss the horrendous book value result for AGNC in the context of its preferreds.

- Higher rates are not the main cause of the decline in book value for mREITs like AGNC - Agency spreads are.

- AGNC may have also been caught out by the steepening of the yield curve.

- AGNCL is the only AGNC preferred that looks attractive - investors should look to NLY and DX preferreds for non-CMT coupon structure.

This week mortgage REIT AGNC Investment Corp ( AGNC ) released preliminary estimates for Q3 earnings, and they weren't great. Specifically, book value was $8.08 as of Q3 or 14% down from the prior quarter. However, and this is likely what precipitated the preliminary estimate, book value midpoint estimate was $6.78 ex-dividend as of 20-Oct or another 16% lower for a total drop of a hefty 28% from Q2.

In this article we discuss these developments from the perspective of preferreds holders as well as how we are positioning in the AGNC preferred suite and, more broadly, the Agency mREIT preferreds sector.

What Happened?

Agency mortgage REIT AGNC has seen better days. The stock is down 13% this week and is down 30% since the end of Q2. What investors will tend to read is that higher rates are what's causing so much Agency mREIT book value pain.

This "higher rates cause lower book values" catechism is, as the old saying goes, clear, simple and wrong. After all, if it were true, book values wouldn't have fallen over the initial COVID period when rates collapsed. For instance, AGNC book value fell 23% in Q1-2020 despite the 10Y Treasury yield falling 1.2%.

Intuitively it makes sense that AGNC would be exposed to rising interest rates - after all it holds primarily 30Y Agency MBS which have a sizable duration exposure. However, mREITs use interest rate hedges to limit their exposure to changing interest rates.

For example, AGNC showed in Q2 that for a 0.75% rise in rates, book value would fall 5.4%, all else equal. Over Q3, rates are roughly 0.75% higher (somewhat different across different tenors as the curve has steepened) and yet the AGNC book value is down almost 3x as much.

DX

This is because interest rates are not the key driver of book value. This largely has to do with the fact that mortgage REITs tend to hedge their outright interest exposure. Let's go through the real drivers of book value.

First, AGNC had a small net duration gap at the end of Q2 of 0.4 - fairly small, but it does scale up with leverage.

Two, Agency MBS are negatively convex while the common hedges like interest rate swaps and Treasuries are linear. This means that the company’s duration lengthens as rates move higher. As rates moved higher over the quarter the company was losing money at an increasingly fast clip and adding hedges at increasingly unfavorable levels.

Third, AGNC may have gotten caught out by the steepening of the yield curve. It holds primarily 30Y mortgages with a focus on the higher coupons. With the recent move in mortgage rates to 8%, a mortgage with a 5% coupon is much less likely to get refinanced. And it is higher coupon MBS that are more negatively convexed than lower coupons (in part because slightly out-of-the-money coupons become in-the-money on a forward basis given the still inverted yield curve).

This means that its hedges, which are primarily in the belly of the curve may have been insufficient. This is precisely the situation that Dynex Capital ( DX ) which breaks out its yield curve exposure profile found itself in. Specifically, DX had a bear steepener on.

For DX, the steepening of the yield curve shaved off around 4% off its own book value. It's not clear if this is what drove the additional book value loss for AGNC, but it may have played a role.

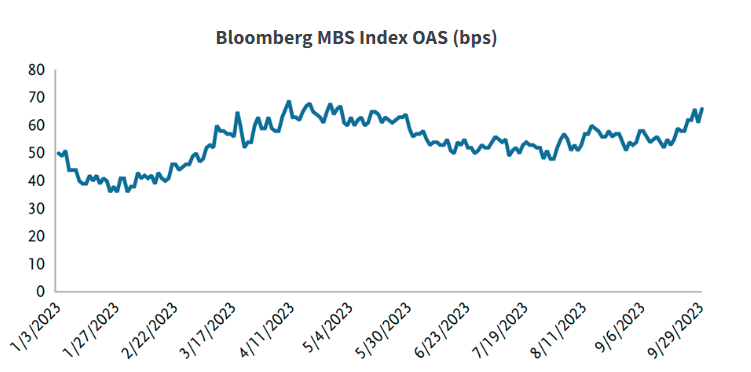

Finally, MBS spreads rose over the quarter as the chart below shows. DX said that their portfolio experienced a 0.15% spread widening over the quarter and another 0.15% since the end of the quarter. It appears that the higher coupons - held by AGNC and DX - performed better than lower coupons, but even they were not immune to wider spreads.

{kind=link}

Ultimately, like we saw in early 2020, mREIT book values are much more driven by Agency OAS rather than "interest rates". At this point, Agency spreads are extremely elevated, under pressure from both the Fed's Quantitative Tightening as well as high interest rate volatility which exacerbates the negative convexity of Agency MBS.

Our Allocation in the AGNC Preferreds Suite

Our allocation in the mortgage REIT space has been very consistent - we stick with preferreds over the common. The chart below shows that AGNC preferreds (orange line) have delivered a steady return over the last nearly 10 years while the common has repeatedly crashed, now trading below its starting point since the period for which we have preferreds data.

Systematic Income

This chart shows that while preferreds have delivered a very respectable annualized return of around 6.7% over the last 9-odd years, the common is in the red.

Systematic Income

To be fair, we don't rule out a period of strong outperformance by the common - in fact, we have seen several periods of common outperformance in the past. However, it is very unlikely that the common will deliver a consistently higher return than the preferreds over this period into the future, particularly now that the preferreds have and will continue to step up to higher coupons.

Our allocation within the AGNC preferreds suite - shown below - is very simple - we only like the Series G ( AGNCL ). AGNCL is a so-called CMT (constant maturity Treasury) preferred in the sense its coupon will reset to the 5Y Treasury yield plus a spread on its first call date, unless redeemed.

Systematic Income Preferreds Tool

For non-CMT coupons, we favor NLY and DX preferreds because investors can get similar yields and coupon structure as AGNC preferreds but with a stronger fundamental profile. DX and NLY preferreds have equity coverage that is close to double that of AGNC, and they have also tended to have a lower level of book value beta, something that is valuable for preferreds holders who worry more about the downside rather than upside

For example, investors who like the floating-rate profile of AGNCN should instead consider NLY.PR.F. The two stocks are trading right on top of each other in yield terms which doesn't make much sense given their very different equity coverage levels - 6.9x for NLY and just 3.4x for AGNC.

Systematic Income Preferreds Tool

For investors who like the Fix/Float profile (i.e. a fixed-coupon now and a likely step-up to a floating-rate profile later) should have a look at DX.PR.C which looks attractive relative to the 3 AGNC Fix/Float preferreds. Granted, AGNCP does edge out DX.PR.C over the longer term however it does come at a cost of a substantially lower yield through Apr-2025 which it only claws back around 2027.

Systematic Income Preferreds Tool

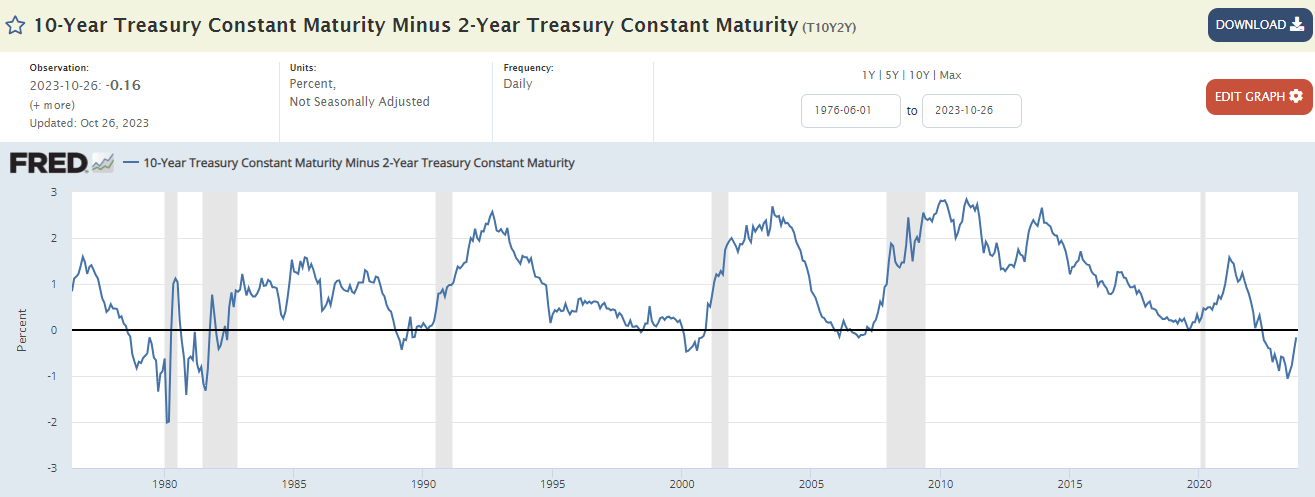

AGNCL is not the only CMT preferreds we hold in our Income Portfolios. The attraction of this niche space is that the yield curve remains inverted - something that's very unusual historically. Although it has nearly disinverted with the recent back-up in longer-term yields, there is likely more room to run based on the historical pattern as the chart shows below.

{kind=link}

AGNCL offers an attractive yield of 9.6% now - currently the second highest in the suite. Although it is then expected to fall to the lowest yield in the suite until its own first call date in 2027, this yield is "locked in" and will not fall if the Fed decides to take the policy rate lower. And if forward rates are realized, its yield will move to the top of the list on its first call date.

Systematic Income Preferreds Tool

Both Agency and CMT preferreds remain attractive components of diversified income portfolios. Agency mREIT common shares have struggled recently on the back of widening Agency OAS, however the preferreds have held up much better. At the same time, CMT preferreds should continue to benefit from yield curve disinversion as well as a coupon that is locked in for several years even if the Fed decides to take the policy rate down.

For further details see:

AGNC: Better Preferreds Elsewhere Except For AGNCL