AEM - Agnico Eagle: Asymmetric Bet On Gold With Capped Downside Using LEAPS Options

2023-09-11 23:45:04 ET

Summary

- Agnico Eagle is one of the largest gold miners in the world owning primarily tier-one assets, located in the safest jurisdictions: Canada, Australia, Finland, and Mexico.

- The company's financials are strong. Agnico has adequate liquidity to cover its expenses and excels on all profitability metrics compared to its peers.

- I give Agnico Eagle a strong buy rating due to its superb portfolio, experienced management, and low price relative to NAV.

- In my portfolio, I own a LEAPS calls on Agnico. They provide a significant asymmetry of the bet, at average one to five, i.e., I risk one dollar to get at least five. The available options are still cheap, measured in implicit volatility.

Thesis

Agnico Eagle ( AEM ) owns mostly tier-one assets in tier-one jurisdictions. This is an indisputable advantage. In the mining business, having such assets means you have a moat. Tier one mines have higher grades than average, with enough reserves for at least ten years at an annual production of 500 thousand ounces. Higher grades mean lower AISC, hence lower cut-off grades even at declining spot prices.

The company has a robust balance sheet with sufficient liquidity and solvency. Agnico's profitability metrics are better than the industry's average and the company`s five-year average. The country risks are almost nonexistent due to the mine's location in Canada, Australia, Mexico, and Finland.

I give Agnico Eagle a strong buy rating due to its superb portfolio, experienced management, and low price relative to NAV.

Gold supply destruction

I am long gold. The reasons have been widely discussed. The gold supply cliff , the monetary base expansion, and the rising global uncertainty will drive long-term price discovery. The gold supply cliff is a function of two variables: capital expenditures to find and develop new deposits and capable personnel to do that.

The former is a chronic issue for extractive companies and has been discussed extensively. The solution is simple: pour more money into new projects. However, the lack of mining personnel undermines the progress in the industry. Even today, If we triple the CAPEX, we have two constraints: human resources and time constraints. The latter depends on the former. More qualified personnel will achieve the goals in shorter timeframes.

I will present two charts to support my statement:

{kind=link}

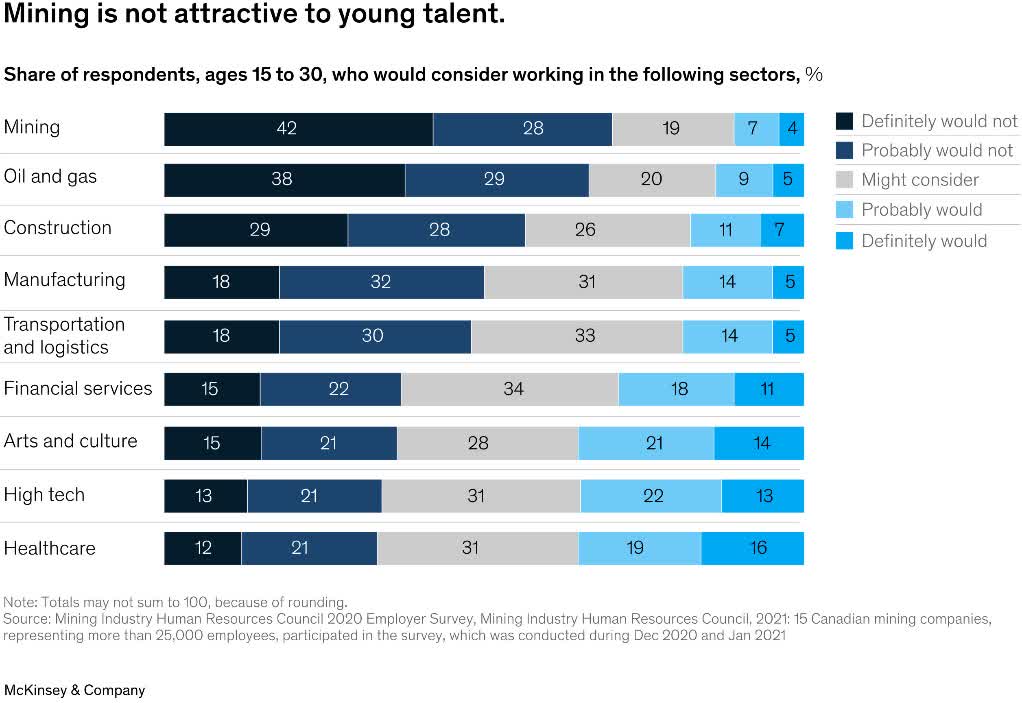

McKinsey & company

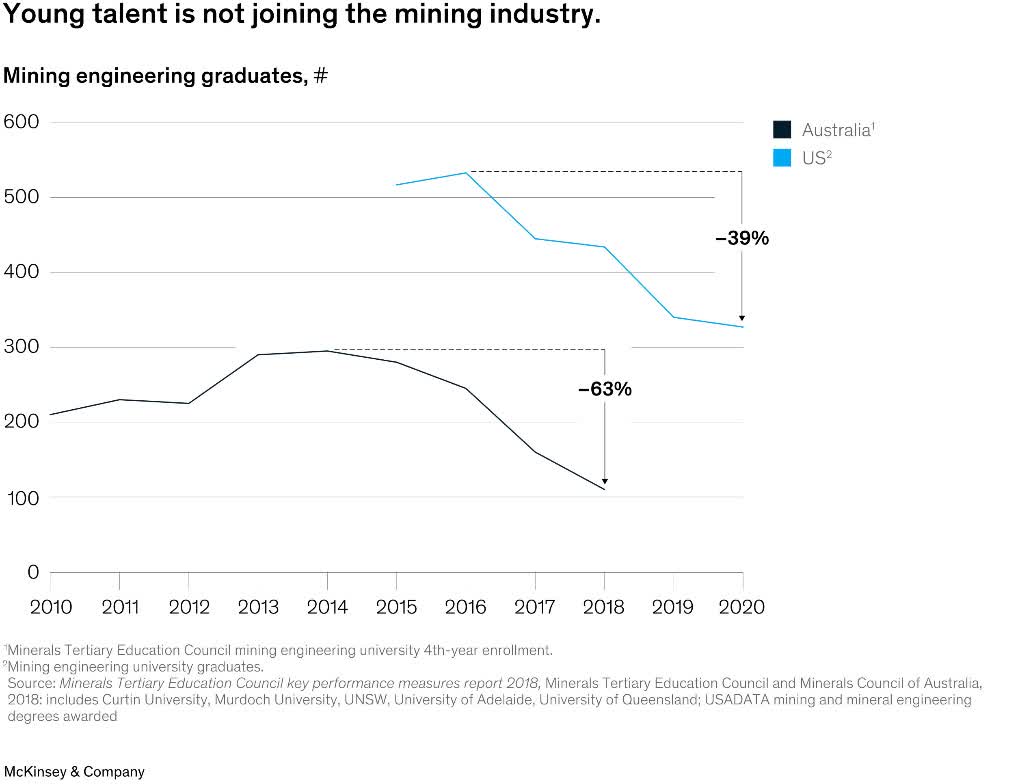

The chart above illustrates the most attractive industries for undergrads in Canada. The interest in mining is almost nonexistent. The following graph represents the number of mining engineering graduates in the USA and Australia.

{kind=link}

Mc Kinsey and Company

The charts paint the same picture: declining interest in the industry quickly. Long term, this trend is unsustainable. The banking system can print money but cannot create skilled engineers overnight. I am a marine engineer graduate with first-hand experience of how long it takes to finish university and then turn the knowledge into practical skills.

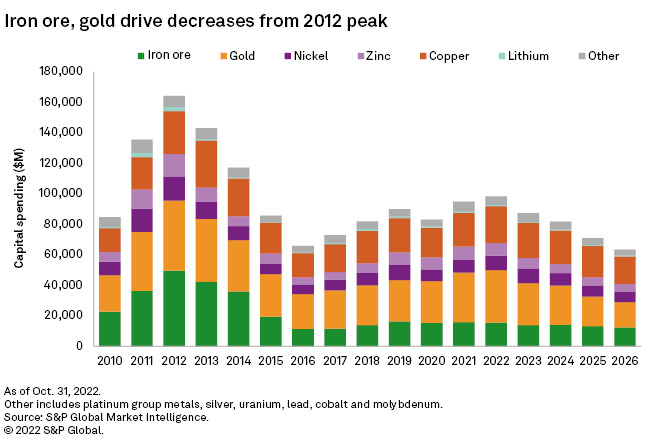

The lack of mining specialists erodes the future supply for all extractive companies. Gold mining is not an exception. We just left the bottom part of the CAPEX cycle, as seen on the chart below provided by S&P500 intelligence :

{kind=link}

S&P Global Intelligence

However, the disinterest in mining among young people is a long-term constraint. That said, the seeds of progress are sown by destruction. Lack of CAPEX and personnel have been the main drivers behind the supply destruction. At the same time, the latter is the reason for higher prices.

I expect the gold price to move higher for longer. However, it will be a volatile ride. We must manage the risk to avoid being overthrown prematurely by the market ebbs and flows. Picking a gold mining stock with low downside risk is the first step of the process. The gold mining industry is diverse and offers everything for all risk profiles. Agnico Eagle is among the best options (pun intended) to bet on gold more safely.

Company Overview

Agnico Eagle is one of the largest gold miners in the world. However, its mines are in the safest jurisdictions: Canada, Australia, Finland, and Mexico. After successful mergers and acquisitions, Agnico became the best major gold producer.

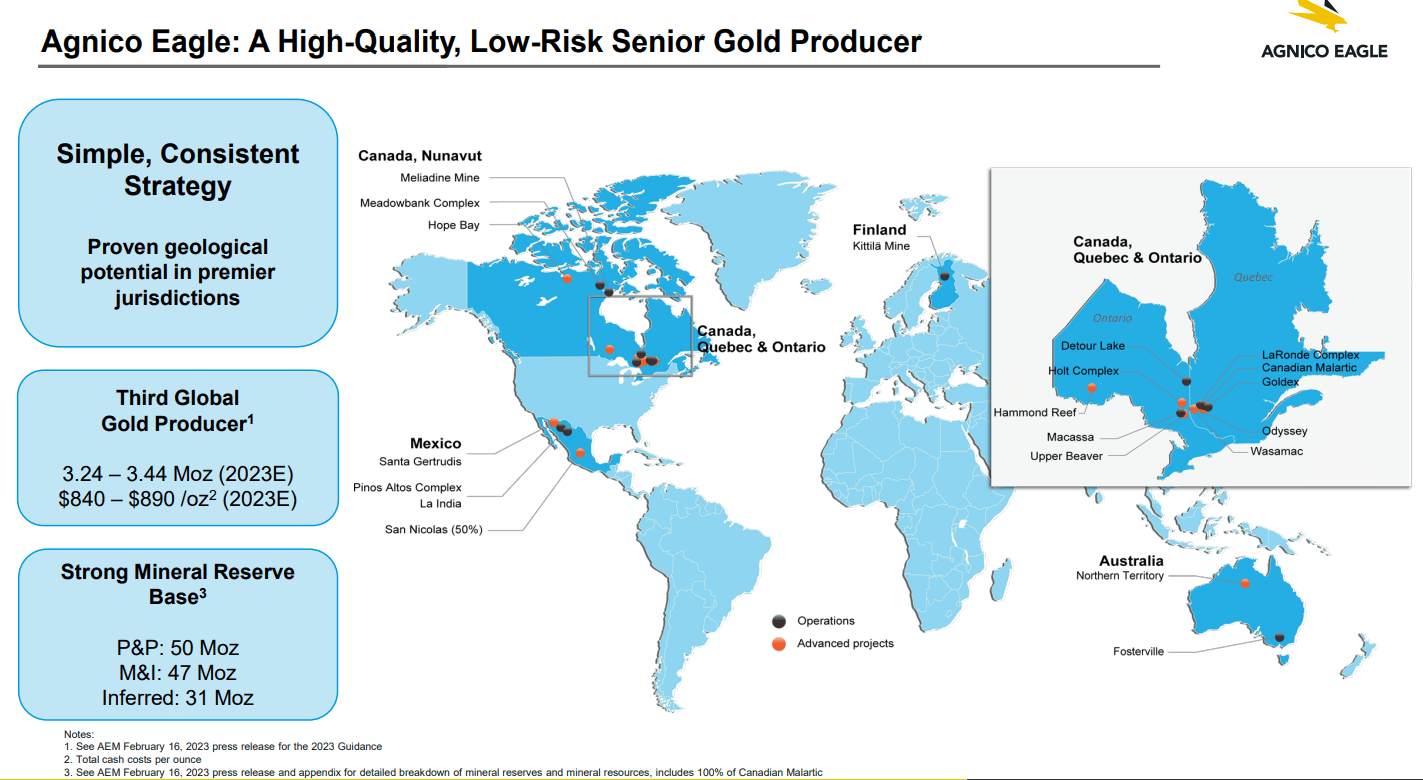

The merger with Kirkland Lake added producing assets in Australia and Canada with high grades and AISC well below the average. The acquisition of Yamana Gold includes in Agnico`s portfolio Odyssey Mine , one of Canada's largest underground gold mines. The image below from the last Agnico presentations gives an overview of the company`s operations:

Mines – location, production, and reserves

{kind=link}

Agnico Eagle presentation

It is impressive to have such a high-quality asset only in safe jurisdictions. Agnico`s significant competitors have mines across the world. For example, Barrick Gold ( GOLD ) operates in Africa, South America, and the USA. Another advantage of having mines in Australia and Canada is the cultural similarities and direct access to qualified personnel.

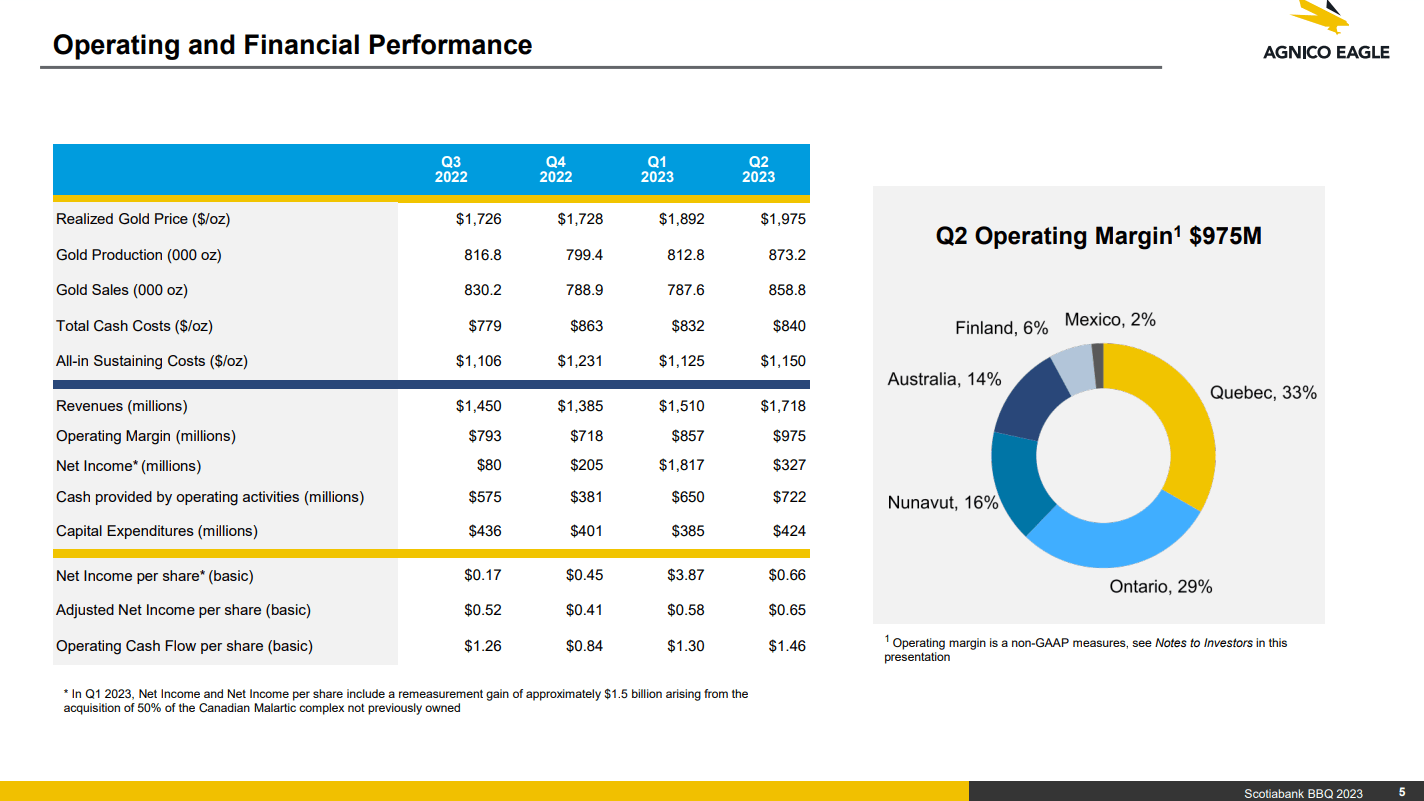

The chart below illustrates the last quarter's performance:

{kind=link}

Agnico Eagle presentation

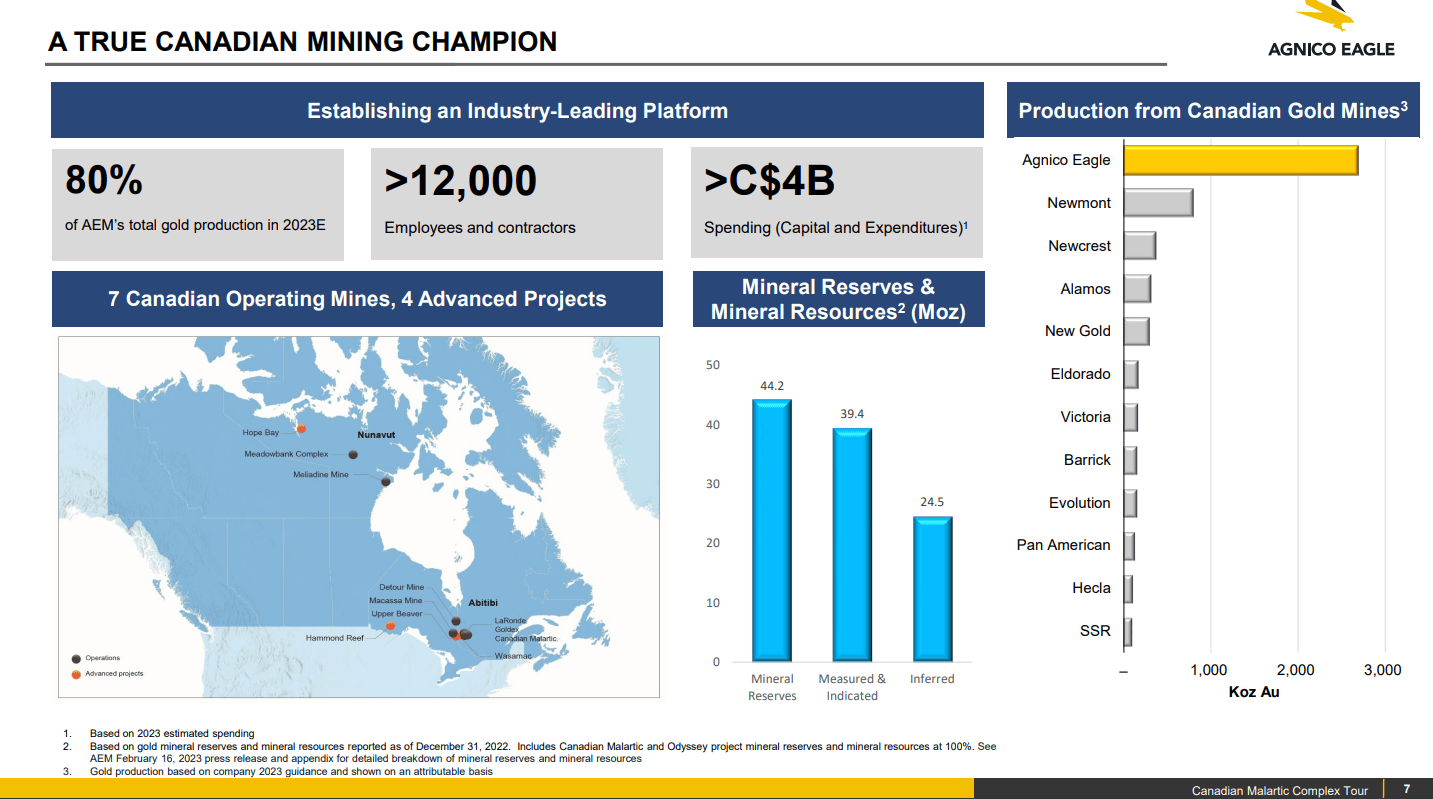

In the first half of the year, Agnico realized strong results. The production and revenue growth transferred into higher income and rising operating cash flows. Most of the company`s revenue comes from Canada. Abitibi Gold Belt hosts all company Canadian mines. Two of the world's largest gold mines are in that region and are part of Agnico`s portfolio.

{kind=link}

Agnico Eagle presentation

Agnico has a few projects to grow its pipeline in the future: expansion of the Detour Lake complex, starting production from the Odyssey underground complex, and ore transformation studies with the potential to increase the company`s reserve base. The current annual production is 3.2-3.4 million oz, according to the company`s guidelines. The incoming projects will increase production, hence the revenues and earnings.

Company Financials

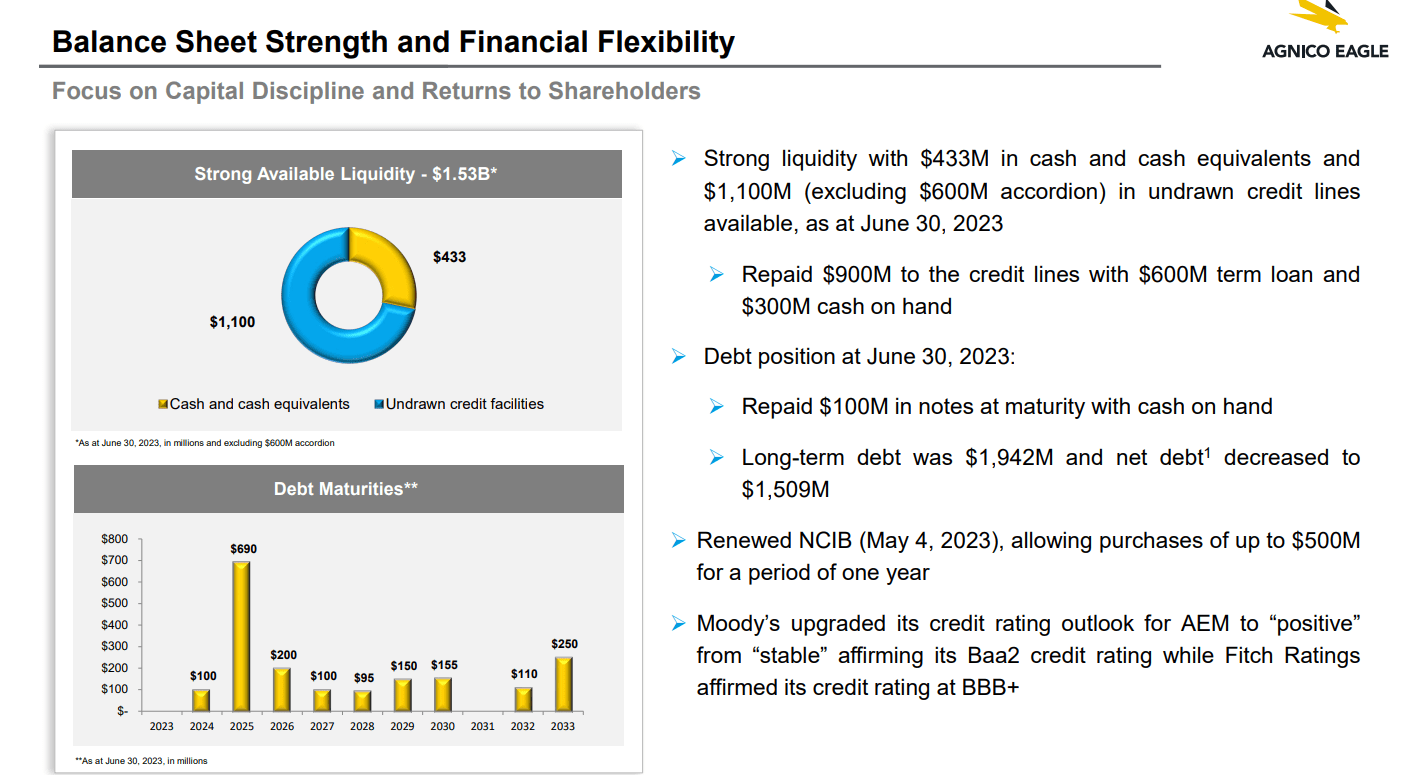

Agnico excels in all solvency and liquidity metrics. The chart below shows Agnico`s financial ratios. The data is from the last company statement:

Seeking Alpha database and authors data

Compared to Barrick and Newmont, Agnico has lower liabilities-to-equity ratios. Barrick has a higher current and quick ratio due to the higher net debt. In 2025, Agnico has $ 690 million of maturing debt. The company now holds $ 432 million of cash and generates FCF TTM $ 618 million. That said, Agnico has more than enough liquidity to repay its debt even now. The image below shows the Agnico`s balance sheet composition:

{kind=link}

Agnico Eagle pesentation

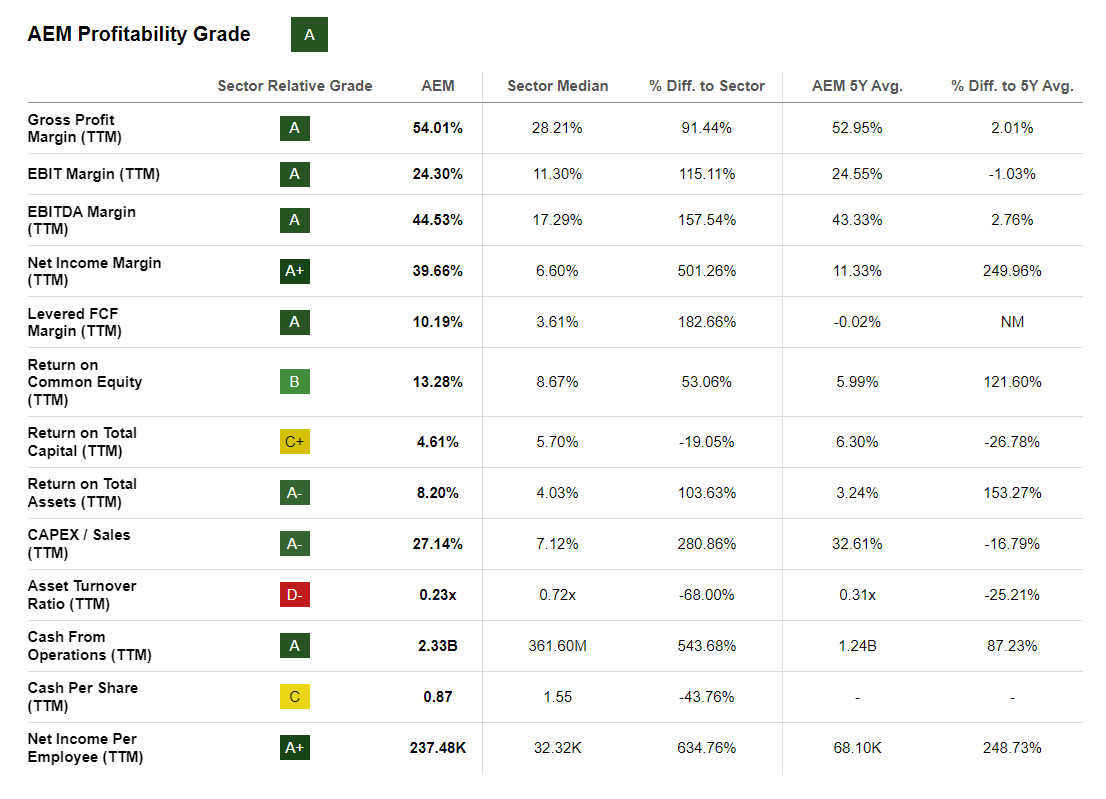

Regarding profitability, Agnico beats its competitors. I like the consistency of the results from gross profit to free cash flows. Usually, the company`s profit gets lost in between despite growing sales. The chart below illustrates Agnico's profitability:

{kind=link}

Seeking Alpha company profile

Agnico maintains a notably high Net Income per employee. It is nine times the industry average and almost four times the company`s five-year average. The last three years have been great for the gold miners in general, but Agnico's results are in the top quartile for the industry.

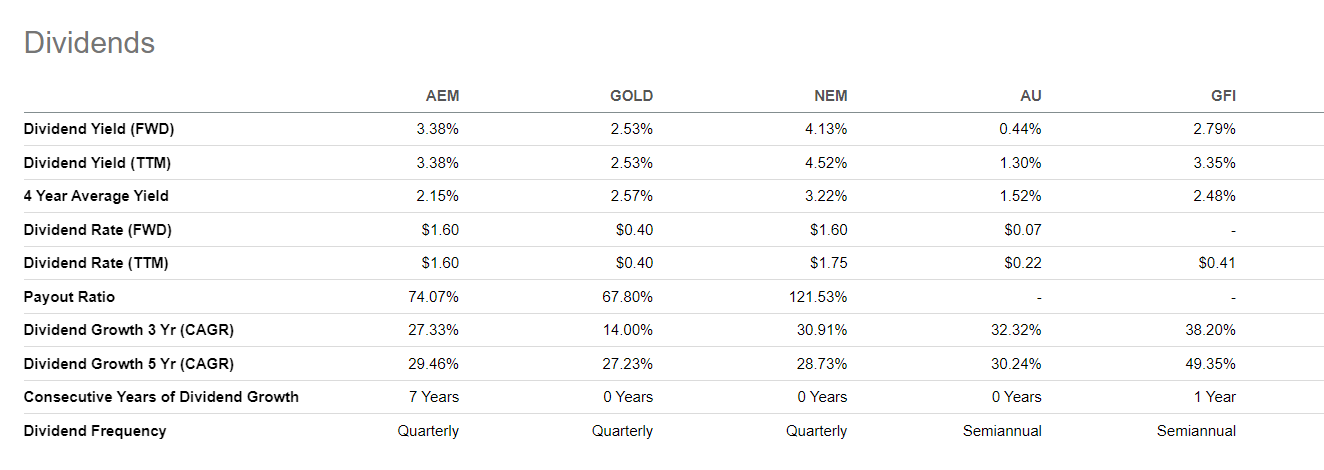

Agnico pays dividends. Below is a chart comparing the dividend policy of Agnico and its competitors.

{kind=link}

Seeking Alpha company profile

Newmont`s dividend yield is higher, but its payout ratio is higher, too. Agnico has better dividend safety and a steady growth rate.

Valuation

Gold mining is not an industry where you can project steady future growth. Its cyclicality, lack of pricing power, and asset-heavy make cash flow predictions often misleading. I value companies in the mining and precious metals sector using two methods:

- Net asset value

- How much do I pay per ounce of plausible reserves

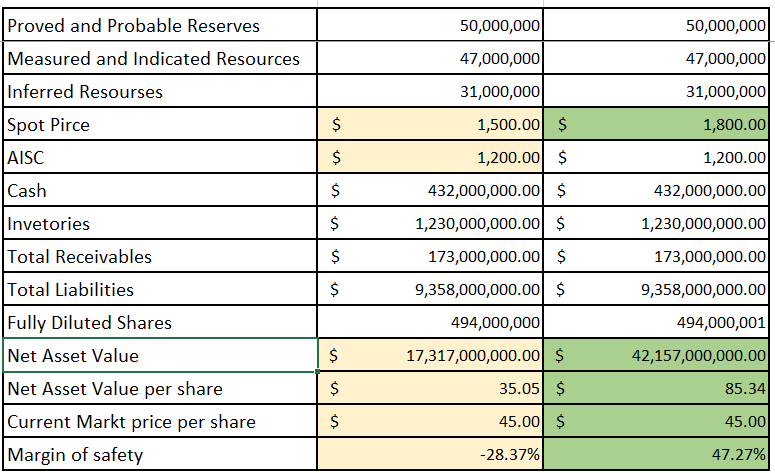

I calculate net assets as follows:

NAV = PR*(SP-AISC) + cash + inventories + total receivables - total liabilities

PR (plausible reserves) = 100% * P&P Reserves + 50%*M&I Resources + 30%*Inferred Resources

{kind=link}

Agnico Eagle presentation and author`s database

I review two scenarios, a conservative one with a gold spot at 1500 $/oz and a base one with a gold spot at 1800 $/oz. As per conservative valuation, Agnico`s shares are overvalued, while as per base one, they are undervalued. As I mentioned earlier, I expect the gold price to rise in the long term above 2000 $/oz. That said, the 1800 $/oz assumption for NAV calculations is safe.

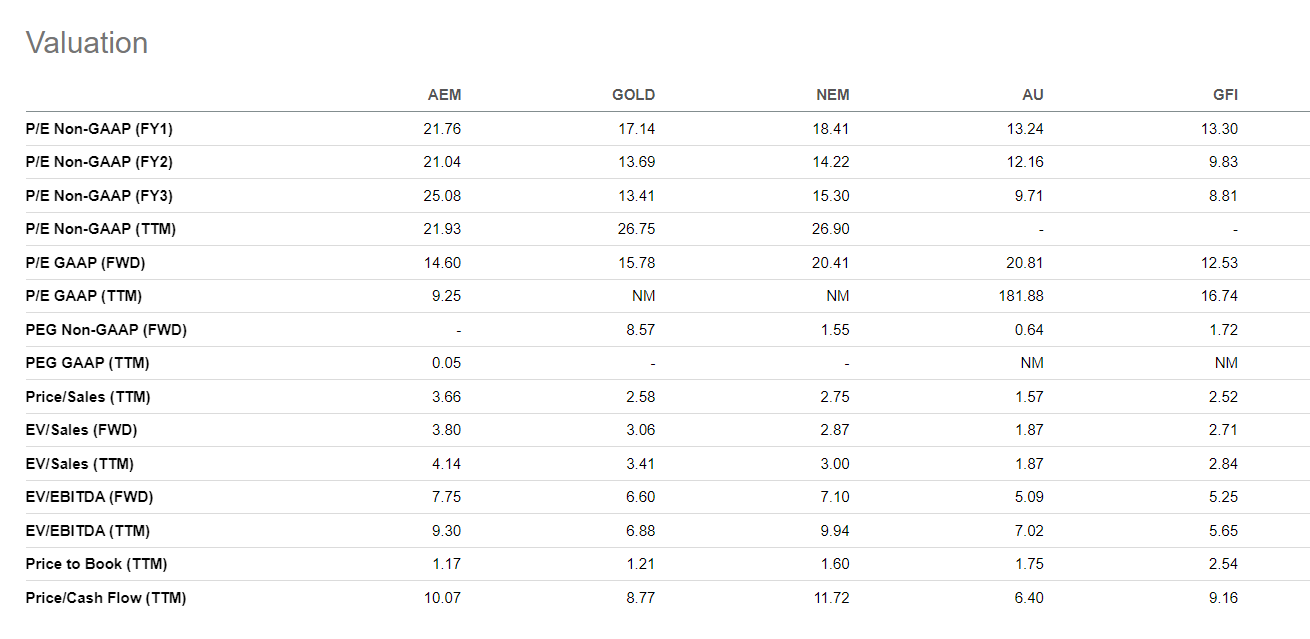

Let`s weigh up Agnico with its major competitors. The image below compares Agnico, Barrick, Newmont ( NEM ), Anglo Gold Ashanti ( AU ), and Gold Fields ( GFI ).

{kind=link}

Seeking Alpha company profile

I use EV/sales and Price/Cash flow metrics while ignoring earnings-based ratios. The latter suffers from accounting gimmicks and adversely affects the quality of data. As the saying goes, earnings are opinion, but cash flow is a fact. Agnico is more expensive based on EV/Sales. On the other hand, Agnico`s value measured with Price/Cash flow is average.

Risk

Buying gold stock is a macro bet. That fact does not diminish the importance of stock picking. Researching individual companies means examining their strengths and weaknesses. The latter carries the downside risks. Our first step as diligent investors is to protect the downside. The primary risks in mining are:

- Political risk

- Metallurgical risk

- Geological risk

- Economic risk

- Financing risk

The political risk is almost nonexistent for Agnico. Its mines are in the safest jurisdiction, according to Fraser Institute research . Metallurgical risk is a complicated topic to assess. Based on Agnico`s experience in the regions where their mines are, I assume such risk is mitigated. The same is valid for the geological risk, too. Agnico has more than enough liquidity and solvency; thus, finance risk is out of the equation.

The more pronounced variable bringing uncertainty is the economic risk. It is a function of inflations, interest rates, and economic growth. It impacts the cost of inputs: labor, energy, and materials. On the other hand, structural inflation benefits asset-heavy industries by increasing their asset valuation.

The economic risk is common for all miners, but the metallurgical, geological, and political risks vary significantly across the companies. Agnico is probably the most de-risked major producer due to its mine location, management expertise, and solid balance sheet. That paragraph summarizes what I understand as downside protection when investing in gold miners.

How to play Agnico

That said, the lower risk comes with relatively capped upside potential. However, the relation between risk and returns is not linear, as the academy taught. The junior miners offer potential for parabolic returns but with a low success rate. I use deep out-of-the-money LEAPS options in major gold miners to obtain junior miners' asymmetric potential with capped downside risk.

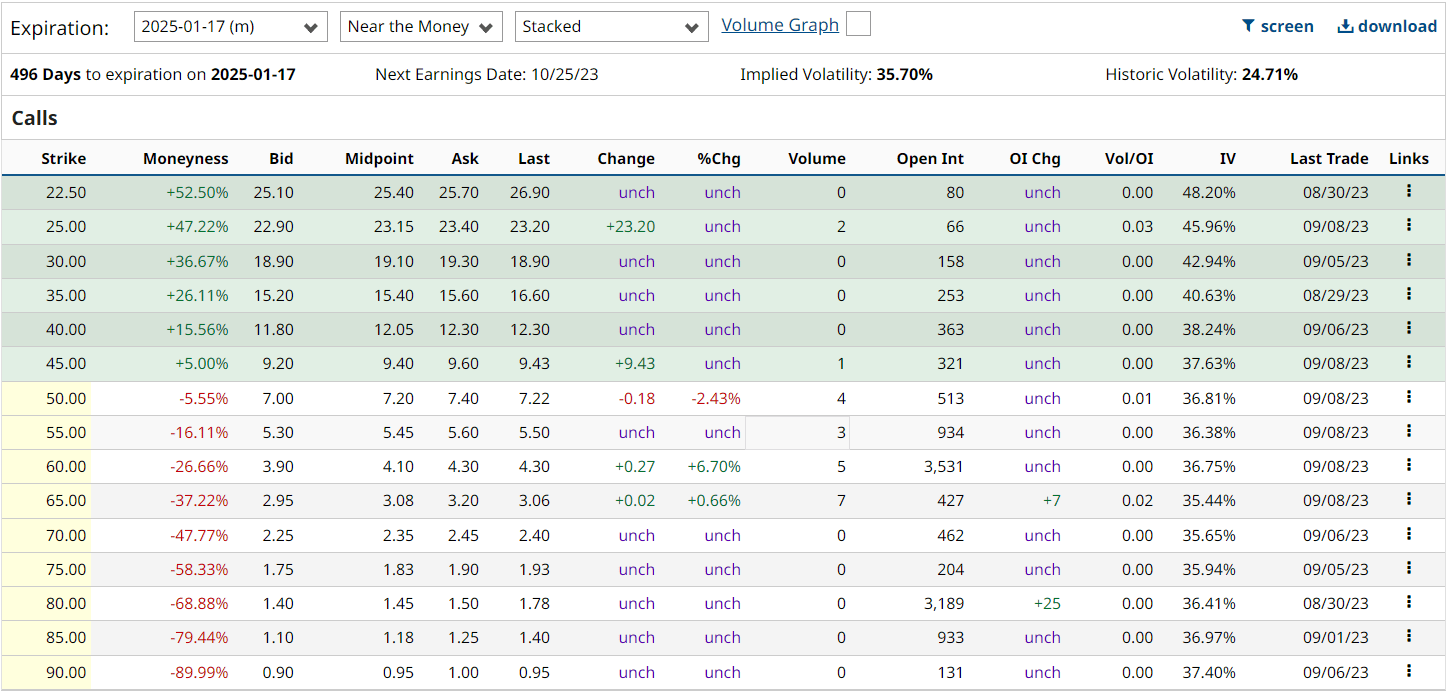

In my portfolio, I own a LEAPS call on Agnico. They provide a significant asymmetry of the bet, at average one to five, i.e., I risk one dollar to get at least five. The available options are still cheap, measured in implicit volatility. The chart below shows the contract with expiration on January 17, 2025.

{kind=link}

Barchart Agnico profile

Sixteen months from now gives enough time for the fundamentals to reflect in the gold price. Another essential consideration when buying an option is the liquidity measured with open interest and volume. For LEAPS, the volume initially is low or even zero, and with approaching expiration, the volume increases. We need high open interest in at least 1000 contracts to ensure enough options to be traded. In such a way, I am confident I will have a buyer to sell my option if I want to, and the spread will remain low.

Important reminder: Options are complex instruments and must be treated as such. Buying options, we trade path dependency for time and volatility dependency. Ignoring that fact can be expensive.

Conclusion

Agnico Eagle is a long-term bet on higher gold prices with limited downside risk. The company owns mines in the best jurisdictions, with AISC below 1200 $/oz, high grade, and LOM beyond 15 years per mine. Agnico has in its pipeline projects as Odyssey and Detour Lake expansion. They will add more ounces to the annual production and the company`s revenue.

The company has a robust balance sheet with adequate liquidity to fund its operations and debt obligations. The next large debt maturity is 2025. Agnico has enough funds to repay its debt. Agnico performs better than its peers on all profitability metrics. I give a strong buy rating because of the mentioned company's strengths and NAV based on the 1800 $/oz spot price.

For further details see:

Agnico Eagle: Asymmetric Bet On Gold With Capped Downside Using LEAPS Options