AEM:CC - Agnico Eagle Mines: Best Of Breed For 2023 And Beyond

2023-07-03 10:36:46 ET

Summary

- Agnico Eagle Mines presents a compelling opportunity for investors in the second half of 2023.

- I'm bullish on gold and gold mining stocks, and AEM, particularly for its superior performance, growth in production, and recent acquisition of Yamana Gold's assets.

- In this article, I'll highlight AEM's low valuation, strong dividend yield, and minimal political risk as additional reasons to consider investing in the company as a 'best of breed' gold stock.

Investment Thesis

Agnico Eagle Mines ( AEM ) has corrected along with other gold mining stocks since early May, and in my opinion, could produce an attractive entry point for a buy in the second half of 2023. I am long-term bullish on gold and gold mining stocks, but at this time I tend to favor quality over more speculative, smaller gold stocks. Of the top gold mining companies, AEM is superior for several reasons and is a standout in the industry. Agnico Eagle is the third largest gold producing company in the world, and one that has actually grown production quite well compared to peers such as Newmont ( NEM ) and Barrick ( GOLD ). The stock is also outperforming peers over the last year, and I expect that this trend could continue into the future. The recent acquisition of Yamana Gold's assets will add considerable value over time, and is one of the main reasons why I own the stock. In this article, I will address why Agnico Eagle is a top pick and explain why I believe the company is a 'best of breed' gold stock worth potentially adding to a long portfolio in the second half of 2023.

Introduction

I do not consider myself a 'gold bug' but there are many reasons to be bullish on the precious metal and also equities with exposure to the industry. It is difficult for me to formulate a long-term bearish thesis on gold; it is a rare thing that has applications far beyond just a store of value for investors who are concerned with the Federal Reserve and the money-printing bonanzas as of late.

{kind=link}

Gold Prices Over The Years (macrotrends.net)

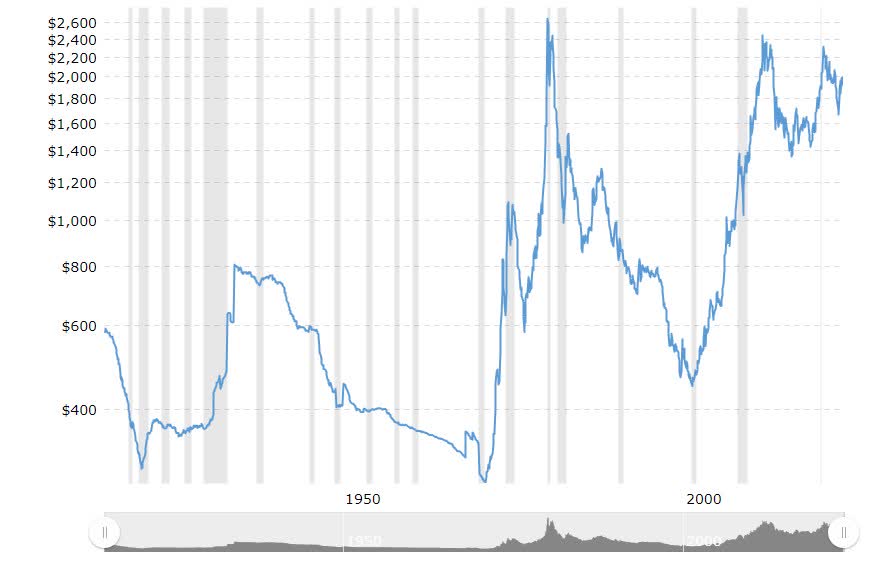

Investors became quite concerned with inflation in recent years, and while gold does not, in my opinion, act as a perfect 'inflation hedge,' it does act inversely against financial uncertainty and disorder. The metal itself, a legacy monetary asset, has appreciated in price around 7x since the lows in the early 1970's and continues to march higher (gold recently topped out near $2,055 per ounce in 2023). After a textbook correction, many gold miners are trading at favorable valuations amidst worries of bank failures in recent months and potentially more instability in the financial system on the horizon. Agnico Eagle trades at just 9.5 times trailing EBITDA and for 1.1 times net asset value, despite being one of the top companies in its sector.

Higher interest rates are also partly due to blame for the correction in gold equities. There are set to be at least two more rate increases for the second half of 2023, after a period of brief pause in the short-term. 2024 is more uncertain, but once interest rates reach a peak, gold should in theory begin to outperform once more. This rising rate environment has begun to be priced-in to gold itself, and gold stocks such as Agnico Eagle have responded just as expected. I may be somewhat early in covering the stock with a 'Buy' rating, but over the long-term, I expect gold to appreciate more in terms of price with an average trading range above $2,000 highly likely for future years. If a longer, more sustained period comes with a normal gold price per ounce in the $2,000 range, there is a large amount of leverage in just about every gold miner you can think of. For this new normal in terms of gold, I like Agnico Eagle as a 'best of breed' stock with higher production growth compared to peers and low debt levels. Recent news that the Canadian Malartic mine's life has been extended to 2042 also supports the long-term bullish thesis. Rising costs due to persistent inflation could be seen as a risk for the long-term, but Agnico Eagle has done a great job of managing increasing labor costs while paying down debt. The dividend is also healthy and sustainable with a yield at over 3.2%.

Why Agnico Eagle? - Yamana Gold's Assets

While buying something such as the VanEck Gold Miners ETF ( GDX ) may be a good option for investors here, I prefer to keep it simple and buy high quality businesses that I am somewhat familiar with. My road leading up to Agnico Eagle was first inspired by one of my old holdings from years ago - Yamana Gold.

I wrote an article on Yamana Gold in July of 2021, recommending the stock as a potential buy after an oversold period where the shares were trading below book value. I had owned the stock previously, and became familiar with the company after conducting research during 2019 and 2020. Since that first article was published, the stock went on to produce a return of around 45% (excluding dividends) in just over a year, before news broke that Gold Fields ( GFI ) was trying to acquire Yamana Gold at a premium. This really surprised me, as virtually no gold mining company in the last five years had been acquired at a premium price - most of the mergers/acquisitions had been about even in terms of net value. The arbitrage opportunity ended abruptly with news of this acquisition, and I made the decision almost immediately to sell my stock in Yamana Gold on the news.

In the months afterward, Gold Fields stock took a clobbering. With Yamana's share price pegged to Gold Fields, it appeared that my decision to sell was the correct one. Even more unexpectedly, the Gold Fields' offer was trumped later on by Agnico Eagle and Pan American Silver ( PAAS ) with an agreement to split up Yamana's assets. I did follow up research on Gold Fields during this time, as part of me still wanted to own Yamana Gold for the long-term, but the stock ran ahead of me faster than I ever thought possible on the reaction to Gold Fields being out-bid. A missed opportunity, for sure.

Another gold stock which I researched over this time period (2019-2020) was Kirkland Lake, which also ended up merging with Agnico Eagle last year. Two of my top gold picks are now one-in-the-same. What an opportunity!

Looking back on my initial article, you may see that Yamana Gold has 'turned into' Pan American Silver in terms of the performance tied to that article (I never recommended buying PAAS, but the stock also looks somewhat interesting here for a potential buy after a large correction). While Pan American Silver is appealing to me at this time, I prefer Agnico Eagle Mines, as many regard it as 'best of breed' among the world's largest gold miners, with higher growth than peers and low debt to EBITDA levels.

Political risks, among other risks, are something I always keep in mind when looking at miners. Looking at the charts of AEM compared to PAAS, it is clear which company investors view as more risky. If my thinking is correct, and I still indeed do want to be long Yamana Gold in some way, shape, or form, then owning Agnico Eagle is the best way to have exposure to the assets. I am quite interested in the Malartic mine in Quebec, which was previously seen as able to produce 700,000 plus ounces of gold per year, but now is being assessed with a longer mine life. Agnico Eagle had previously owned half of the Malartic mine, but now owns 100% thanks to the Yamana Gold acquisition. The Kirkland Lake merger last year also will add considerable value over the long-term, as well as future production growth from the Abitibi Gold Belt, which Agnico Eagle has a distinct competitive advantage in.

Reasons For Owning AEM Over Peers

All of Agnico Eagle's mines, except for two, are in North America, and neither of the exceptions (Finland and Australia) seem to present with much political risk. I mainly stay away from companies outside the United States of America and Canada, as I see them being outside of my circle of competence, but price also plays a factor. If the price is cheap enough, then my competency on the matters may not end up mattering at all. Something like Sibanye Stillwater ( SBSW ) comes to mind, as this is an example of a cheap stock in another part of the world which I do not understand well enough. I have learned over the years that my investing style is to focus on quality above all else, and to not take inordinate amounts of risk. Political risk in other countries is something I try to avoid, and in terms of Agnico Eagle, the risks in this area seem minimal. Not to say this is a company without any political risk at all.

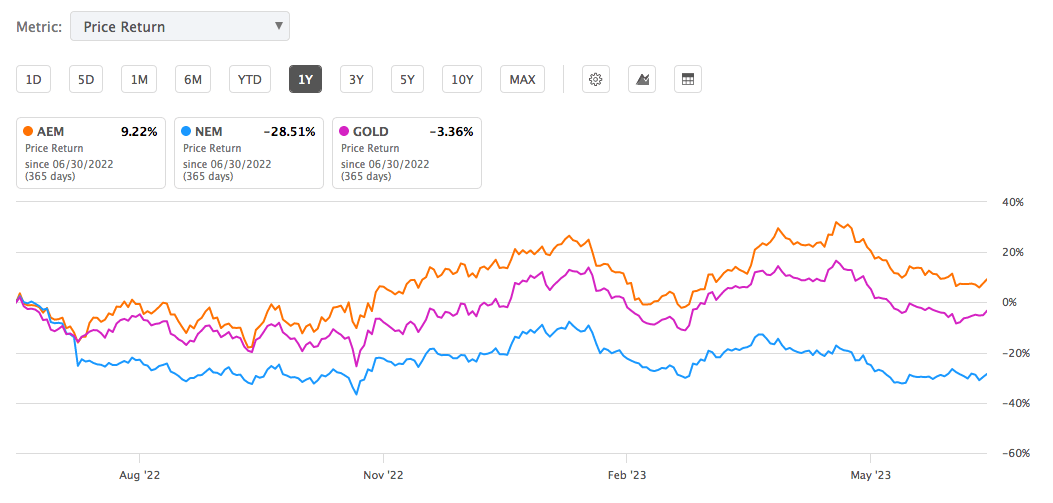

Despite some political risk, Agnico Eagle is a standout among peers and one major gold producer that has proven to be a consistent grower and a good allocator of capital. Newmont has been stumbling in terms of growth for some time, with around 6 million ounces of gold per year which has held steady, and Barrick Gold's production levels sunk to almost a 23-year low as of last year. I prefer Agnico Eagle to both of these, as future growth projected from the recent acquisitions of Kirkland Lake and Yamana Gold will add considerable value over time. Growth, even by acquisition, in a mostly no-growth industry makes the stock a standout among the top peers. Debt levels at Agnico Eagle are also lower than at Newmont and much lower than Barrick ( Debt/Equity of 0.30 vs. 0.40 vs. 0.60). The market capitalizations of Newmont and Barrick are higher than Agnico Eagle, but over time I could see Agnico Eagle eclipsing Barrick for the No. 2 spot. Could Agnico Eagle one day become the world's largest gold miner by market capitalization? I do not believe this is such a crazy thought.

{kind=link}

As seen in the above comparison, Agnico Eagle has been outperforming peers over the last year, and I expect that this outperformance will continue into the future. The technical picture is appealing after a correction from the recent highs, and the fundamental picture is even more appealing.

With now full ownership of the Malartic mine, Agnico Eagle will have two mines projected to produce more than 700,000 ounces of gold per year until at least 2042. This makes the stock a good buy for the second half of 2023, with a holding period of more than 5-6 years before needing to reassess the long-term investment opportunity.

Agnico Eagle's gold production rose to 3.1 million ounces in 2022 from 2.1 million ounces in 2021, counting the added production from Yamana's assets yet to come (the acquisition has officially closed very recently). The company's gold mineral reserves increased around 9% to 48.7 million ounces last year, and are expected to rise even more in coming years. Agnico Eagle has also cut its debt by more than half, to around $650 million from $1.5 billion at the start of 2020. This puts Agnico Eagle's ratio of net debt to EBITDA at roughly 0.30. Barrick's Debt to Equity is approximately 0.60, while Newmont's is around 0.40. In summary, Agnico Eagle has higher production growth, lower debt levels, and better stock performance than both Newmont and Barrick, making it a 'best of breed' gold stock for the coming years.

Dividends And Low Valuation, Other Risks

Unlike Newmont or Barrick, Agnico Eagle did not reduce its dividend recently, and sports a 3.2% dividend yield for its shareholders. Over 3% is a healthy, sustainable dividend for the company, and as the shares continue to correct, the dividend proposition offered by the company becomes even more attractive. Agnico Eagle's shares also do not trade at a high earnings multiple (around 9.5 times trailing 12-month EBITDA) and the valuation is low at 1.1 times net asset value. For one of the best gold mining stocks in the entire market, this overall valuation seems extremely low to me.

If the dividend yield is not enough to sooth the risk-averse investor, then perhaps insider buying is also worth mentioning. On February 22nd, 2023, after reporting earnings, Agnico Eagle's CEO bought 8,200 shares . Over the past six months, insiders have been net buyers of the shares as the price has swung from lows near $45 per share to as high as $61.15. Many analysts are bullish on the stock as well, with Wall Street analysts producing 15 buy recommendations, one hold, and zero sell recommendations.

Other risks include the potential for harsher regulations and restrictions, along with some political risk in other countries outside of North America. Gold prices correcting even further below $1,900 per ounce for an extended period of time would be a substantial risk to keep in mind as well. Will demand for gold falter in the coming years? It is a major risk, but current data does not show this being the case. Central bank demand for gold has been setting records in 2022 and Q1 2023, with the first quarter coming in 34% higher than the previous record set in 2013. It remains to be seen what Q2 demand will look like, but falling demand over the coming years is another risk that should be considered before making an investment in gold mining stocks.

Conclusion

Agnico Eagle Mines is one of my top gold picks for the second half of 2023 and beyond. I recently bought the stock and intend to hold for at least 5-6 years, with opportunities for dividend reinvestment along the way. I am bullish on gold itself, but even more bullish on gold mining equities at this time. I like Agnico Eagle as a 'best of breed' stock with higher production growth and lower debt levels compared to peers such as Newmont and Barrick Gold. Rising costs due to persistent inflation could be seen as a risk for the long-term, but Agnico Eagle has what it takes to manage labor costs, among other costs as well. The dividend is also healthy and sustainable with a yield at over 3.2% for its shareholders. Political risk is minimal, and a low valuation of 9.5 times trailing EBITDA and 1.1 times net asset value make the stock an attractive buy.

For further details see:

Agnico Eagle Mines: Best Of Breed For 2023 And Beyond