AEM - Agnico Eagle: Outperforming The Market By Avoiding Crowded Areas Of The Market

2023-12-19 12:20:37 ET

Summary

- Agnico Eagle Mines has become an unlikely winner as the stock outperformed the market amidst waning investor interest.

- I take a closer look at the company's low cost structure and its implications for margins going forward.

- The record high free cash flow margin does not appear to be at risk and this should be a major tailwind for the stock price in 2024.

Outperforming the market on an absolute and risk-adjusted basis does not necessarily involve buying into the hottest technology stocks. Neither does it require you to own the most popular names with the equity market where quite often momentum trades could result in a heavily-one sided market which creates a risk of sharp reversal in share prices.

Agnico Eagle Mines (AEM) is by no means a low-risk stock and as a mining company comes with significant idiosyncratic risks and high standard deviation of daily returns (see the graph below).

Having said that, however, the company has outperformed both the gold miners sector and the S&P 500, which is heavily weighted towards the popular technology names.

Contrary to its idiosyncratic risk, AEM is a low risk stock when it comes to its market exposure. Its 2-year beta is below 0.6 which makes the stock's outperformance of the S&P 500 even more impressive.

Seeking Alpha

Similarly to other gold mining stocks and precious metals more broadly, Agnico is also not a very popular choice among investors which further reduces downside risk during broader market sell-offs.

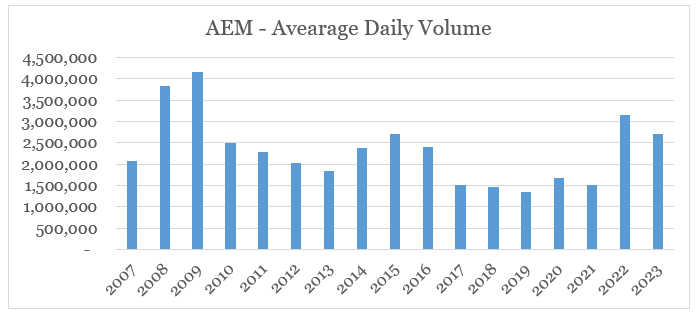

When looking at average daily volumes, one could easily be led to think otherwise.

{kind=link}

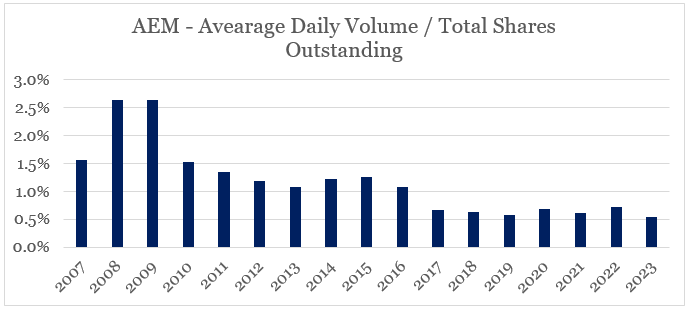

However, if we compare Agnico's daily trading volumes to the company's total shares outstanding, we can see that investor interest has been exceptionally low since 2017.

{kind=link}

Keeping Costs Under Control

Ultimately, an investment thesis for AEM would rely on gold prices remaining near or above their all-time highs which in my view is a highly likely scenario as we enter 2024.

Additionally, Agnico is among the low-cost producers with very low jurisdiction risk which makes the company a good choice for anyone looking to minimize downside risk.

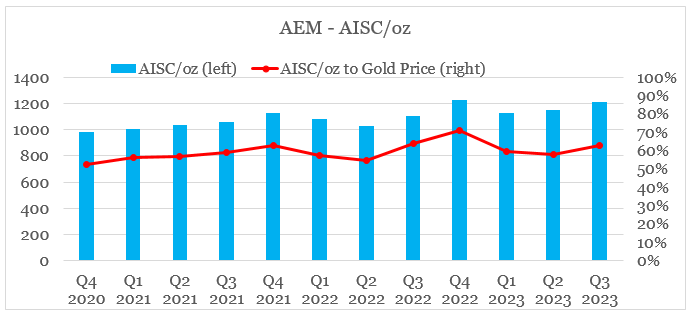

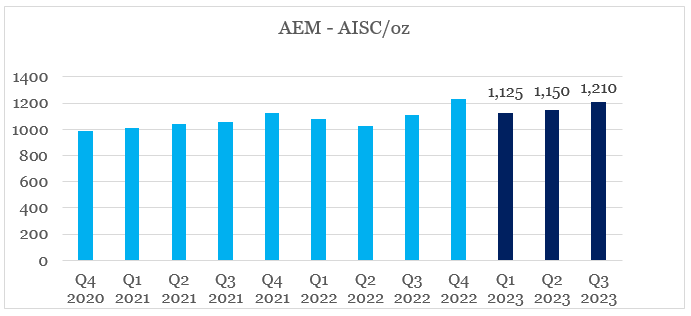

As gold is trading near its all-time high, AEM's all-in sustaining cost (AISC) per ounce has been under control. During the last reported quarter, AISC per ounce stood at $1,210 when the average price of gold was around $1930 per ounce.

All that makes Agnico a highly profitable business that is also not very popular among investors - a combination that is rarely seen in the equity market.

Seeking Alpha

Over the past few years, Agnico's costs per ounce have been slowly creeping up as commodity prices have gone up significantly during the same period. However, they remained under $1,200 per ounce for the better part of 2023 which has resulted in a drop of the company's AISC to the price of gold ratio.

prepared by the author, using data from Quarterly Earnings Releases

{kind=link}

In the meantime, Agnico continues to expand production at a higher than initially-expected rate, while keeping costs under control.

With regards to production , we're well positioned to be above the midpoint of our guidance and if things go well with us in Finland, we will be closer to the top-end of that guidance on the production side.

Importantly on cost , the team has also done an excellent job. We continue to forecast within guidance and towards the midpoint of guidance .

Source: Agnico Eagle Mines Q3 2022 Earnings Transcript

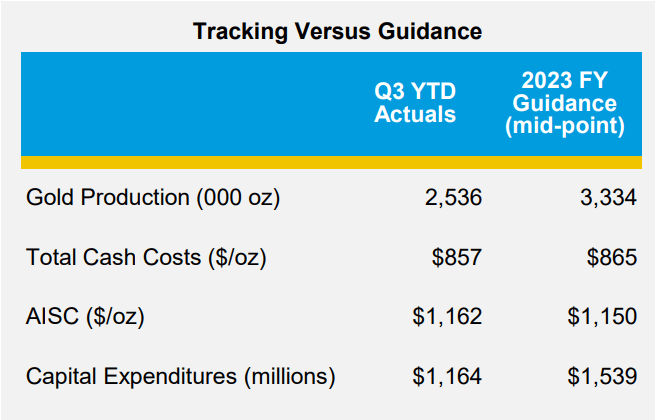

Management has recently reiterated its FY 2023 guidance with a midpoint for AISC per ounce of $1,150.

{kind=link}

The upper-bound of the AISC range stands at $1,190 which is still well-below the current prices of gold and even more importantly, Agnico's management expects costs to decline in 2024 and 2025.

AISC per ounce in 2023 are expected to be between $1,140 and $1,190 . The higher costs, when compared to Previous Guidance of between $1,000 and $1,050, are largely a result of higher total cash costs per ounce and slightly higher capital expenditures. AISC per ounce are expected to decline in 2024 and 2025.

Source: Agnico Eagle Mines Q4 2022 Earnings Release

To put this into perspective of what expectations for the fourth quarter of this year are, AISC should come in around $1,300 during the quarter, allowing the company to meet the high end of the cost guidance of $1,190 for the full fiscal year.

prepared by the author, using data from Quarterly Earnings Releases

{kind=link}

Anything above this number, is likely to put short-term pressure on AEM's stock price and in my view will present a good opportunity for medium to long-term shareholders.

Looking Beyond The Next Quarter

Beyond the current quarter, Agnico is also in a very good position to improve its gross margins and with that the company's overall profitability and free cash flow.

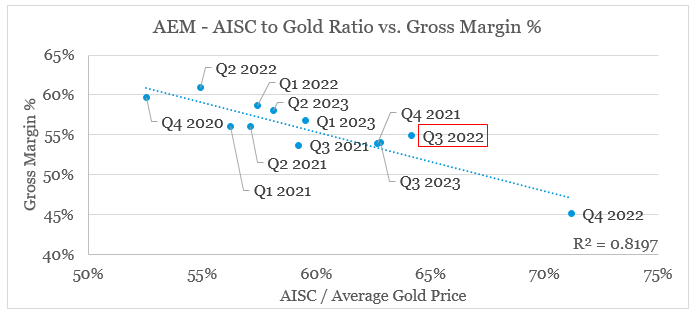

The ratio of AISC to Gold prices we saw above is a very good measure of what Agnico's gross margins would look like, given the strong relationship between the two. Therefore, if gold prices remain at their current levels and AISC falls (lower AISC/Gold ratio), it is reasonable to expect for the company's gross margin to improve over the coming years.

prepared by the author, using data from Quarterly Earnings Releases and Seeking Alpha

{kind=link}

Assuming Agnico's AISC would remain at the high-end of the 2023 range at around $1,200 and gold prices are flat at $2,000 an ounce, would give us a AISC/Gold ratio of exactly 60%. Based on the graph above, this would translate into gross margin of roughly 55%.

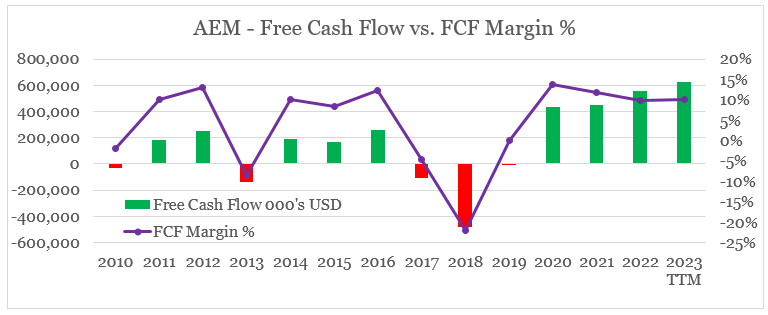

This is roughly in-line with the company's current margins, which result in a very high free cash flow on an absolute basis and a record-high free cash flow margin of 10%.

{kind=link}

These numbers should continue to improve as Agnico fully integrates its recent acquisitions. This alone is enough to provide a lasting tailwind for annual gold production and operating margins.

At the same time, however, gold prices are now flirting with the $2,100 level and given management's expectations of lower AISC in 2024 and 2025, the probability of AEM achieving even higher margins in the coming years is very high.

Conclusion

After outperforming the market in recent years, Agnico remains well-positioned to continue to do so. In addition to my favourable view on precious metals more broadly, Agnico's margins could improve further over the coming year. But even if the dynamic between gold prices and energy costs turns into a headwind, Agnico should be able to retain its high free cash flow. In my view, all that results in a positive skew in the stock's risk-reward profile as we are about to enter 2024.

For further details see:

Agnico Eagle: Outperforming The Market By Avoiding Crowded Areas Of The Market