AEM - Agnico Eagle Mines: Another Blowout Quarter In Q2

2023-07-27 15:33:16 ET

Summary

- Agnico Eagle Mines Limited reported record gold production of ~873,200 ounces in Q2, despite operational challenges such as wildfires and power outages.

- The company's costs came in below expectations due to easing inflationary pressures, and revenue soared with help from the gold price.

- With Agnico Eagle continuing to be one of the only gold producers consistently growing its per share metrics, I would view sharp pullbacks as buying opportunities.

It's been a mixed Q2 Earnings Season for the VanEck Gold Miners ETF ( GDX ), with several large producers coming out of the gate with weaker than expected results, including Newmont ( NEM ) and Evolution Mining ( CAHPF ). However, #3 gold producer Agnico Eagle Mines Limited ( AEM ) certainly bucked this trend, reporting record gold production of ~873,200 ounces, a nearly 2% increase from the year-ago period. Notably, this performance was achieved despite headwinds from cancelled shifts in Ontario/Quebec related to wildfires and two significant power outages, and a tougher quarter in Nunavut with an extra-long caribou migration season that contributed to a 15-day mill shut (Meadowbank) and 11 days of downtime (Meliadine).

More importantly, it was another record quarter for safety. Finally, Agnico's costs came in below expectations due to the continued easing of inflationary pressures, and revenue soared with AEM finally getting some help from the gold price. Let's take a closer look below:

All figures are in United States Dollars unless otherwise noted.

{kind=link}

Q2 Production & Sales

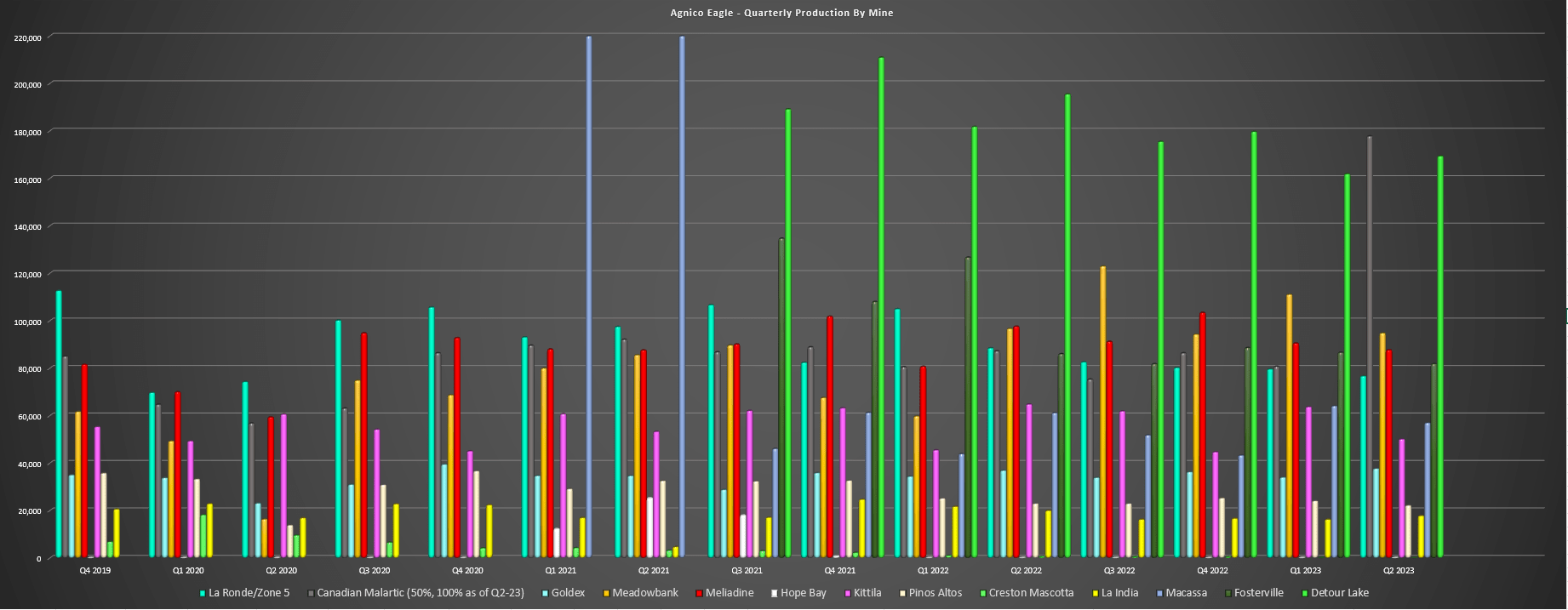

Agnico released its Q2 results this week, reporting quarterly production of ~873,200 ounces of gold, an increase from ~858,200 ounces of gold in Q2 2022, and what represented a record quarter for the company. And while this was only a slight increase on a year-over-year basis despite acquiring the other half of one of the world's largest gold mines (50% ---> 100% ownership of Canadian Malartic), Agnico was up against difficult comps on a year-over-year basis and saw headwinds in the period that affected production.

For starters, Detour Lake had a monster quarter in Q2 2022 (~195,500 ounces due to benefiting from higher-grade feed), LaRonde had an ~89,000-ounce quarter before the change to the mining sequence announced earlier this year, and Meliadine also had a huge quarter with ~97,600 ounces produced. Finally, it was an exceptional for Kittila, which benefited from record mill throughput and produced ~65,000 ounces. So, given the impact from wildfires and caribou migration combined with a tough quarter it had to lap, the ~2% increase in output was quite impressive.

Agnico Eagle Mines - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

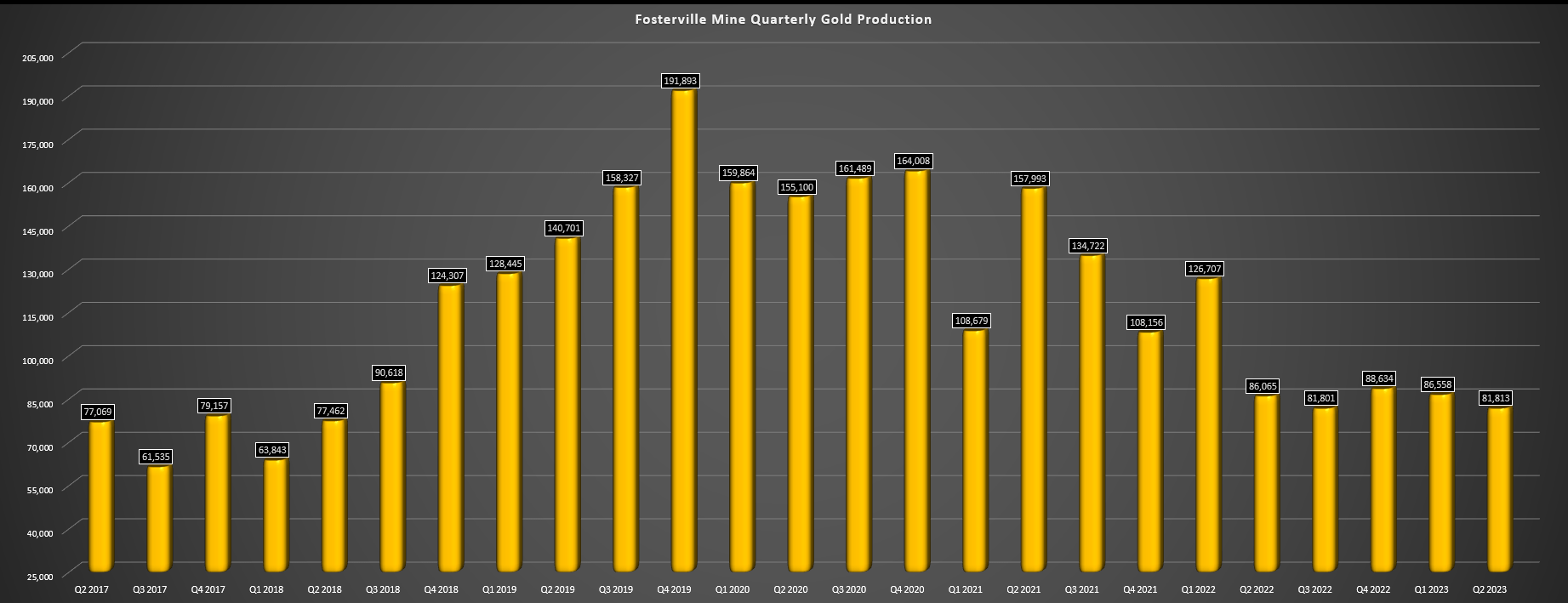

Starting with one of the company's newer mines, Fosterville, it was a soft quarter with production of ~81,800 ounces of gold, a 5% decline from the year-ago period. The decline in output was related to lower grades in the period (14.77 grams per tonne of gold vs. 22.24 grams per tonne of gold), with Fosterville also lapping a tough comparison from Q2 2022, with the drop in grades related to being in a lower-grade area (mining sequence) and lower grades than planned in a specific area of the Swan Zone. And given that this shortfall was made up by increased throughput and we saw inflationary pressures (consumables) on a year-over-year basis, cash costs increased to $436/oz (Q2 2022: $377/oz), but these costs still remained near the lowest levels sector-wide, with cash cost margins above $1,500/oz.

Fosterville Mine - Quarterly Production (Company Filings, Author's Chart)

{kind=link}

The silver lining to the softer Q2 performance was that the Victorian Environmental Protection Authority [EPA] has lifted restrictions on the mine that resulted in surface fans having to be offline from midnight to 6 AM, which affected the asset's mining rates. This should benefit FY2024 production, which was previously guided at 240,000 ounces, and this positive news may prompt Agnico to direct some more capital towards this asset, with it making less sense to be aggressive on exploration when dealing with headwinds that severely impacted its mining rates. Hence, although Q2 production was lower because of lower than expected grades, I don't see this as an issue as this is an asset that has historically outperformed expected grades and the much bigger news is the lifting of restrictions at this ultra high-grade underground mine.

Moving over to Meadowbank, Agnico produced ~94,800 ounces of gold (Q2 2022: ~96,700 ounces of gold) at cash costs of $1,156/oz vs. $993/oz in the year-ago period. The lower production was related to a 15-day mill shut related to longer than usual caribou migration which resulted in road closures and impeded transportation of fuel and ore, and resulting in a 19% decline in ore processed.

However, if not for these headwinds, it would have been a massive quarter with grades up ~9% to 3.79 grams per tonne of gold, development rates above expectations and the benefit of the newly commissioned high pressure grinding rolls. In regards to costs, mining and fuel costs were up due to underground mining at Amaruq and higher fuel prices, partially offset by a weaker Canadian Dollar in the period. And while mine production was affected, stockpiles helped to offset the impact in the period.

{kind=link}

As for Meliadine, production was down over 9% to ~87,700 ounces of gold (Q2 2022: ~97,600 ounces), with the mine also impacted by the longer than usual caribou migration (affected open pit and paste plant). However, unlike the Meadowbank Complex which benefited from higher grades, Meliadine was up against tough comps from a grade standpoint, and the combination of lower grades and only marginally higher throughput (~461,000 tonnes) resulted in higher costs and lower production in the period. That said, plant performance continues to be exceptional with record mill throughput in May and these figures will improve further in the next 18 months with a plan to increase throughput to 6,000 tonnes per day by year-end 2024. As for costs, they increased to $1,019/oz (Q2 2022: $837/oz) related to higher fuel prices and consumption of stockpile inventory.

Moving away from Nunavut to its largest operations, LaRonde saw a meaningful decline in production (~76,800 ounces vs. ~88,500 ounces) related to lower throughput and grades with a change in its mining method (pillarless mining) announced earlier this year, which is contributing to a lower mining rate. The result of lower production and higher mining costs due to increased labor and materials costs resulted in increased cash costs in the period ($884/oz vs. $649/oz), with a further impact in costs from the timing of concentrate sales. That said, even at this lower production, this is still a meaningful contributor for Agnico and it should benefit from concentrate from Akasaba West (expectations of Q1 2024 commercial production) and potentially Amalgamated Kirkland in the future to leverage its excess processing capacity.

{kind=link}

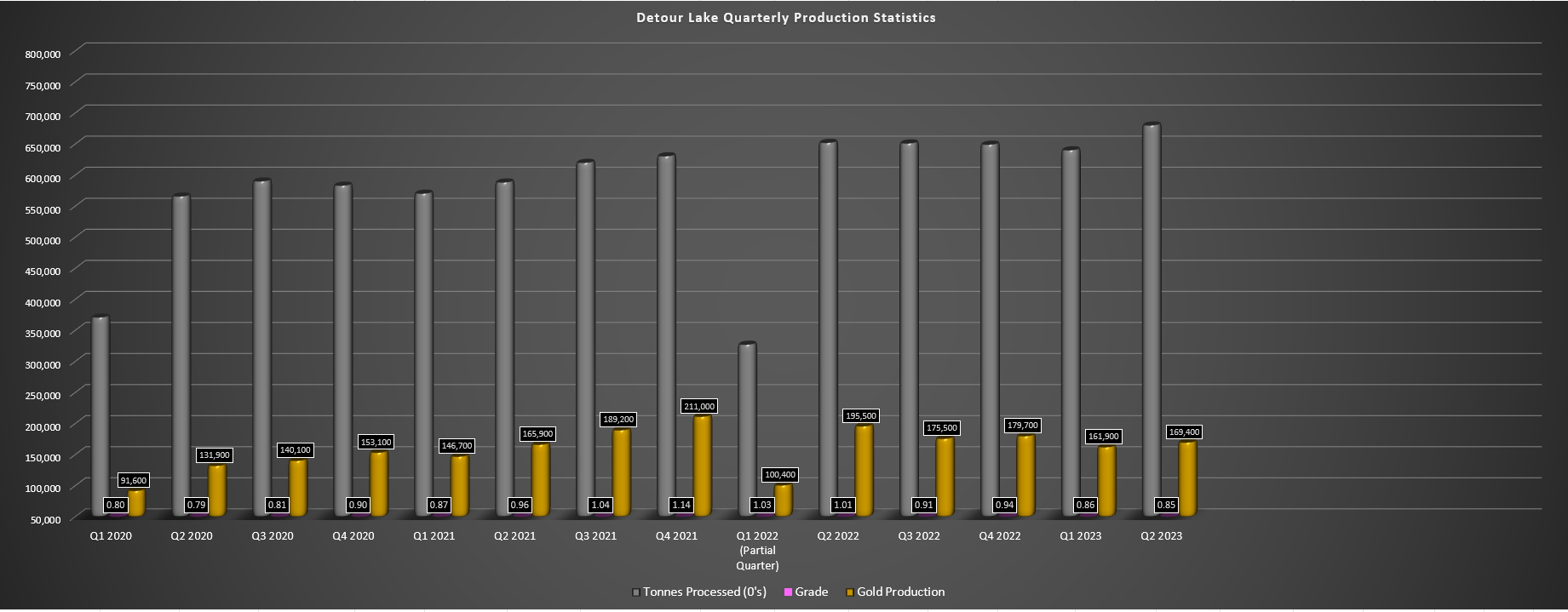

As for Quebec and Ontario, Canadian Malartic and Detour Lake both had solid quarters. At Canadian Malartic, production came in at ~177,800 ounces vs. ~87,200 ounces, reflecting the full ownership of the asset in the period vs. 50% last year. Production benefited from higher throughput that was offset by marginally lower grades, and the mine produced its seven millionth ounce of gold, an incredible feat. During the quarter, the Canadian Malartic Pit was depleted, with work underway for in-pit tailings disposal in 2024. As for Detour Lake, the mine reported record mill throughput of ~6.8 million tonnes, benefiting from improved mill availability of 92.8% which was just shy of the 93% goal outlined in the 2020 TR. Notably, Agnico continues to reiterate that it believes it can reach and potentially its first major target of 28 million tonnes per annum throughput levels. During the quarter, Detour Lake produced ~169,400 ounces of gold, with the increased throughput offset by lower grades related to the mining sequence (0.85 grams per tonne vs. 1.01).

Detour Lake - Quarterly Production & Stats (Company Filings, Author's Chart)

{kind=link}

In addition to solid performance and reiterating a potential beat on its 28 million tonne per annum first major throughput target, Agnico noted that it's looking at the potential for ore sorting and implementation of advanced process control which would utilize AI or expert systems to deliver above the 28 million tonne per annum goal. And based on encouraging 2022 results, Agnico has initiated an ore sorting pilot test which will inform the viability of a larger sorting operation at this monster mine that could ultimately be a 1.0 million ounce producer one day. Finally, the company continues to enjoy exploration success in the West Pit extension area, with some highlight intercepts of 14.4 meters at 2.8 grams per tonne of gold, 2.4 meters at 26.7 grams per tonne of gold, 2.5 meters at 81.4 grams per tonne of gold, and 22.8 meters at 3.7 grams per tonne of gold. This success has prompted a $5.2 million increase in its 2023 exploration budget with increased drilling aimed at accelerating the delineation of underground mineral resources west of the West Pit.

Finally, looking at the company's smaller operations, Kittila produced ~50,100 ounces of gold with production impacted by autoclave maintenance, which was only partially offset by slightly higher grades. However, the asset could be set up to deliver bonus ounces above guidance (~30,000 ounces) in H2 if the SAC reinstates the company's 2.0 million tonne per annum operating permit.

Elsewhere, Macassa saw lower production year-over-year with ~57,000 ounces produced due to lower grades related to mine sequencing. However, the mill reported record throughput in the quarter and with the commissioning of Shaft #4 and improved productivity from the Macassa deep mine, the mill is expected to reach full capacity of ~600,000 tonnes per annum by mid-2024. And in addition to record mill throughput, the mine reported record tonnes hoisted and record underground development, with improved working conditions (ventilation) with the second of two 3,000 horse power fans commissioned in the quarter.

To summarize, it was a solid quarter overall for Agnico with several positive developments, including record mill throughput at multiple assets, solid progress on organic growth projects at key assets (Detour Lake, Macassa, Meliadine) and all of this achieved with exceptional safety performance, evidenced by the best safety performance in any H1 in its 65+ year history. This strong safety performance has followed what was a record year for safety performance in 2022, and the LaRonde Complex also reported its best quarterly safety performance overall in a decade. Just as pleasing, revenue hit record levels of ~$1.72 billion, with Agnico finally getting some help from the gold price, reporting a realized price of $1,975/oz in the period. This resulted in ~$300 million in free cash flow in Q2, and helped the company end the quarter with just ~$1.5 billion in net debt despite coming off two major deals (Yamana Canada, Kirkland Lake Gold).

Costs & Margins

As for Agnico's cost and margin performance, the company excelled in this category as well, benefiting from favorable exchange rates and easing inflationary pressures. The company called out relief on some consumables (primarily energy), the benefit of hedging a large portion of diesel, with diesel exposure for the remainder of H2 2023 at $0.69/liter (below budget of $0.93/liter) by being patient and waiting for costs to come down from last year's elevated levels.

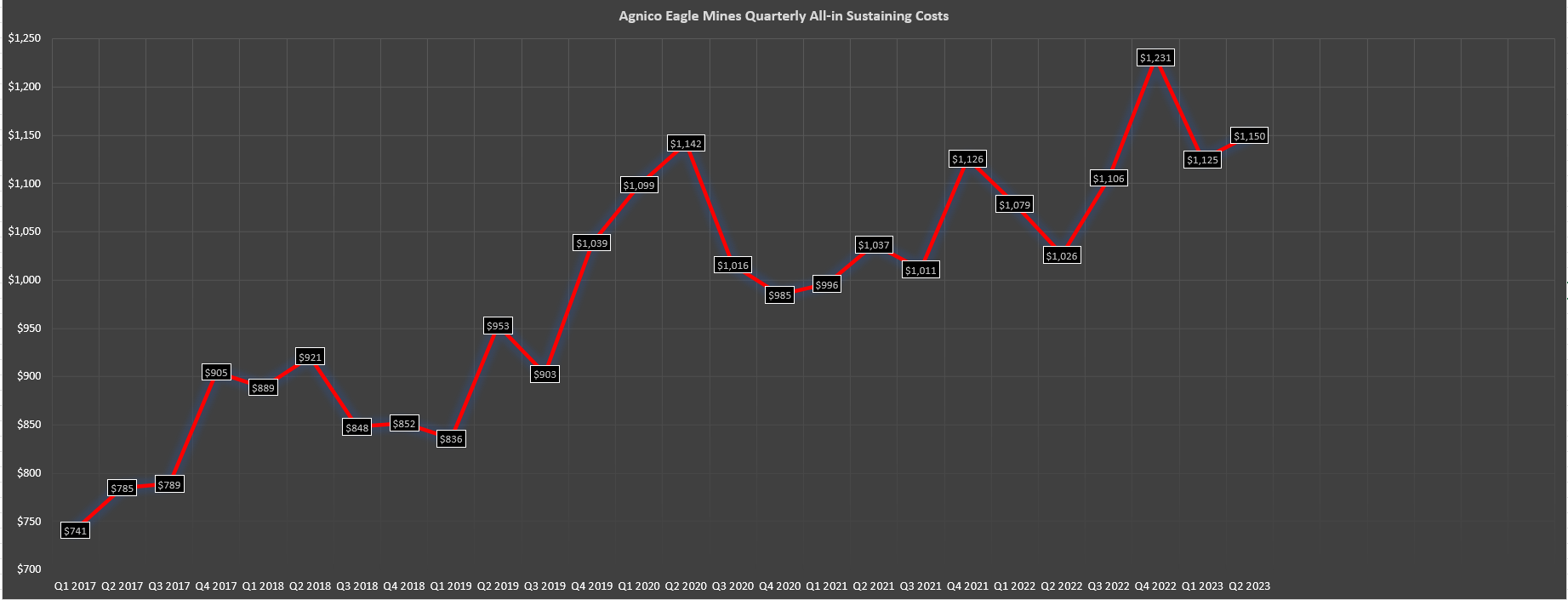

Elsewhere, costs have improved for steel and cyanide, and the company is starting to see improved availability and performance of drillers. The result was that despite higher sustaining capital on a year-over-year basis, all-in sustaining costs came near industry-leading levels for million-ounce plus producers of $1,150/oz, and costs are tracking well against guidance of $1,140/oz to $1,190/oz for the year (year-to-date AISC of $1,138/oz).

Agnico Eagle Mines - Quarterly AISC (Company Filings, Author's Chart)

{kind=link}

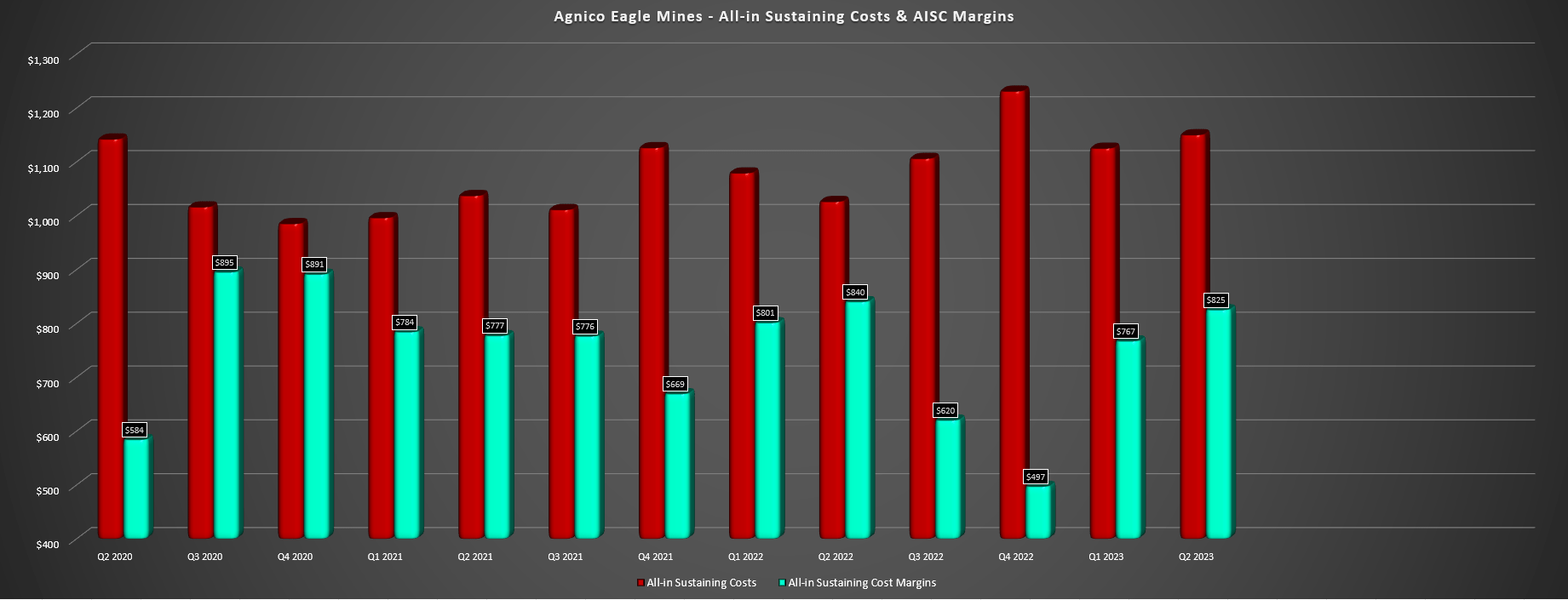

As for Agnico's margins, AISC margins improved to $825/oz, down slightly year-over-year (Q2 2022: $825/oz), but up significantly on a sequential basis vs. Q1 2023 ($767/oz). This was primarily driven by the increase in the gold price to $1,975/oz, and while the company may not benefit from a gold price this strong in H2 2023, we should see a similar cost performance, meaning that Agnico will maintain margins well above the industry average for the year (~$780/oz assuming $1,925/oz average realized gold price in FY2023) vs. $600/oz for the universe of all gold producers.

And while it's unfortunate that Agnico confirmed that labor inflation continues to remain sticky which was discussed by other producers, this is not a company-specific issue. Agnico continues to be one of the best positioned to deal with labor inflation, being a regional miner with large-scale and long-life assets and an employer of choice.

Agnico Eagle Mines - AISC & AISC Margins (Company Filings, Author's Chart)

{kind=link}

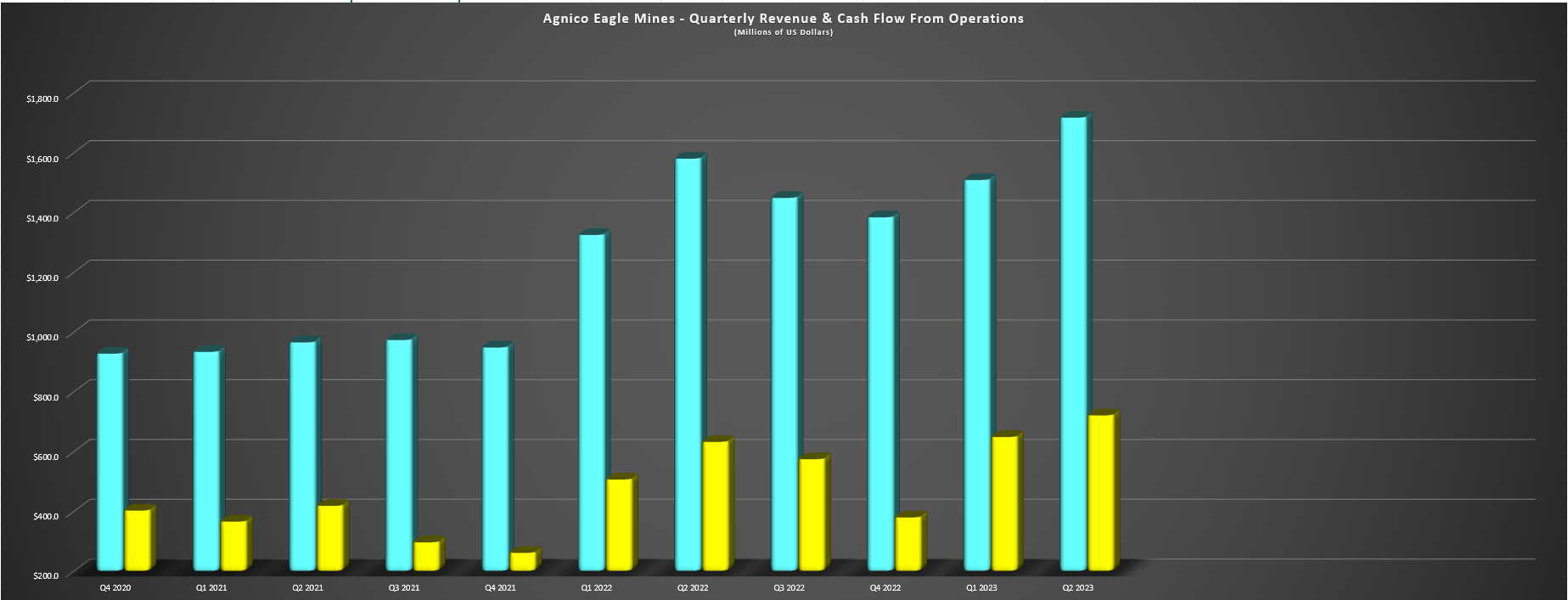

Given the impressive operating performance, Agnico reported strong operating cash flow of ~$722 million in the period (Q2 2022: ~$633.3 million) and finished the quarter with $473 million in cash despite significant debt repayment in the period. Meanwhile, operating cash flow per share came in at $1.46, up from $1.39 in the year-ago period, continuing the company's track record of per share growth. And with multiple irons in the fire (Wasamac, Upper Beaver, AK/Upper Canada) and low-capex growth options that can be achieved without any share dilution with a plan to leverage excess processing capacity, I would expect this trend to continue. Hence, for investors looking for a miner that continues to grow cash flow, dividends, production, and reserves per share, Agnico Eagle continues to be one of the only companies passing this hurdle with flying colors.

Agnico Eagle Mines - Quarterly Revenue & Cash Flow From Operations (Company Filings, Author's Chart)

{kind=link}

Summary

While we've had a mixed start to the Q2 Earnings Season for the Gold Miners Index, Agnico Eagle was certainly an exception, delivering a record quarter for production (helped by acquisition of the other half of Canadian Malartic), a record quarter for mill throughput at multiple assets, and surprise positive news that restrictions have been lifted at Fosterville.

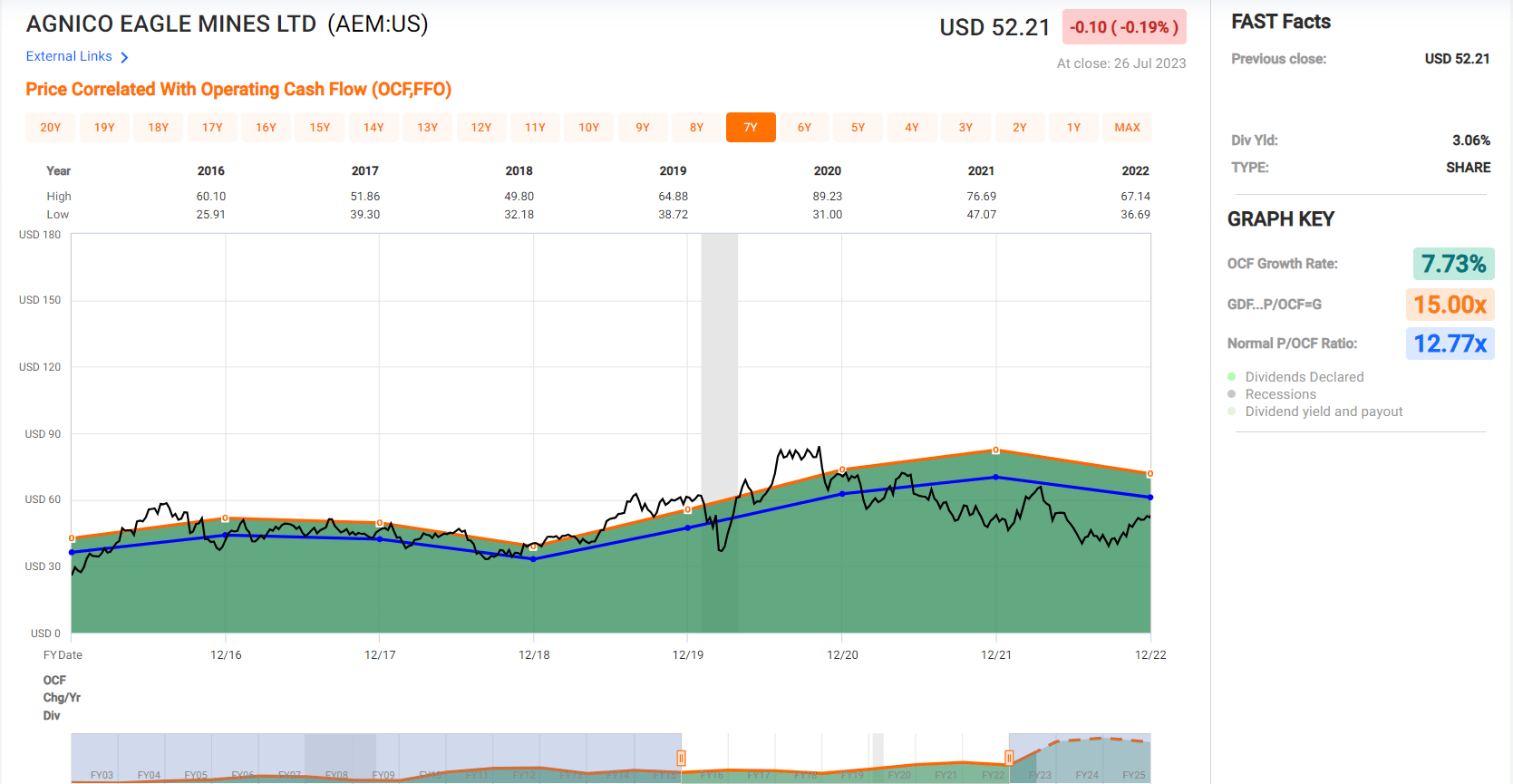

This solid Q2 performance has placed the company in a position to easily meet its FY2023 guidance midpoint of 3.34 million ounces of gold as it heads into H2 at ~50.5% of its guidance midpoint, with the potential for some bonus ounces at Kittila depending on the SAC decision. And despite this solid performance and one of the best portfolios sector-wide with the best jurisdictional profile among major producers, Agnico continues to trade at a very reasonable valuation, sitting at just ~8.7x conservative FY2024 cash flow per share estimates of $5.90.

Agnico Eagle Mines - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

As discussed in past updates , I believe a more reasonable multiple for a company that benefits from scale (including 100% ownership of two of the largest gold mines globally), diversification, an incredible track record of per share growth and a path to relatively low-capex growth should trade at a minimum of 12.0 to 12.5x cash flow, roughly in line with its historical multiple. Even if we use the low end of this multiple and conservative FY2024 cash flow per share estimates of $5.90, this translates to a fair value of US$70.80, pointing to a 38% upside from current levels which assumes no improvement in metals prices.

Following an exceptional Q2 performance and what will be another record year for the company, I continue to see Agnico Eagle as a top-3 gold producer sector-wide. I would view any pullbacks below its June/July lows as buying opportunities.

For further details see:

Agnico Eagle Mines: Another Blowout Quarter In Q2