KGC - Agnico Eagle Mines: A Softer 2023 Outlook

Summary

- Agnico Eagle Mines Limited reported its Q4 and FY2022 results, meeting its production guidance, and coming in just above its range on costs, representing a rare miss for the company.

- While the slight miss on costs wasn't a big deal, the 2023 outlook was a little softer than expected, with lower planned output at multiple mines vs. its 3-year guide.

- I see this as negative short term, especially with the weakness in the gold price that we've seen, given that Agnico is now set to see slight margin compression year-over-year.

- That said, Agnico continues to have a phenomenal pipeline, a peer-leading growth profile among million-ounce producers (2024-2030), and several of the best operating assets, suggesting 25% corrections in the stock should provide buying opportunities.

Just over four months ago, I wrote on Agnico Eagle Mines Limited (AEM). I noted that the stock looked to be a steal below $40.00, with a recent addition to an already strong pipeline (50% interest in San Nicolás). This could be a very high-margin project similar to LaRonde, which is Agnico's longest-running mine and one of the most impressive VMS deposits in Canada.

While some investors might have believed this to be a change in strategy or a deviation from its core strategy, it wasn't all that different. Agnico was already producing zinc and copper at LaRonde in Quebec, and both projects having a somewhat similar metal profile (copper, zinc with by-product gold/silver for San Nicolás and gold with incremental silver, lead, and zinc at LaRonde). Meanwhile, Agnico Eagle also had copper already in its pipeline with Upper Beaver, a high-grade gold-copper project in the eastern portion of the Kirkland Lake Camp.

Since the September update, Agnico Eagle has performed well, rebounding over 45% off its lows in just four months, prompting me to take some profits above $55.00. I attribute the strong performance to another brilliant acquisition which consolidates ownership of Canadian Malartic and sets the company up to grow output with reduced permitting requirements and lower capex if it builds mines that feed a central plant vs. stand-alone projects at Upper Beaver and Wasamac. That strategy benefits from 40,000 tonnes per day of excess mill capacity post-2027 at Canadian Malartic, which is why I have no issue with the price paid for Yamana's Canadian assets. However, the stock has come under pressure recently, with the gold price correcting, and while the Q4 earnings report met expectations, the 2023 outlook came in well below my expectations. Let's take a look below.

Canadian Malartic Mine (Company Presentation)

{kind=link}

All figures are in United States Dollars unless otherwise noted.

Q4 & FY2022 Production & Sales

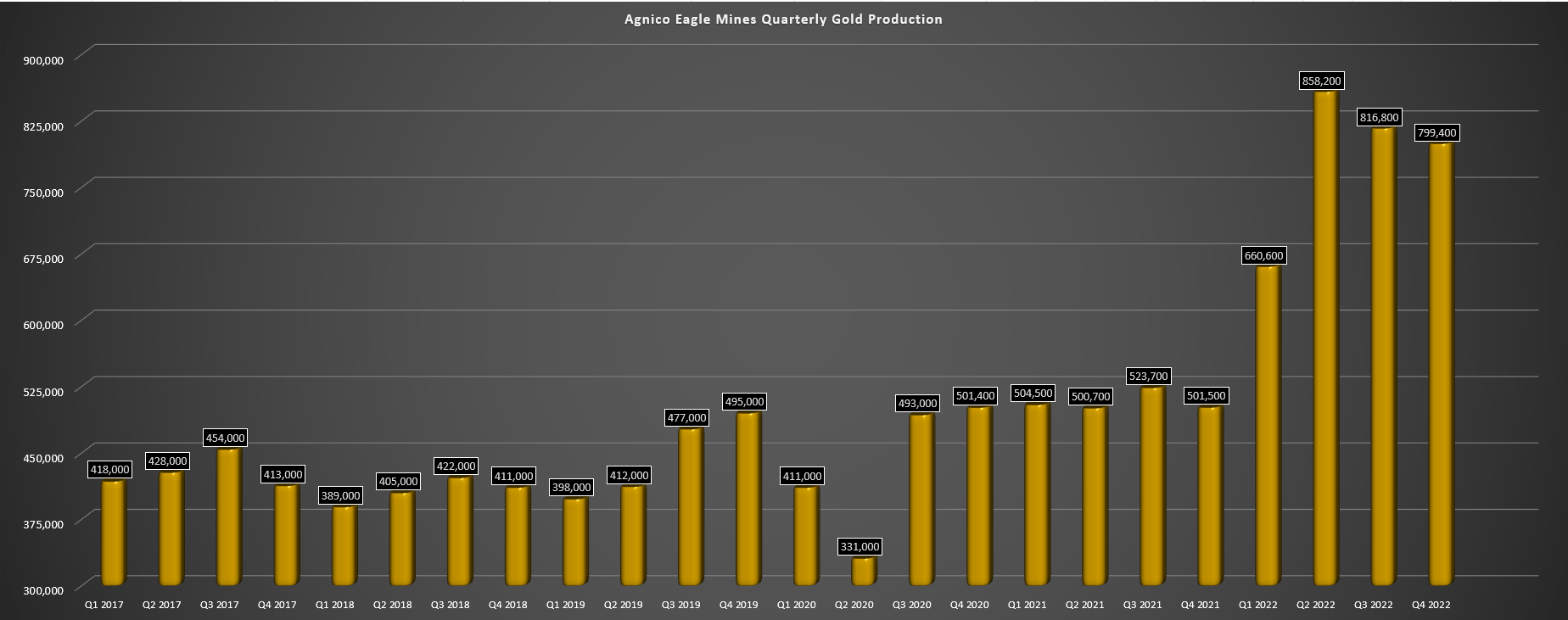

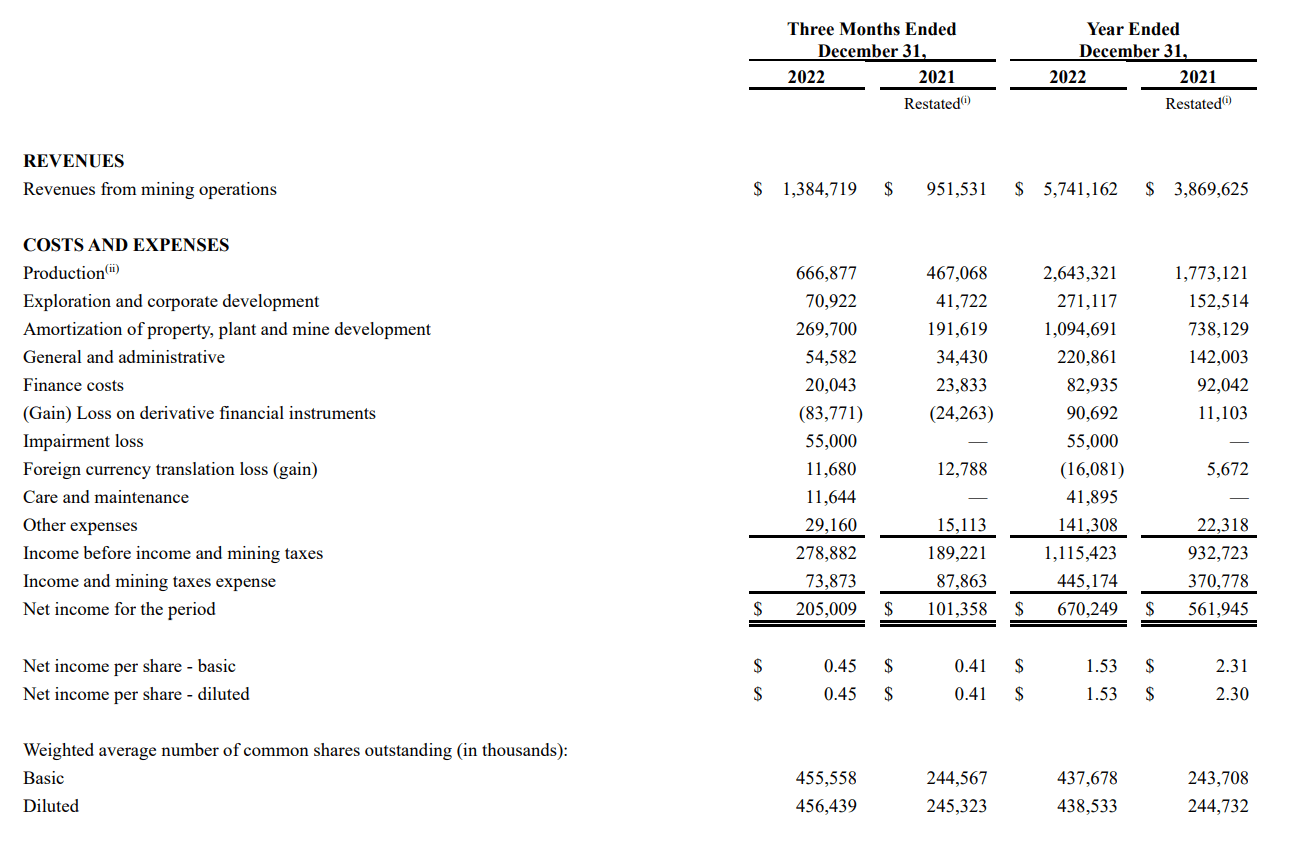

Agnico Eagle Mines Limited released its Q4 and FY2022 results this week, reporting quarterly production of ~799,400 ounces, translating to a ~50% increase from the year-ago period. The sharp increase in production was inorganic, with this being attributed to the Kirkland Lake Gold merger, with an offset from the company placing its Hope Bay Operations in care & maintenance as the company focuses on exploration and better understanding the project's geological potential. On a full-year basis, Agnico Eagle reported payable production of ~3.14 million ounces of gold (~3.28 million ounces when including a full year from Kirkland Lake's operations), with the former figure representing a 51% increase from 2021 levels (~2.08 million ounces).

Agnico Eagle Mines - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

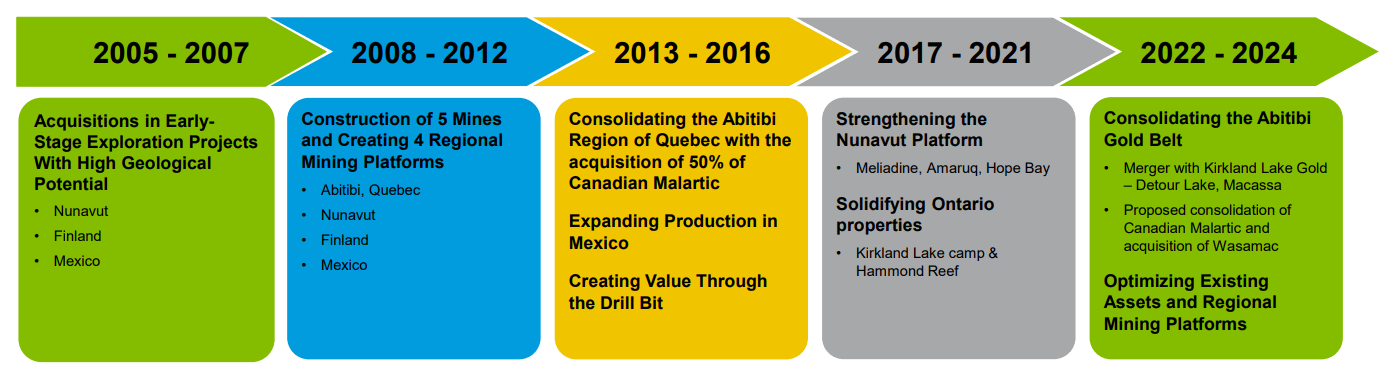

This solid performance continued Agnico Eagle's peer-leading track record of not only production growth, but production growth per share, with this made possible by its capital discipline to focus on low-risk projects with multi-decade potential and paying the right price for these assets. This is a key differentiator for Agnico, unlike others that have paid enormous sums to add future production like deals for Red Back Mining (2010), Equinox Minerals (2011), Richfield (2011), Fronteer Gold (2011), Trelawney (2012), N-Mining (2020), and Great Bear (2021). The Great Bear may pay off, but if Kinross Gold Corporation ( KGC ) had simply waited for GBR to release a sub 4.5 million ounce resource, it likely could have had got the deal for less than $900 million (vs. ~$1.40 billion), as the stock likely would have been halved.

In Agnico's case, the company's acquisitions have all been solid, which has contributed to production growth per share, and its aggressive exploration budget has helped to add additional value to these projects. Examples include Riddarhyttan (Kittila) in 2004, Pinos Altos in 2006, Cumberland (Meadowbank) in 2007, Comaplex (Meliadine) in 2010, 50% of Osisko (Malartic) in 2014, TMAC (Hope Bay) in 2021, and Yamana's Canadian assets late last year. Notably, these operations all remain in production today (ex Hope Bay which should restart in 2026). Plus, Agnico acquired counter-cyclically or Agnico waited for depressed prices to acquire (TMAC Resources).

The exception was Yamana, but the deal made too much sense to pass on, and Agnico still didn't overpay (paying a very fair price given the quality of the asset and value that it could unlock for decades to come).

Agnico Eagle History (Company Presentation)

{kind=link}

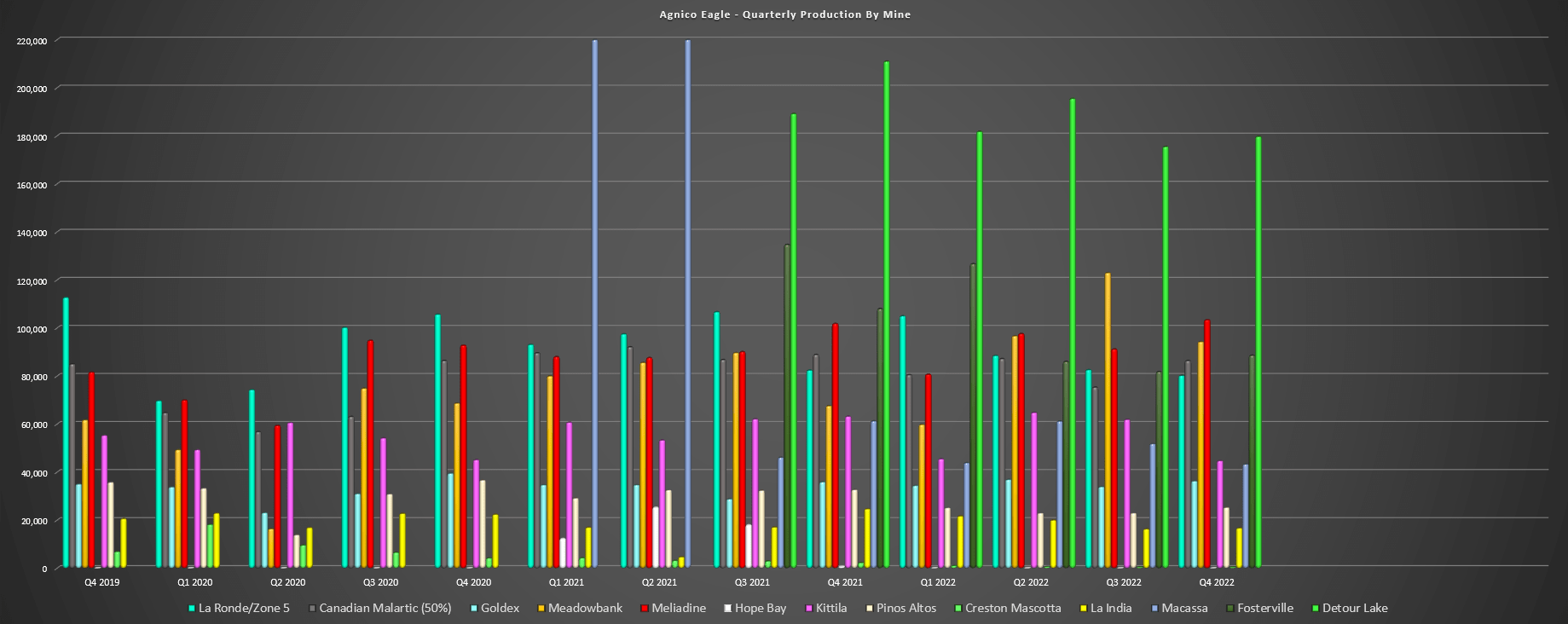

Getting back on track and digging into Agnico's operations a little closer, the company had a solid quarter and year across the board. A couple of assets outperformed expectations, and a few came in slightly below expectations. In terms of outperformers, Detour Lake produced 732,600 ounces (2% beat vs. guidance mid-point), Macassa produced ~200,800 ounces (12% beat vs. guidance mid-point), Meliadine produced ~372,900 ounces (1% beat vs. guidance mid-point), Canadian Malartic produced ~329,400 ounces (3% beat vs. guidance mid-point), and Meadowbank also had a huge year in Nunavut, producing ~373,800 ounces, a more than 7% beat vs. its guidance mid-point. Finally, although one of Agnico's smallest contributors, Goldex had a solid year, with ~141,500 ounces produced, a 5% beat.

Agnico Eagle - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

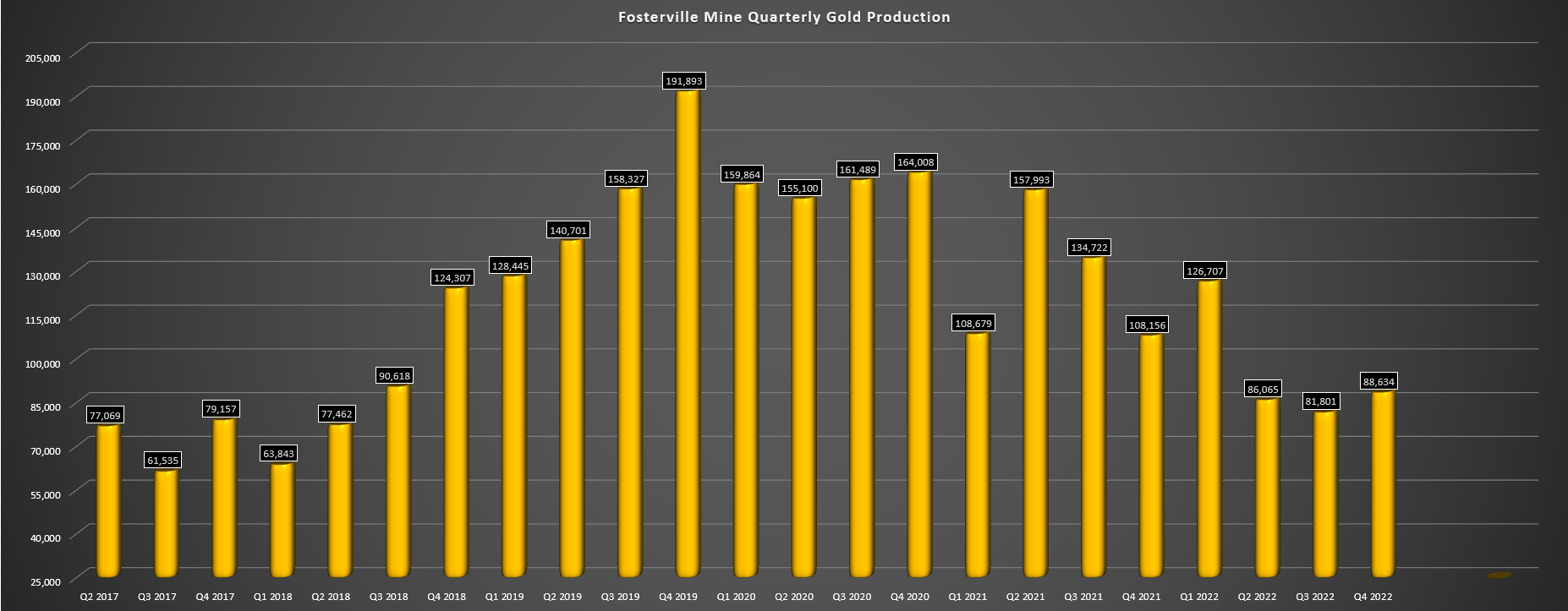

Unfortunately, this was offset by lower production at a few of Agnico's other operations, including a weaker year at two of its lowest-cost assets, Fosterville and LaRonde. At Fosterville, production came in at ~383,300 ounces, which resulted in a 7% miss vs. its guidance mid-point despite a strong finish to the year (~88,600 ounces produced at an average grade of 20.30 grams per tonne of gold). Meanwhile, at LaRonde, production came in at just ~356,400 ounces, a 6% miss vs. its guidance mid-point, and Agnico also announced a softer outlook for the next few years, which we'll discuss later. Elsewhere, its Kittila Mine in Finland missed production guidance by 11% (~216,900 ounces vs. 242,500 ounces). Finally, at Agnico's two smallest assets in Mexico (Pinos Altos and La India), production came in 24% and 9% below guidance, respectively.

Fosterville Mine - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

Overall, Agnico's production results were satisfactory, and the company expects to see further growth in output next year, with annual production of ~3.34 million ounces at the mid-point, representing a 2% increase compared to FY2022 production (including Kirkland Lake operations). That said, this was below my estimates of 3.45+ million ounces given the addition of the other half of Canadian Malartic (250,000+ ounces in FY2023 depending on when deal closes). Let's take a closer look at cost performance:

Costs & Margins

While Agnico Eagle met its production guidance in FY2022 (3.2 - 3.4 million ounces), costs missed, with cash costs and all-in-sustaining costs [AISC] of $793/oz and $1,109/oz, respectively. It's worth noting that these figures compared favorably to FY2021 cash costs and AISC of $761/oz and $1,038/oz, but they missed relative to guidance mid-points of $750/oz and AISC of $1,025/oz, and by a relatively wide margin for a company that has consistently over-delivered on promises.

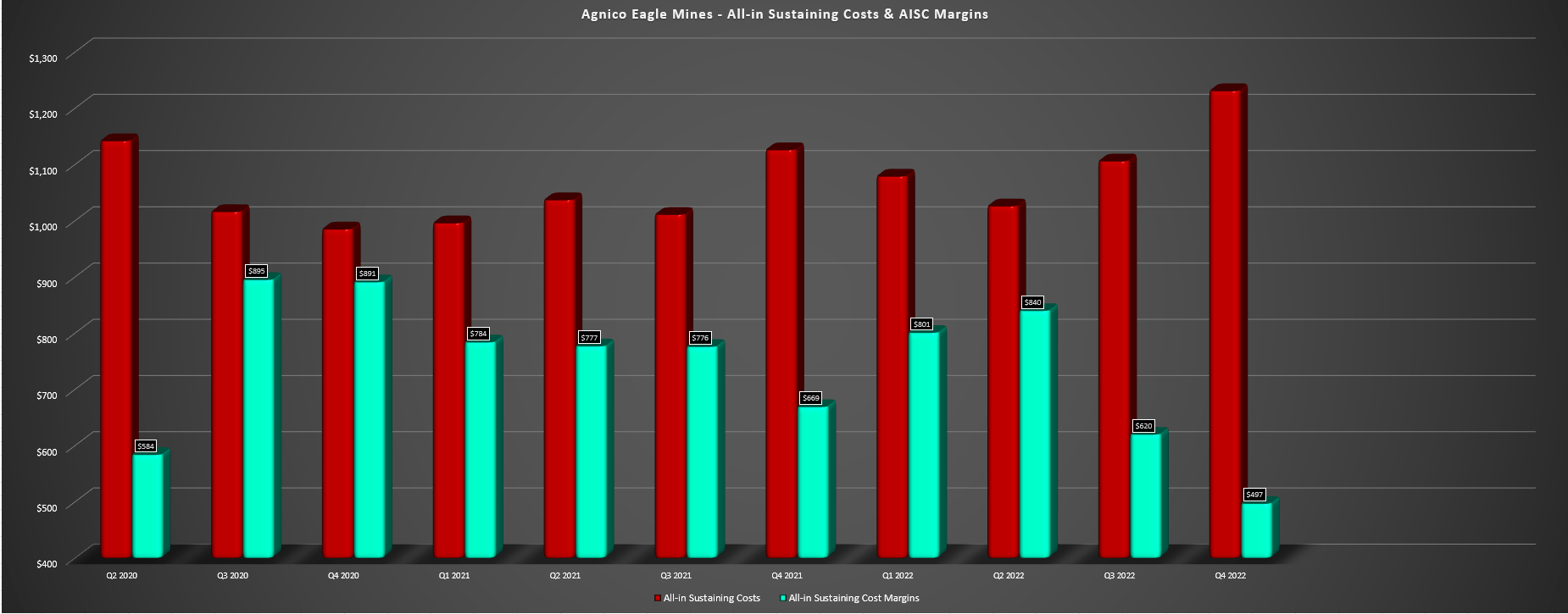

That said, this wasn't a company-specific issue, and stickier inflationary pressures combined with supply chain headwinds led to dozens of misses on costs sector-wide. Hence, I don't see this as an issue specific to Agnico Eagle, and given the quality of these assets and declining costs as Detour/Malartic/Macassa that should benefit from economies of scale, I would expect 2023 to mark peak costs for Agnico with a steadily declining cost profile. Unfortunately, while costs and margins will improve, AISC margins did slide to just $497/oz in Q4 2022, down from $669/oz in Q4 2021, impacted by higher costs and a lower average realized gold price ($1,728/oz vs. $1,795/oz).

At 1.0 million ounces per annum (plus the possible added benefit of trolley assist), Detour Lake is likely a sub $850/oz per annum operation (recent mine plan $920/oz). At Canadian Malartic and with the benefit of multiple feeds, costs should also decline materially, with this asset also looking like it has 1.0 million ounce per annum potential post-2030. Finally, Macassa is a higher-cost operation at 200,000 to 225,000 ounces per annum regardless of its grades, but could see AISC dip below $775/oz as well if it can achieve and maintain a 320,000 ounce per annum production profile post-2025.

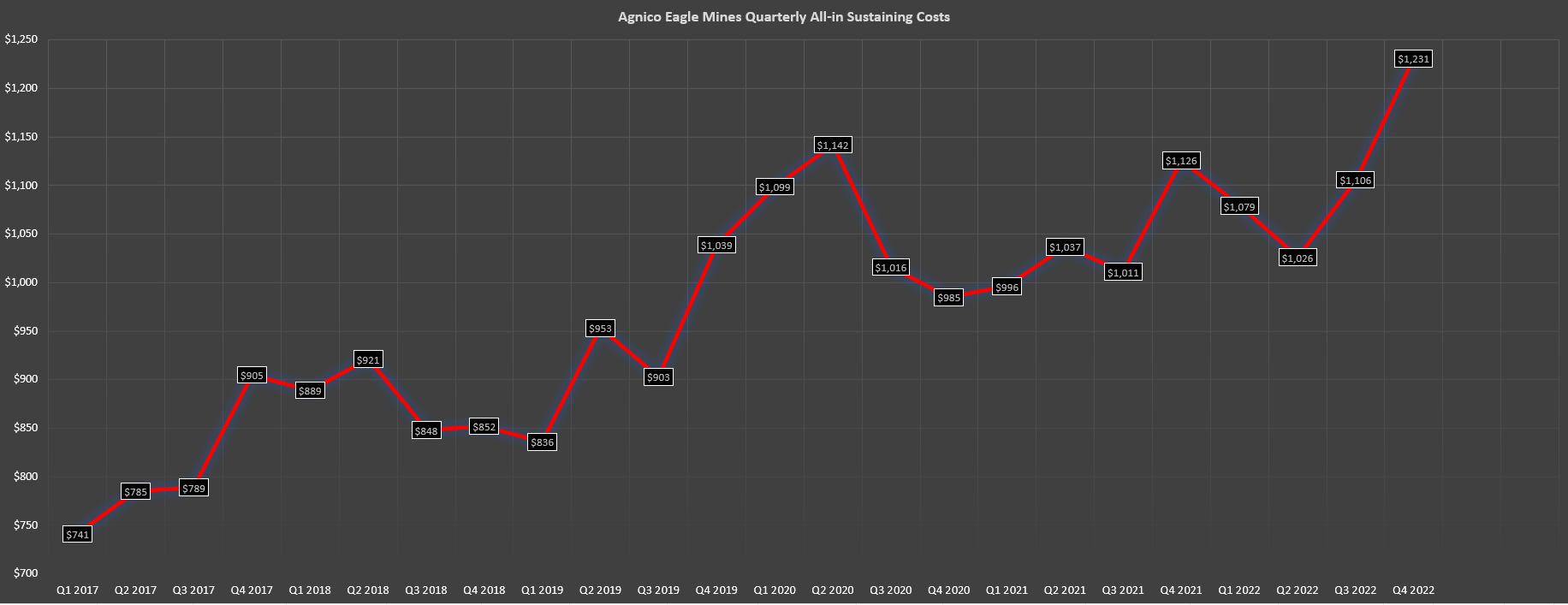

Agnico Eagle - Quarterly AISC (Company Filings, Author's Chart) Agnico Eagle - AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Looking at the chart above, the quarterly trend in unit costs likely doesn't inspire much confidence, and this was Agnico's worst quarter to date with AISC of $1,231/oz. However, this was partially due to elevated sustaining capital in Q4 ($227 million), and Agnico noted that it continues to see pressure on costs from labor, electricity, fuel, and consumables, which will impact 2023 unit costs as well. The good news is that unit costs will decline post-2023 (as guided), and the company did note that it expects "some easing on input costs to occur later in 2023." One reason for the increased costs next year is another year of elevated sustaining capex (~$800 million), with higher deferred stripping costs at Detour Lake and Amaruq and higher capital spend with the full ownership of Malartic, with limited offset from higher sales volumes.

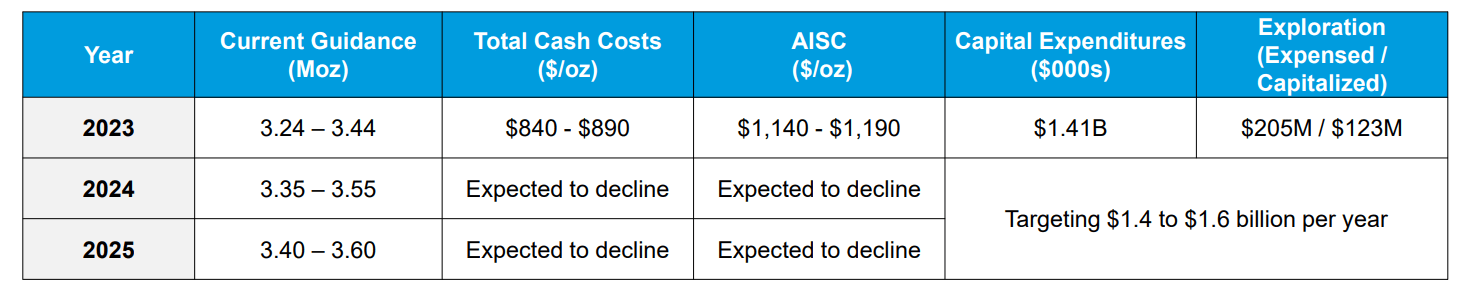

Agnico - Updated 3-Year Guidance (Company Presentation)

{kind=link}

Meanwhile, it has hedged 42% of diesel exposure for 2023 at $0.86/liter to reduce volatility in case we do see a spike in energy prices, and it's armed with a strong balance sheet (just ~$680 million in net debt) to continue to invest in optimization, technology and exploration, which should all help to claw back lost margins. In the case of Detour, this certainly looks to be the case, with valuable ounces added west of the West Pit (highlight intercepts include 28.9 meters at 10.2 grams per tonne of gold and 39.9 meters at 3.9 grams per tonne of gold), and the possibility of an underground component to the asset. Assuming 5,000 tonnes per day at 2.4 grams per tonne of gold and a ~96% recovery rate, the underground alone could contribute an incremental 135,000 ounces per annum.

Detour Lake Operations (Company Presentation)

{kind=link}

Meanwhile, Agnico noted that it could see availability improve by up to 3% at the Detour Mill by using its expertise at Canadian Malartic for its annual maintenance strategy. An additional 1.0 million tonnes per annum at an average grade of 0.85 grams per tonne of gold equates to an additional ~25,000 ounces of gold production per annum just with minor tweaks, and Agnico appears confident that it can meet and potentially exceed the previous goal of 28.0 million tonnes per annum by 2025. It's worth noting that this asset is permitted for up to 32.8 million tonnes per annum, so there is further upside long-term, and at those levels with an underground component, this could be a much lower-cost operation and Canada's largest mine by a wide margin (950,000 to 1.0 million ounces per annum).

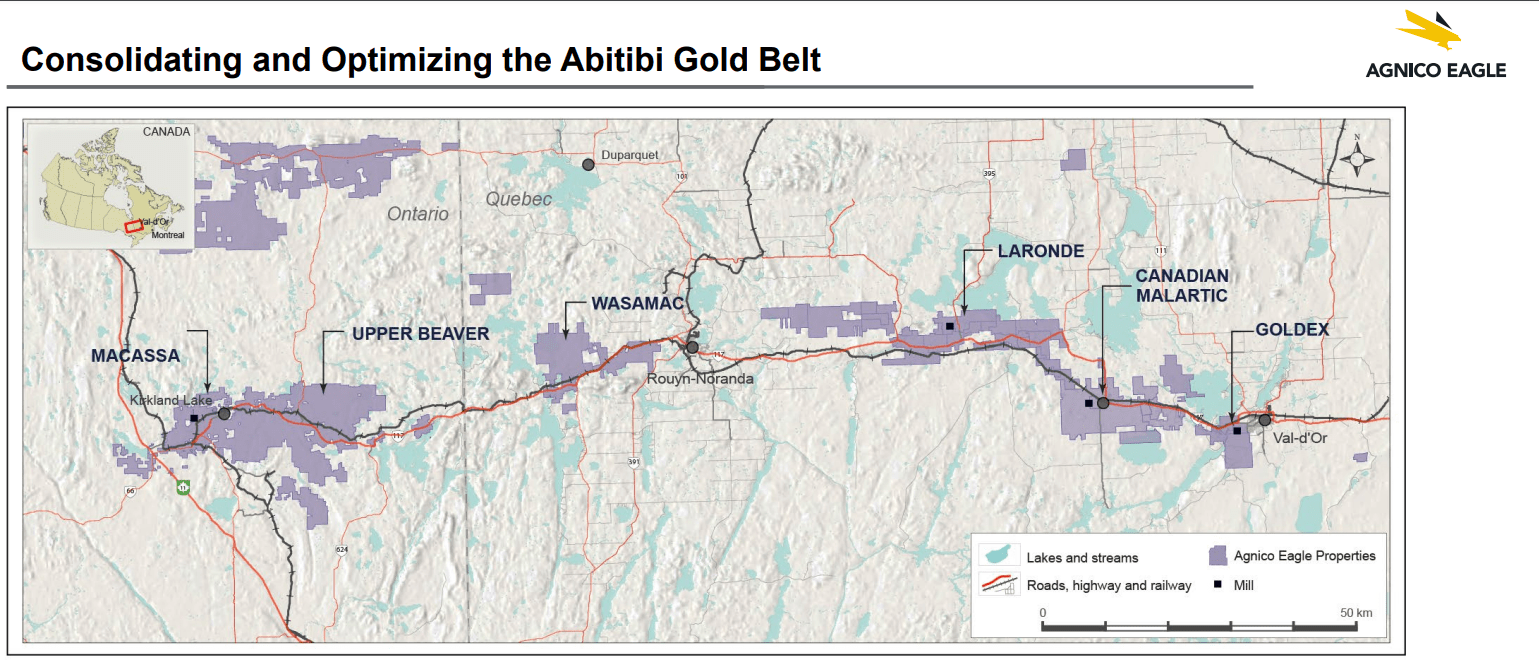

Notably, this is just one asset of many where the company is investing to optimize and reduce costs over the long-term, and there are several opportunities across the portfolio. Another example of leveraging existing infrastructure is potentially sending near surface Macassa ore and feed from Amalgamated Kirkland to a hungry LaRonde plant on the eastern portion of the Abitibi Gold Belt vs. expanding the mill at Macassa. Finally, and as noted earlier, a hub & spoke strategy with the Malartic Mill and its considerable capacity could turn this asset into a monster for decades and reduce permitting requirements, with permits focused on smaller footprints (no need for stand-alone processing facilities). Hence, I don't see this short-term increase in unit costs as that material, and Agnico's future remains very bright from a pipeline/organic growth standpoint.

Agnico Eagle Operations - Abitibi Gold Belt (Company Presentation)

{kind=link}

The Negatives

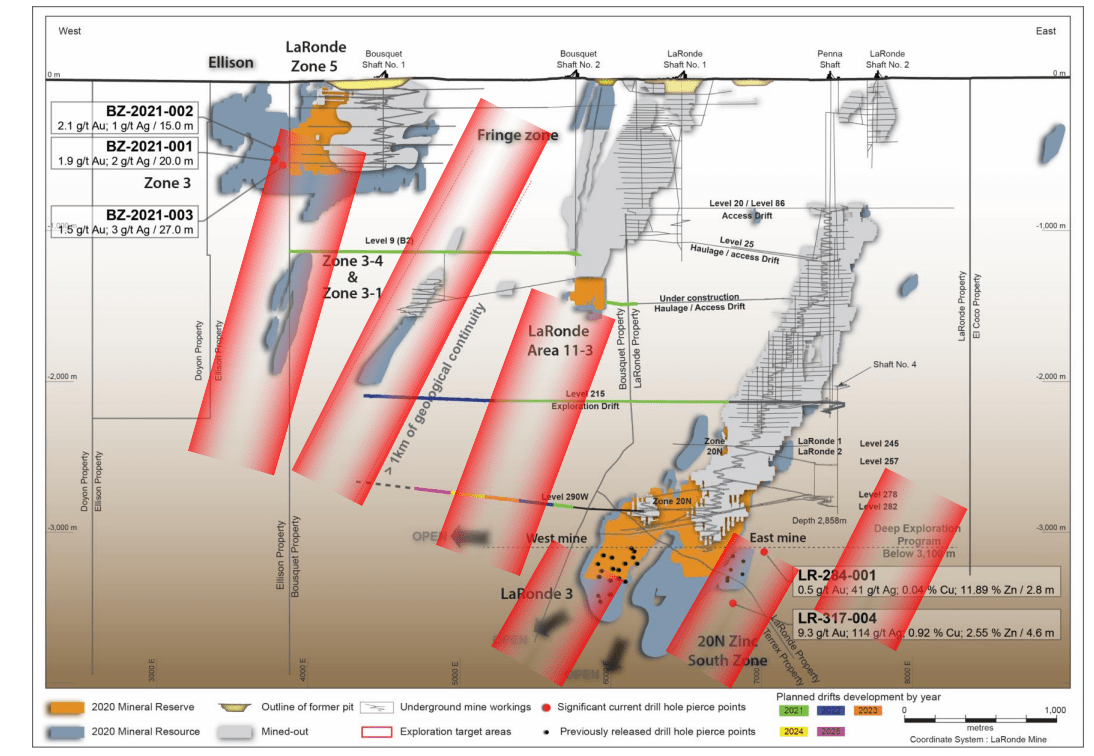

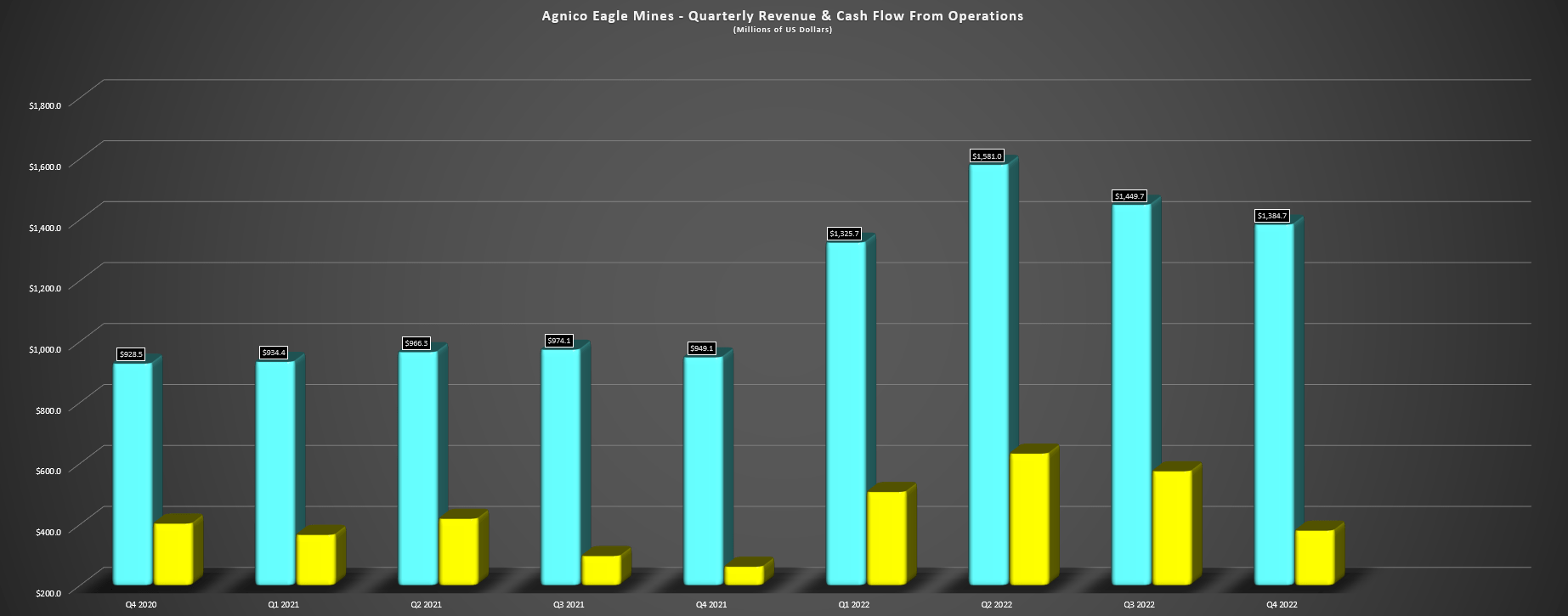

Although Agnico's 2022 production and costs were solid, with outperformance from larger assets offsetting guidance misses at some other mines and the company generating nearly $1.4 billion in cash flow and revenue of ~$5.7 billion for the year despite a weak gold price, there were some negatives. For starters, LaRonde has a more conservative mine plan due to a change in development plans and a transition to pillarless mining, with production expected to decline more than 25% year-over-year at this low-cost asset (275,000 ounces vs. 382,000 ounces previously guided). This is unfortunate, given that this is a very low-cost asset for Agnico and a major contributor from a production standpoint.

Agnico noted that the reduction in guidance is primarily related to a lower mining rate at the LaRonde Mine, with it being prudent to change its mining sequence in the East Mine to "reduce stress levels on secondary stopes, reduce seismic risk, and promote sustainability of the operation in the long run." The combination of adjusting the ramp design in the East Mine to be further from geological structures and the switch to pillarless mining will lead to lower mining rates. However, with considerable resources along the Abitibi Gold Belt (especially in the Kirkland Lake Camp), there are satellite opportunities to top up the plant medium-term and long-term, and Agnico is also exploring increasing the mining rate at its LZ5 Mine to 4,000 tonnes per day with new ore sources (LZ5 Deep, LR11-3 Zone, Ellison, and Fringe zones).

LaRonde Mine (Company Presentation (Q4 2021))

{kind=link}

Unfortunately, things haven't been any easier for Agnico than they were for Kirkland Lake in Australia, with the Environmental Protection Authority of the Victoria Government placing operational constraints on Fosterville. This has to do with the low frequency noise (below the level of human hearing) which is being emitted by primary surface fans at Fosterville. With these fans unable to operate from midnight to 06:00 AM, it is difficult to support previous mining rates. Agnico has continued to work and complete studies to address these issues and work towards a resolution, and noted that if and once this is resolved, we could see a 50,000 ounce lift in production in 2023/2024. For now, though, the company is guiding more conservatively at 305,000 ounces in 2023 and 240,000 ounces in 2024 vs. 375,000 ounces and 247,500 ounces, respectively.

Finally, at Kittila, and adding insult to injury after a tough year due to inflationary pressures in Finland, the company has yet to receive the reinstatement of its 2.0 million tonne per annum operating permit, with the company waiting on a decision by the Supreme Administrative Court of Finland. This will lead to lower production in 2023 unless it's received ahead of time, with guidance reeled in from 250,000 ounces to 200,000 ounces. For those unfamiliar, Agnico already had a very tough year at the mine, with electricity prices soaring to peaks of 300 to 500 Euros per megawatt hour on a daily basis in November and December vs. typical electricity prices of 50 Euros/megawatt hour. The spikes in electricity prices were related to the delayed commissioning of a nuclear power plant in Finland.

On a full-year basis, electricity costs were up 180% year-over-year at Kittila, but the asset still managed to have a decent year, with ~216,900 ounces produced at cash costs of $980/oz given the challenges. Unfortunately, with an even lower production profile next year, I wouldn't expect a very robust year for Kittila from a margin standpoint, especially with a full year of what have been very sticky inflationary pressures. These negative developments do not impact the long-term outlook for LaRonde, Fosterville or Kittila, but it's understandable why Agnico is seeing cost increases that will extend into 2023 when two of its cash cows (LaRonde and Fosterville are higher-margin operations) had tougher years and will remain below planned output levels in 2023. Let's look at the valuation to see whether this is priced into the stock.

Valuation

Based on ~490 million shares (post-Yamana acquisition) and a share price of $49.30, Agnico Eagle traces at a market cap of ~$24.2 billion and an enterprise value of ~$24.8 billion. This is a very reasonable valuation for the company's top-3 producer whose unique attributes include having 90% of production coming from Tier-1 jurisdictions, an incredible dividend track record (50x increase over the past two decades) and track record of production growth per share , industry-leading margins (sub $1,100/oz AISC long-term), and an industry-leading growth profile. In the latter case, Agnico has the development pipeline to support up to 4.5 million ounces of gold production per annum, with multiple projects in the wings like Upper Beaver, Wasamac, San Nicolas (50%), and Hope Bay.

Agnico Eagle - Quarterly Revenue & Cash Flow (Company Filings, Author's Chart) Agnico Eagle - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

{kind=link}

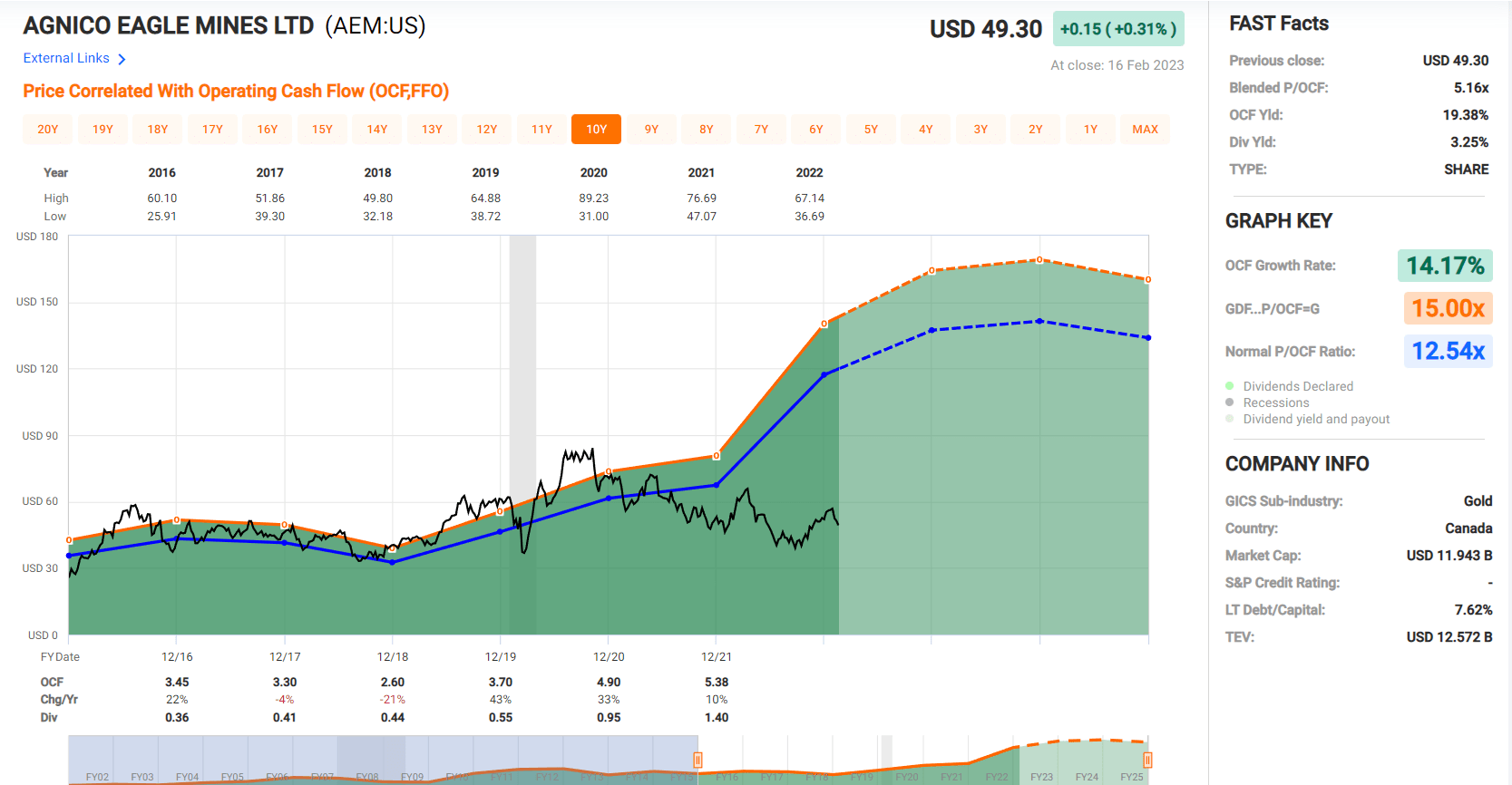

Looking at the chart above, Agnico has historically traded at 12.5x cash flow, and I would argue that a multiple of 13.0 is more than reasonable, given that it's the premier major producer with favorable jurisdictions and attractive margins. Based on conservative FY2023 cash flow estimates of $4.50, this translates to a fair value for the stock of US$58.50, pointing to 20% upside from current levels. However, this fair value estimate is based on what will be a weak year for Agnico, and it doesn't place any value on its strong development pipeline or exploration upside, where I think we can easily assign a value of $5.0+ billion (Santa Gertrudis, Upper Beaver, Wasamac, Hammond Reef, Hope Bay, San Nicolas [50%], exploration upside). It also doesn't place any value on organic growth at existing assets like Detour Lake.

Agnico Eagle - Revenue, Expenses & Net Income (Q1-Q3 2022) (Company Filings)

{kind=link}

Given that valuing the stock on cash flow understates the company's long-term potential, I believe the best way to value Agnico Eagle Mines Limited stock is on a P/NAV basis. Based on an estimated net asset value of ~$23.7 billion after adjusting for G&A expenses, and assigning a 1.45x P/NAV multiple given its strong history of reserve replacement, I see a fair value for Agnico stock of ~$35.0 billion. After dividing by ~490 million shares (year-end 2023), this translates to a fair value for the stock of US$71.40, translating to a 44% upside from current levels or ~47% upside on a total return basis.

Importantly, this doesn't account for upside in the gold price, with these assumptions based on a $1,700/oz gold price, in line with the three-year average. Given its undervaluation, I continue to see Agnico as one of the best buy-the-dip candidates sector-wide. So, while the Q4 report was undoubtedly fixed, I do see some of the negatives priced into the stock already, but that doesn't mean we won't see some selling pressure.

Summary

Agnico Eagle Mines Limited put together solid Q4 and FY2022 results in a challenging year and has entered 2023 much stronger. Its development pipeline is beefed up further, and this being a unique development pipeline that leverages off existing infrastructure. That said, the Agnico Eagle Mines Limited 2023 outlook is softer than I expected for both output and costs. I would have seen this as less material if the gold price were above $1,950/oz given that this would offset the higher costs, but it looks likely that we'll see some margin compression in 2023 after Agnico already suffered moderate margin compression in 2022.

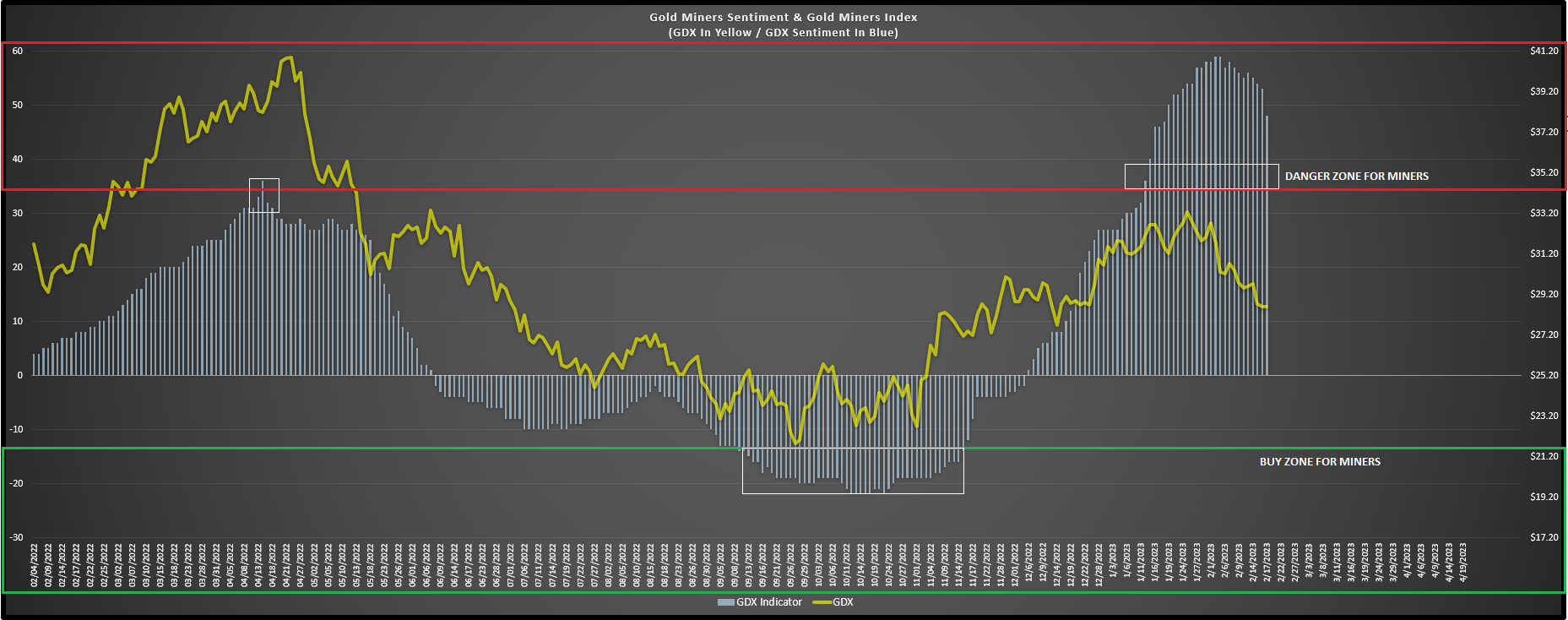

GDX Index & Gold Miners Sentiment (Author's Data & Chart)

{kind=link}

Given that this is temporary and costs are guided to trend lower post-2023, I don't see any change to the investment thesis and continue to see Agnico Eagle Mines Limited as a core holding. However, with the stock short-term extended and sentiment in the sector over-heated (shown above), I took some profits above $55.40. Assuming this weakness continues and if Agnico's correction were to extend to over 25% from its recent highs, I would consider adding back some exposure to Agnico Eagle Mines Limited stock.

I am neutral short-term on Agnico Eagle Mines Limited from $49.30 given that I previously expected to see margin expansion in 2023 ($1,850/oz gold price assumption with declining costs). However, I remain long-term bullish, with Agnico Eagle Mines Limited continuing to be a top-3 producer sector-wide and one of the safest ways to get exposure to gold, with a team that has a near flawless track record of capital discipline.

For further details see:

Agnico Eagle Mines: A Softer 2023 Outlook