DX - AGNC Q2 Earnings: A Relatively Solid Quarter

2023-07-25 11:34:39 ET

Summary

- AGNC Investment reported a relatively good quarter.

- Share issuance was again the primary highlight though as AGNC used the premium to book value to unload over 10 million shares.

- Hedges fall a lot over the next 12 months and the dividend will likely be readjusted lower after that.

In our last coverage of AGNC Investment Corp. ( AGNC ) we suggested that investors avoid the company and should even take a vacation from the sector.

We would show you a comparative chart of where AGNC stands relative to other mortgage REITs, but that will be misleading in our opinion. It would imply that if you get this cheap enough relative to tangible book value, you should buy it. While we have made a similar argument on occasion for different mortgage REITs, at this point in the cycle, we think the risks are just too great to do that.

Source: Q1 Earnings: Shrinking Assets, Expanding Share Counts

AGNC stock is up marginally since then and the total return for once has actually been decent.

Seeking Alpha

Let's look at the just released Q2-2023 numbers and see if there is genuine cause for optimism.

AGNC Q2 2023 Earnings Results

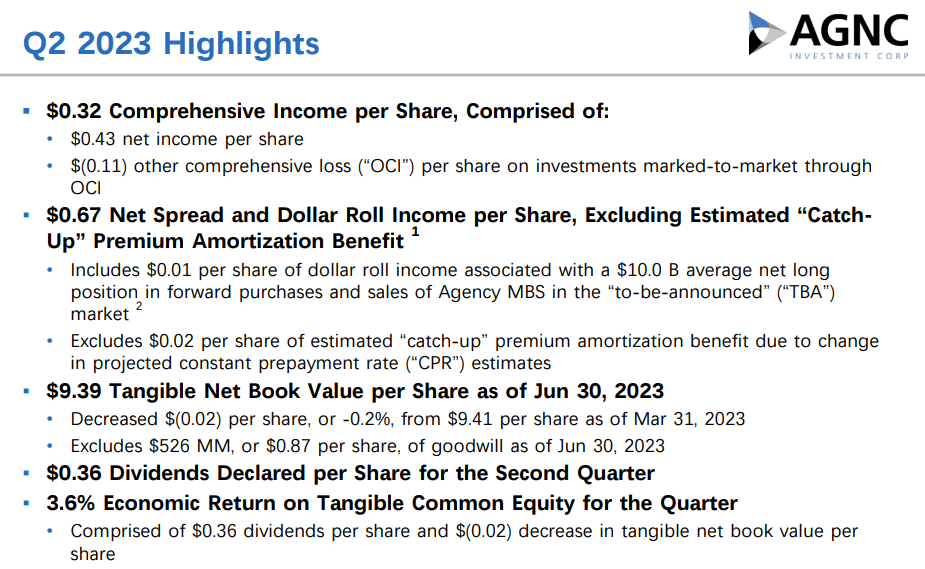

The best information AGNC provides comes in one of the first slides it uses in its presentations. Unfortunately we think investors have over the years gone to great lengths to hide themselves from the truth that AGNC dishes out. We will start by looking at that though.

{kind=link}

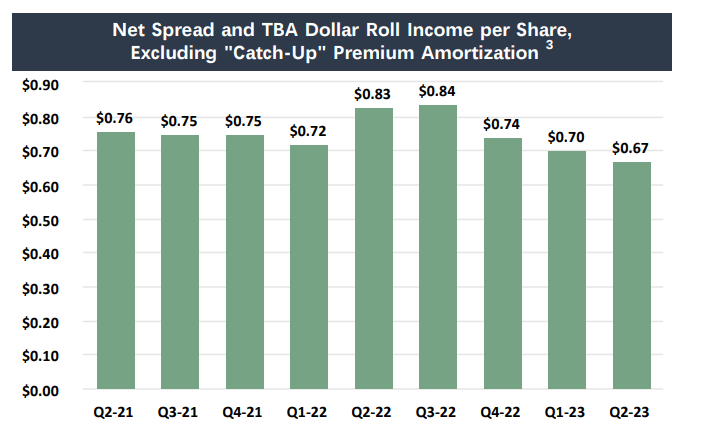

The highlights shown above include the tangible book value, the change in tangible book value and the economic return on tangible common equity. These are the big three which highlight actual, real-world, money making abilities. There is another number on this slide and that is the $0.67 of net spread and dollar roll income. We believe that is about the most useless piece of information you can find. If this number below meant anything, AGNC's book value (and consequently stock price) would be growing by about 40 cents a quarter for the last two years. We derive that by the difference between this number and the dividends paid.

{kind=link}

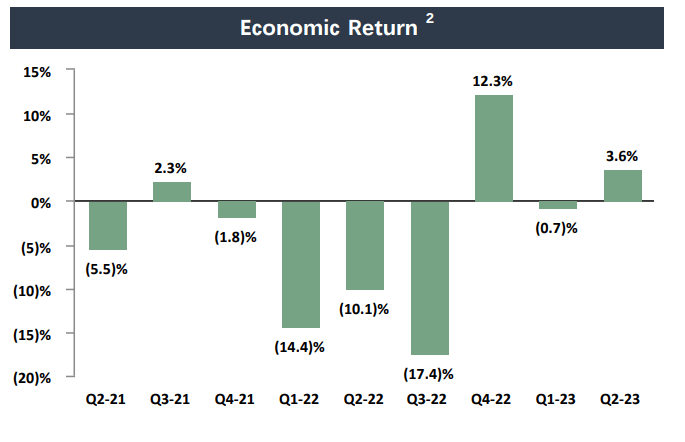

Instead, the economic return shown by AGNC is what most correlates with the stock's total return.

{kind=link}

Ok, so AGNC had an economic return of 3.6% and that is actually one of the better quarters we have seen. In Q1-2023 it was slightly negative.

{kind=link}

For the year 2022, it was a disaster.

{kind=link}

So obviously investors should be happy that we got a good positive number.

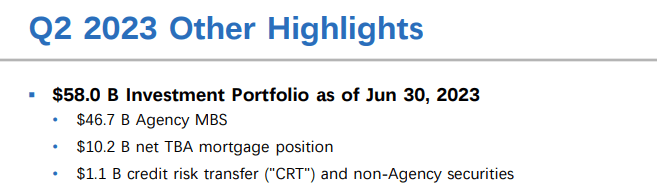

One area that we like to go to next is the investment portfolio. AGNC held $58 billion in investments as of June 30, 2023. As shown below, AGNC continue to take very little credit risk in its portfolio.

{kind=link}

The $58 billion number was a slight expansion from Q1-2023 ($57.2 billion). The portfolio remains far smaller today compared to Q2-2021 ($87.5 billion). We have yet another quarterly report that flies in the face of the idea that mortgage REITs think this is a great time to buy assets.

Q2-2023 Presentation

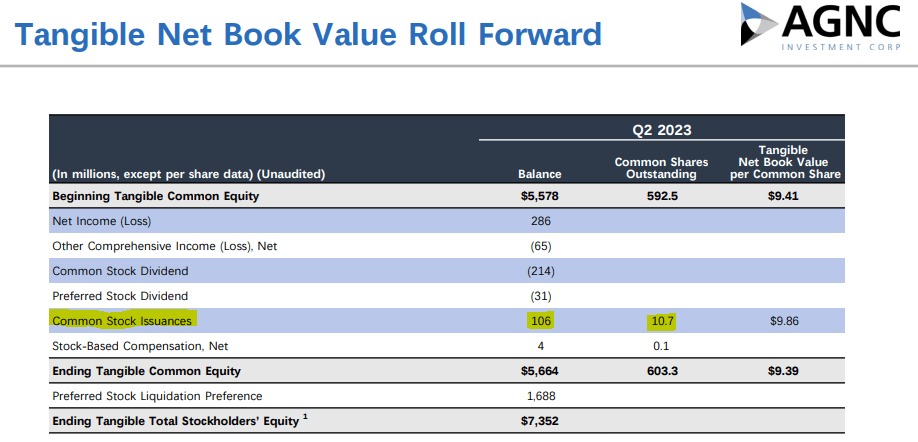

AGNC did make sure investors bought some of its stock though.

{kind=link}

This quarter saw 10.7 million shares issued. Share counts are up about 80 million in the last 12 months (522.7 million to 603.3 million).

Hedges

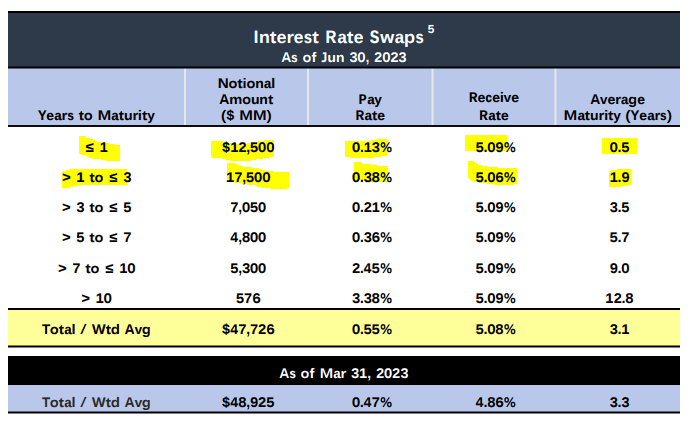

One key reason that AGNC has not done even worse during this era of unprecedented tightening, is the management foresight to lock in low funding rates.

Q2-2023 Presentation

These swaps are incredibly valuable today as you can see the spread between the pay rate and receive rate.

{kind=link}

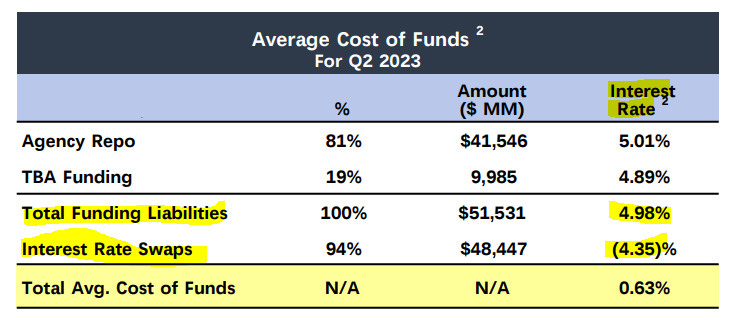

You can see this in the average cost of funding for AGNC slide where the interest rate swaps are creating a big offset.

{kind=link}

There are two crucial things you need to keep in mind here.

1) About 25% of these (weighted average basis) roll off within 6 months.

2) All hedge gains are marked to market. The tangible book value incorporates all these "gains".

Outlook

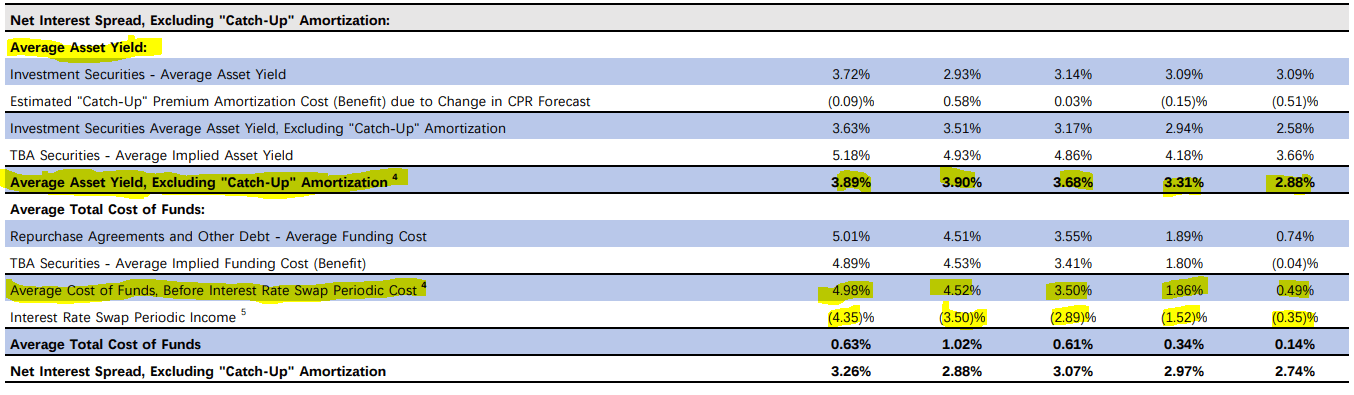

The reason AGNC is selling shares today and has increased share counts by 17% over the last 12 months, is not because the stock is undervalued. The math then is that whatever price AGNC sells enough stock at, ultimately becomes the book value and the price where it will trade in the medium term. The biggest headwind though for the sector is the spread between the asset yield, and cost of funding.

{kind=link}

Asset yields are extremely poor and well below cost of funding. The interest swaps have stepped in to protect income every single quarter, but what happens when they start running out? Everyone always is pricing in the next interest rate cut but you can bet your bottom dollar that the Fed is eyeing this new AI asset bubble with trepidation. Asset bubbles enhance inflation and at least two more rate hikes are very probable at this point. AGNC will face steeply rising costs by early 2024 as hedges get lower. We would look for things to break down in the mortgage REIT space. Despite all the cry about how undervalued mortgage backed securities are, there is really no cure for such an inverted yield curve. Yes, the Fed will likely cut after things really break in the equity markets but we don't want to own a leveraged play into that outcome.

Preferreds

AGNC has 5 listed preferred shares.

- AGNC Investment Corp. 6.12% DP SH PFD F (NASDAQ: AGNCP )

- AGNC Investment Corp. 6.5% DP SH PFD E (NASDAQ: AGNCO )

- AGNC Investment Corp. 6.875% DEP REP D (NASDAQ: AGNCM )

- AGNC Investment Corp. CUM 1/1000 7% C ( AGNCN ).

- AGNC Investment Corp. 7.75% DP PFD G (NASDAQ: AGNCL ).

AGNCN is the most notable here for its yield which is tied to 3-Month CME Term SOFR plus 0.26161%, plus a spread of 5.111%, per annum. So yield on par will now be over 11% very soon. The stock is trading at a slight premium to par ($25.50 as we write this), but the yield is still a very hefty cost to AGNC, so a redemption is quite probable. Some might argue that this is lower than the common equity yield, but that is comparing apples and oranges. Preferred yields should be way lower than common equity yields. Plus common equity yield is not written in stone. Over time all mortgage REIT dividends tend to follow the same path.

Currently none of the preferreds offer a compelling entry point for us. We do own one mortgage REIT preferred but even that is likely to be exited soon.

Paired Trade

While we have been hesitant to go long any mortgage REITs in general, we did get an opportunity for a paired trade in our Marketplace Service as things looked rather extreme at one point from a tangible book value perspective.

CIP Trade

The trade we did do was a short AGNC/Long Dynex Capital, Inc. ( DX ).

CIP Trade Update

We closed out half this morning and are holding on to the other half.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

AGNC Q2 Earnings: A Relatively Solid Quarter