AEM - Agnico Eagle: An Industry Leader For Reserve Growth Per Share

2023-03-30 09:43:57 ET

Summary

- Agnico Eagle has been one of the worst-performing gold miners year-to-date, underperforming the GDX by 1200 basis points with softer FY2023 guidance than anticipated.

- While this underperformance has frustrated many investors, especially as it overshadowed a year of over-delivering on synergies and incredible exploration results, it hasn't changed the investment thesis.

- This investment thesis is backed by one of the largest reserve bases globally (largest when adjusting for only Tier-1 jurisdiction ounces), and continued growth in per share metrics.

- Given Agnico Eagle's position as a senior producer with an attractive dividend yield, meaningful production growth on deck (assuming no divestments), and strong margins, I would view sharp pullbacks as buying opportunities.

The Q4 Earnings Season for the Gold Miners Index ( GDX ) is ending, and reserves & resource update season is well underway, with several reports trickling out over the past month. One of the first companies to release its updated Reserve & Resource statement was Agnico Eagle ( AEM ), which grew its total reserves for the third consecutive year, and looks to be on track for another year of reserve growth with East Gouldie ounces being converted, a tailwind from increased ownership in Canadian Malartic (50% --> 100%), and the potential inclusion of Wasamac into reserves (Yamana acquisition). Although this growth still left Agnico in the #5 spot globally, but the #1 spot among gold producers for Tier-1 jurisdiction ounces (Canada, United States, Finland, Australia). Let's look at its FY2022 reserve update below:

2022 Reserves

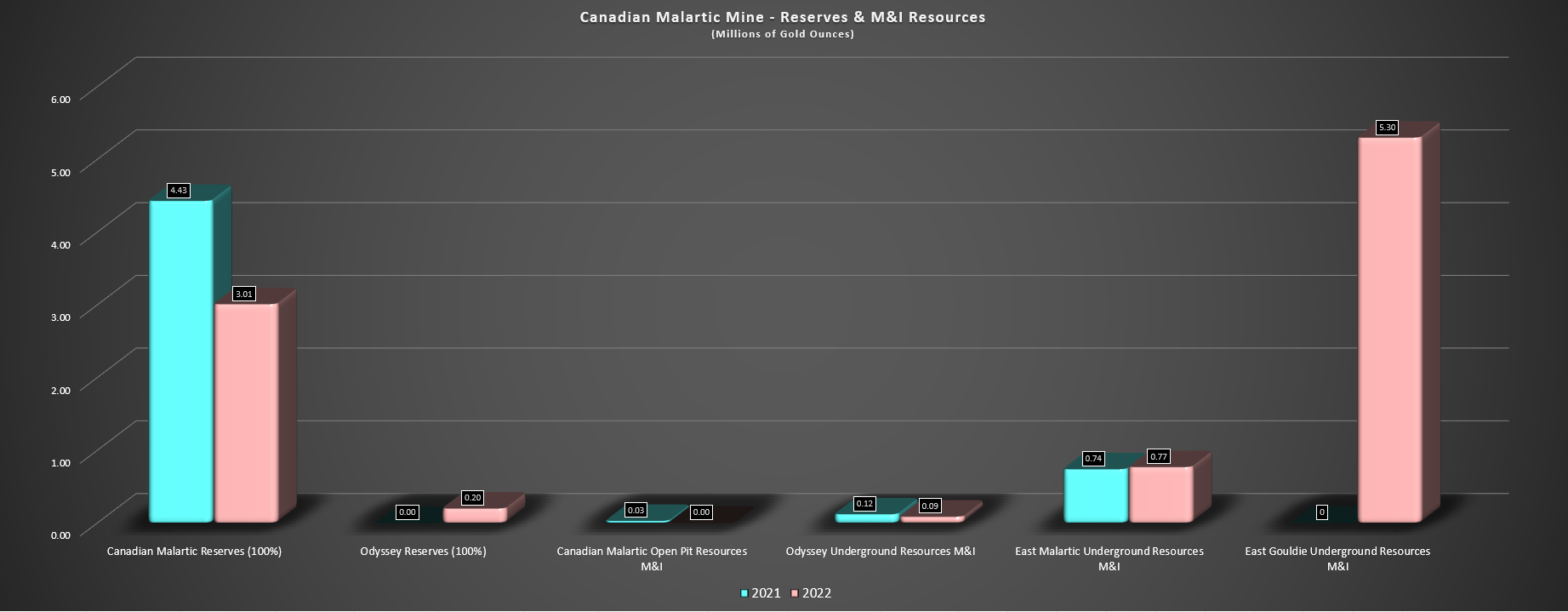

Agnico Eagle released its FY2022 Reserve & Resource update last month, reporting 9% growth in its global mineral reserves to ~48.7 million ounces, up from ~44.6 million ounces in the year-ago period. This was driven by a considerable increase in reserves at its newly owned Detour Lake Mine in Ontario, Canada, which finished the year with a massive 20.7 million ounce reserve base at a grade of 0.76 grams per tonne of gold. Unfortunately, this was partially offset by a moderate decline in reserves at several other assets (LaRonde Complex, Meadowbank Complex, Pinos Altos, La India, Fosterville), and a marginal decline at Kittila. That said, this reserve figure doesn't paint a complete picture, especially following consolidation of Canadian Malartic [CM].

{kind=link}

Canadian Malartic - Reserves & M&I Resources (100% Basis) (Company Filings, Author's Chart)

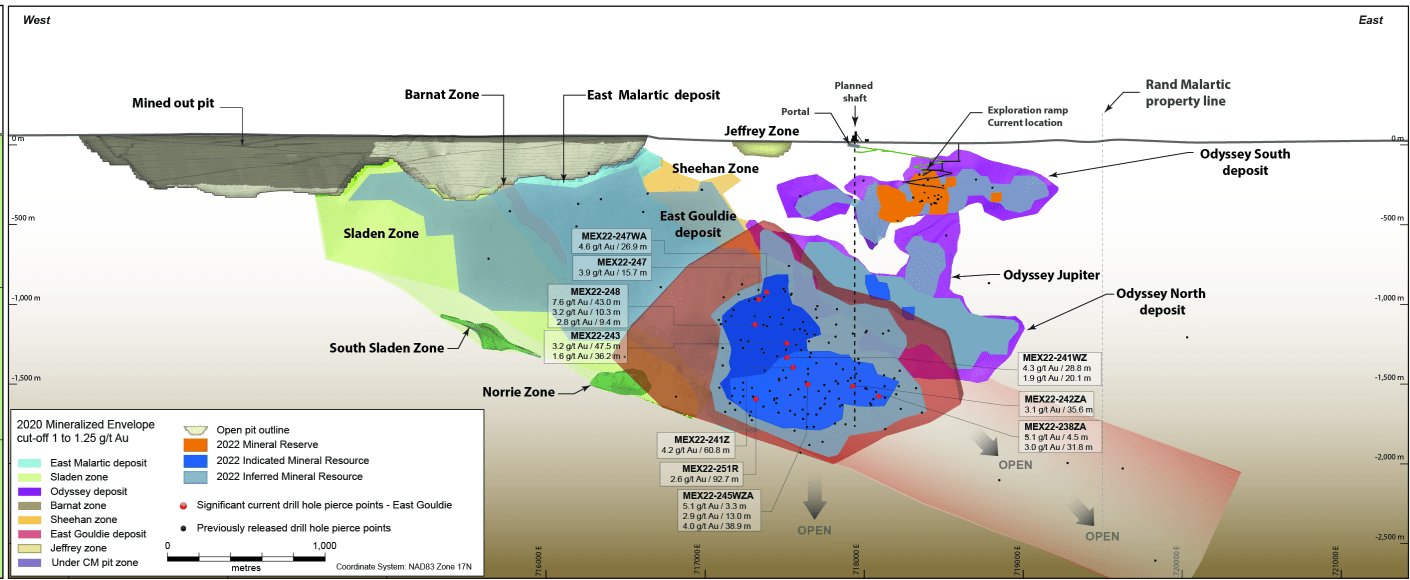

As shown above, CM is home to just ~3.2 million ounces of reserves on a 100% basis (as of year-end 2022 Agnico Eagle had ~1.55 million ounces of these ounces in its attributable reserves before the Yamana deal closing), but this asset has a total resource base (reserves, M&I resources, and inferred ounces) of ~18.6 million ounces currently. While the bulk of the 2022 reserve figure (~3.0 million ounces on 100% basis) will see further depletion as ounces get mined out of the open pit and are not replaced, there is a massive M&I inventory at East Gouldie which will move into reserves, and additional successful conversion ahead from other zones at Odyssey. Plus, Agnico will go from having 50% ownership in the reserves to 100%, a tailwind because of its acquisition of Yamana's Canadian assets (other half of CM and Wasamac).

{kind=link}

Canadian Malartic - Exploration Success & Eastern Extension of East Gouldie (Company Website)

Although it's not yet clear whether Wasamac will enter reserves at year-end 2023 or year-end 2024 (given that Agnico is treating this as a historic resource for now), this would add another 2.0+ million ounces to Agnico's reserve base at grades (2.50 grams per tonne of gold) that are 70% higher than its current reserve grade of 1.51 grams per tonne of gold. So, when we combine the benefit of a 50% increase in ownership at CM, the addition of Wasamac to reserves in coming years, and what appears to be a high likelihood of further reserve growth at Detour (West Pit extensions, Detour Underground), further reserve additions at Hope Bay and massive step-outs east of East Gouldie, there is a clear path to Agnico growing reserves by another 20% later this decade to ~55.0+ million ounces, assuming it doesn't divest any non-core assets, and even without including the San Nicolas partnership with Teck Resources ( TECK ).

In fact, Agnico Eagle could ultimately prove up over 30.0 million ounces of reserves between Detour Lake and Canadian Malartic alone, just two assets of its nearly a dozen assets in its reserve base that sit ~500 kilometers from each other in Ontario and Quebec, Canada.

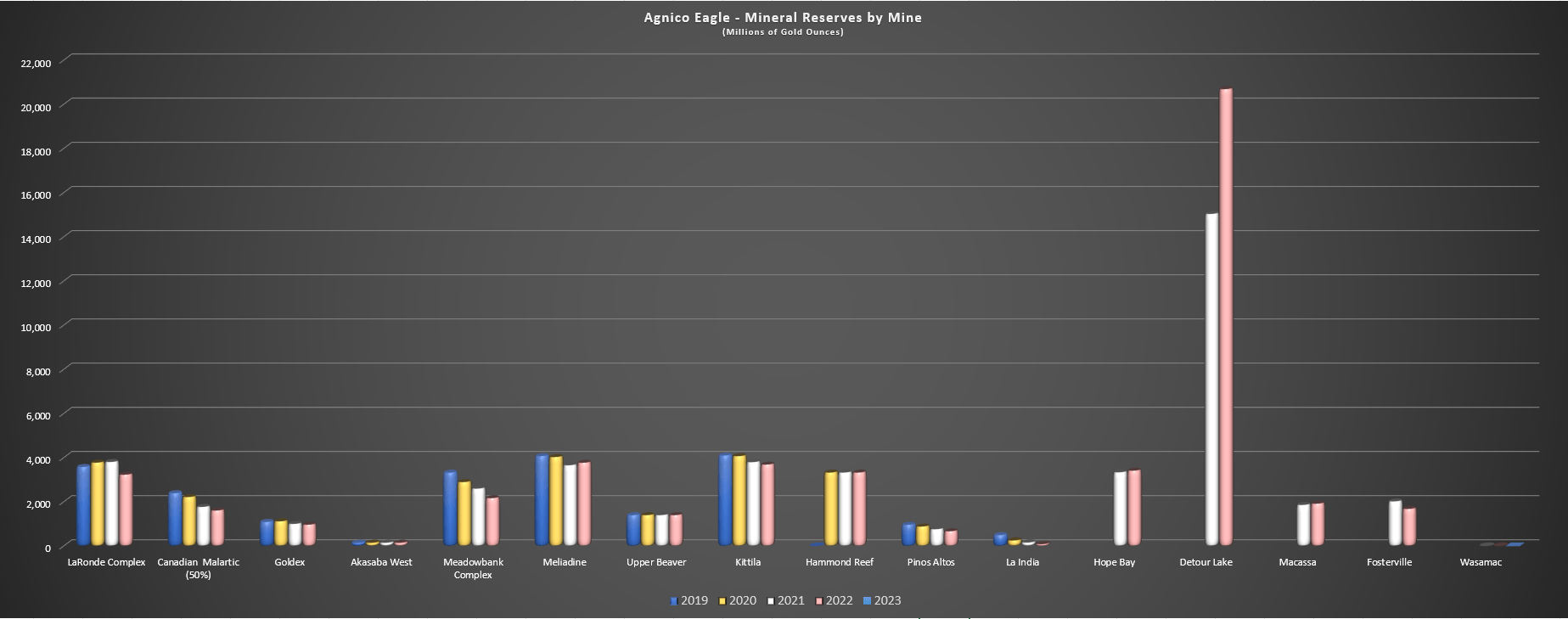

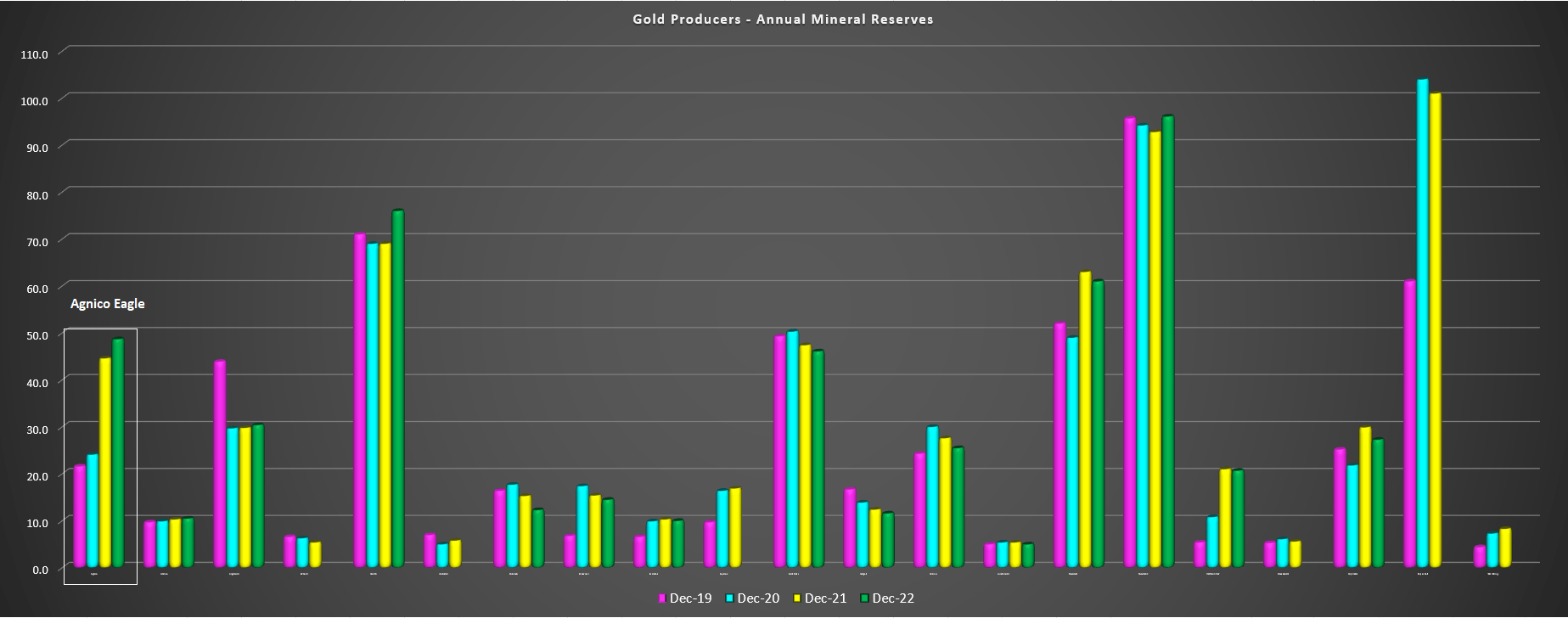

As for its reserve calculations, Agnico maintained its very conservative gold price assumption of $1,300/oz for calculating reserves in a year when many other companies revised their reserve price assumptions. This included Newmont ( NEM ) moving to $1,400/oz, Gold Fields ( GFI ) moving to $1,400/oz, and Kinross ( KGC ) moving to $1,400/oz. The only negative about the reserve update is that while Agnico has double reserves at its top-2 assets, it has achieved the bulk of the reserve growth since 2020 through M&A (addition of Detour Lake, Macassa, and Fosterville) and while it certainly did the deal at the right price, I would have preferred to see more reserve additions at other key assets like Meadowbank/Amaruq, Fosterville, LaRonde, and Macassa, which have struggled a little to replace reserves (especially at the same grades), as shown by the trend in reserves below.

{kind=link}

Agnico Eagle - Mineral Reserves by Mine (Company Filings, Author's Chart)

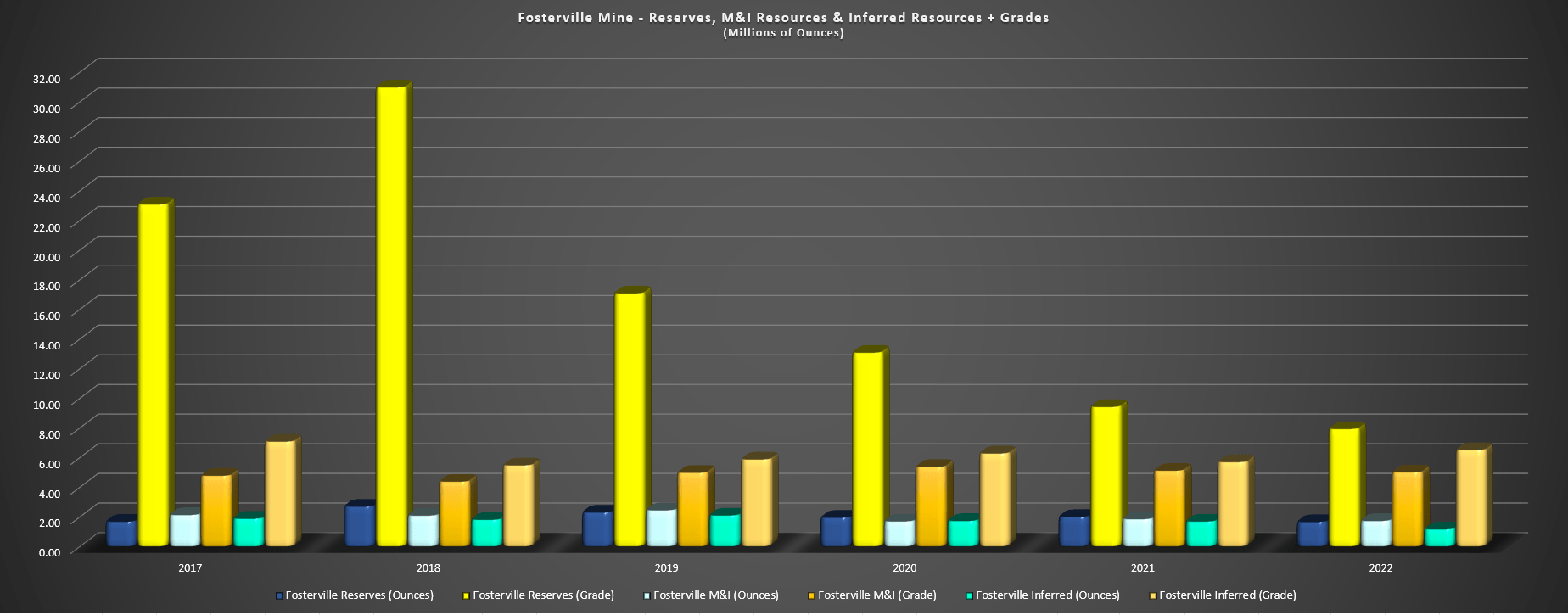

By far the most disappointing has been Fosterville, which continues to see some promising results, but less robust results and additions than I hoped, given the $120 million thrown at the asset in the past two years in exploration. Since peak reserve grades in 2018 (31.0 grams per tonne of gold), reserve grades have slid to 7.95 grams per tonne of gold, and total ounces have declined by ~30% to 1.68 million ounces of gold. This sharp decline in reserves is despite the addition of Robbins Hill, which has helped to buoy the declining reserve base and it's despite relatively aggressive exploration budgets to make a new major discovery.

{kind=link}

Fosterville Mine - Reserves, M&I Resources & Inferred Resources + Grades (Company Filings, Author's Chart)

Although there are meaningful ounces in the M&I and inferred category (2.93 million ounces combined), they aren't sitting much above the upper end of the 2.0 to 5.4 gram per tonne cut-off grade with M&I grades of 5.03 grams per tonne of gold, and inferred grades of 6.53 grams per tonne gold. Plus, I imagine because of inflationary pressures and the recent operating constraints (lower mining rates due to not being able to operate surface fans for one-fourth of operating hours per day) that cut-off grades have increased materially. Hence, while there's a lot to like about the exploration success at several assets (Detour Lake, CM, Hope Bay, Meliadine), the future is less clear for Fosterville post-2025.

The good news is that while this is by far Agnico's lowest-cost asset with total cash costs of $357/oz in FY2022 (40% below the closest comparable of Detour Lake at $657/oz), Agnico is seeing production growth in other key low-cost assets like Detour Lake (potential for 900,000+ ounces per annum). Plus, Fosterville is part of a much larger portfolio today and represents barely 10% of Agnico's annual production (2022 figures). So, while this sharp decline in grades combined with operating constraints would have been a serious blow for Kirkland Lake, where this would have represented ~30% of annual production. So, while there's lots of animosity towards the Kirkland Lake/Agnico deal, I think Kirkland Lake's CEO Tony Makuch did a solid job given that investors enjoyed a 2000% return in just a few years before Fosterville's outlook became less robust.

Some investors might argue that Detour Lake was only getting better and Macassa is still an incredible asset, and while I don't disagree, I don't know if those two assets plus a less clear future for Fosterville could have supported a $10.0+ billion valuation. Obviously, it's not yet time to count out Fosterville entirely and having the sector driller working to make a new discovery or add half-ounce per tonne material at the world's previously highest-grade gold mine is a great setup. That said, between operating constraints that impact mining rates (temporary because of Victoria Government EPA) and much fewer ounces being added than I hoped per million spent in exploration budgets, I've gone from optimistic to only cautiously optimistic on Fosterville.

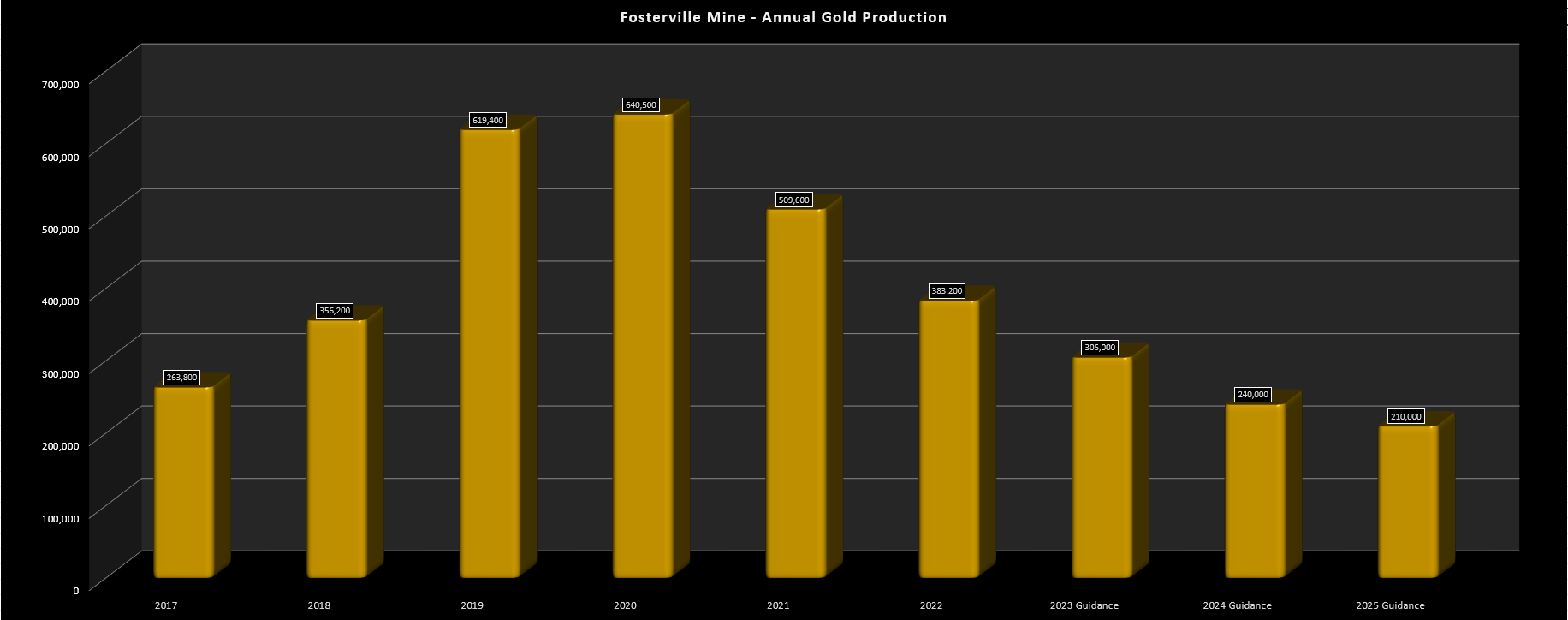

The silver lining is that with a much lower production profile, it will get easier to replace depleted ounces with this asset depleting ~600,000+ ounces per year in its prime (2019, 2020).

{kind=link}

Fosterville Mine - Annual Production & Three Year Guidance (Company Filings, Author's Chart)

As shown in the chart above, Agnico's guidance points to average three-year production (2023-2025) of 251,700 ounces, a significant decline from trailing three-year average production of 511,100 ounces. The declining output is mostly related to grades normalizing, given that the 1.0+ ounce per tonne ore at the Swan Zone certainly wasn't going to last forever, but it's also impacted by lower than planned mining rates because of operating constraints (lower mining rates related to the Victoria EPA disallowing the use of surface fans from midnight to 6:00 AM due to low frequency noise ). The operating constraints being resolved and the 2023/2024 exploration program will be key to Fosterville's future, as it might be tougher to justify throwing ~$25 million at this asset per year if neither are meeting expectations (resolution, new discoveries).

2023 Plans

Looking ahead to 2023, Agnico Eagle has a ~$328 million budget for exploration and project expenses, including ~$143 million in expensed exploration, ~$123 million in capitalized exploration, and ~$62 million in project studies/other expenses. The assets seeing the lion's share of exploration dollars are Detour Lake, Hope Bay, CM, Fosterville, and Macassa. At Detour Lake, $29.4 million of $33.2 million will focus on near-mine drilling (Saddle, West Pit, potential underground opportunity) with the rest used to test regional targets. At Macassa, $18.4 million will be spent to upgrade mineral resources, with $1.2 million to test extensions of targets at the South Mine Complex. In addition, Agnico has budgeted $9.4 million to compile all historical information on the Kirkland Lake Camp for target generation, with plans to complete an 8,000 meter drill program.

{kind=link}

Detour Lake Mine Exploration Success (Company Website)

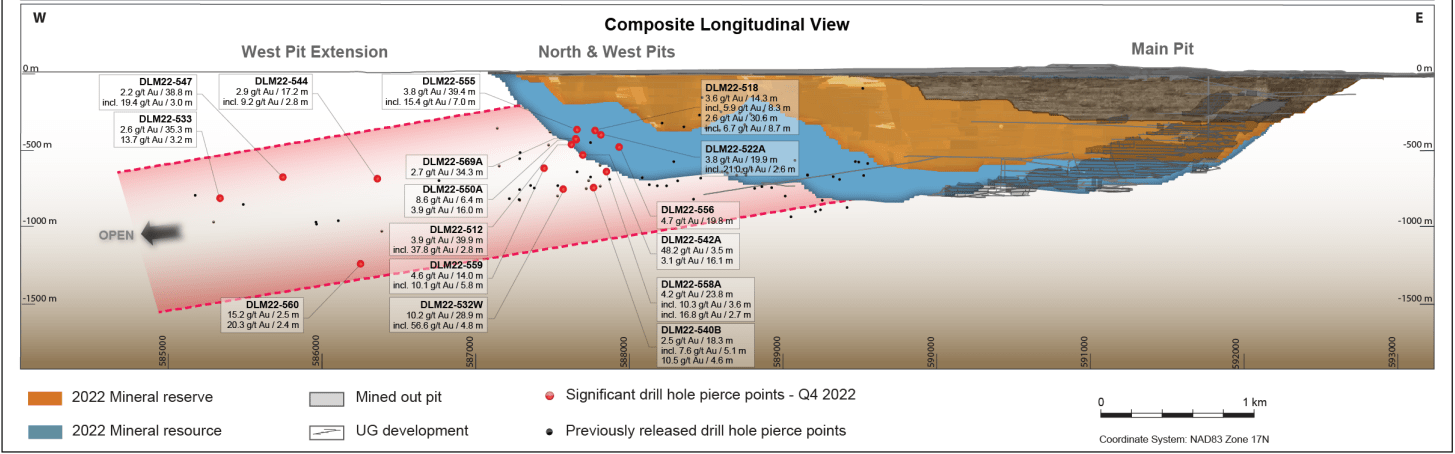

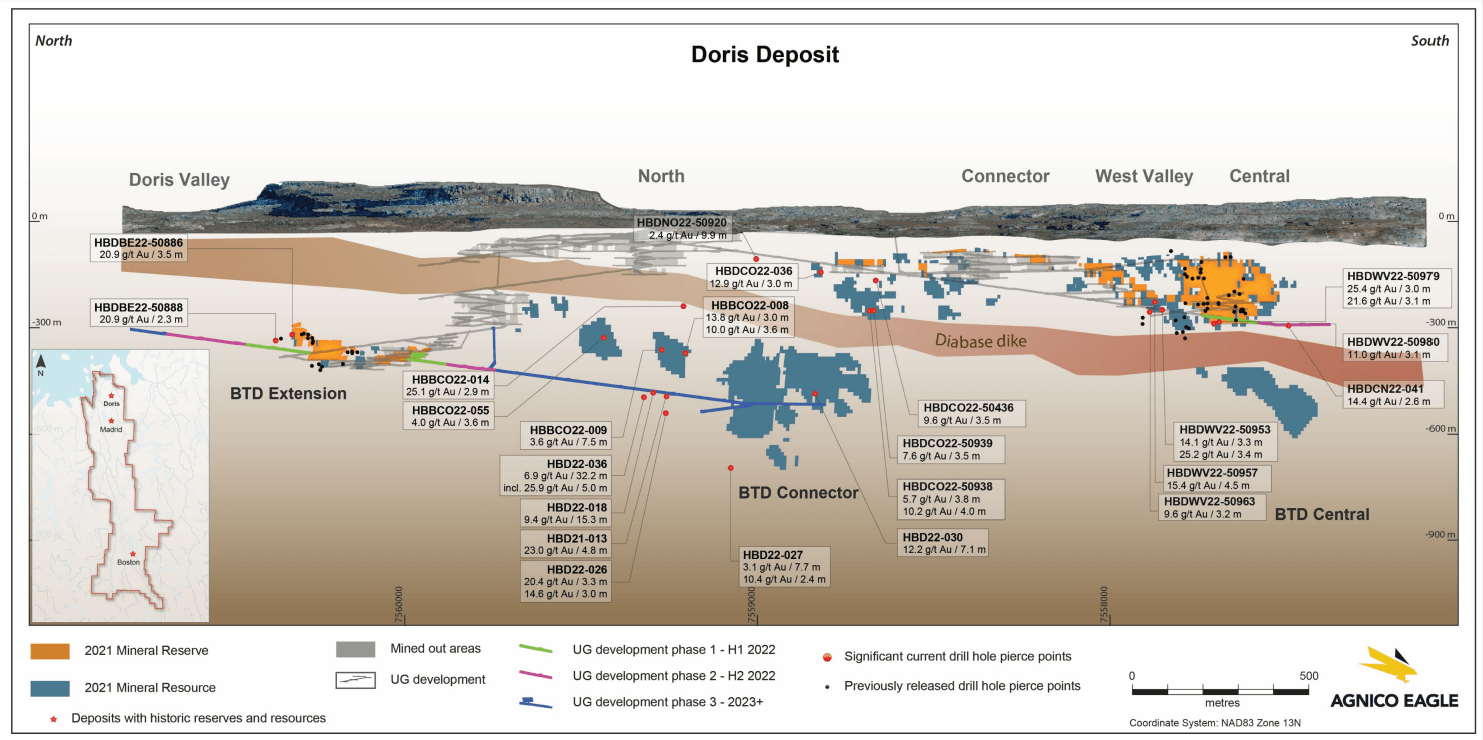

Moving east to CM, Agnico is planning another busy year of exploration at Canadian Malartic with $21.8 million expected to be spent. This includes $11.8 million on near-mine targets and $10.0 million on semi regional targets that could contribute to future feed, like Camflo and targets on the East Gouldie and Barnat corridors. As for Hope Bay in Nunavut, Agnico continues to have an aggressive budget with $30.6 million planned, owing to the success of last year's drill program, with multiple high-grade intercepts in the West Valley Zone, on the northern edge of the BTD Extension zone, and below the dike in the BTD Connector zone, including a deep hole (~600 meters below surface) that hit 3.3 meters at 20.4 grams per tonne of gold.

{kind=link}

Hope Bay Project - Doris Deposit (Company Website)

Finally, moving to Fosterville, the asset is seeing a material decline in exploration dollars from 2021 (Kirkland Lake) and 2022 levels (Agnico), with $20.8 million for capitalized drilling, $4.4 million for underground and surface exploration, and $1.3 million for regional drilling. This compares to $34.6 million last year (albeit higher due to developing exploration drifts), $19.7 million on underground and surface exploration, and $2.9 million for regional exploration. That said, this is still a top-5 exploration budget company-wide, but the company is certainly directing more dollars to its largest two mines (and areas around them) that could ultimately be 900,000-ounce plus per annum operations. This makes complete sense given that there's the potential for these assets to produce well into 2040s, while Fosterville's future is less clear post-2025, especially if the operating constraints remain in place.

Given the expectation to add considerable mineral reserves in 2023 and 2024 from East Gouldie and other underground zones at Odyssey (Canadian Malartic Underground) as ounces are converted (plus adding the other 50% of CM), plus the potential to declare initial mineral reserves at Wasamac at year-end 2023 or year-end 2024 and continued exploration success at Hope Bay, I would expect the trend to be higher for reserves and inferred resources over the next few years. So, while Agnico Eagle may be slightly behind smaller producers like Newcrest and neck and neck with Gold Fields, I see a strong likelihood of increasing its lead relative to Gold Fields by 2025 (helped by winning the Yamana deal) and continuing to keep pace with Newcrest, which is also enjoying exploration success at several key assets (Havieron, Red Chris, Brucejack).

The Most Important Metric

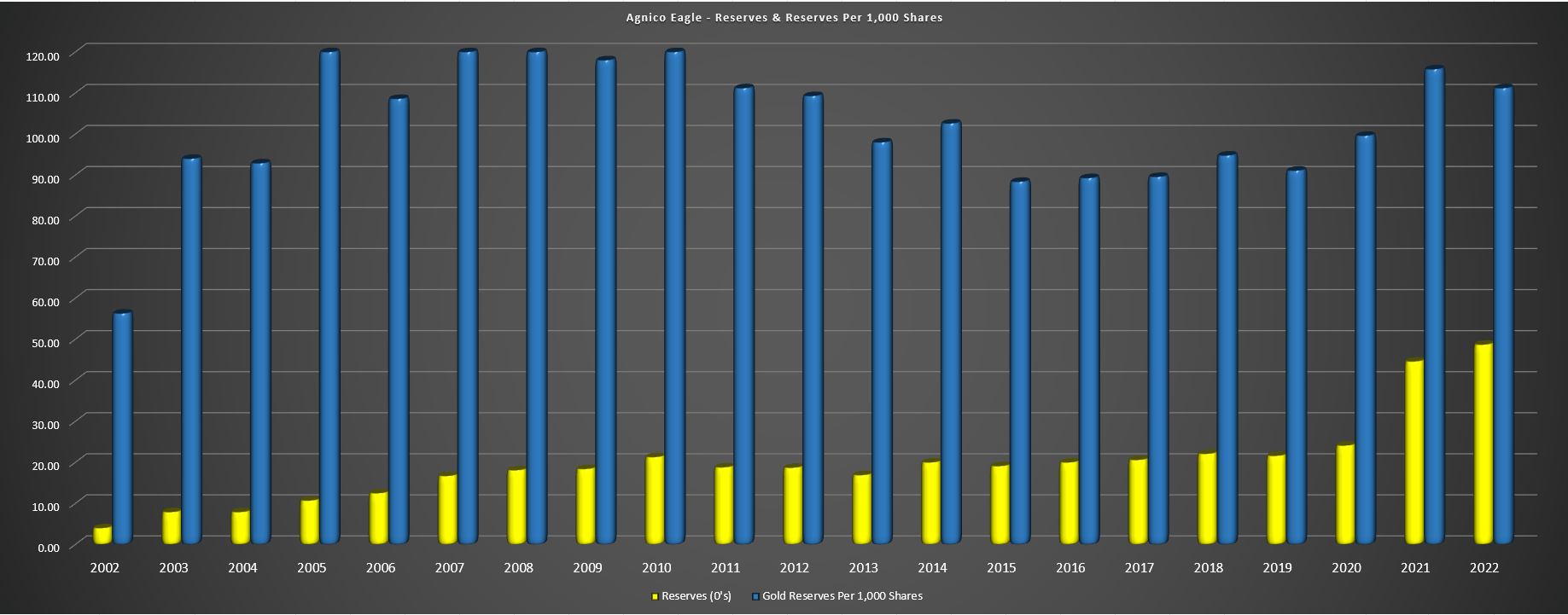

Agnico Eagle has done an incredible job growing its reserve base by ~1100% from ~4.0 million ounces to ~48.7 million ounces over the past two decades (2002 to 2022) despite considerable depletion as it's grown into one of the world's largest producers. This has been accomplished by focusing on exploration, a regional strategy that has allowed it to leverage off existing infrastructure and have a competitive advantage, and rigid capital discipline not to waste a single dollar on assets in unsafe jurisdictions or those that might not pan out.

Key wins have included incredible reserve replacement at LaRonde, building a massive production profile in Nunavut through the acquisition of Cumberland and Comaplex, coming over the top of Goldcorp to scoop up half of Canadian Malartic, and a merger of equals with Kirkland Lake to add Detour Lake and bolster its land position in the Kirkland Lake Camp. Other notable moves have included scooping up Kittila with its acquisition of Riddarhyttan Resources for just $150 million in the early innings of a new bull market for gold in 2005, and recent moves to ensure it has the resources to take advantage of 42.0+ million tonnes of excess processing capacity by 2028 at the LaRonde Complex and Canadian Malartic.

{kind=link}

Agnico Eagle - Gold Reserves & Reserves Per 1,000 Shares (Company Filings, Author's Chart)

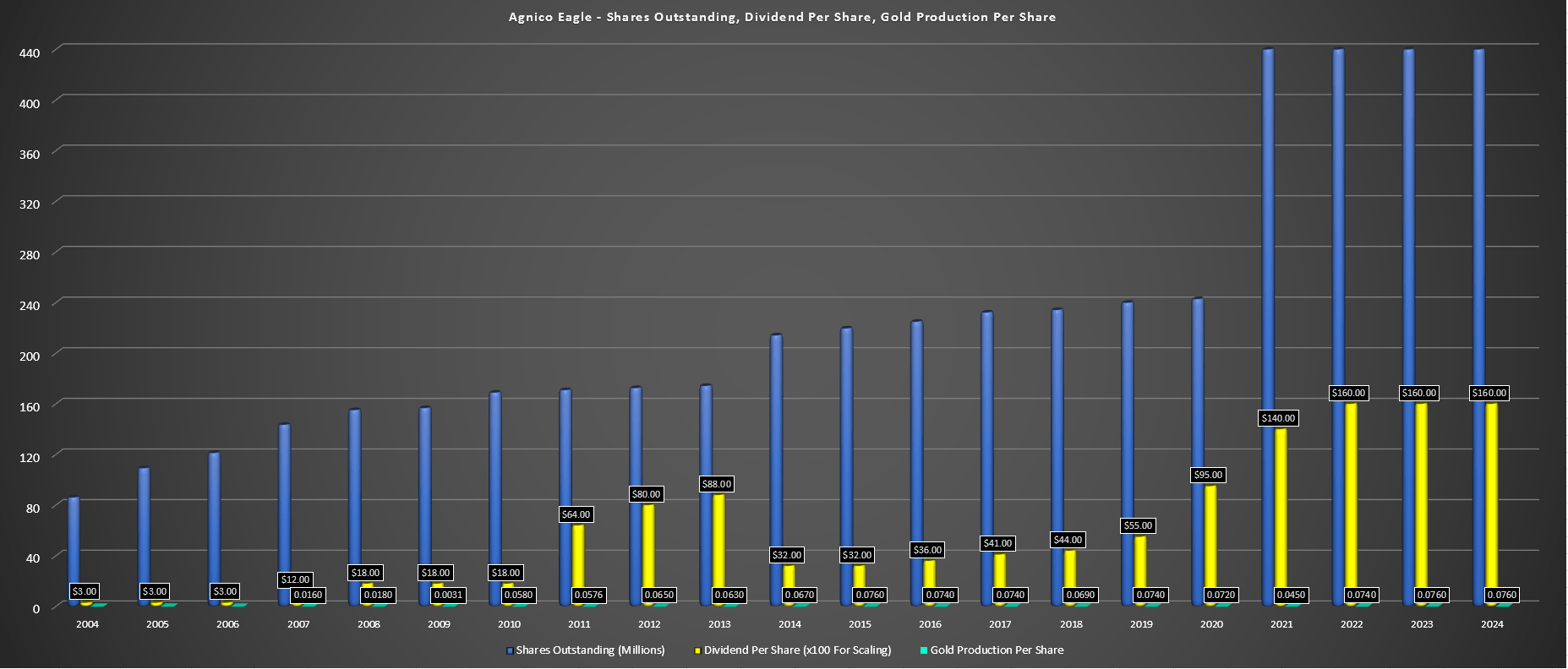

However, while reserve growth is great, the key for investors and the one metric they should look at is reserve growth per share, as well as production growth per share, and net asset value per share. In Agnico's case, the company continues to excel in these instances, with investors enjoying increases gold ownership for every share they own. The evidence is in total reserves growing from 4.0 million ounces to 48.7 million ounces and having a path to 55.0+ million ounces of gold (~14x growth if 55.0 million ounces of reserves achieved later this decade) while the share count is up less than 7x in the period from to ~490.0 million shares (Yamana acquisition closing) vs. ~71.0 million shares in 2002. This is not the case with other producers that have overpaid and have bloated share counts, like Kinross with Red Back Mining, Great Bear, and Aurelian.

{kind=link}

Agnico Eagle - Production Growth & Dividends Per Share (Company Filings, Author's Chart)

Just as importantly, Agnico Eagle has a sound track record of returning this capital to shareholders and we can see in the above chart, production and dividends per share continue to grow. In fact, Agnico Eagle has seen its dividend increase 50x over the past two decades ($0.03 to $1.60). This compound annual growth rate is in line with Apple ( AAPL ) and is just behind Starbucks ( SBUX ) which is nothing short of incredible for a depleting business that must constantly be replacing reserves in a world where major discoveries are becoming more difficult. I attribute this to its regional strategy and its rigid discipline under Sean Boyd and its new CEO, Ammar-Al Joundi, where they only make big bets when the risk is low, such as scooping up half of an asset they already know intimately last year, Canadian Malartic.

Valuation

Based on ~490 million shares (post-Yamana acquisition) and a share price of $52.20, Agnico Eagle trades at a market cap of ~$25.6 billion and an enterprise value of ~26.2 billion, making it the third-largest gold producer by market cap, just behind Barrick Gold ( GOLD ), and the fourth-largest precious metals name, with Franco-Nevada ( FNV ) just ahead of Agnico at a ~$28.0 billion market cap. At first glance, Agnico's valuation might seem rich relative to peers like Newmont ( NEM ) at ~$38.7 billion and Barrick at ~32.0 billion, given that both are larger producers with much larger reserve bases. However, Agnico Eagle deserves to trade at a premium for several reasons, which are:

- glowing track record of growth in per share metrics

- position as the only gold producer with a 2.0+ million production profile with ~90% of production from Tier-1 jurisdictions

- industry-leading margins with AISC likely to remain below $1,100/oz post-2023

- an enviable development pipeline with several projects (San Nicolas [50%], Santa Gertrudis, Hammond Reef), and many that could leverage off existing infrastructure (Upper Beaver, Kirkland Lake Camp, Wasamac, Hope Bay)

{kind=link}

Senior & Intermediate Gold Producers by Reserves (Company Filings, Author's Chart)

Based on what I believe to be a fair multiple of 12.5x cash flow (a slight premium to its 10-year average of ~12.1) and FY2023 cash flow per share estimates of $4.98, I see a fair value for Agnico Eagle of $62.25. If we add in a value of $4.2 billion [$8.55] for its development portfolio, this translates to a fair value of US$70.80. This represents a 36% upside from current levels or closer to 38% total return when including its annualized dividend. That said, I am looking for a minimum of a 35% discount to fair value to justify starting new positions, pointing to an ideal buy zone of US$46.00 or lower for AEM. This doesn't mean that the stock must drop to these levels, but I don't see a low-risk buying opportunity here, even if the stock is more attractively valued than some of its peers like Newmont or Newcrest ( OTCPK:NCMGF ).

{kind=link}

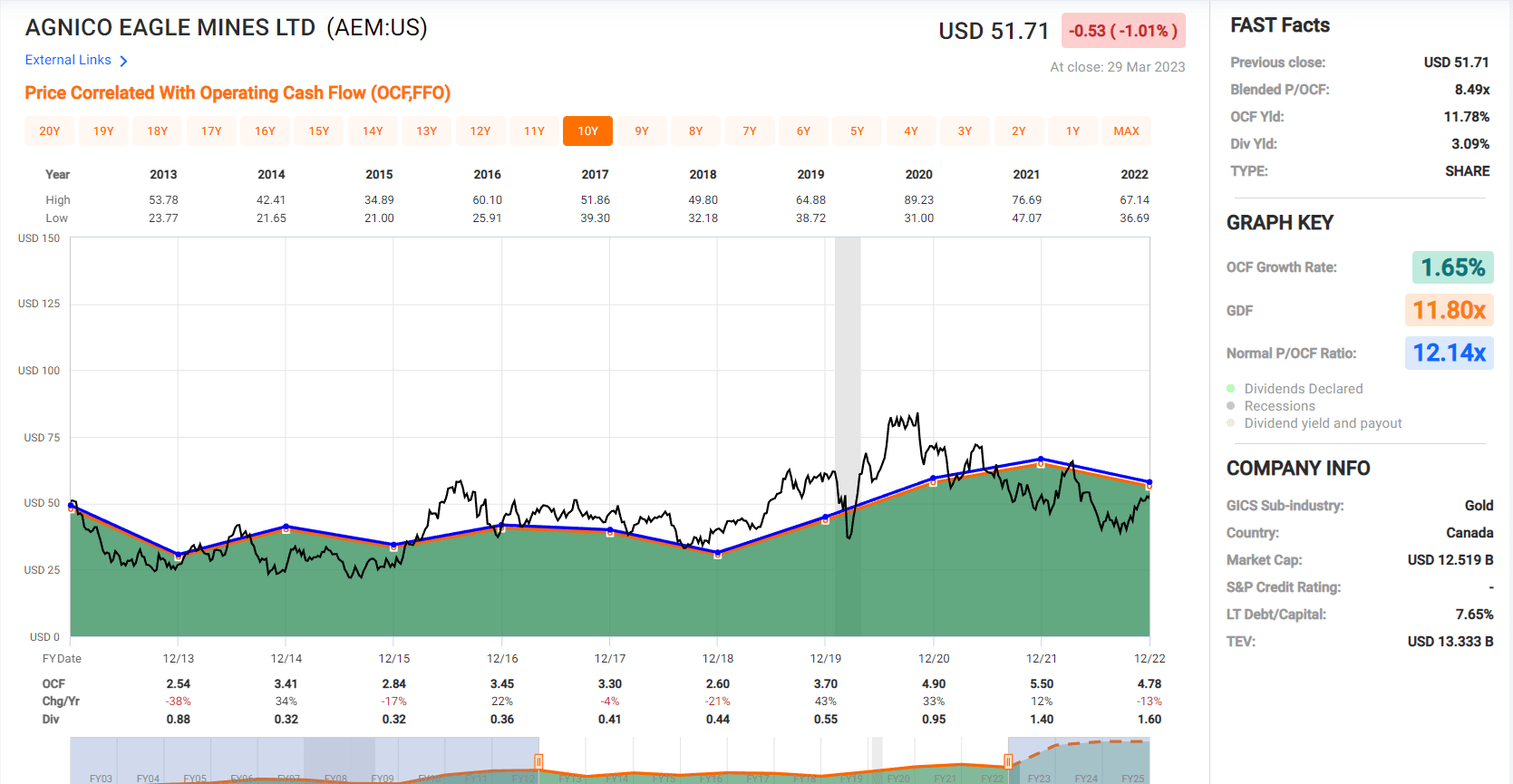

Agnico Eagle - Historical Cash Flow Multiple (FASTGraphs.com)

Summary

Agnico Eagle is undoubtedly a top-5 gold miner sector-wide, and one of the few gold producers out there that one can tuck away in one's portfolio as a core position. This is because it has rigid capital discipline (no stupid M&A), it continues to grow its per share metrics while maintaining a tight share structure, and it operates some of the best assets in the top mining jurisdictions globally. That said, I prefer to buy or add to miners only when they're trading at a deep discount to fair value and ideally when sentiment in the sector is in the gutter. So, while I remain long Agnico and it remains one of my largest positions, I don't see this rally above US$52.00 as a low-risk buying opportunity.

For further details see:

Agnico Eagle: An Industry Leader For Reserve Growth Per Share