AGNC - AGNC Investment: Not Even Touching The 10% Preferred Shares

2023-10-09 10:28:12 ET

Summary

- AGNC Investment Corp. has a dividend yield of 16% on its common shares and a floating preferred share issuance with a 10.6% yield.

- AGNC's net interest income has been negative due to higher interest rates, and its cash flow statement shows cash burn.

- The company's reliance on derivatives and hedges is not a sustainable long-term strategy, and the value of its agency portfolio has dropped.

AGNC Investment Corp. ( AGNC ) is a real estate investment trust that invests primarily in agency backed mortgage securities. This mREIT has a dividend yield of 16% on its common shares and one of its preferred share issuances ( AGNCN ) is floating with a 10.6% yield. With AGNCM and AGNCO set to float next year and AGNCO trading at the biggest discount, I wanted to take the opportunity to review the viability of these preferred shares. I discovered serious concerns and am advising against an investment in AGNCs common and preferred shares.

QuantumOnline

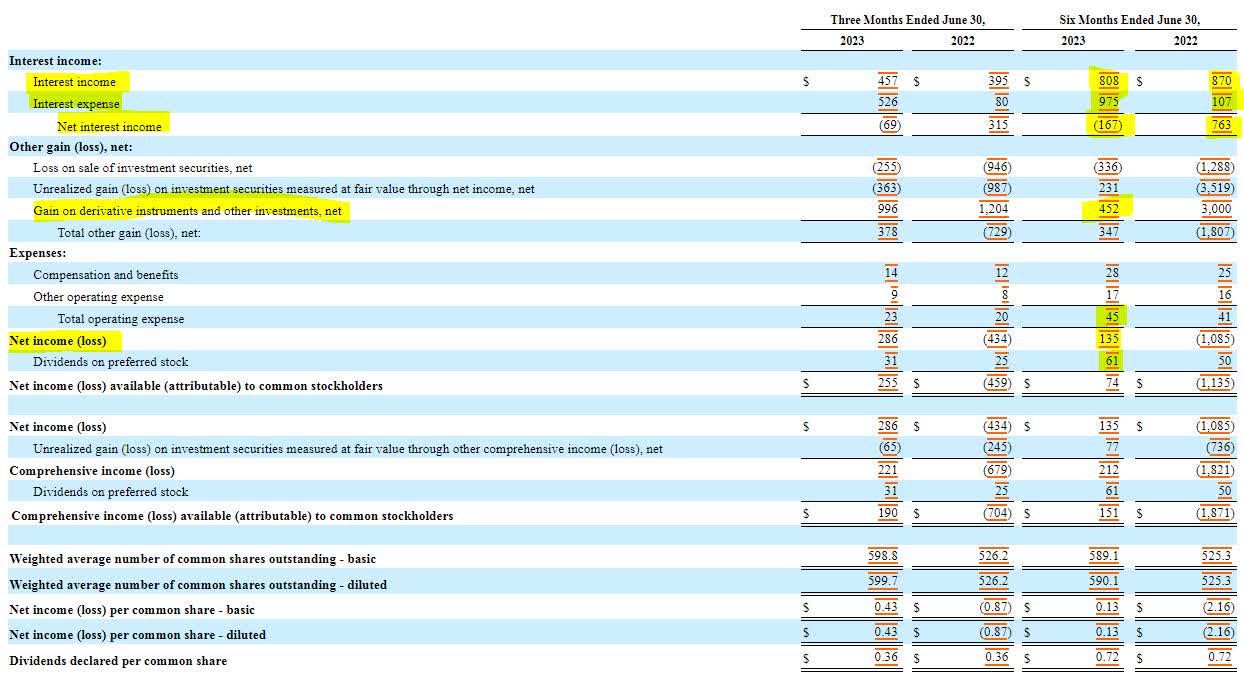

AGNC’s primary source of income is the investment of agency backed mortgage securities and that investment is currently upside down. During the first half of 2023, net interest income was negative compared to $763 million in net interest income during the same period last year. This is due to higher interest rates feeding into the company’s borrowing costs. AGNC’s only saving grace has been $452 million in derivative income from hedging against higher interest rates.

{kind=link}

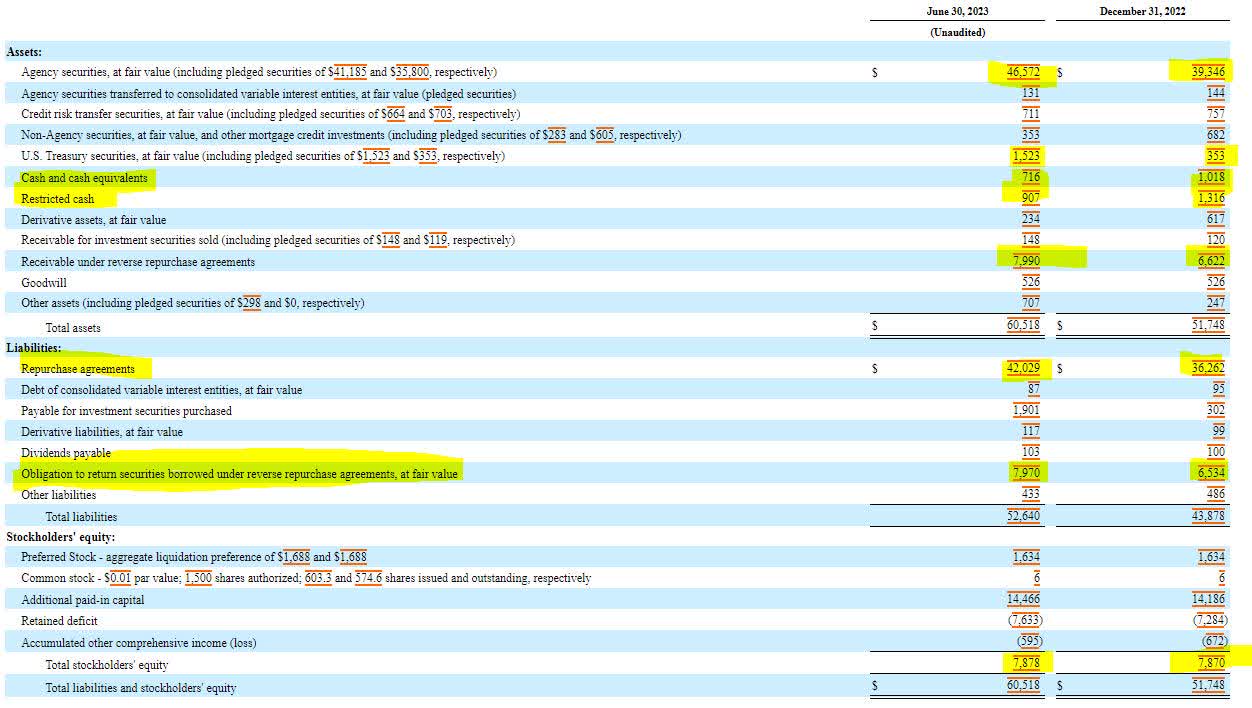

A look at AGNC’s balance sheet gives investors a better idea of how the organization operates. The primary assets are agency backed securities and the primary liabilities are repurchase agreements. Essentially, the company borrows short, with repurchase agreements that mature in days and lends long towards mortgages that mature years down the road. Shareholder equity has remained constant in 2023, but cash has been drawn down from $2.3 billion to $1.6 billion. It is important to note that the company has increased its investment in U.S Treasuries.

{kind=link}

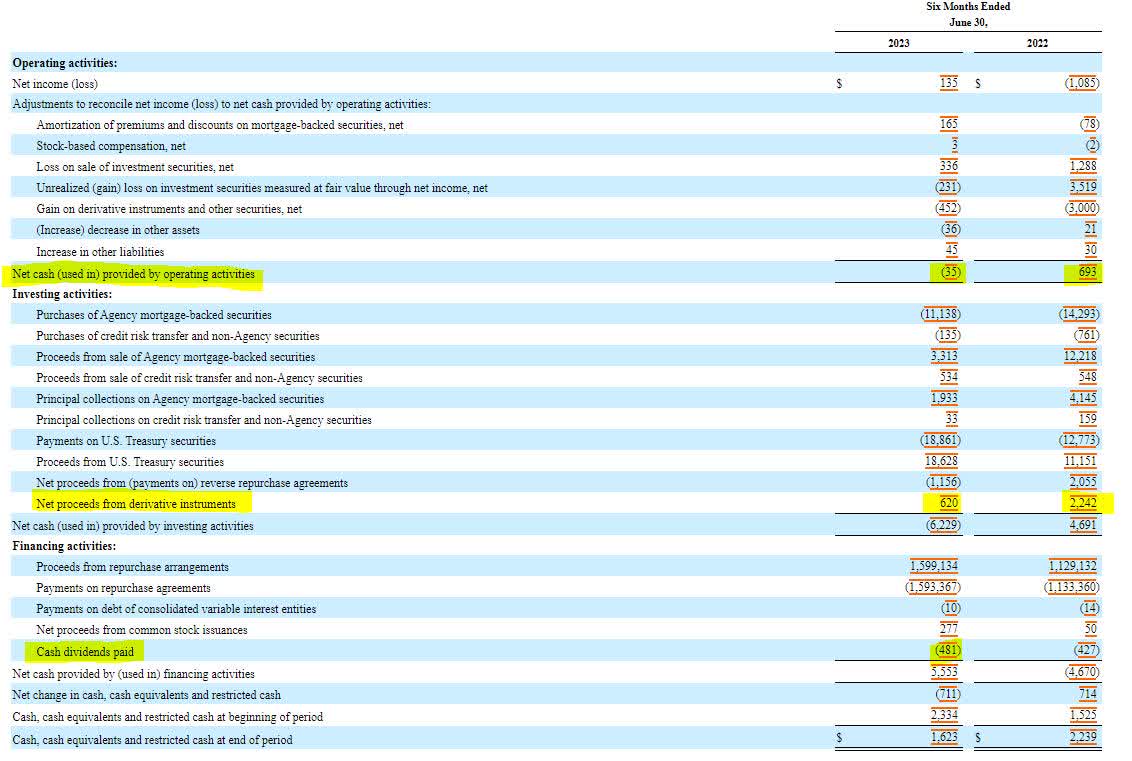

The company’s cash flow statement continues to draw on the concerns of the operating losses. Day to day operations have burned $35 million in cash year to date. The only saving grace to cash flows once again is the over $600 million generated by the sale of derivatives. This sale of derivatives was the sole source of funding dividends. While hedging is a great strategy to protect a company from short term losses, it is not a viable strategy for long term shifts in the marketplace. At some point, the advantage of derivatives is going to run out.

{kind=link}

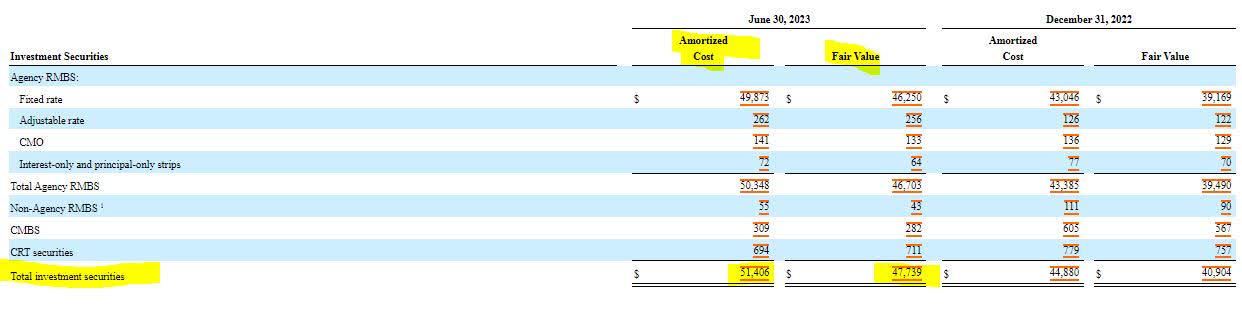

Unfortunately, unlike other REITs, the sale of assets is not a good option for funding any future cash shortfalls or dividends. With the rise in interest rates, the value of the company’s agency portfolio has dropped, leaving a nearly $4 billion unrealized loss on the portfolio. This would become a realized loss if the assets were sold.

{kind=link}

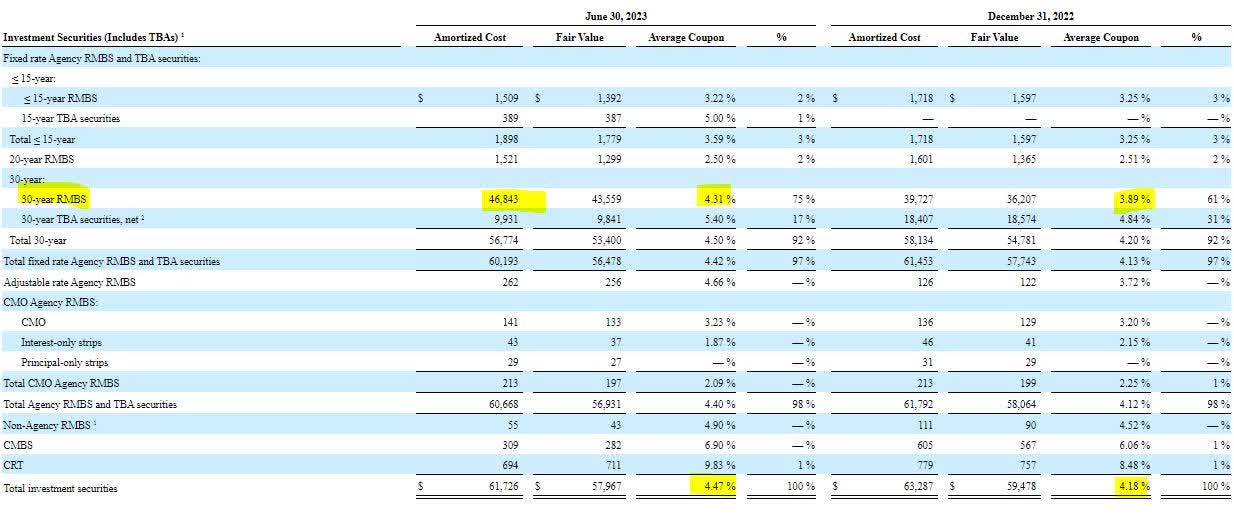

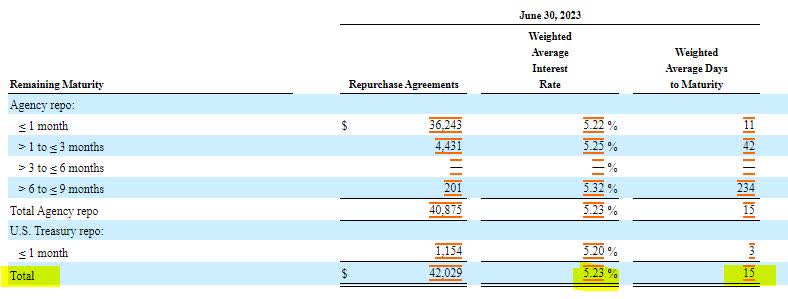

What’s worse is that the average loan yield in the entire portfolio currently sits at 4.47%. These loans were underwritten and purchased during the pandemic response when interest rates were historically low. Most of these fixed rate investments mature in 5 to 10 years, meaning it will be awhile before the company gets the principal back to invest and raise its portfolio yields. Furthermore, the average interest rate on the company’s borrowings is 5.23%, 75 basis points higher than its income yields. AGNC is holding long term, low yield assets with near constant maturity of higher interest rate liabilities.

{kind=link}

{kind=link}

{kind=link}

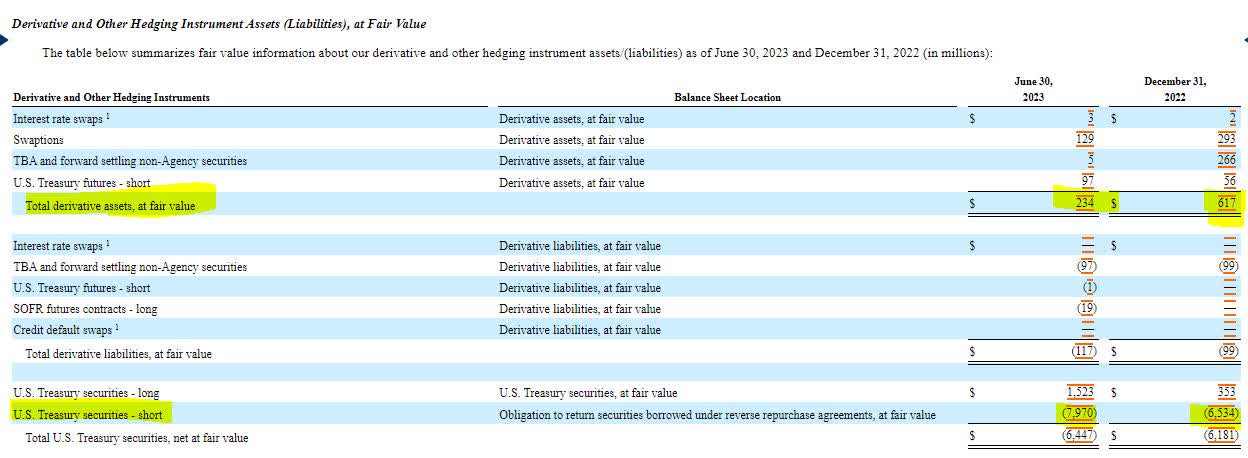

The clock is also quickly running out on AGNC’s derivatives hedge, with the balance of its derivatives holdings down nearly $400 million from the end of last year. The company has taken on a short position of US Treasuries, but based on the balance sheet, I don’t believe it hasn’t earned a significant amount of cash.

{kind=link}

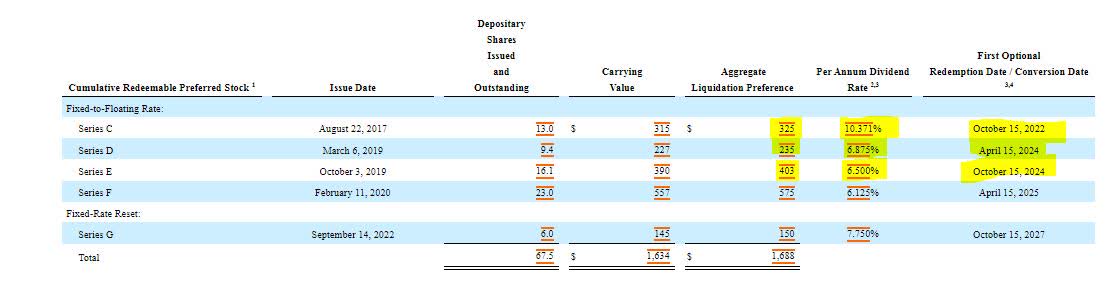

Depending on hedges and derivatives is not where I want my preferred share investments to be when investing. Additionally, the floating nature of one preferred issuance and two others scheduled to float next year, makes the investments less attractive. With three preferred issues scheduled to yield over 10% by the fourth quarter of next year, the accelerated dividend obligation against the underperforming assets means the dividend will be even less sustainable in twelve months.

{kind=link}

Some are hoping that higher mortgage rates will help AGNC as higher mortgage rates mean higher return on agency backed mortgages. The problem here is that the returns can only be attained if demand holds up. As interest rates have risen, mortgage underwriting has collapsed, demonstrating that mortgages are highly elastic and higher yields don’t necessarily mean higher volumes.

{kind=link}

Investors are drawn to AGNC due to the agency backed mortgages, which are insured by the government. The quality of the assets is not the problem, though, it's the fixed, long-term yields at rates below current borrowing costs. While the hedges are doing their job, they are not a long-term solution. Investors who believe that interest rates will drop in the near term are better off buying long duration Treasury bonds.

For further details see:

AGNC Investment: Not Even Touching The 10% Preferred Shares