NLY - AGNC: Share Issuance & Asset Sales Continue To Dilute Potential Upside

Summary

- AGNC had a terrible 2022 but Q4-2022 was a significant improvement.

- While tangible book value improved, there were two major actions which reduced potential upside.

- We look at the key takeaways from the results and put to rest the idea that the company is buying mortgage backed securities at great prices.

AGNC Investment Corp. ( AGNC ) certainly gave you an exciting 2022. If you were a champion of the "may you live in interesting times" phrase, AGNC delivered. January was fine, though a head fake where you thought you could sit back and collect dividends. That was followed by the long drawn out remorseless pain which saw you down over 51% at the October lows.

Of course if you bought right at the bottom, you were almost 40% by year end and 53% today.

Good times.

Of course most investors have long touted AGNC for its remarkable dividends. They are not in for the trade, but the buy and hold and to collect dividends. That has been one of the worst exercises you could do in the market over the last decade.

{kind=link}

Buy Upside

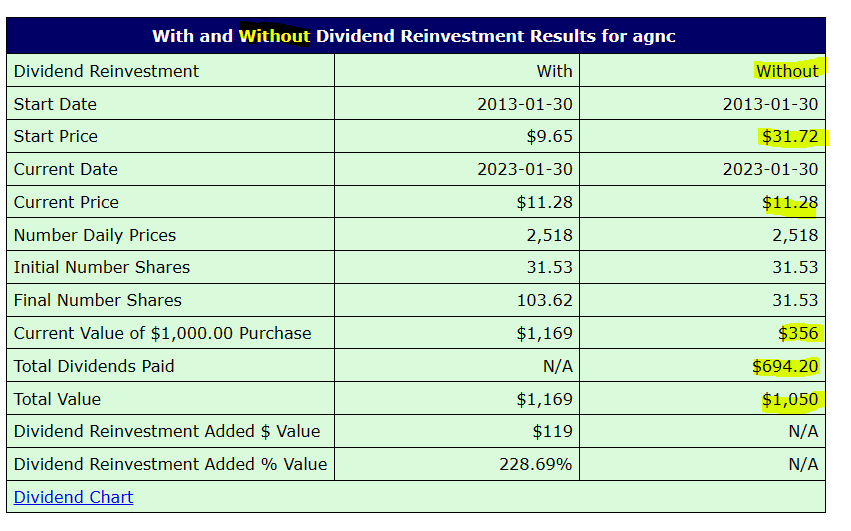

If you bought $1,000 worth of AGNC shares exactly a decade back, here is what happened.

1) Your $1,000 is now worth $356.

2) You got $694.20 of dividends.

3) Your total return was 5%. Not 5% a year. Just 5% total, over 10 years.

4) Your original yield on your investment was 15.76%. AGNC paid $5.00 a share on the $31.72 cost basis. Who wouldn't love that?

{kind=link}

AGNC (AGNC Website)

4) The current dividend is $1.44.

5) The yield on your original investment is now 4.54% ($1.44/31.72). Who could realistically be happy about that?

Those are the facts and they are not in dispute. What usually gets debated is how great an investment AGNC is today. Let's look at that.

Q4-2022

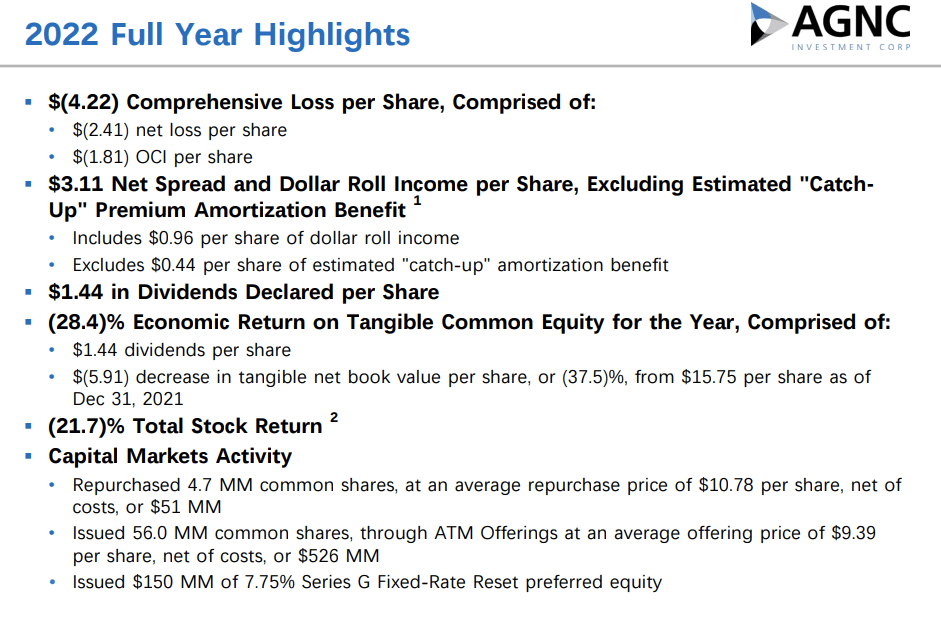

2022 obviously was a harrowing experience for AGNC. With $4.22 of comprehensive loss, investors had little to cheer about.

{kind=link}

AGNC Q4-2022 Presentation

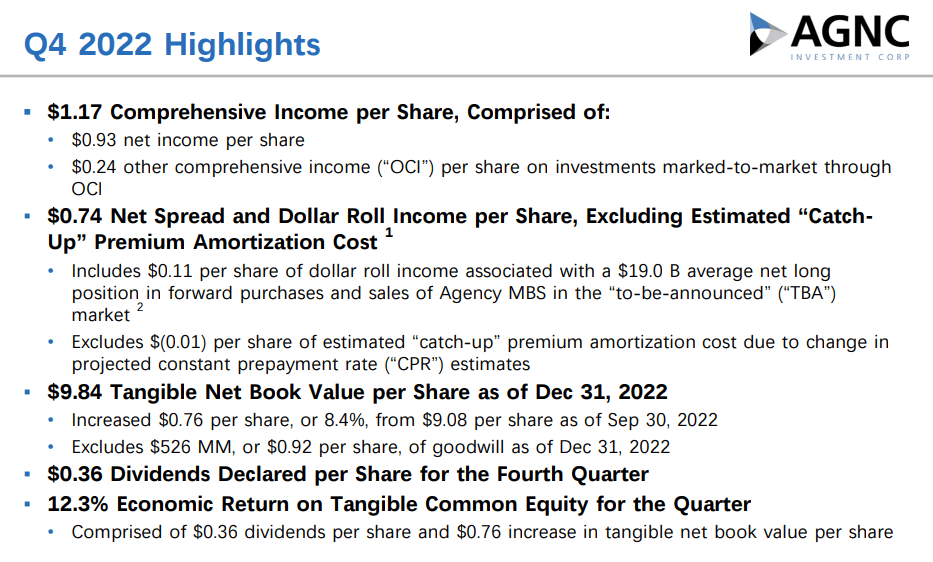

Q4-2022 was better though.

{kind=link}

AGNC Q4-2022 Presentation

Tangible book value increased $0.76 and AGNC delivered 12.3% total return on tangible common equity. What we want to focus on is how the company navigates choppy markets and how that works out for common shareholders.

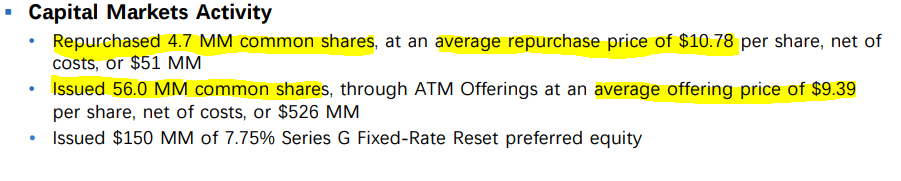

Share Issuance

AGNC issued a ton of shares in 2022. Yes they bought a few, but we will note that they bought 4.7 million at $10.78 and sold 56 million at $9.39 a share.

{kind=link}

AGNC Q4-2022 Presentation

This gets us to our first point that mortgage REITs never care about the absolute value of the share issuance. They only care about it relative to tangible book value.

So if markets tank in 2023 and AGNC's tangible book value is at $7.00 and the stock is at $7.50 they will happily issue new shares. Paradoxically, after that, if the markets rally and AGNC trades at $7.50 while tangible book value is at $9.00, they might buy shares back.

Your Holdings Are Diluted

Contrary to what the bulls say, AGNC is not buying assets at the best possible time. In fact by issuing shares they are doing the opposite. They are diluting your exposure to those assets which are supposed to rebound. If the company has 10% more shares outstanding, then whatever upside is there gets diluted out, by about 10%. Unfortunately for the bulls, AGNC just cannot stop doing that (issuing shares) if it wants to have the right sized equity to liabilities.

AGNC Is Not Just Not Buying , It Is Liquidating Assets

We have heard multiple arguments how this is a great time for agency mortgage REITs to buy. We have heard how this is the best time to "lock-in" spreads between treasuries and mortgage backed securities. Unfortunately we have a thing known as facts and those facts look really different. Below is how AGNC's portfolio has evolved over the last two years.

AGNC Q4-2022 Presentation

Let's zoom in what happened in Q4-2022.

AGNC Q4-2022 Presentation

Assets were reduced by $2.0 billion. Wait, did the bulls not say that assets were being bought?

AGNC needed to do that (sell assets) to get its leverage back under control.

AGNC Q4-2022 Presentation

As you can see above, at risk leverage was at 8.7X at September 30, 2022. So furious share issuance coupled with some asset sales meant that you were back to 7.4X.

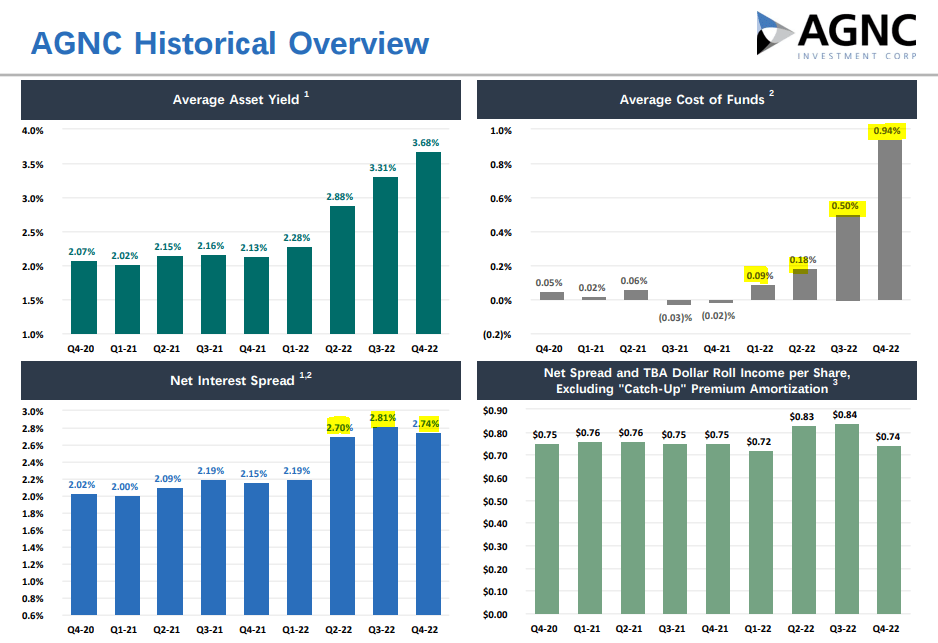

Extremely Low Funding Costs Still Saving The Day

If there is one thing that AGNC deserves credit for, it is for locking in their funding costs when the going was good. Their lock was so extraordinary and for so long, that it continues to allow net interest rate spread to stay steady even now. Average cost of funds was just 0.94% and net interest margin was 2.74%.

{kind=link}

AGNC Q4-2022 Presentation

Compare this to Annaly Capital Management Inc. ( NLY ) from their Q3-2022 results. Note how NLY's spread income collapsed from Q2-2022 to Q3-2022. We should see some more of this in Q4-2022.

NLY Q3-2022 Presentation

AGNC is doing far better in Q4-2022 than what NLY did in Q3-2022! These hedges protect AGNC for now and funding costs will rise slower for them than for any other mortgage REIT that we follow.

Verdict

AGNC's sole bright spot is the lock on funding costs. This should buffer some gyrations for the next 12 months. With low prepayment rates, AGNC will not be able to navigate to significantly higher coupon rates over the next 12 months. The stock also trades very expensive to tangible book value. Investors must keep in mind the total returns shown above are after that tremendous rally off the lows. AGNC like the mortgage REIT sector as a whole, is a poor generator of total returns. In general, if someone wants to get involved with this sector, our choice is to stick with the preferred shares. In case of AGNC, we don't like the preferred to common equity ratio , although it has improved thanks to the massive common share issuance. We rate AGNC a hold at this point and would move to a Sell rating over $12.50.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

AGNC: Share Issuance & Asset Sales Continue To Dilute Potential Upside