AGNCM - AGNC Q1 Earnings: Shrinking Assets Expanding Share Counts

2023-04-25 07:00:00 ET

Summary

- AGNC Investment reported Q1 2023 results and the adjusted non-GAAP income looked strong.

- Total economic return as presented by AGNC was negative.

- We look at where things stand and why AGNC preferred shares might be a better bet.

When we last covered AGNC Investment (AGNC) we told you our sell trigger and explained why the company remained a poor investment.

AGNC like the mortgage REIT sector as a whole, is a poor generator of total returns. In general, if someone wants to get involved with this sector, our choice is to stick with the preferred shares. In case of AGNC, we don't like the preferred to common equity ratio, although it has improved thanks to the massive common share issuance. We rate AGNC a hold at this point and would move to a Sell rating over $12.50.

Source: Share Issuance & Asset Sales Continue To Dilute Potential Upside

While the call worked perfectly, after all who is not happy to have avoided this yield trap for yet another quarter, we did not get the short sell trigger. The stock went straight down. The stock is now down 13% and we just got the Q1-2023 results .

Seeking Alpha

Let's look at that to see if we see some hope for the long suffering bulls.

AGNC Investment Q1 2023 Results

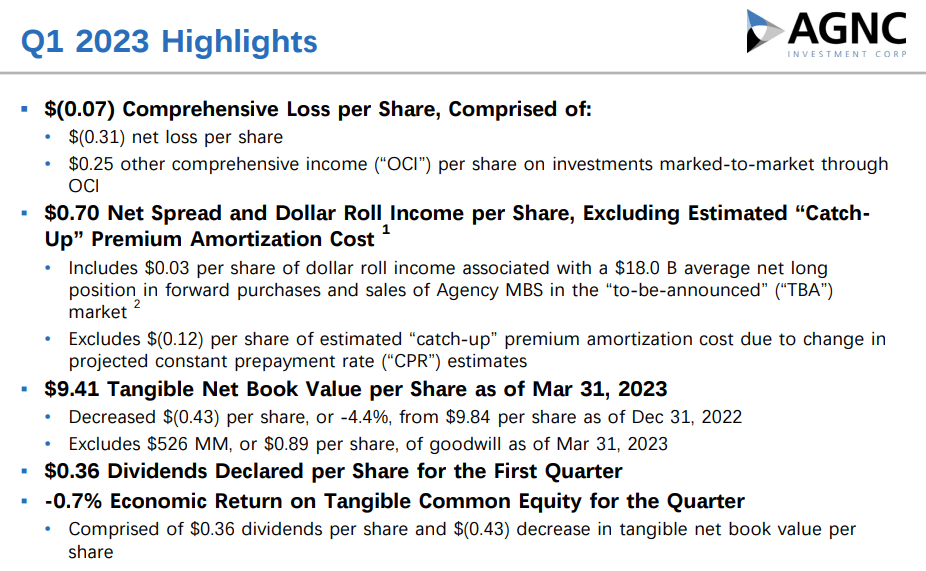

AGNC announced the non-GAAP earnings number of 70 cents a share. That number has generally had little bearing on economic returns and tangible book value. We saw that once again with net tangible book value per share declining 4.4% in the last quarter.

{kind=link}

The negative 0.7% actual economic return is a fairly good measure and one we encourage investors to keep track of. Leverage for the quarter came in at 7.2X, a shade below the 7.4X at the end of last year. Now enquiring minds want to know as to how leverage declined, if tangible book value dropped at a 17% annualized rate? We get that answer in the slide below.

{kind=link}

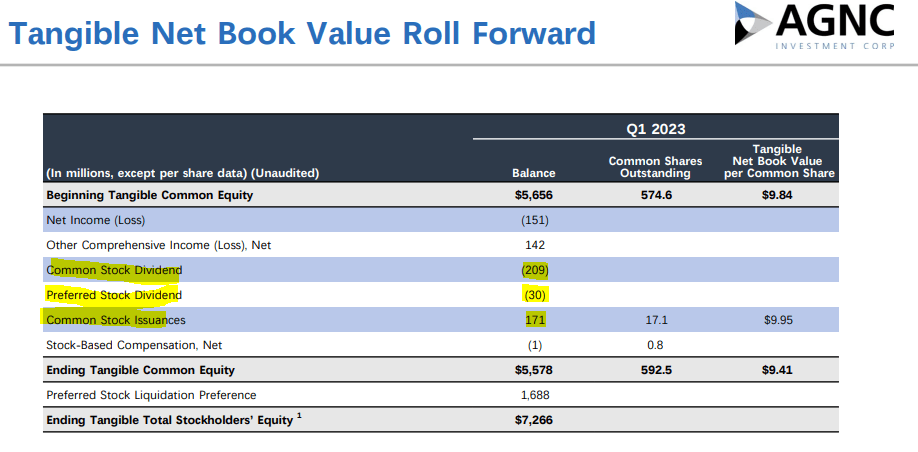

17 million of shares issued at $9.95 per share definitely helped. Another way to look at it is that AGNC did not really create any economic returns during the quarter. But it still paid $239 million of common and preferred share dividends. $171 million of that $239 million was offset via share issuance.

{kind=link}

Outlook

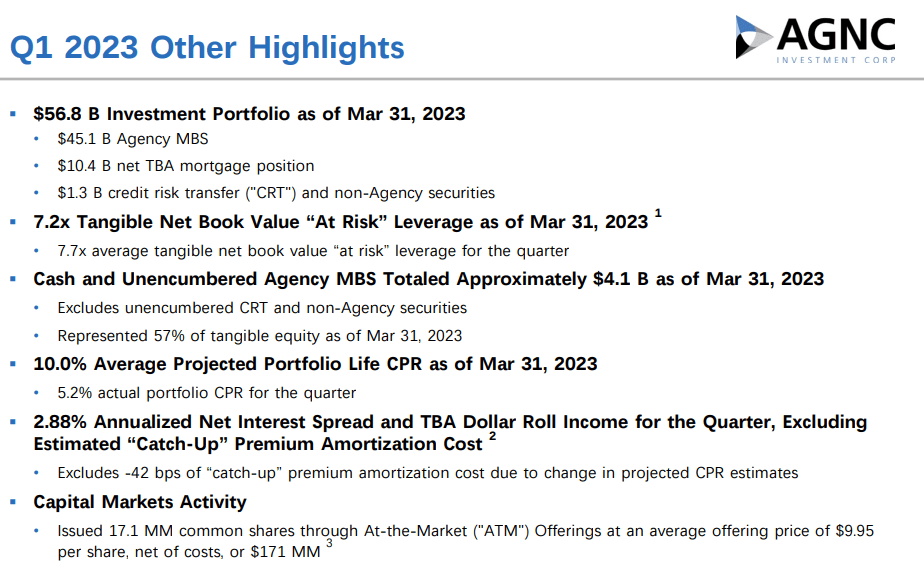

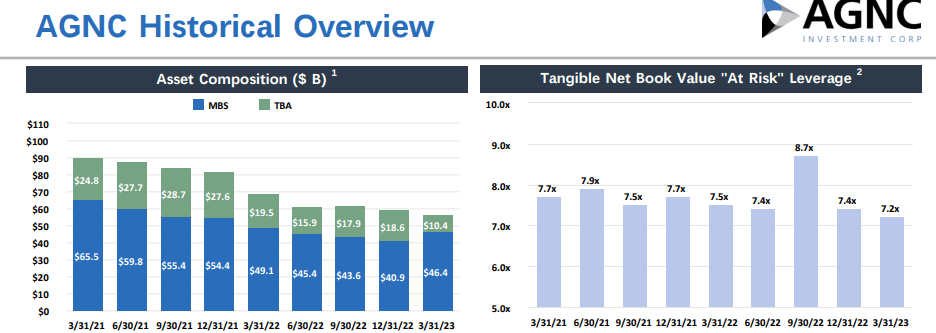

AGNC has collapsed its portfolio over the last 9 quarters from $90 billion to $57 billion. There was small drop (only $2.7 billion) this quarter as well.

{kind=link}

Apparently they are still missing the memo from the bulls that this is the greatest time to buy mortgage backed securities. They just keep liquidating on a net basis, quarter after quarter. Go figure. Comprehensive income has been negative through this time and tangible book value has fallen by almost 50%.

AGNC Presentation

The big saving grace for AGNC continues to be its outlandishly large hedge position on short term interest rates . If you look at the income statement, interest expenses are already ahead of interest income.

{kind=link}

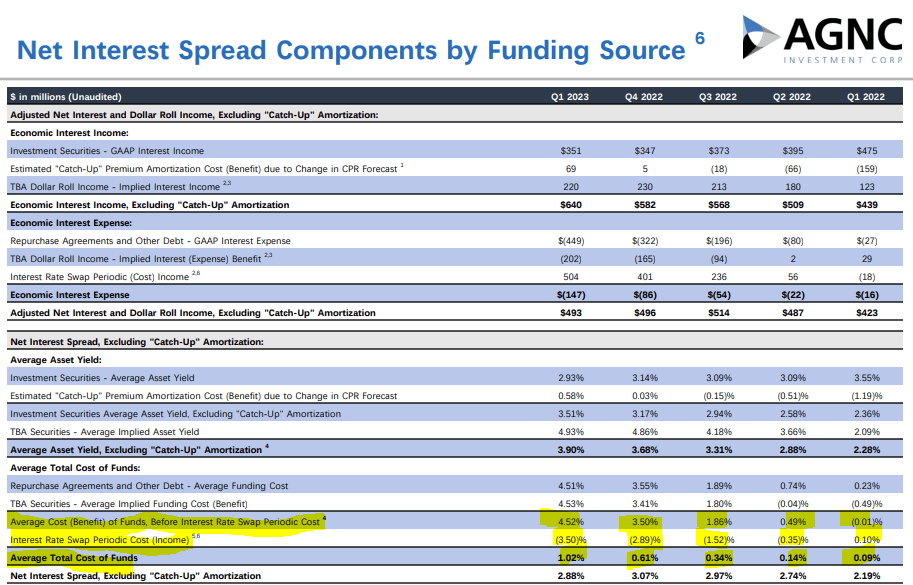

This is because their extremely long duration mortgage backed securities have been paired up against rapidly resetting short term interest rates. But that is not the whole story thanks to the hedges. This can be visualized in the next slide. AGNC's asset yield is below the cost of its funds. But the rapidly rising interest costs are being offset by swap income (hedges).

{kind=link}

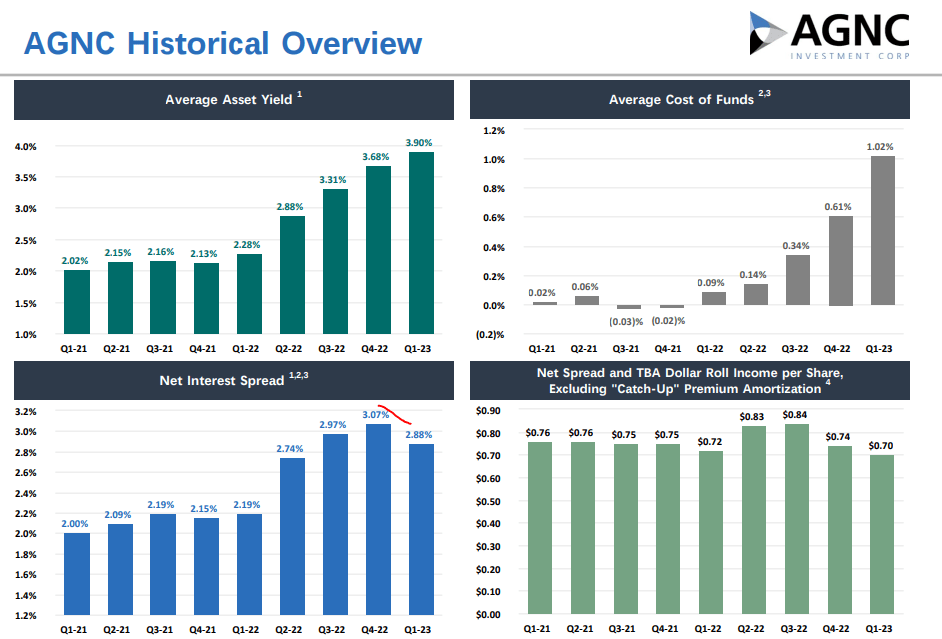

While AGNC's interest costs are going up, they continue to be tremendously advantaged compared to the rest of the mortgage REITs.

{kind=link}

But in all likelihood, this spread income has peaked as well and we are now likely to move into the downslope. We will add here that this is happening even on a far smaller portfolio than what AGNC had when it created these hedges.

Verdict On AGNC Common Shares

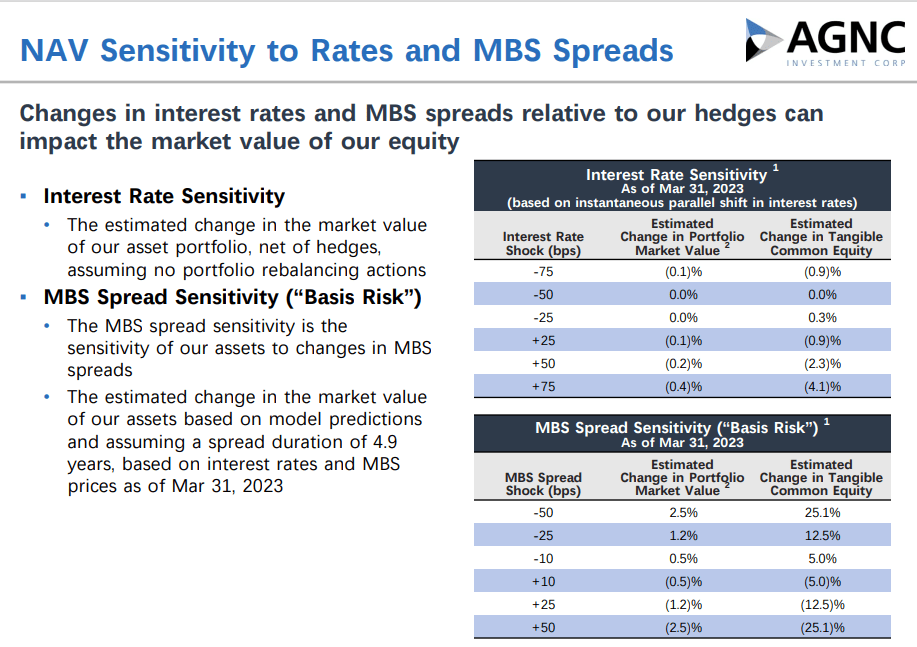

Mortgage REIT positioning is a bet that we don't get a further explosion in spreads. You can see below that a 50 basis point further spread expansion between mortgage backed securities and treasuries can wipe out 25% of their portfolio.

{kind=link}

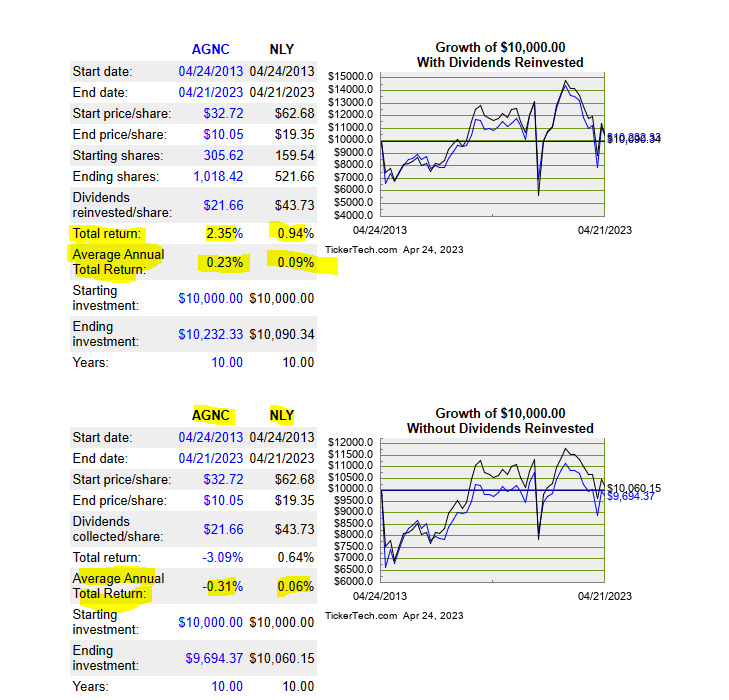

Of course there are mitigating steps including issuing equity and adding some expensive hedges on spreads, but that does not help the common shareholder. That has been the long term story for AGNC and most other mortgage REITs. We have shown Annaly Capital Management Inc. ( NLY ) as a comparative.

{kind=link}

Of course real returns have been far lower as there are big taxes to pay on the "income". While some may see this as a bargain with a 14% yield, we would still stay out as the headwinds are too severe. We have a massively inverted curve and at some point AGNC's hedges will run out. Even if they don't run out before the next round rate cuts start, investors should recognize that the tangible book value already incorporates the gains on these hedges. In other words, that $9.41 per share includes all the credit for that great decision. Buying AGNC because they have those hedges is equivalent of double counting. We would show you a comparative chart of where AGNC stands relative to other mortgage REITs, but that will be misleading in our opinion. It would imply that if you get this cheap enough relative to tangible book value, you should buy it. While we have made a similar argument on occasion for different mortgage REITs, at this point in the cycle, we think the risks are just too great to do that.

AGNC Preferred Shares

While common shareholders have not made any money over the last decade, the preferred shareholders have been sitting pretty. AGNC has 5 preferred shares listed currently.

- AGNC Investment Corp. 6.12 DP SH PFD F (NASDAQ: AGNCP )

- AGNC Investment Corp. 6.5% DP SH PFD E (NASDAQ: AGNCO )

- AGNC Investment Corp. 6.875 DEP REP D (NASDAQ: AGNCM )

- AGNC Investment Corp. CUM 1/1000 7% C ( AGNCN ).

- AGNC Investment Corp. 7.75% DP PFD G (NASDAQ: AGNCL ).

AGNCN (also known as series C) is the most interesting one here, floating currently at 10.37129% in the most recent quarter.

The Series C annual dividend rate is as of the most recent dividend determination date. Series C accrues at a floating rate equal to 3M LIBOR plus a spread of 5.111%, per annum. Commencing on July 15, 2023, the Series C will accrue at a floating rate equal to 3M CME Term SOFR plus 0.26161%, plus a spread of 5.111%, per annum.

Source: AGNC

This is fairly expensive for AGNC, especially if we get two more rate hikes from the Fed. We think that AGNC will call these very soon and if they do so via common share issuance, it would improve the common equity buffer over remaining preferred shares. These shares make sense for those believing in the "higher for longer" scenarios, as these would definitely force AGNC's hand.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

AGNC Q1 Earnings: Shrinking Assets, Expanding Share Counts