AEM - Agnico Eagle Mines: A Stronger Year On Deck

2024-01-01 08:33:17 ET

Summary

- Agnico Eagle had a solid 2023 despite minor headwinds at multiple assets, but 2024 will be a better year with higher production of ~3.5 million ounces at lower costs.

- That said, while 2024/2025 will be better years with significant free cash flow generation, the company has its work cut out for it to smooth out production in 2026-2028.

- In this update, we'll look at the company's 2024 and long-term outlook, recent developments, and whether the stock is worthy of investment at current levels.

It's been a tough year for the Gold Miners Index ( GDX ) with the disappointing results of a few souring sentiment for the group, and continued share-price underperformance vs. the gold price. Some of the detractors with pitiful results and/or per share metrics (due to continued share dilution) have been Coeur Mining ( CDE ), First Majestic ( AG ), and Iamgold ( IAG ). Meanwhile, although Evolution Mining's ( OTCPK:CAHPF ) margins have been solid, we've seen significant share dilution with more aggressive growth by M&A, with this being the third deal in three years (Battle North, Ernest Henry, Northparkes).

On a positive note, metals prices are finally at favorable levels where the usual (share dilution) suspects might be able to avoid issuing additional shares, and the sector leaders have some of the strongest balance sheets in years on balance, while the average million-ounce producer is paying a dividend yield double that of the S&P-500 ( SPY ). In addition, we've seen far more disciplined growth from most miners (unlike past cycles), with one company that's doned an excellent job over the past few years of beefing up its portfolio at accretive prices being Agnico Eagle Mines ( AEM ). In this update, we'll look at the company's 2024 and long-term outlook, recent developments, and whether the stock is worthy of investment at current levels.

Kittila Operations - Company Website

{kind=link}

2024 & Long-Term Outlook

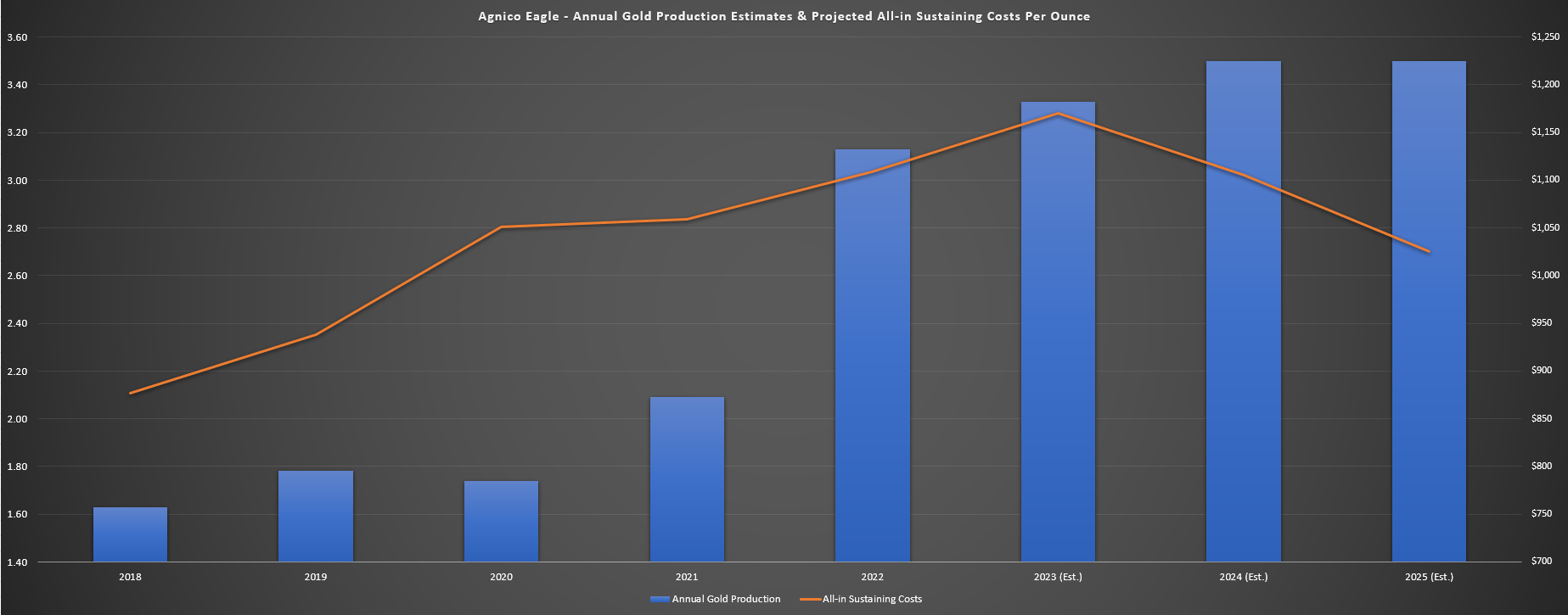

2023 was a solid year for Agnico Eagle despite some hiccups (Detour downtime in Q3, restrictions at Fosterville, permit delays at Kittila), but these issues have since been resolved and the company will have another record year with production of ~3.4 million ounces. This has been helped by full ownership of Canadian Malartic (50% --> 100%) and another strong year from Meadowbank (~322,400 ounces in first nine months of 2023) which helped to offset lower grades/mining rates at Fosterville and a change in the mining method at LaRonde. Hence, despite was expected to be a tougher year with some uncertainty related to production rates at Fosterville/Kittila, Agnico will come in above its guidance mid-point of 3.34 million ounces, consistent with its track record of over-delivering on promises.

Agnico Eagle 2018-2025 Production & Foward Outlook - Company Filings, Author's Chart & Estimates

{kind=link}

Unfortunately, while production hit a new record in 2023, costs were up sharply from the three-year average of $1,073/oz (2020-2022), impacted by inflationary pressures and higher sustaining capital (higher deferred stripping costs at Detour Lake and Amaruq, plus full ownership of Canadian Malartic). The result was that Agnico Eagle guided for higher costs of $1,140/oz to $1,190/oz in 2023, and costs look like they will come in near the mid-point for 2023, at or below $1,175/oz. On a positive note, 2024 is expected to be a much better year, with Agnico benefiting from higher production (helped by Meadowbank, Macassa/Amalgamated Kirkland, Kittila and Canadian Malartic), with Meadowbank expected to have a near 500,000 ounce production profile in both 2024 and 2025. The higher sales combined with what could be a lower fuel price suggest a much better year on deck, with Agnico set to produce closer to 3.5 million ounces at ~$1,120/oz AISC (3% increase in output and ~5% decline in costs).

Kittila's production will benefit from the operating permit being restored to 2.0 million tonnes per annum.

Sean Boyd

Dominique, do you want to help us with the split between underground and open pit at Meadowbank as we go beyond 2023.

Dominique Girard

Yeah, the Amaruq underground is going to bring 100,000 ounces, 140,000 ounces to the game. That's going to bring overall Meadowbank getting - they're going to reach over 500,000 ounces, which is going to be our biggest operation in those years 2024, 2025.

- Agnico Eagle Mines Q4 2020 Conference Call

This improvement in the cost profile will help Agnico to regain its throne as one of the lower-cost million-ounce producers sector-wide and the higher gold price should contribute to a significant increase in operating cash flow and free cash flow when combined with more normalized sustaining capital expenditures this year. In fact, Agnico is positioned to generate up to $1.35 billion in free cash flow in 2024 if gold prices can remain above $2,000/oz, and 2025 should be just as strong with a similar production profile but at even lower costs (in line with Agnico's guidance provided at year-end 2022 that stated costs would decline from 2023 levels in 2024/2025). However, the company does have its work cut out for it in the latter half of the decade to offset depletion, and the recent Nunavut Impact Review Board's Reconsideration and Recommendation Report (which we'll discuss later) related to the Meliadine Phase 2 Expansion has added additional uncertainty.

For those unfamiliar, Meadowbank/Amaruq has been a cash cow for Agnico Eagle since it went into production in 2010 (producing well over 4 million ounces of gold to date from Meadowbank/Amaruq), and production exceeded planned levels with production originally expected to end in 2020 with ~3.6 million ounces of open-pit reserves across three pits (Vault, Portage, Goose). However, production is expected to decline in 2026 from just shy of 500,000 ounces in 2024/2025 as mining is completed at the Whale Tail Pit. Agnico noted in its Q3 2023 Conference Call that it is looking at potentially extending production past 2027 at Meadowbank, which could be achieved by completing a pushback at the IVR Pit. Still, production will be lower at this #3 asset by size (just behind Detour and Canadian Malartic) later this decade, and it's not clear how much further the mine life can be extended past 2026.

Meadowbank Operations - Company Website

{kind=link}

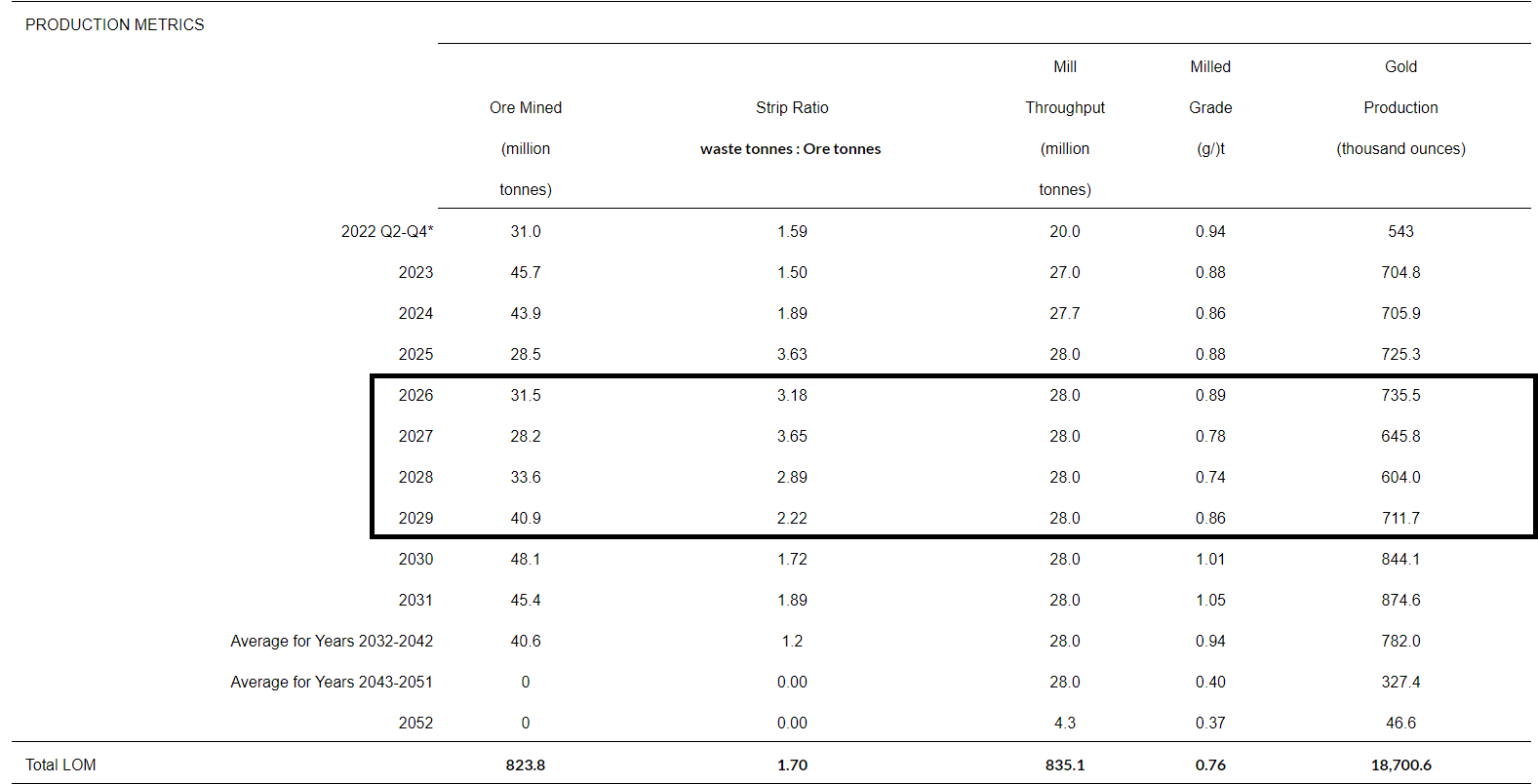

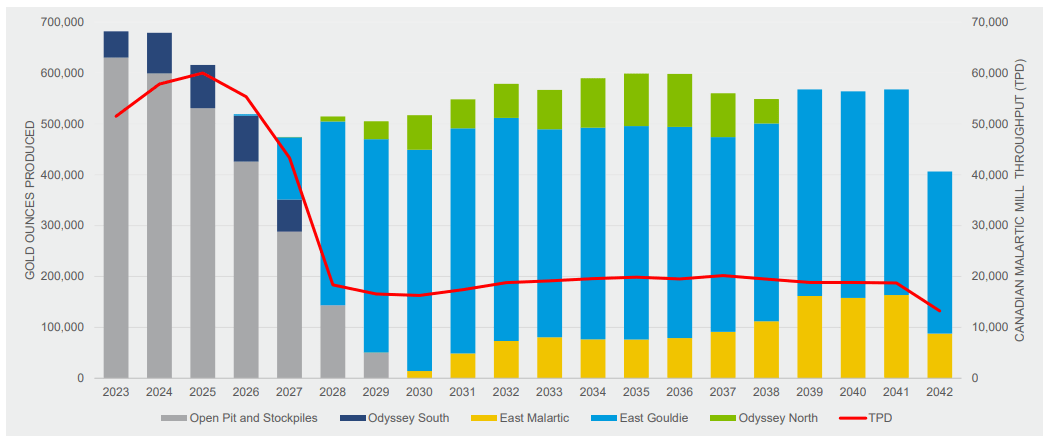

Simultaneously, Canadian Malartic's open-pit is being depleted while the company works to bring the more productive and higher-grade East Gouldie Mine online (part of the Odyssey Project), with Canadian Malartic's production set to decline to ~500,000 ounces from 2026-2029 without further optimization under the updated life-of-mine plan. This is a nearly 200,000 ounce headwind from 2024 levels, and while not nearly as impactful, La India in Mexico is also set to head offline in 2025. Finally, although Detour Lake has the potential to be a 1.0 million ounce per annum asset, 2026-2029 are expected to be lower-grade years for the mine. And even if we see throughputs closer to 29.5 million tonnes at Detour Lake (28.0 million tonnes assumed in 2022 TR), production should average ~690,000 ounces in the period, an additional headwind in this same 2026-2028 period.

Detour Lake Life Of Mine Plan - Company Filings Canadian Malartic Life Of Mine Plan - Company Website

{kind=link}

{kind=link}

So, is decline in production a big deal?

While it looks like Agnico Eagle could see production slip to ~3.1 million ounces in 2027/2028 if the company doesn't acquire another producing asset, production is set to come roaring back at the end of the decade and could grow ~30% from the 2027/2028 trough looking out to 2030/2031 depending on the sequencing of projects. This is because Detour has the potential to be a ~1.0 million ounce per annum asset if the company green-lights Detour Underground and can take fully advantage of the ~32 million tonnes per annum of permitted capacity (currently operating closer to ~26 million tonnes per annum). Meanwhile, Canadian Malartic is a ~550,000 ounce producer while utilizing just one-third of capacity, and between Camflo, near-mine opportunities and future spokes (Upper Beaver/Wasamac alone could deliver a combined ~380,000 ounces) transported by rail to the hungry mill, the complex could also produce ~1.0 million ounces per annum.

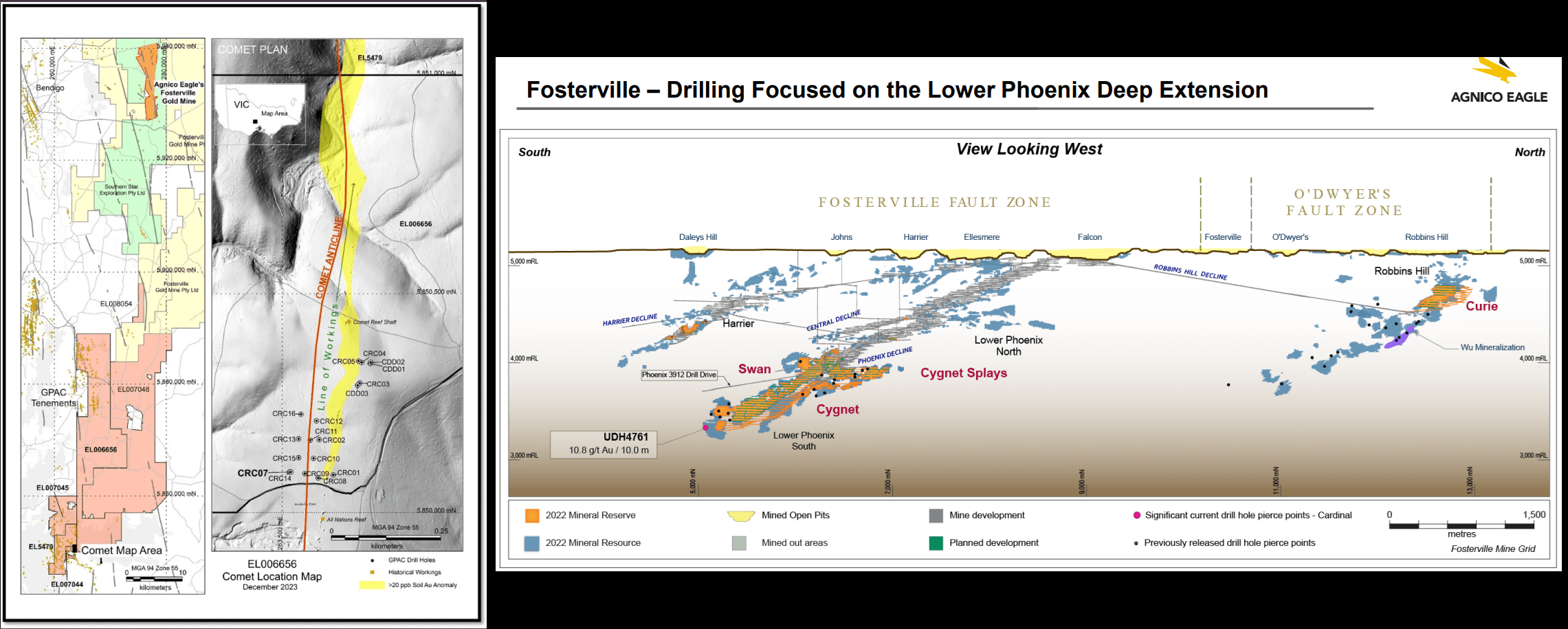

On top of these organic growth opportunities, the company could produce upwards of ~250,000 GEOs if it green-lights San Nicolas in Zacatecas, Mexico (same state where Penasquitoa, Juanicipio, La Colorada and Camino Rojo operate). In addition, the compay's Hope Bay Project (previously in operation) was bought for a song and has 350,000+ ounce per annum potential. Finally, while there's no guarantees, a new high-grade discovery at Fosterville could certainly bring this asset back into the picture (currently expected to produce at just ~200,000 ounces), and the recent Comet discovery south of Fosterville by Great Pacific Gold (5 meters at 166 grams per tonne of gold) suggests this area of Bendigo in Australia may have more left in store both south of Fosterville and on the company's existing tenements. Obviously, one hole does not make a new discovery, but I continue to be cautiously optimistic regarding a new high-grade discovery at Fosterville which could provide a lift to production later this decade.

Great Pacific Comet Prospect & Agnico Eagle Drilling Fosterville - Agnico Eagle Website, Great Pacific Gold Website

{kind=link}

And while on the topic of Fosterville, Agnico continues to have exploration success at depth at Lower Phoenix, hitting 10.8 grams per tonne of gold over 10.0 meters in the Cardinal splay at 1,830 meters depth, 190 meters down-plunge from its current mineral reserve base. The Cardinal Zone was initially identified in 2022 by Agnico Eagle in the hangingwall of Lower Phoenix with intercepts of 1.1 meter at 365.5 grams per tonne of gold (1,680 meters depth), 1.4 meters at 226.2 grams per tonne of gold (1,715 meters depth), and 2.9 meters at 168.6 grams per tonne of gold (1,680 meters depth), so this new visible gold intercept is the deepest at Cardinal to date.

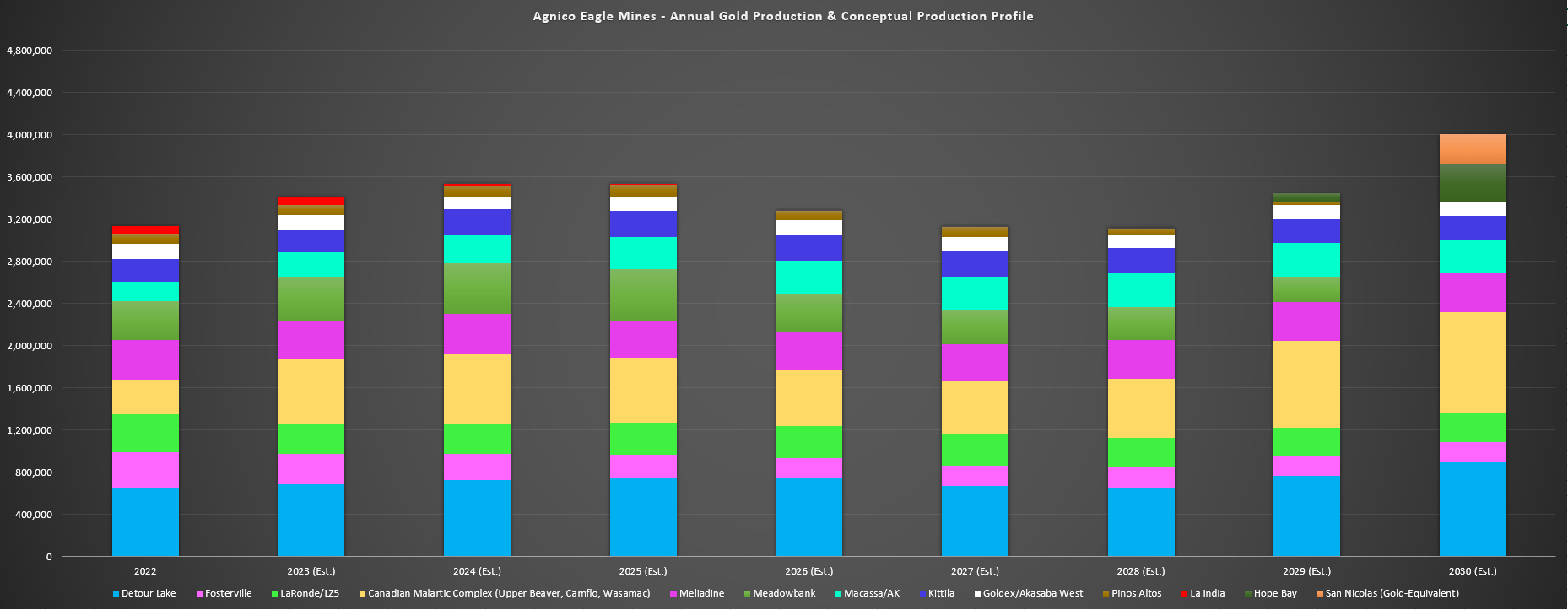

Agnico Eagle - Annual Gold Production & Conceptual Production Profile (2022-2030) - Company Filings, Author's Chart & Estimates

{kind=link}

Taking all of this into consideration, a conceptual look at Agnico Eagle's production profile looking out to 2030 is shown above, and we can see that 2024 and 2025 should be two significant years of free cash flow generation before a slight drop off in output in 2026-2028. However, production could increase to 3.9+ million ounces in 2030 with Hope Bay and San Nicolas (50%). And while multiple growth projects (Detour Underground, Wasamac/Upper Beaver, San Nicolas (50%), Hope Bay) might seem like a lot to take on at once, it's important to note that these are shared capex and/or relatively low capex opportunities vs. building a massive stand-alone greenfields operation like Cote with a $2.5+ billion capex bill.

Why? Hope Bay benefits from existing infrastructure, San Nicolas is shared with Teck Resources ( TECK ), and Hope Bay/Wasamac already have a home for their ore if mines are developed at both sites. Hence, this is not like the company is building three Cote's or three Greenstone's at once which would be unreasonable, and it certainly has the cash flow to support this growth with the potential for ~$1.5 billion in free cash flow in 2025. The last point worth noting is that while growth may appear to lag some of Agnico's peers, the difference is that Agnico hasn't seen its growth drop off materially from 2019-2022 and is having to grow from a high watermark vs. a low watermark such as larger gold producers whose production peaked last decade (shown below).

Major Gold Producers Annual Gold Production - Company Filings, Author's Chart

{kind=link}

Finally, while gold production may decline from the expected peak in 2024/2025 to 2027/2028, it's quite possible that we could see similar revenue and cash flow generation if the gold price can finally enter a new bull market. And if Agnico really wanted to, it could plug this gap overnight with a bolt-on acquisition of a relatively low capex or already producing 300,000+ ounce per annum asset. To summarize, I don't see this production cliff as an issue to the investment thesis, but there's no question that the company has some optimization work to do to smooth out this profile as much as possible. The good news is that exploration success at multiple assets continues to come in at or above expectations, allowing other assets to maintain production profiles and extend their mine lives.

NIRB Report On Meliadine Expansion Project

Agnico Eagle responded to the Nunavut Impact Review Board [NIRB] earlier this month in relation to its Meliadine Mine (one of its largest operations producing ~400,000 ounces of gold per annum), with its response being to the NIRB's conclusion to not allow the Extension Proposal at Meliadine to proceed at this time given that "the potential for significant adverse ecosystem and socio-economic effects cannot be adequately managed and mitigation".

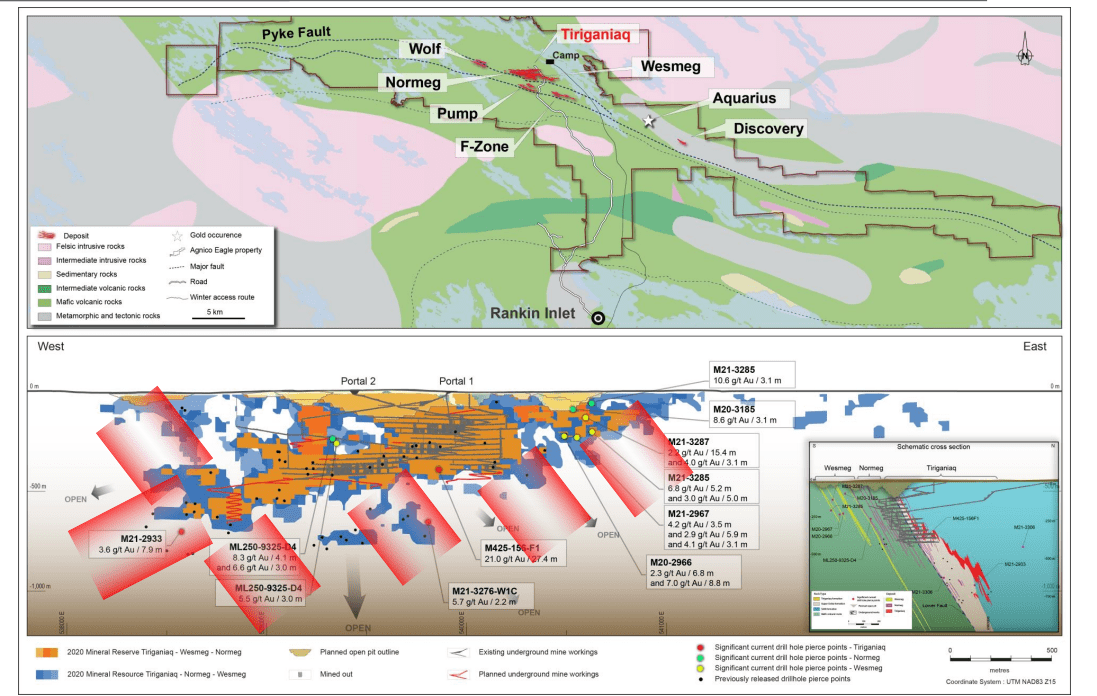

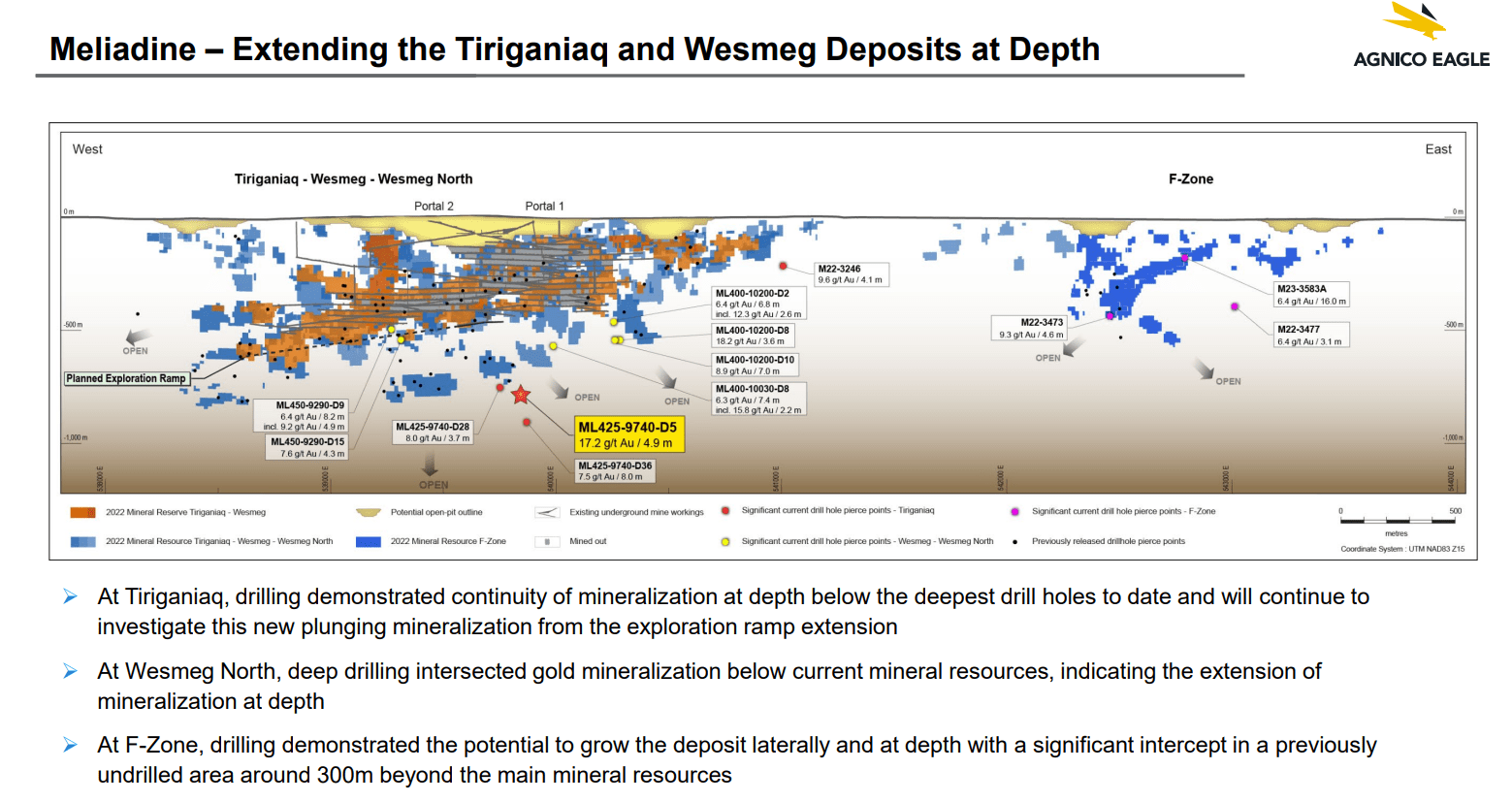

Images below highlight Agnico Eagle's land package, regional targets, and exploration success/upside on its massive Meliadine land package next to current reserves at Tiraganiaq, Wesmeg, and Wesmeg North.

Agnico Eagle Meliadine Mine & Exploration Highlights - Company Website Agnico Eagle Meliadine & Exploration Success - Company Website

{kind=link}

{kind=link}

To provide some background on the asset, Agnico Eagle's current mine plan at Meliadine runs until 2032 (commercial production began in 2019), and the company has been a massive contributor from an economic standpoint to Nunavut with its two mines (Meadowbank/Meliadine) over the past decade and a half. The plan was to extend Meliadine's mine life from 2032 to 2043 and the company had planned for an increase in throughput from ~4,500 to ~6,000 tonnes per day, with this expected to be completed by year-end 2024. However, the NIRB's recent decision to not allow this to proceed for the time being has certainly thrown a temporary wrench in these plans.

Agnico Eagle's response was that it was "surprised and disappointed" , especially considering the lost economic benefit from Meadowbank, which is starting to run short on mine life. In fact, Meadowbank's operations should head offline by the end of this decade even if the company goes ahead with a planned pushback to extend production past 2027. Obviously, this will have a significant impact on Nunavut's GDP, with one of its two major mines in Nunavut already set to go offline later this decade and Agnico also stated that it is withdrawing its proposal for the Meliadine Extension immediately, but that it is not ruling out the submission of a new application at a later date when conditions are suitable.

Regarding the NIRB's decision, Agnico pointed to several inconsistencies, and it looks there was some miscommunication of extension plans in the report. The issues raised are surprising regarding the issues with the Meliadine Extension with one sticking point being the effects on caribou migration even though the effects have actually been less than predicted initially a decade ago, and Agnico has been very accommodating at its operations with the mine shutting down for between 9-28 days in past years (all-weather access road and surface restrictions) to ensure no impact to caribou migration. Another sticking point in approving the Meliadine Extension was the proposal of a wind farm, but this was not an essential component of the planned extension.

The pushback related to the planned wind farm was that this would be the first wind farm that the caribou herd would be exposed to and it's unclear what negative effects this could have on the herd. Agnico Eagle pointed to wind farms at the Raglan and Diavik mines being directly comparable, and that no adverse impacts were identified for caribou at these operating wind farms in Nunavut. An additional sticking point discussed by the NIRB was related to worries about adding additional roads and water lines, but this is not relevant as the Discovery Site and Discovery Road are already part of the permitted project under the previous Project Certificate 006 (granted in 2015).

Third, while the project will be expanded, there will be minimal additional surface disturbance as mining will take place at the F Zone, Pump, and Discovery (portals/vent raises already within the previously approved footprint) and underground waste rock piles are within the amounts approved in the 2014 FEIS. Plus, there will actually be a reduction in waste rock storage facilities on surface as part of the Meliadine Extension, as well as a decreased TSF footprint with 13.4 million tonnes to be used underground. Finally, the overall increase in the permitted footprint is a mere 190 hectares (vs. 3,369 hectares already approved), so this is hardly a meaningful increase such as doubling the footprint where it might be reasonable to expect some pushback and not wanting to approve the project immediately.

Reconsideration Report Errors & Comments - Agnico Eagle Response to NIRB Recommendation

{kind=link}

There was several other inaccuracies that Agnico Eagle pointed out from the Reconsideration and Recommendation Report and the company also noted that there were procedural issues including that the full sitting board of NIRB members did not participate in the vote, the admission of late filings caused confusion, and although the NIRB confirmed that the application met information requirements, it contradicted itself in the report by stating that insufficient information was available. To summarize, this appears to more of a misunderstanding between the two parties (Agnico Eagle & NIRB) rather than hostility against Agnico Eagle, and the benefits (or lost economics benefits if not approved) are massive with Meadowbank already set to head offline later this decade.

Overall, Agnico is no stranger to permit delays/issues (Kittila, Fosterville which slightly weighed on sentiment and valuations for these mines over the past year), but both permits were since approved and I would expect the Meliadine Extension to be approved as well. In addition, Agnico Eagle contributes over 25% to the GDP of Nunavut, has paid nearly $300 million in employment income to Inuit employees since 2010, has invested significantly in the community while investing just shy of $10 billion in Nunavut to date. Hence, this is not a case of a lack of community support or a severe environmental issue that has changed the outlook for the asset, and Agnico has always been one of the best operators of the best sector-wide for taking care of employees, its community, and being a responsible operator in regards to environmental impacts/wildfire.

As an example, it paid its Nunavut employees to stay home (75% of their salaries during COVID lockdowns) because of the more fragile healthcare system in Nunavut.

Overall, the recent decision by the NIRB is certainly a negative development short-term and could impact planned production from Meliadine in 2025/2026. In addition, it's not ideal to have added uncertainty around a major mine when the company is already working hard to offset depletion from the Canadian Malartic Open Pit, Meadowbank, La India, and lower production from Fosterville as grades have normalized after several years of . That said, I ultimately expect this to be resolved in the company's favor, but it is certainly a development worth monitoring going forward.

Valuation & Technical Picture

Based on ~496 million shares and a share price of US$54.90, Agnico trades at a market cap of ~$27.2 billion and an enterprise value of ~$28.8 billion, making it one of the highest capitalization names in the sector. This is certainly justified given that it's the third largest gold producer globally, and the company has a significantly more favorable jurisdictional profile than its peers with over 95% of 2024 production coming from Tier-1 ranked jurisdictions. Meanwhile, Agnico Eagle has the best per share growth metrics among its multi-million ounce producer peers, and also boasts the highest margins, with FY2025 all-in sustaining cost margins set to come in near 50% assuming a $2,000/oz gold price. In my view, this justifies a premium relative to peers, especially given the more volatile environment from a jurisdictional standpoint that has led to divestments and some assets heading offline (Kupol, Boungou, Cobre Panama, etc.).

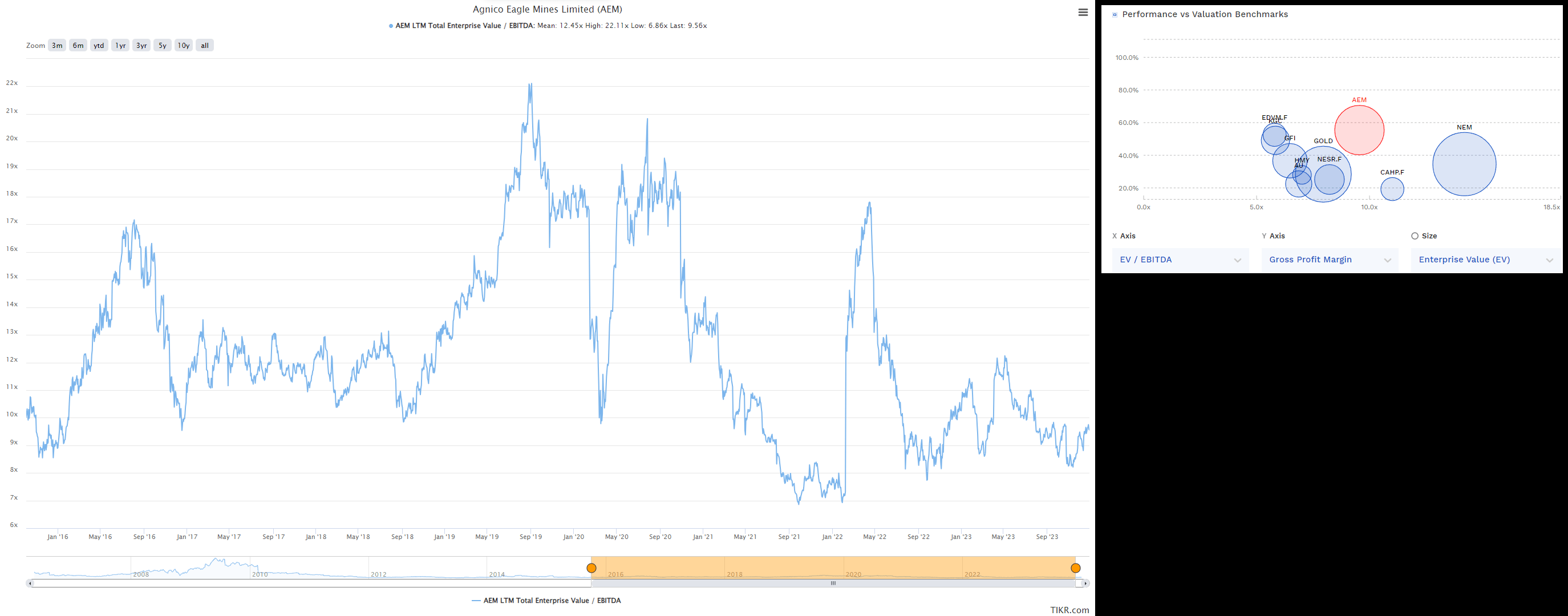

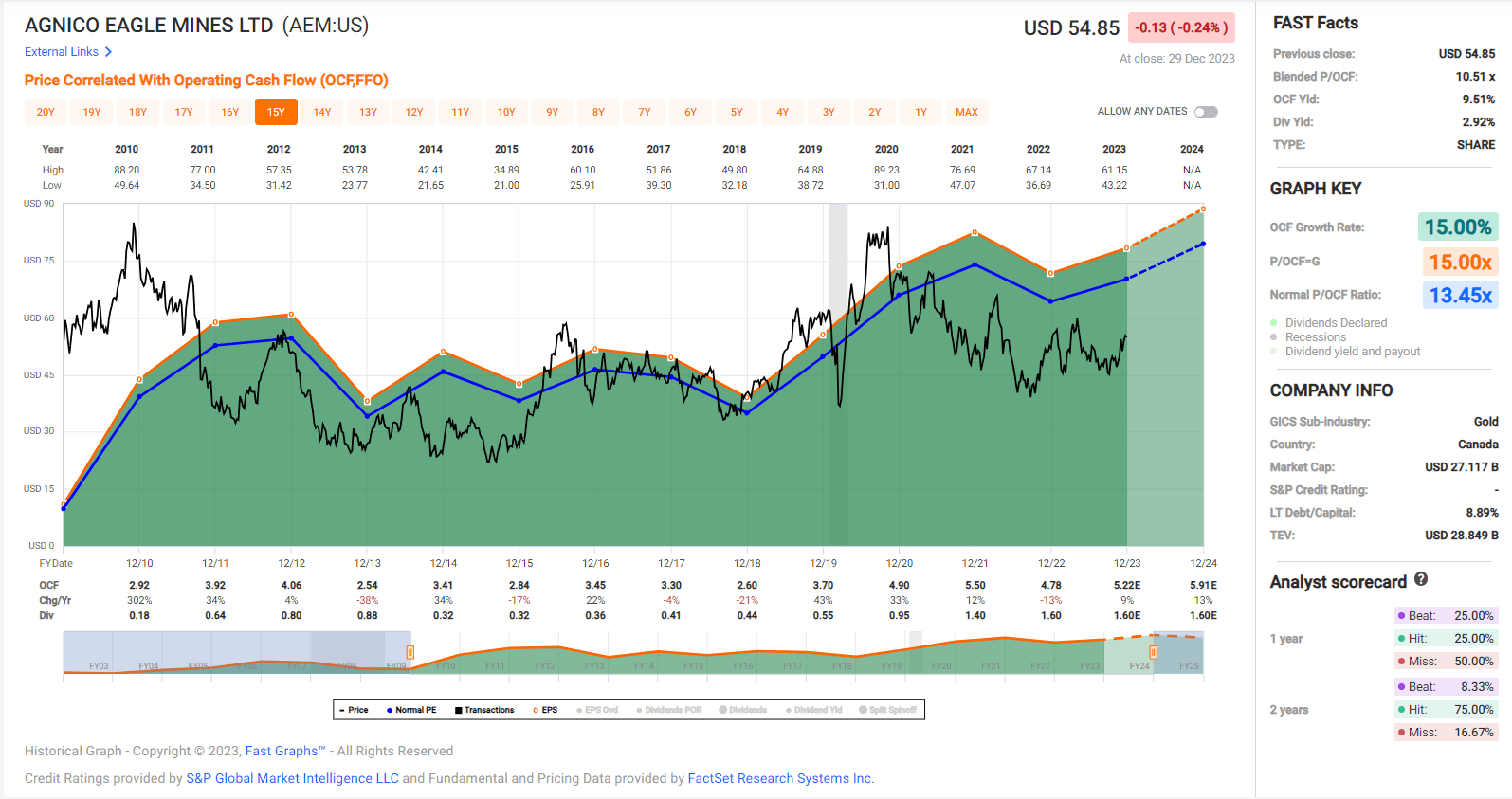

Agnico Eagle EV/EBITDA Multiple vs. Peers/Historical Multiple & Margins - TIKR, FinBox Agnico Eagle - Historical Cash Flow Multiple - FASTGraphs.com

{kind=link}

{kind=link}

Looking at how the stock's valuation stacks up relative to peers, Agnico is one of the more expensive names (largely justified by its superior margins, scale, jurisdictional profile and consistent per share growth), but we can also see that it trades at a significant discount to where it has since the secular bear market for gold ended in 2015. Meanwhile, the stock also remains reasonably valued from a price to cash flow standpoint, sitting at just ~9x FY2024 cash flow per share estimates vs. a historical multiple of ~13.4x (15-year average). And even if we use more conservative multiples of 1.40x P/NAV and 11.5x cash flow and a 65/35 weighting (P/NAV vs. P/CF), I see a fair value for the stock of US$69.00. This points to a 25% upside from current levels or closer to a 28% upside on a total return basis when including its ~3.0% dividend yield.

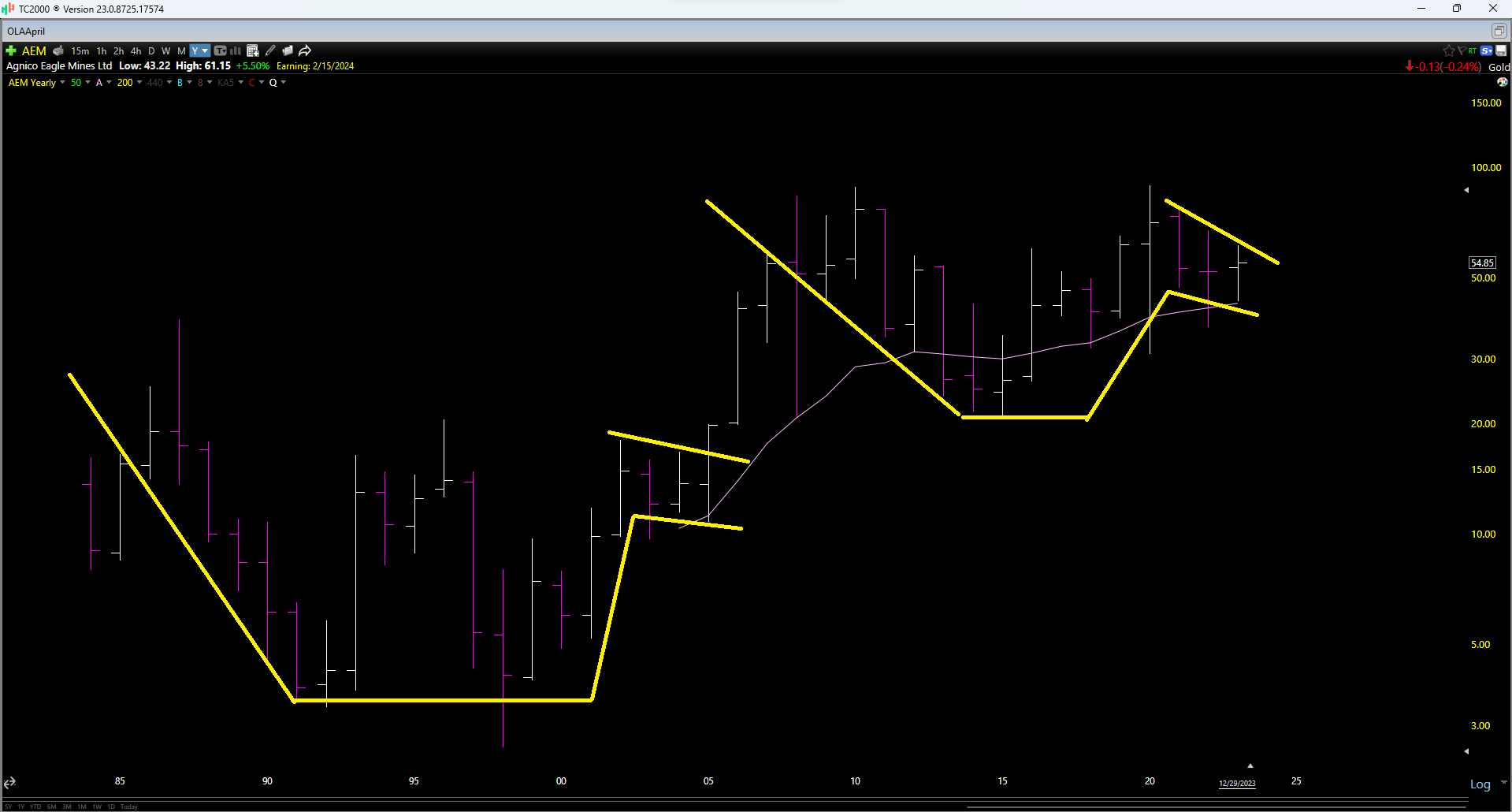

As for the technical picture, investors have bid up high-flying retail and tech names to levels of significant extension past their most recent base breakouts, with names like Elf Beauty ( ELF ), Nvidia ( NVDA ), Super Micro Computer ( SMCI ), and Costco ( COST ) up between 70% and 250% last year alone. However, if one is willing to shop around in different sectors, names like Agnico Eagle ( AEM ) are quietly building decade long cup and handle bases, with the current base in Agnico Eagle being quiet similar to the one that sent the stock up ~350% in barely three years from its 2005 breakout. Given the size of the company relative to 2005, I would not expect a repeat from a percentage standpoint. Still, if the stock does breakout of this base, the measured move would easily exceed its previous highs of $90.00 per share, pointing to significant potential upside from current levels.

{kind=link}

Some investors might question what the catalyst would be for Agnico Eagle to head back to new all-time highs, but as I've pointed above, the stock actually trades at a very reasonable valuation today and well below the ~20x cash flow multiple that it traded at its 2020 peak. This is despite the fact that the company has a stronger pipeline, a larger production profile and has held the line on costs better than peers. Plus, Tier-1 jurisdiction operators have never been in more demand after we just saw one of the largest copper mines taken offline in Panama which had led to enormous losses for First Quantum ( OTCPK:FQVLF ) investors. Hence, even if the stock traded at ~15x cash flow which isn't that much of a stretch given the premium that Tier-1 operators should command, this would translate to a share price of ~$90.00 based on FY2024 estimates.

Summary

Agnico Eagle has had another transformational year in what's been a transformational decade for the company and its 2024 results should be even better. This is evidenced by the company gaining 100% ownership of two ~700,000 ounce per annum assets with each asset having the potential to operate ~1.0 million ounces per annum in an upside case scenario. The fact that these are Tier-1 jurisdiction operations is a massive advantage for investors that want a "sleep-well-at-night" investment, and the company's robust pipeline outside of these assets (San Nicolas 50%, Hope Bay, Hammond Reef optionality, Upper Beaver/Wasamac as spokes for Canadian Malartic) means Agnico Eagle is not desperate for M&A to grow and should be able to grow into a ~4.0 million ounce producer by 2030.

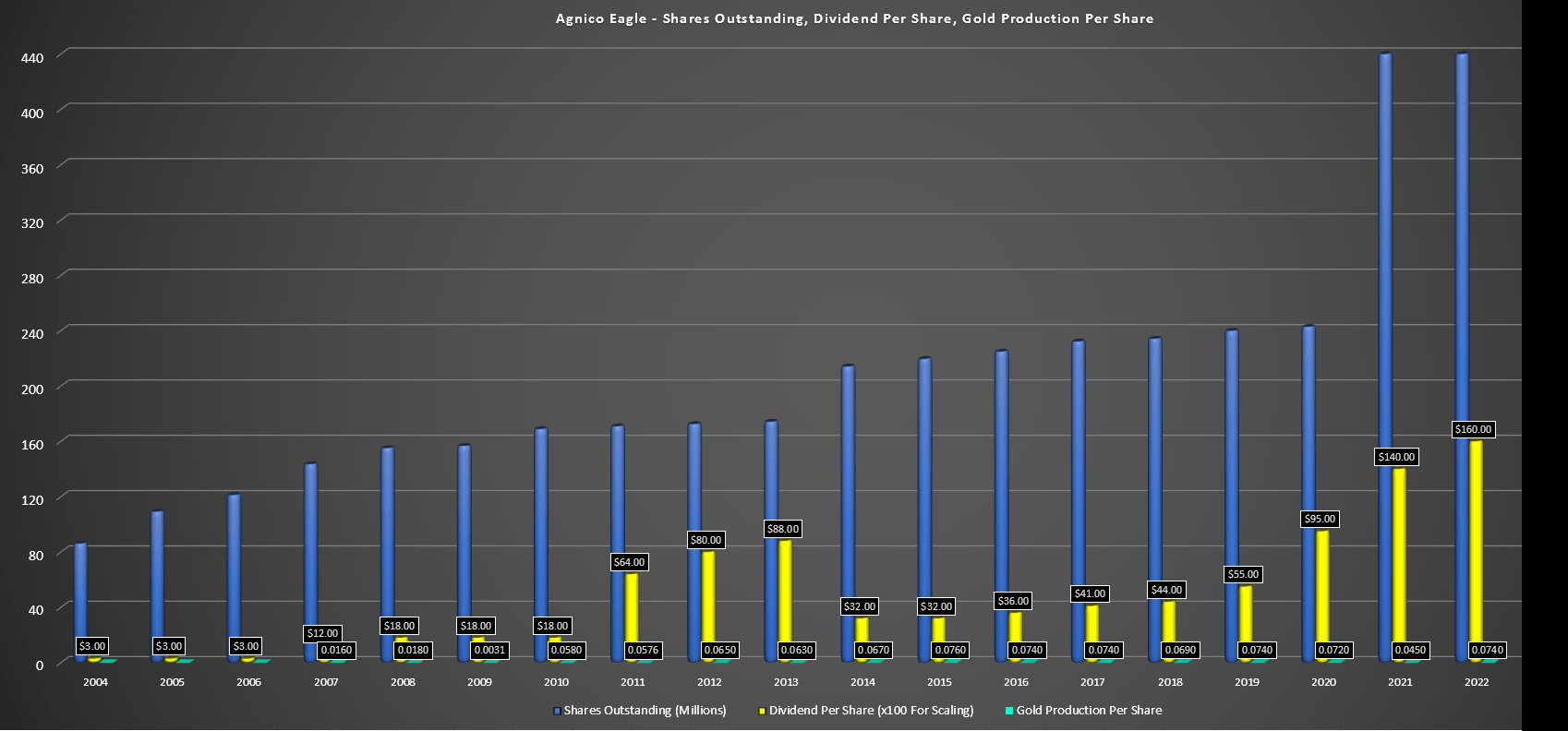

Agnico Eagle Shares, Dividend Per Share & Production Growth Per Share - Company Filings, Author's Chart

{kind=link}

While this may not make Agnico the biggest producer, the company's discipline and laser focus on staying true to its model (regional miner) and per share growth make it arguably the best producer, and also one of the most consistent names from an income standpoint with a dividend that's grown at a higher pace (24% compound annual growth rate) than many Dividend Aristocrats. Finally, the company has a phenomenal track record of adding value to its mining assets, and being one of the most aggressive drillers in the sector has paid off by extending mine lives and not needing to do over-priced M&A like some of its peers to fill gaps in its production profile (ultimately affecting other producers' per share growth).

In summary, with a very reasonable valuation, a bright future ahead, and a disciplined team at the helm, I see Agnico Eagle as a staple for any precious metals portfolio, and I would view any sharp pullbacks as buying opportunities.

For further details see:

Agnico Eagle Mines: A Stronger Year On Deck