AEM - Agnico Eagle: Strong As The Canadian Shield

2023-12-18 09:53:04 ET

Summary

- Agnico Eagle Mines is the third largest gold producer in the world, with operations in Canada, Finland, Australia, and Mexico.

- The company's strategy focuses on performance and growth, establishing a robust project pipeline, investing in its people, and socially responsible operations.

- Agnico has recently been active in mergers and acquisitions, but has faced shareholder scrutiny over executive compensation.

Company Overview

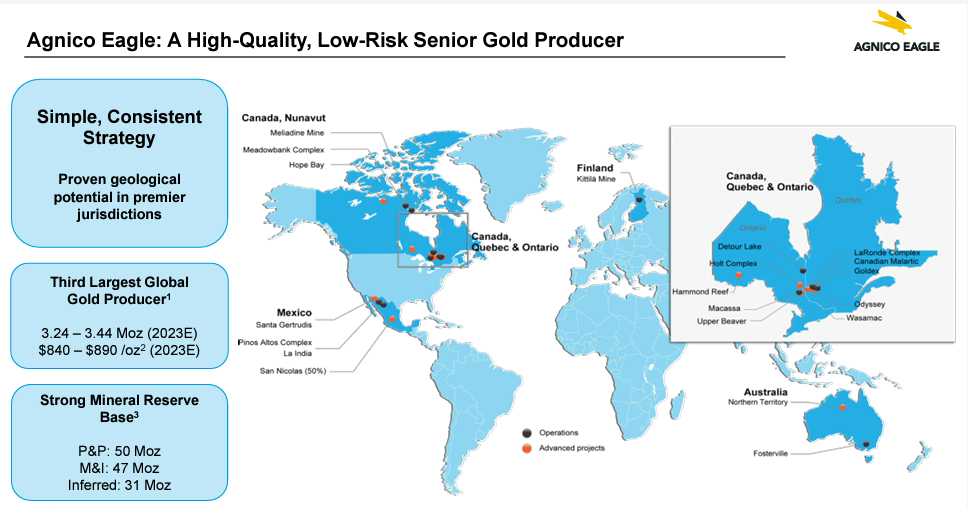

Agnico Eagle Mines (AEM) Limited is the third largest producer of gold in the world with a total output of nearly 3.5M ounces . Agnico is headquartered in Canada with operations in Canada, Finland, Australia and Mexico and exploration and development activities extending to the United States. Agnico is a solid option for investors looking for precious metals exposure. It is unhedged and retains full exposure to spot gold prices. Investors have been attracted to Agnico due to its combination of low geopolitical risk, consistent dividend payments and its track record of stable operations. Agnico currently has a market cap of just under $27B and an attractive dividend yield of ~3%. I believe this makes Agnico a solid hold at today's prices and if multiples become more attractive.

Agnico's Strategy Overview

-

Deliver on performance and growth expectations: Ensuring current operations meet expectations, minimize operational risks, and generate cash flow.

-

Establishing a Robust Project Pipeline: Focusing on developing a top-tier project pipeline to replenish mineral reserves and production. Maintaining high standards for project quality, manageability, and alignment with the overall portfolio.

-

Investing in its People: Providing growth opportunities for employees and fostering the necessary skills and infrastructure to support operational and project development.

-

Socially Responsible Operations: Creating shareholder value while prioritizing safety, social responsibility, and environmental consciousness. Contributing to the prosperity of employees, their families, and the communities where Agnico operates.

AEM's strategy (Company Filings)

{kind=link}

Agnico Has Been Busy

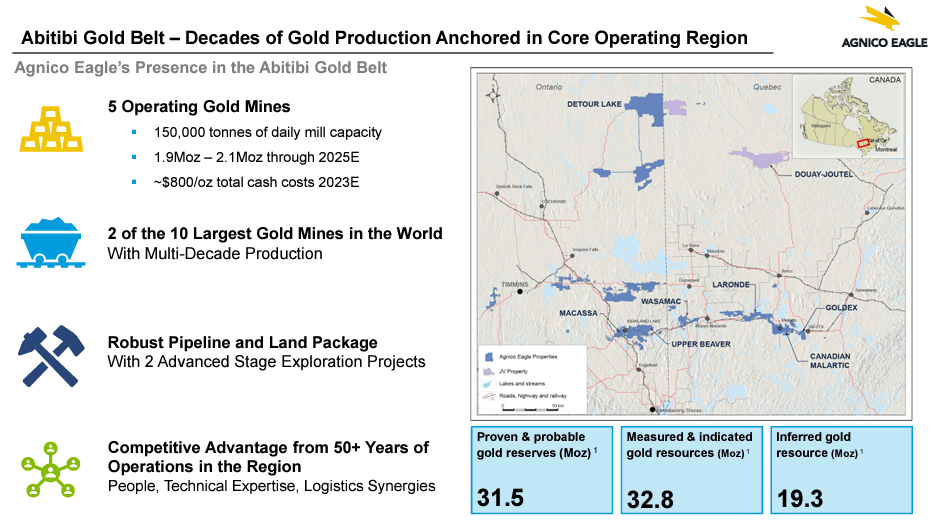

AEM has been quite active on the M&A front of late. In early 2022, it successfully acquired Kirkland Lake Gold which brought along with it the Detour Lake Gold mine in Canada and the Fosterville operations in Australia. Earlier this year, it consolidated its ownership of the Malartic Gold Mine in Quebec, Canada by acquiring Yamana's interest in the project. These moves have resulted in fortifying Agnico's presence as the dominant producer of gold in Canada's Abitibi belt.

{kind=link}

The recent spate of M&A has primarily been financed by equity. This has seen Agnico's share count increase by over 102% over the past 24 months. In addition to the massive increase in the shares outstanding, investors have been uneasy with the compensation practices at AEM of late.

Shareholder Scrutiny on Agnico Remains in Focus

AEM stood out in 2022 with the most significant executive payroll among major Canadian miners, a factor that seemed intrinsically linked to shareholder dissatisfaction . In their recently disclosed proxy circular for the annual meeting, Agnico Eagle revealed one-time bonuses awarded to top executives in recognition of their role in the merger with Kirkland Lake Gold in February 2022. This included a substantial $10-million bonus for executive chairman and former CEO, Sean Boyd, resulting in a total compensation surpassing $20 million-exceeding the compensation of CEOs in the S&P/TSX 60 metals mining sector.

Agnico Eagle has defended these bonuses in the proxy statement, citing the merger's transformative impact, solidifying the company's stature as a 'super senior' in the gold mining realm. However, despite these justifications, Agnico Eagle will face a bumpy road in winning over shareholder approval for its largesse. Last year's say-on-pay vote registered as the lowest in Canada, with only 24% of shareholders endorsing the compensation strategy. Looking out into 2024 and beyond, investors will likely remain laser focused on AEM's compensation practices.

An Enviable Portfolio Being Operated Responsibly

Agnico has continued to operates its mine as it has through the years - responsibly and with stability. Agnico is now the largest gold producer in Canada and its operations are overwhelmingly focused on the famed Abitibi Gold Belt. Agnico Eagle Mines is currently operating five gold mines in the Abitibi region. The combined capacity of these mines allows for the processing of approximately 150,000 tonnes of ore per day. This capacity indicates the amount of ore that can be processed through their milling facilities on a daily basis. The company anticipates producing between 1.9 to 2.1 million ounces of gold through the year 2025. The estimated total cash cost to produce one ounce of gold is around $800 for the year 2023. This cost includes various expenses directly tied to gold production, such as mining, processing, and refining, among other operational costs. AEM's scale of operations allows it to exert significant influence on its suppliers thereby allowing them access to better prices and better terms on items and consumables necessary to run their mines. Being one of the largest gold miners in the regions also allows AEM to attract and retain high quality talent and provide them with the necessary runway for future success in their chosen roles.

Finland, where AEM operates the Kittila Mine has been a source of good news recently. In 2020, Agnico Eagle Mines received pivotal environmental and water permits from the Regional State Administrative Agency of Northern Finland, authorizing significant expansions at the Kittila mine. This included enlarging the CIL2 tailings storage facility, scaling operations to 2.0 million tonnes per annum (mtpa), and constructing a new discharge waterline. However, these permits faced opposition, leading to an appeal that was upheld by the Vaasa Administrative Court in Finland.

Responding to this setback, AEM pursued an appeal in August 2022, challenging the Vaasa Administrative Court's decisions and seeking the reinstatement of the permits through the SAC (Supreme Administrative Court). The recent confirmation from the SAC regarding the validity of the 2020 environmental permits allows AEM to sustain operations at the expanded 2.0Mtpa rate as initially permitted. Had the SAC ruled differently, AEM might have faced the necessity to curtail operations or potentially suspend activities in Q4 to ensure compliance with operating permit regulations.

This resolution bears significant implications for AEM's gold production projections. The company anticipates an approximate additional yield of 30,000 ounces from Kittila in the current year and elevating the total output from the mine to an expected 240,000 ounces.

In the recent quarter, exploration findings unveiled promising developments, notably at Kittila, hinting at a potential parallel structure alongside the Main Zone. These initial indications point to the possibility of an additional structure that could hold significance for future mining operations.

Over at Hope Bay, exploration efforts at Madrid showcased positive outcomes, particularly in step-out drilling activities. These results further bolster the prospects for a potential resurgence at Hope Bay. Initial drilling conducted in a previously unexplored area identified substantial potential to delineate a new high-grade zone. This discovery presents an exciting opportunity to uncover and potentially tap into a previously untapped area rich in high-grade resources.

A Discussion on Valuations:

Agnico currently trades at a market cap of ~$27B and an enterprise value of $29B. Over the coming years, the likelihood of unexpected bumps in production and unforeseen CAPEX are low. I expect the company to be able to retain its existing production profile of ~3.5-3.6M ounces annually. AEM's scale also allows them the maintain relative stability on its costs, which are expected to be ~$1100-1200 per ounce on an All-In Sustaining Cost ((AISC)) basis. These costs should translate to an annual EBITDA of ~$3B using today's gold prices. On a multiple basis, this translates to 9x EV/EBITDA multiple for 2024 and 2025. The current street consensus multiple is 8.3X 2024 EBITDA and 9.2x 2025 EBITDA. This is not cheap and I would argue that historically, AEM has never been viewed as a "cheap" gold stock. It operates in highly stable jurisdictions and its operating address has provided Agnico with a premium multiple. Agnico is expected to generate around $2.5B of cash from its operations in the coming years, and invest around $1.4-1.5B back into its business. The associated free cash flow as a result is expected to be ~$1B annually. While the FCF yield isn't high, the free cash should allow AEM to continue its dividend payout at its current level while providing investors with an exposure to rising metal prices.

What Could Go Wrong?

Being a gold miner is not without risks as many readers will know. The most important risk facing Agnico is declining metal prices. Being an unhedged gold producer, Agnico Eagle's top and bottom line are overwhelmingly linked to the spot price of gold. A material decline in gold price would negatively impact its share price. Secondly, we are still living in times where inflation risks are elevated. Continued wage and consumable inflation would increase operating costs for Agnico, thereby reducing their profitability. Thirdly, if Agnico's operations are impacted by safety incidents, we could see their mines be suspended temporarily as these issues are remediated. Given AEM's track record, the probability of a major incident is quite low. Finally, given its low-risk geographic exposure, the probability of Agnico losing its operating permits like we saw happen to First Quantum (FM:CA) is quite low.

Conclusion:

Agnico has an enviable portfolio that is derived from quality mines with long lives ahead of them. While there are concerns around Agnico's compensation practices, I suspect these will be addressed in the coming years. If you are looking for names with a higher torque to gold, you could do better elsewhere. However, Agnico is tailormade for investors looking for a highly liquid, "steady Eddy" type of a precious metal stock. It is unhedged, it operates in low-risk jurisdictions and it has access to long-life mines.

For further details see:

Agnico Eagle: Strong As The Canadian Shield