AEM - Agnico Eagle Mines: Solid Cost Control In A Tough Environment

2023-04-30 04:12:20 ET

Summary

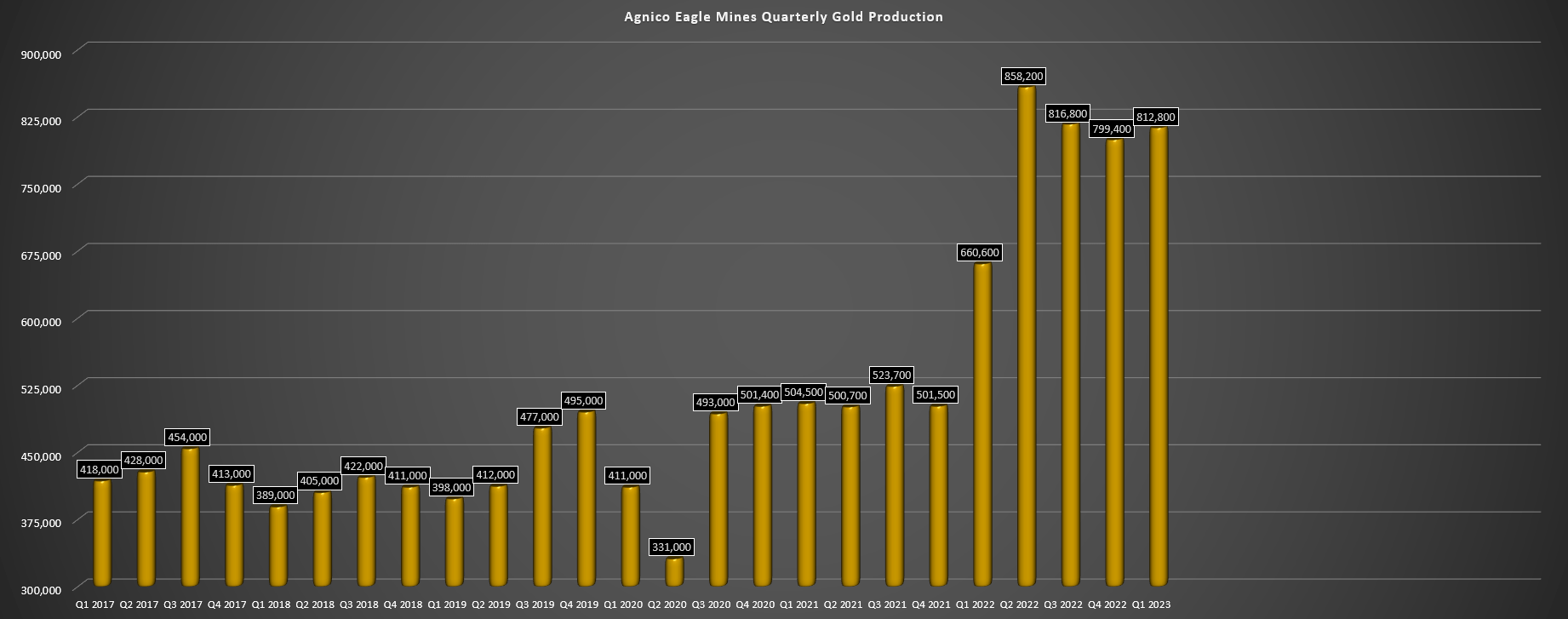

- Agnico Eagle Mines released its Q1 results last week, reporting quarterly production of ~812,800 ounces of gold at all-in sustaining costs of $1,125/oz.

- While costs were higher year-over-year because of inflationary pressures, costs came in well below the industry average and below the bottom end of its guidance range.

- Just as importantly for Agnico and the sector, inflationary pressures appear to be easing, with AEM calling out steel, fuel, some consumables and improving supply chain/logistics.

- Agnico's combination of capital discipline, steady growth at attractive margins, a strong balance sheet, and a portfolio that's concentrated in the safest jurisdictions sector-wide makes a solid buy-the-dip candidate.

The Q1 Earnings Season for the Gold Miners Index ( GDX ) has finally begun and while we've only seen some of the benefit of the higher gold price enjoyed year-to-date, Agnico Eagle ( AEM ) saw a significant improvement in margins sequentially. Costs coming in well below the industry evidenced this, with some help from a weaker Canadian Dollar on a year-over-year basis, what appears to be some easing of inflationary pressures vs. H2-2022 levels, and a regional strategy that has ensured it's well positioned from a labor standpoint with a higher proportion of employees to contractors.

Just as importantly, its development pipeline looks better than ever, allowing Agnico to steadily grow production without the need for additional acquisitions. And this growth is not only low-risk (in jurisdictions it's already established) but relatively low-capex, with one example being the potential to leverage excess mill capacity along the Abitibi Gold Belt and bring assets into development without the need to construct new processing plants (Wasamac, Upper Beaver, Amalgamated Kirkland, Akasaba West). Finally, I'd be remiss not to note that Agnico now has full control of Canada's two largest gold mines with the closing of the Yamana deal. Let's dig into the Q1 results below:

Q1 Production Results

Agnico Eagle reported its Q1 results last week, producing ~812,800 ounces of gold, a significant increase from the year-ago period based on the mid-quarter closing of the Kirkland Lake merger, and a marginal increase when using full production figures for Q1 2022 from Kirkland Lake's three mines (Detour Lake, Fosterville, Macassa). This increase in production was driven by a solid performance across the board from its mines, with a very strong quarter from its two Nunavut mines (~201,600 ounces combined), higher production from Kittila (~63,700) which was up against easier comps due to delayed access to high-grade stopes in Roura Zone in Q1 2022, a better quarter from Macassa which was also up against easy comparisons (lower than planned grades), and solid quarters from its two largest assets, Canadian Malartic and Detour Lake.

Agnico Eagle - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

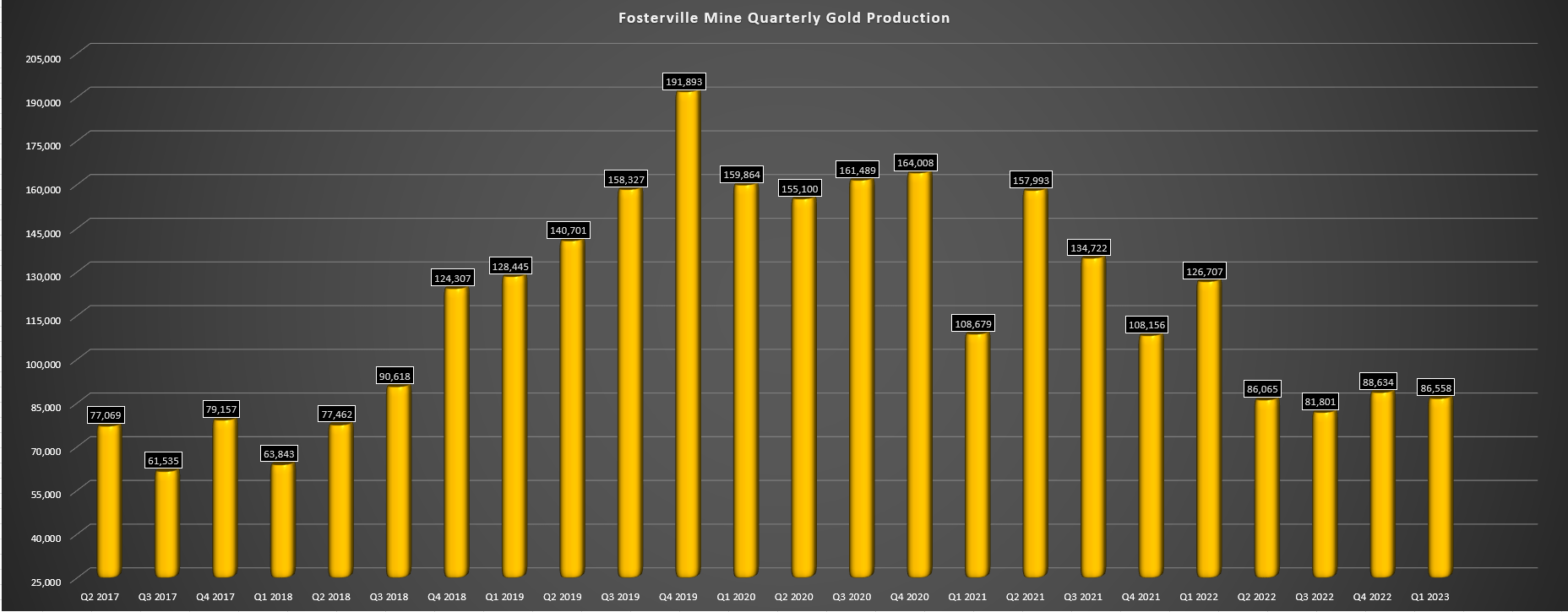

Unfortunately, the strong performances at several key assets was offset by weaker production at its LaRonde Complex (~79,600 ounces vs. ~105,000 ounces) due to lower mining rates with a switch to pillarless mining to better manage seismicity and significantly lower production at Fosterville (~86,600 ounces vs. ~126,700 ounces) due to lower throughput (operating constraints) and grades. That said, Fosterville's grades in the period were still better than nearly every other gold mine globally (exception of the much smaller Trixie Mine in Utah and Agnico's Macassa Mine in Ontario) at 18.6 grams per tonne of gold. This resulted in industry-leading cash costs of $396/oz despite the sharp decline in grades (18.6 grams per tonne of gold vs. ~29.0 grams per tonne of gold).

Fosterville - Quarterly Gold Production (Company Filings, Author's Chart)

{kind=link}

Starting with the operations with the more significant year-over-year declines, LaRonde had a much weaker quarter as noted, with ~79,600 ounces produced at cash costs of $958/oz due to changes to the mining sequence with lower mining rates, throughput, and grades. The mine's profitability in the period was further impacted by reduced by-product credits from lower zinc and silver prices. At Fosterville, the mine processed ~147,000 ounces which was well below the ~174,000 tonnes processed in Q1 2021 by Kirkland Lake Gold, with mining rates impacted by primary ventilation due to operating constraints in place with the State of Victoria Environmental Protection Authority [EPA] not allowing the use of surface vans from midnight to 6 AM. For those unfamiliar, this is related to low frequency noise complaints and has been an issue for over 18 months back to when Kirkland Lake operated the mine.

Agnico noted that abatement works for the low frequency noise were completed in Q1 and in conjunction with the State of Victoria EPA, an eight-week trial of various fan speeds was conducted. Agnico stated that it believes the results were promising and it's possible we could see a favorable resolution here. As many are aware, this is a mine that is seeing its grades normalize after several years of enjoying bonanza grades and a second Swan hasn't been discovered yet. So the combination of significantly lower grades post-2025 combined with lower mining rates could make it harder to justify keeping this as a core asset. However, this ongoing issue is resolved in an amicable and timely manner and exploration success continues, I would think that this would increase the probability of keeping this asset in the portfolio.

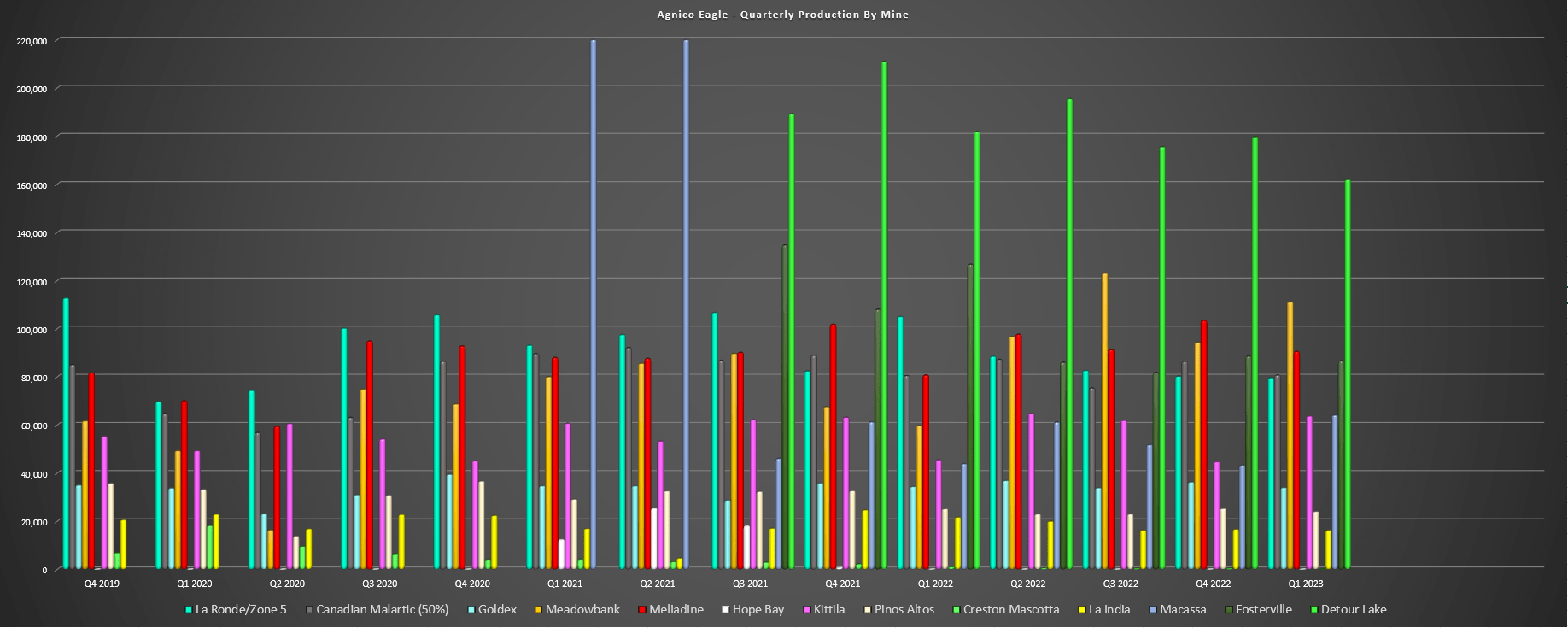

Agnico Eagle - Quarterly Production by Mine (Company Filings, Author's Chart)

{kind=link}

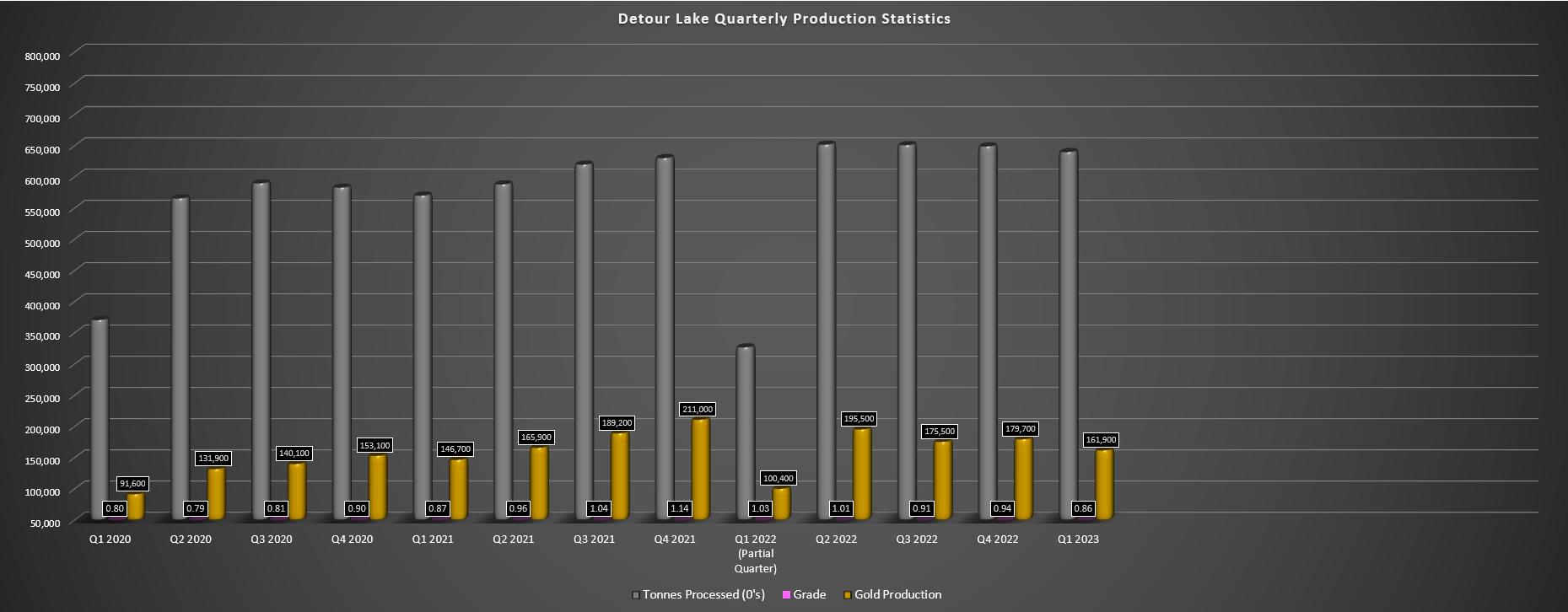

As for Detour Lake, the asset saw lower production year-over-year (adjusting for the shortened quarter under Agnico Eagle's ownership) with ~161,900 ounces produced based on ~6.40 million tonnes processed at 0.86 grams per tonne of gold. However, the lower production figure masked what was phenomenal performance at the asset with its best ever first-quarter mill performance in what's a seasonally lower period for the asset due to colder temperatures and the impact on material handling. And while there was a slight delay in access higher grade ore in Phase 2, the main culprit for the lower production was being up against difficult comps from Q1 2022 with increased throughput offset by lower grades (0.86 grams per tonne of gold vs. partial quarter with grades of 1.03 grams per tonne of gold).

Detour Lake - Quarterly Production Statistics (Company Filings, Author's Chart)

{kind=link}

It's worth noting that that mammoth-sized mine is already a cash-cow with an annualized run rate north of 700,000 ounces per annum with Q1 cash costs of $771/oz. However, Agnico Eagle is confident that it can push throughput to north of 28.0 million tonnes per annum (current annualized run rate just shy of ~26.0 million tonnes per annum), and this asset is permitted to process 32.8 million tonnes per annum. So, with the combination of increased throughput from improved mill availability, the potential to feed higher grades from Detour Underground (targeting internal evaluation in early 2024), this is an asset capable of producing closer to 1.0 million tonnes per annum, translating to 35% plus growth from current levels if achieved.

As for Canadian Malartic, the mine produced ~80,700 ounces in the period, with the higher grades offset by the plan to reduce throughput from ~60,000 tonnes per day to 51,500 tonnes per day to optimize production and cash flows as it transitions to processing Odyssey Mine ore. And in the case of Odyssey, Agnico saw mine production of ~2,800 ounces from primarily development ore in the period, it noted that shaft sinking has begun on schedule, and that the first production blast occurred in late March (~50,000 ounces expected from Odyssey this year). Similar to previous years, Agnico continues to drill aggressively to infill Odyssey internal zones and East Gouldie to declare additional reserves while also focusing on resource expansion east and west of East Gouldie.

{kind=link}

As of March 30th following the closing of the Yamana deal, Agnico Eagle is the 100% owner off Canadian Malartic, with significantly higher production from this asset expected going forward vs. previously having a 50% interest in the mine shared with its partner Yamana.

Moving west to Macassa in Ontario, Agnico reported production of ~64,100 ounces of gold at industry-leading costs of $604/oz. During the quarter, Macassa produced its six millionth ounce of gold, benefited from higher grades and throughput with an average grade of 23.3 grams per tonne of gold, and its Shaft #4 production hoist was commissioned in the quarter. The company also noted that material handling and ventilation will improve going forward with the successful commissioning of the first of two 3,000 horsepower fans and the completed construction of the conveyor loadout station, rock breakers and the loading pocket and the connection of new shaft infrastructure to existing mining areas.

As for the company's two Nunavut Mines, both assets reported solid performance in Q1, with Meadowbank having a monster quarter with ~111,100 ounces of gold production, helped by higher throughput at significantly higher grades (3.91 grams per tonne of gold vs. 2.26 grams per tonne of gold). This was related to higher gold grades from the Whale Tail and IVR open pits, and the start of underground mining at Amaruq. Meadowbank may have stole Meliadine's thunder with a 110,000 ounce quarter, but Meliadine performed exceptionally as well (~90,500 ounces produced), helped by higher throughput and grades. In fact, Meliadine saw record mill throughput and continued progress towards its mill expansion to 6,000 tonnes per day (equivalent to ~540,000 tonnes per quarter).

Finally, the company's Kittila Mine in Finland had a solid quarter due to higher throughput and grades (~496,000 tonnes processed at 4.73 grams per tonne of gold), and its Mexican assets had a decent quarter, combining for ~40,400 ounces from La India and Pinos Altos. As for permitting progress at Kittila, Agnico plans to host the Supreme Administrative Court of Finland [SAC] for a site visit and expects a final decision on its planned increase in mining rates to 2.0 million tonnes per annum. Agnico noted that if the SAC does not reinstate its right to operate at or near 2.0 million tonnes per annum, it will submit an updated permit, and the company is guiding conservatively for the time being while it awaits a decision.

Costs & Margins

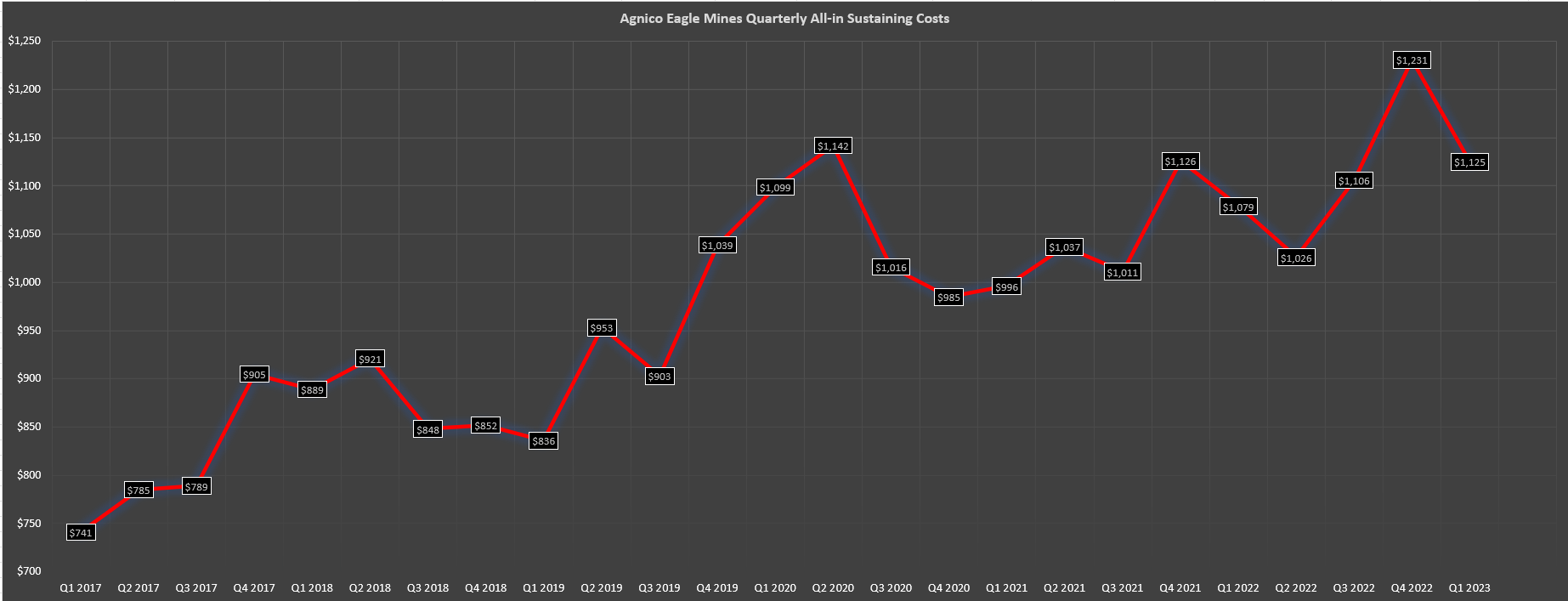

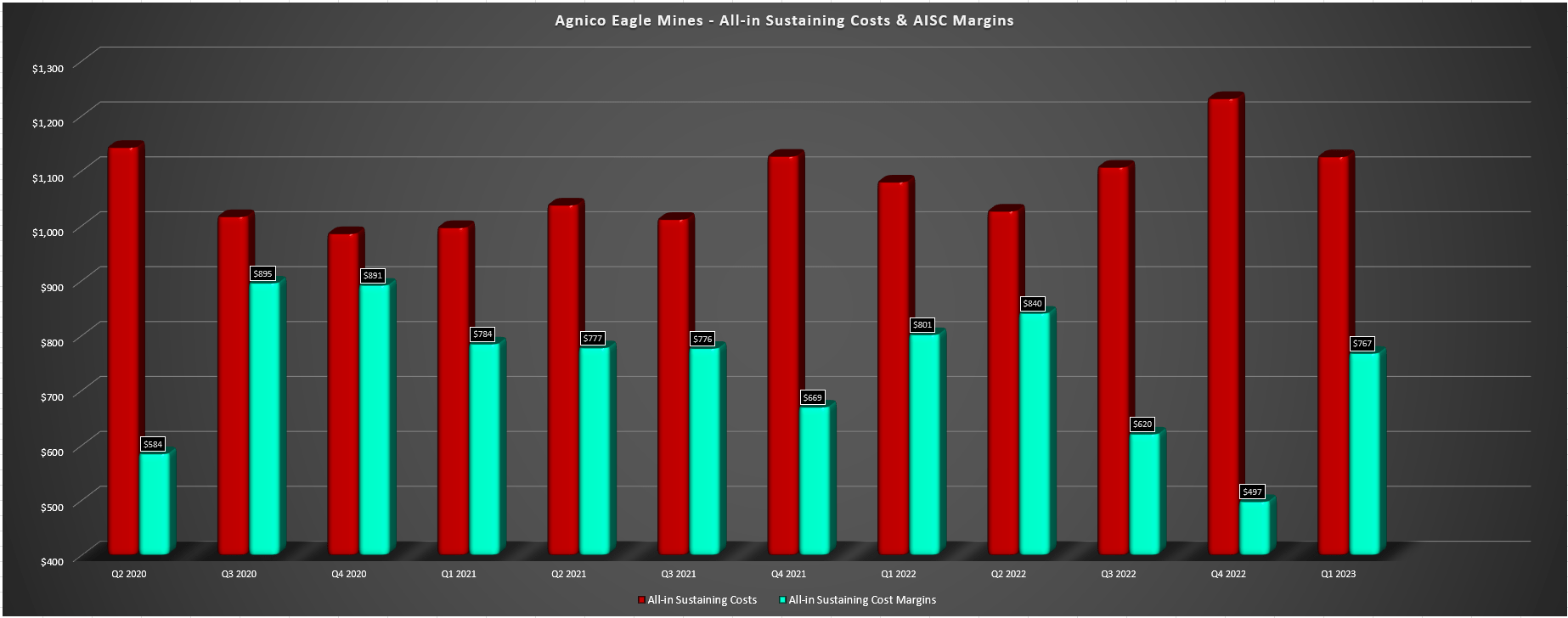

As for costs and margins, Agnico Eagle reported cash costs of $832/oz (Q1 2022: $811/oz) and all-in sustaining costs of $1,125/oz, with the latter figure up nearly 5% year-over-year from the $1,076/oz reported in Q1 2022. This was related to higher fuel costs, general inflationary pressures felt sector-wide, and increased sustaining capital, which came in at $170.0 million. However, while this led to a slight decline in AISC margins year-over-year to $767/oz (Q1 2022: $804/oz), these margins are still well above the industry and were much stronger than that of Newmont ( NEM ) at $552/oz.

Agnico Eagle Mines - Quarterly AISC (Company Filings, Author's Chart)

{kind=link}

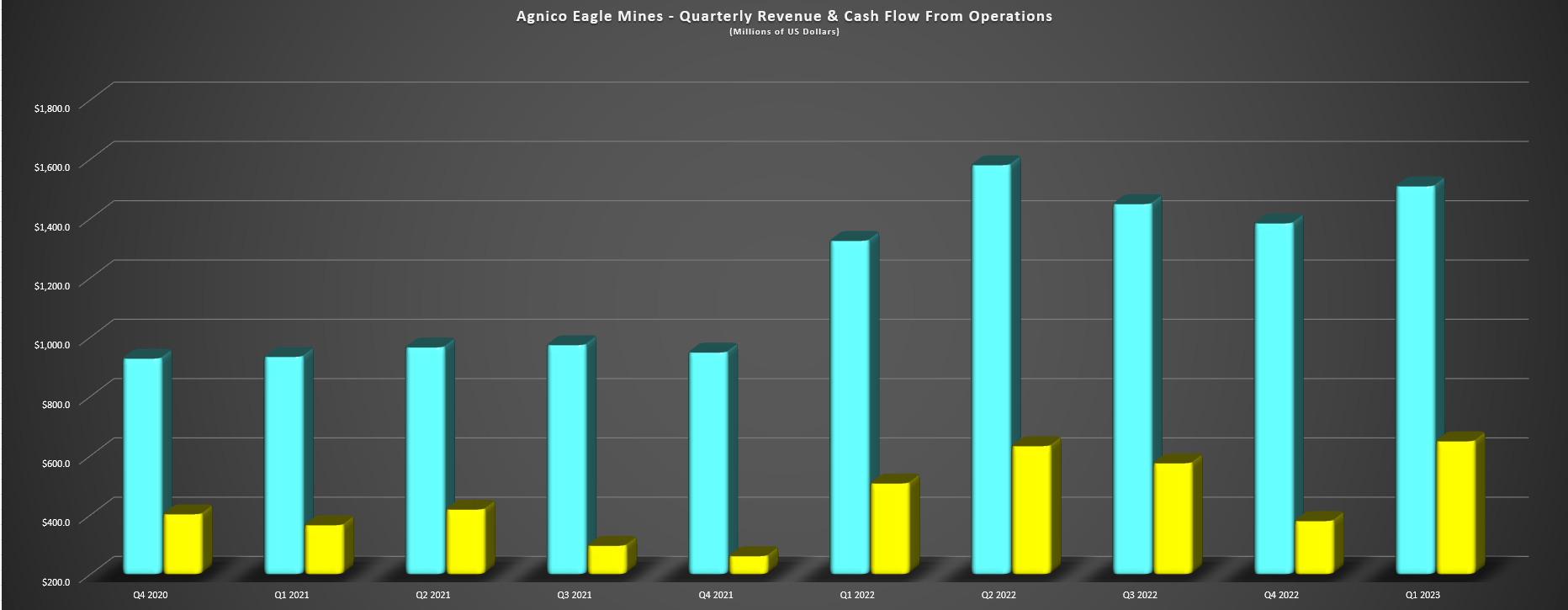

While the chart above might not appear all that encouraging (steadily rising costs), this is the trend we've seen for gold producers sector-wide, but Agnico has contained its costs better than peers due to lower labor inflation which makes up a significant portion of costs and the benefit of having multiple mines relying on lower-cost hydroelectricity, plus the addition of two lower-volume and ultra high-grade underground mines (Macassa and Fosterville). This increase in production and a slight increase in the gold price helped Agnico to report significantly higher operating cash flow of $649.6 million, and over $260 million in free cash flow came in the period despite much higher capital expenditures ($341.7 million vs. $250.1 million).

Agnico Eagle - AISC & AISC Margins (Company Filings, Author's Chart) Agnico - Revenue & Operating Cash Flow (Company Filings, Author's Chart)

{kind=link}

{kind=link}

Although some investors might have expected more from a margin standpoint following the addition of three lower-cost assets in the Kirkland Lake merger, it's worth noting that we've seen near unprecedented challenges for miners from a cost standpoint (tight labor market, inflationary pressures, supply chain headwinds), which have eaten some expected margin gains. That said, there are signs that these cost pressures are abating a little, as discussed in Agnico's Q1 2023 Conference Call:

We are seeing some relief, frankly, on the inflationary side, we were talking to our procurement team the other day. And we are starting to see from the -- frankly from the merger with Kirkland Lake. We said it would take a while for some of this to come through. Some of that is starting to come through with some of the new procurement contracts the team has been working exceptionally hard on that. We had some currency tailwinds that help us. So I think we're very comfortable with the guidance that we have with costs.

- Agnico Eagle CEO, Ammar Al-Joundi, Q1 2023 Conference Call

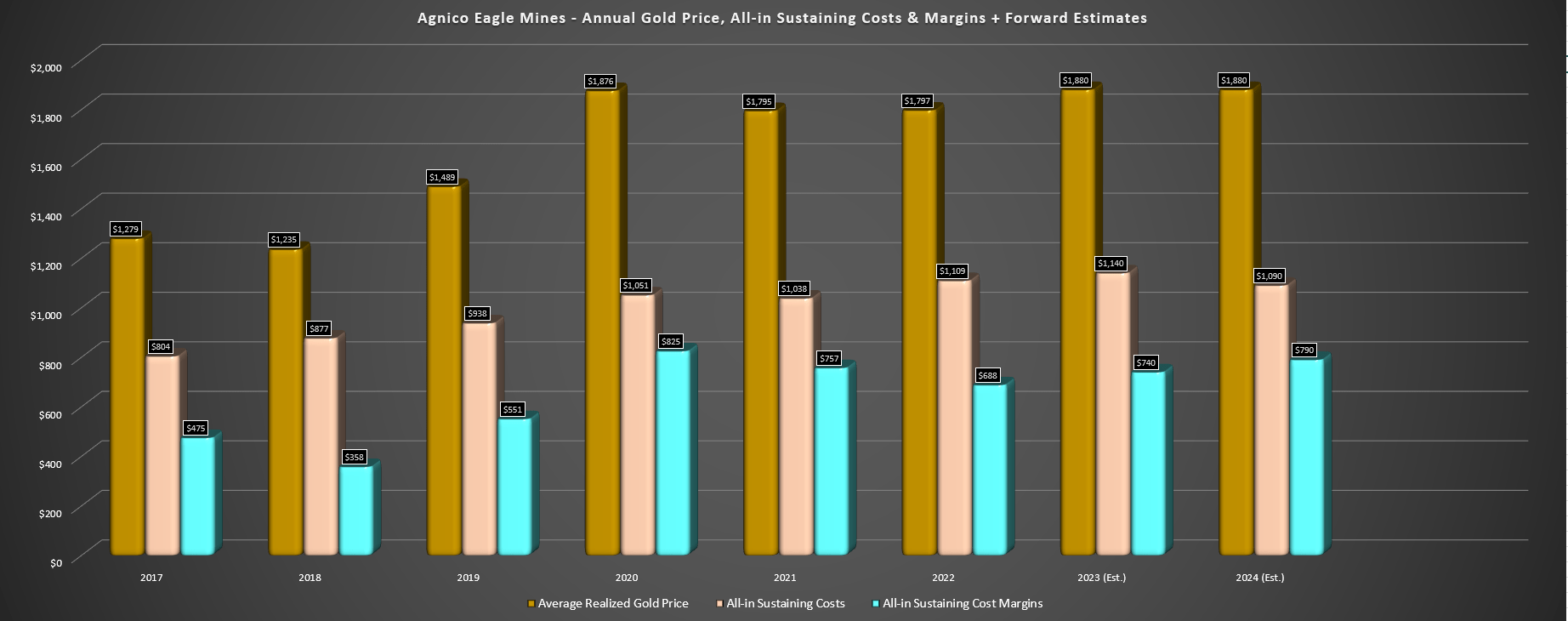

As discussed in the conference call, steel prices have cooled off as have fuel prices, and diesel prices started declining in March at the company's largest mine (Detour Lake), and continued to drop in April with improved electricity costs as well. One area that has remained sticky is maintenance parts and electrical material, and costs have been stickier in Finland according to the company. That said, the supply chain improvements combined with easing of some commodity prices are encouraging and from a big picture standpoint, Agnico Eagle is set to see meaningful margin recovery year-over-year and in 2024 assuming conservative gold prices of $1,880/oz.

Agnico Eagle - Annual AISC, Gold Price & AISC Margins + Forward Estimates (Company Filings, Author's Chart & Estimates)

{kind=link}

In fact, if we see AISC at the low end of guidance this year (1,140/oz vs. $1,140/oz to $1,180/oz guidance) and $1,100/oz AISC next year, we would see AISC margins improve to $740/oz and $790/oz, respectively. This would diverge materially from many of its peers, with AISC margins coming in just below FY2020 levels of $825/oz by 2024 even under the assumption of a sub $1,900/oz gold price to be conservative. To summarize, I continue to believe that we saw trough margins in Q3/Q4 2022 for Agnico Eagle, which is why the pullback in the stock was such a gift given that it was near a trough cash flow multiple despite a solid case for margin recovery as inflationary pressures eased and gold prices gained back some ground vs. their brief trip to the $1,700/oz level.

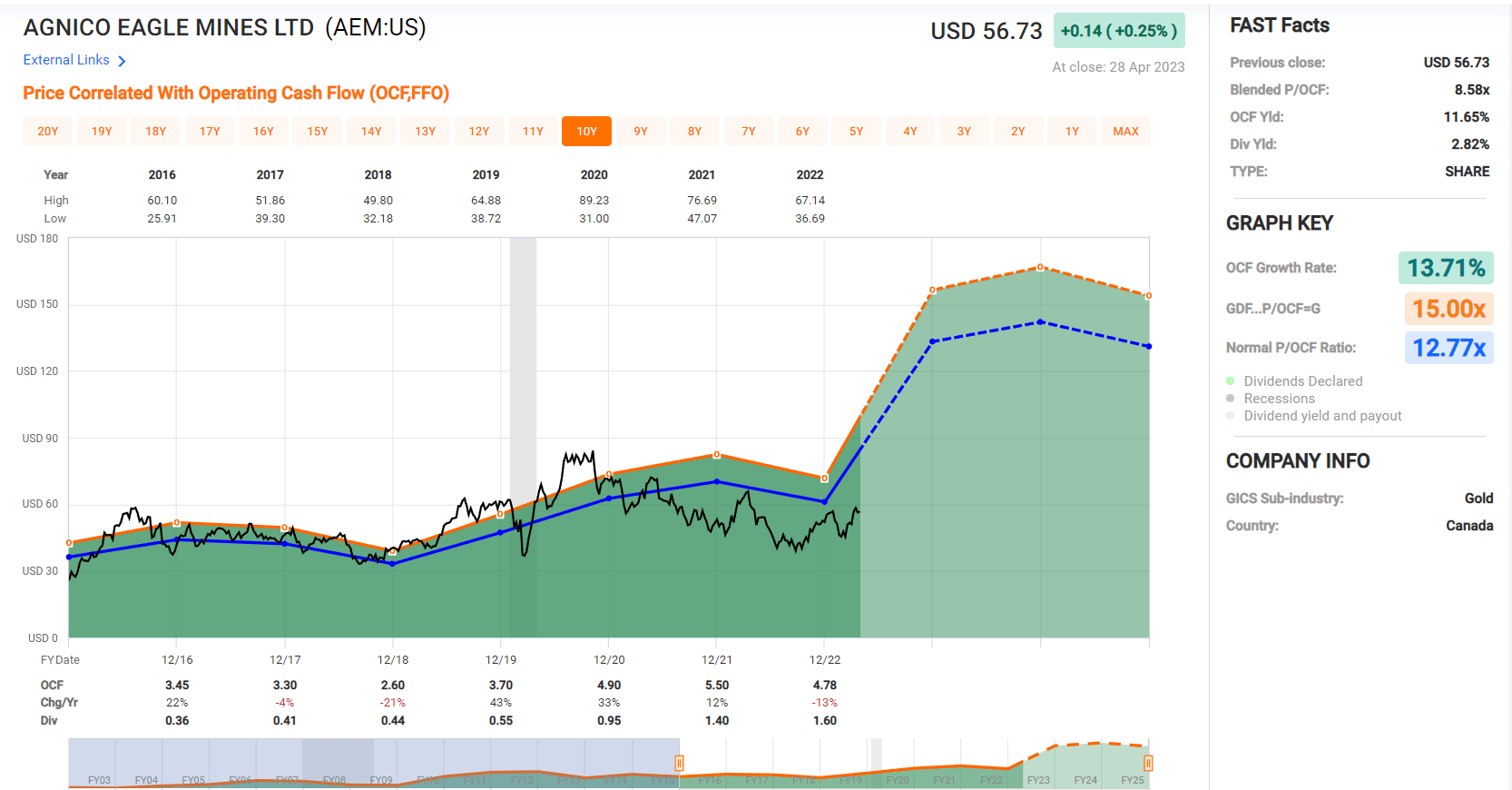

Valuation

Based on ~490 million shares and a share price of $57.00, Agnico Eagle trades at a market cap of ~$27.9 billion and an enterprise value of ~29.5 billion. This places Agnico Eagle just behind Barrick ( GOLD ) regarding its enterprise value despite a smaller production profile, but Agnico deserves to trade at a premium to peers like Newmont and Barrick for several reasons. These include its industry-leading track record of growth in per share metrics (production, reserves, net asset value, and dividends), its unique position as the only 2.0+ million ounce gold producer with over 90% of production from Tier-1 ranked jurisdictions, and its industry-leading margin profile among the top-5 producers.

Agnico Eagle - Historical Cash Flow Multiple (FASTGraphs.com)

{kind=link}

As shown in the chart above, Agnico has historically traded at ~12.8x cash flow and I would argue that a conservative multiple is 12.5x cash flow to reflect its lower production growth profile offset by increased diversification, larger scale, and an increased focus on Tier-1 jurisdictions than the previous cycle, which should command a premium multiple. Multiply this figure by FY2023 cash flow per share estimates of $5.65 translates to a fair value of $70.65 (24% upside from current levels). While this is a very reasonable upside case for one of the lowest-risk ways to get leverage to gold, I prefer a minimum 30% discount to fair value for large-cap producers. And after applying this discount, AEM's updated low-risk buy zone comes in at $49.50.

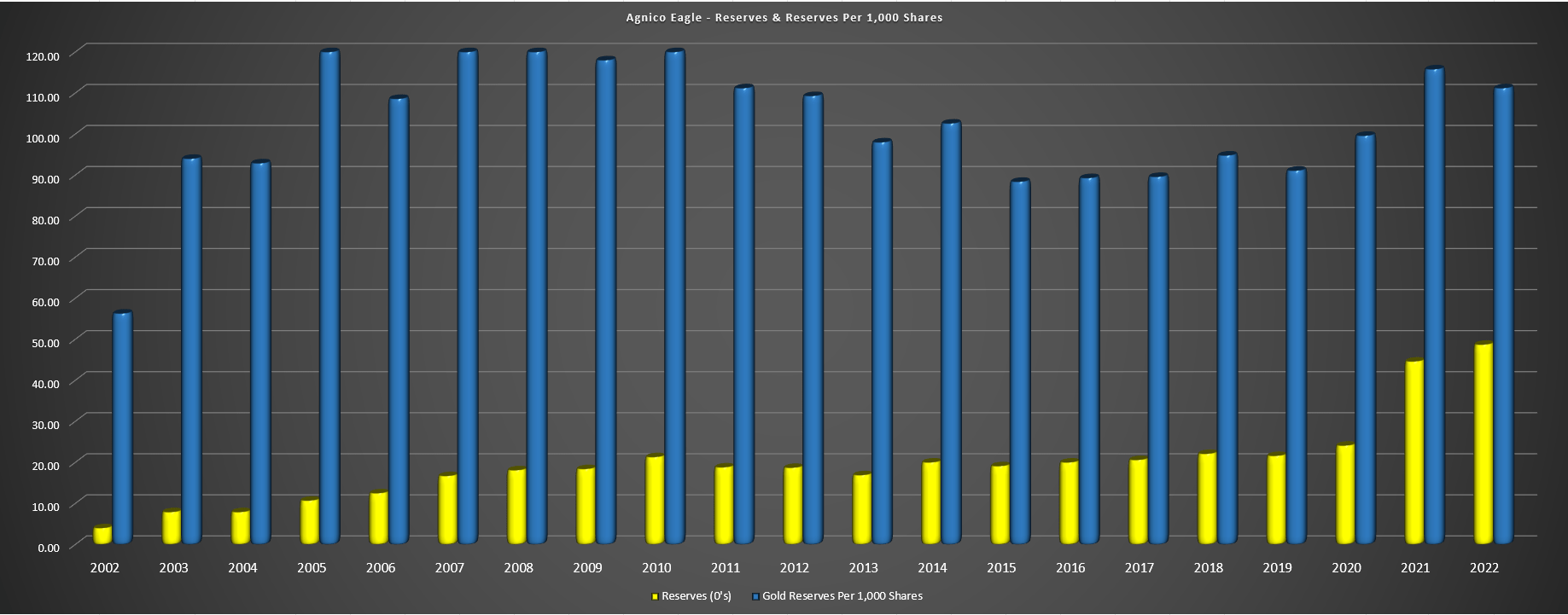

Agnico Eagle - Annual Gold Reserves & Reserve Growth Per Share (Company Filings, Author's Chart)

{kind=link}

Obviously, there's no guarantee that the stock heads to these levels, and the stock could head well above $70.00 per share in the next 18 months if strength in the gold price persists. That said, I prefer to only add to positions at a deep discount to fair value and the ideal time to buy Agnico was below $45.00 when many investors were disgusted with the sector's performance and couldn't bear to put more money to work in Q3 of last year. In summary, while I am bullish medium-term and long-term on Agnico Eagle, I am neutral short-term given that the stock is no longer trading at an extreme discount to fair value and is up over 60% off its lows.

Summary

Despite significant inflationary pressures felt sector-wide, supply chain headwinds and labor tightness since 2020, Agnico continues to fire on all cylinders with arguably the strongest results among its million-ounce producer peers. 800,000+ ounces of quarterly gold production evidenced this, with costs 15% below the estimated Q1 2023 industry average. This has been aided by the addition of high-margin assets at an attractive price (KL merger) rather than overpaying for growth like we've seen over the past two decades sector-wide (Andean, Red Back Mining, Great Bear, Pretium, Equinox), corporate and operational synergies, and a regional strategy that has made it an employer of choice and reduced its reliance on higher-cost contractors.

{kind=link}

This strict capital discipline has allowed the company to maintain industry-leading margins and grow not only its absolute production but also production per share with the company being very careful with M&A to ensure if it is paying a large price tag, it's doing so with a low-risk asset that complements the portfolio. Given the recent transactions, Agnico's portfolio has never looked better, with a vast development pipeline, significant scale, and a path to lower costs and relatively low-capex growth as it works to grow by leveraging off existing infrastructure in jurisdictions that it's already present (excess mill capacity at Malartic/LaRonde, continued work to restart a past-producing mine in Nunavut, mine/mill expansions at Kittila/Meliadine).

Agnico's combination of capital discipline, steady growth at attractive margins, a strong balance sheet, and a portfolio that's concentrated in the safest jurisdictions sector-wide makes it a must-own name and arguably the highest-quality producer sector-wide. And this thesis for owning Agnico is strengthened because other low-risk options for leverage to the gold price are not cheap, such as Franco-Nevada ( FNV ). So, with a reasonable valuation, significant ammo to support its stock if we see share price weakness and the comfort that the company will not overpay for assets (given its discipline and that it has all the growth it needs within its portfolio), I would view any sharp pullbacks as buying opportunities.

For further details see:

Agnico Eagle Mines: Solid Cost Control In A Tough Environment