AEM:CC - Agnico Eagle: Tier One Assets Strong Financials Makes This A Buy

2023-11-07 05:27:31 ET

Summary

- Agnico Eagle owns tier-one assets in tier-one jurisdictions. 86.9% of the company's revenue derives from Canada and Australia, and the remaining is from Mexico and Finland.

- The last quarter's results are solid. The average realized price was $1918/oz, compared to 2Q23 of $1726/oz. Agnico generated $1.62 billion in 3Q23, or 13.3% growth compared to 2Q22.

- Agnico's financials are strong, with improved balance sheets, profitability, and prudent capital allocation. The company pays dividends with a 3.23% yield.

- Agnico's EV/EBITDA and EV/Sales multiples are lower than their historical values. However, compared to Newmont and Barrick, Agnico is fairly priced.

- Considering the fundamentals and the price action, my verdict is a buy rating.

Introduction

Gold stocks are a mandatory part of my portfolio. I like to invest in majors with attractive dividend yields. Agnico Eagle (AEM) is among those companies. It is, in my opinion, the best major gold miner with assets in top jurisdictions, high-grade deposits, and AISC below world average $1358/oz. Agnico pays dividends with respectable yields and trades at low multiples. For gold investors focused on income, AEM is no-brainer.

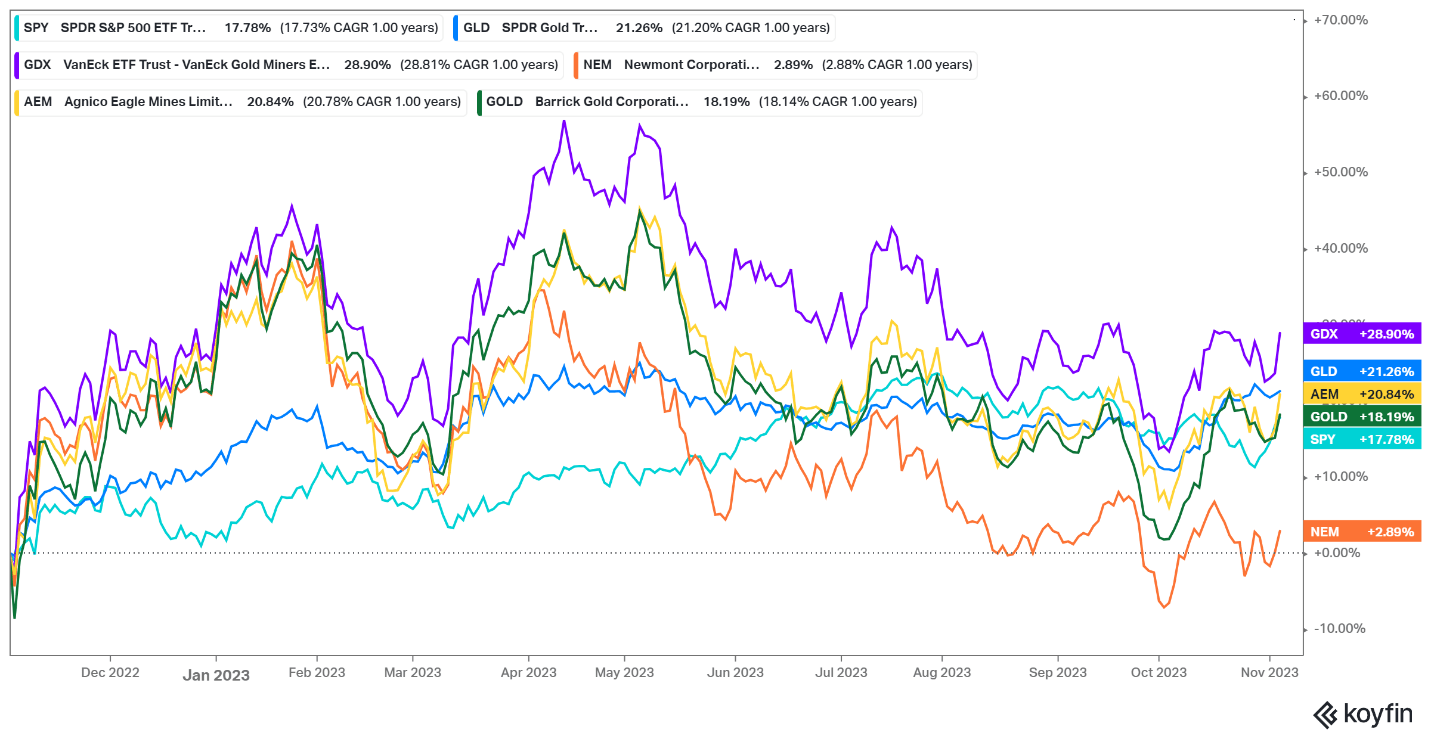

Gold stocks outperformed SPY for the last twelve months. The chart below compares SPY with VanEck Gold Miners (GDX), SPDR Gold Trust (GLD), Agnico, Newmont (NEM), and Barrick (GOLD).

{kind=link}

GDX and GLD hold the leading positions with 28.9% and 21.26% respectively. AEM is the best performer among the big three, with 20.84%. I expect the company to continue delivering its strong performance.

What does the company do?

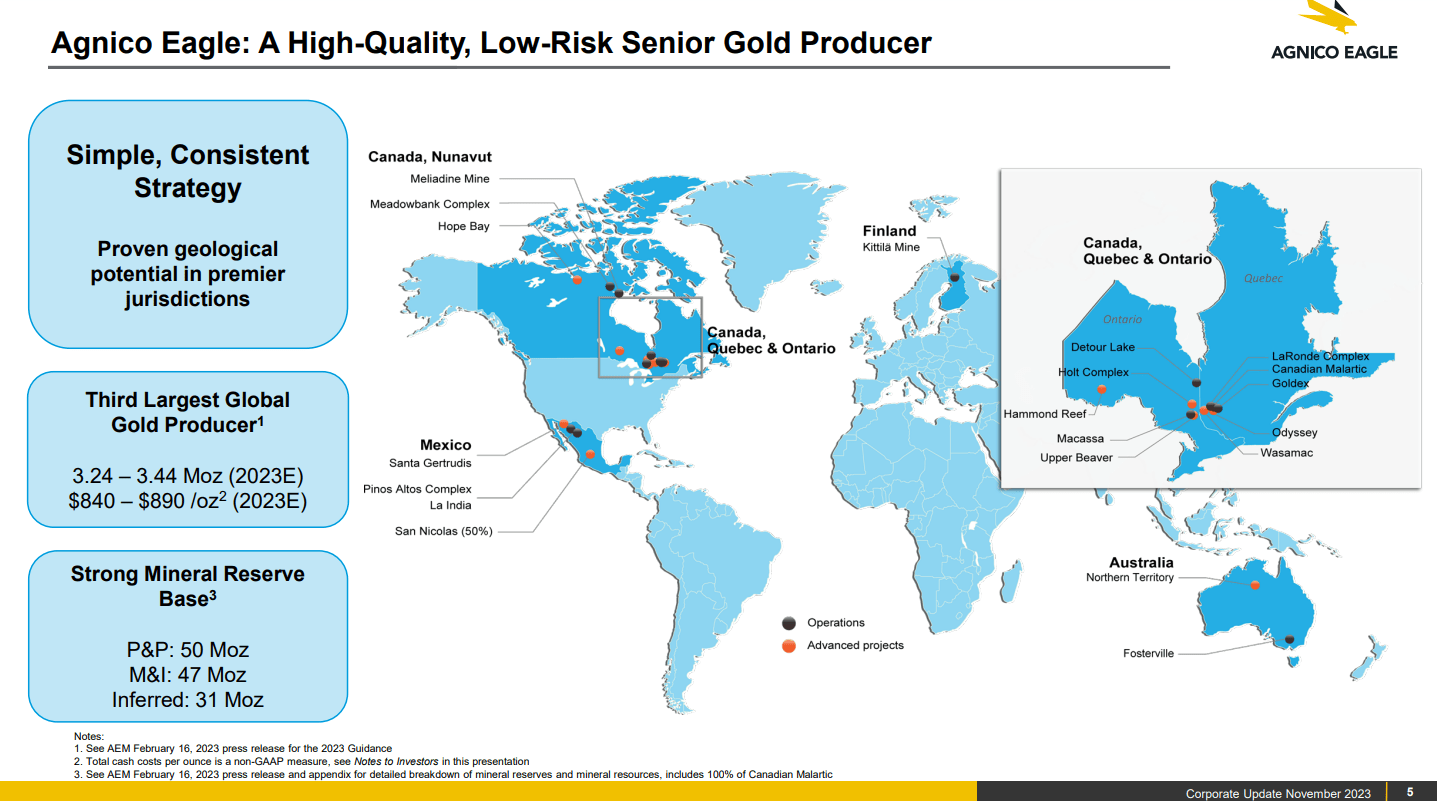

The merger with Kirkland Lake created the best gold major. Agnico is the third largest gold miner globally, next to Newmont and Barrick. However, I believe Agnico owns the best mines, given their location, size, grade, and AISC. The company's mines are in Canada, Australia, the USA, and Finland, all tier-one jurisdictions, per the Fraiser Institute report. Agnico's assets are shown on the map below from the last presentation .

{kind=link}

Agnico owns two of the largest gold mines in North America: Canadian Malartic and Detour Lake. Both combined deliver 1.2 million ounces per annum.

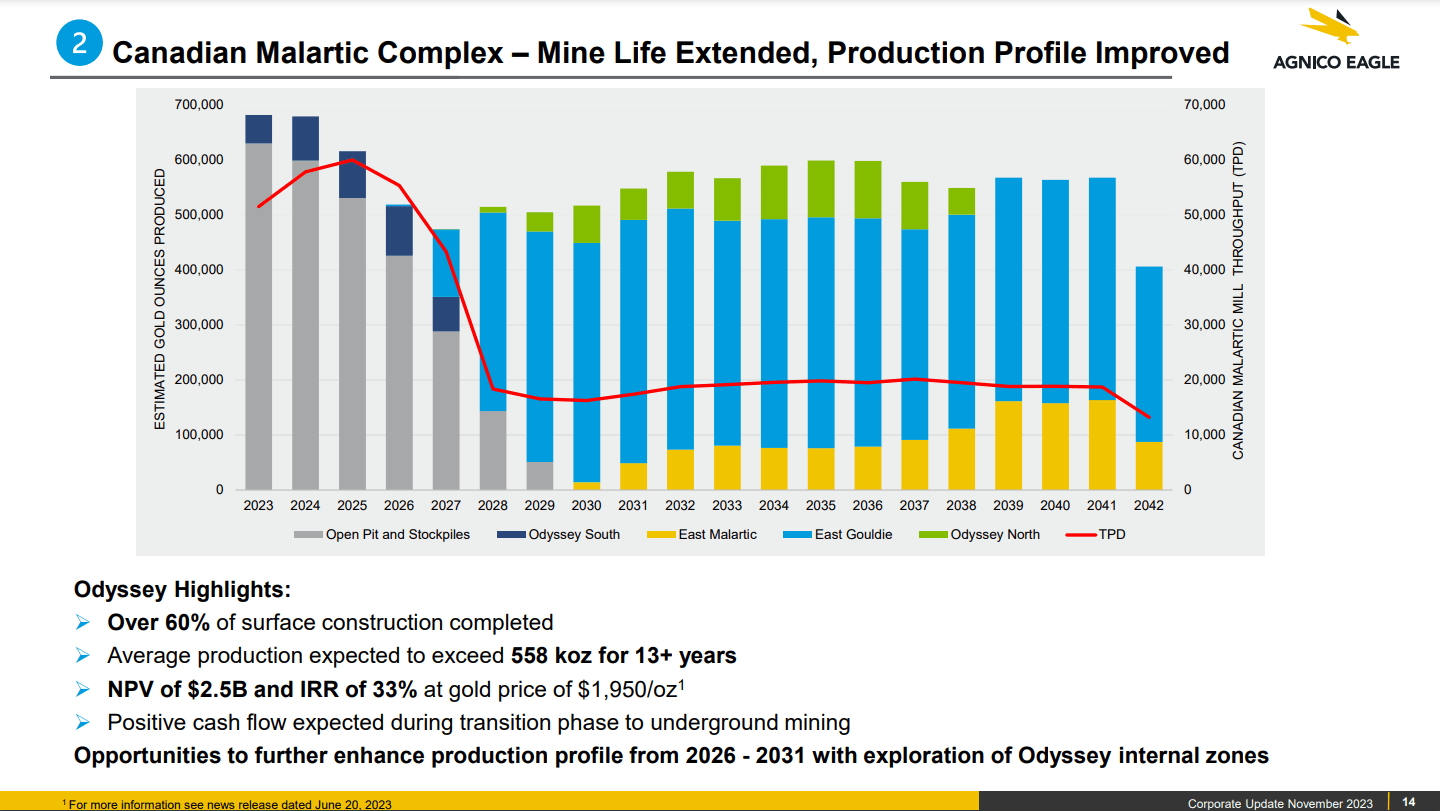

Odyssey mine in the Canadian Malartic complex is expected to become the largest underground gold mine in Canada. The chart below shows the development of the project.

{kind=link}

Its average production is expected to be 558 k oz for over 13 years. The company has two other mines in Quebec: La Ronde and Goldex.

Detour Lake in Ontario is the largest gold-producing mine in Canada, with the largest gold reserves at 20.7 million. Its mine life is until 2052, $752/oz cash cost and 715 k oz annual production. Agnico's second mine in Ontario is Macassa. It is one of the gold mines with the highest ore grade globally. Its mine life is until 2029, and annual production is 215 k oz. The cash cost is $761/oz.

Agnico's remaining assets are in Australia, Mexico, and Finland. Kirkland's asset, the Fosterville mine in Australia, has a cash cost of $378/oz, one of the lowest globally. The mine life is until 2031, and annual production is above 300k oz. Kittila mine in Finland is among the largest gold mines in Europe. It delivers 200 k oz per annum at $950/oz cash cost. Agnico's Mexican mines, La India and Pinos Altos, bring 150k oz to the annual production.

Agnico's annual production is above 3 million ounces of gold. For 2023, the guidelines are 3.24-3.44 million ounces. I expect the company to achieve its goals, given its strong performance.

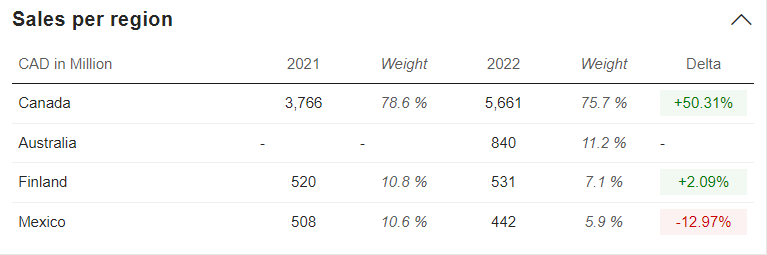

Geographically, the revenue is distributed as follows.

{kind=link}

86.9% of the revenue comes from Australia and Canada. Going into more detail, Agnico's 86.9% of revenue comes from three provinces: Quebec, Ontario, and Victoria. Unlike Barrick, Newmont, and Endeavour, Agnico owns tier-one assets in tier-one jurisdictions.

3Q2023

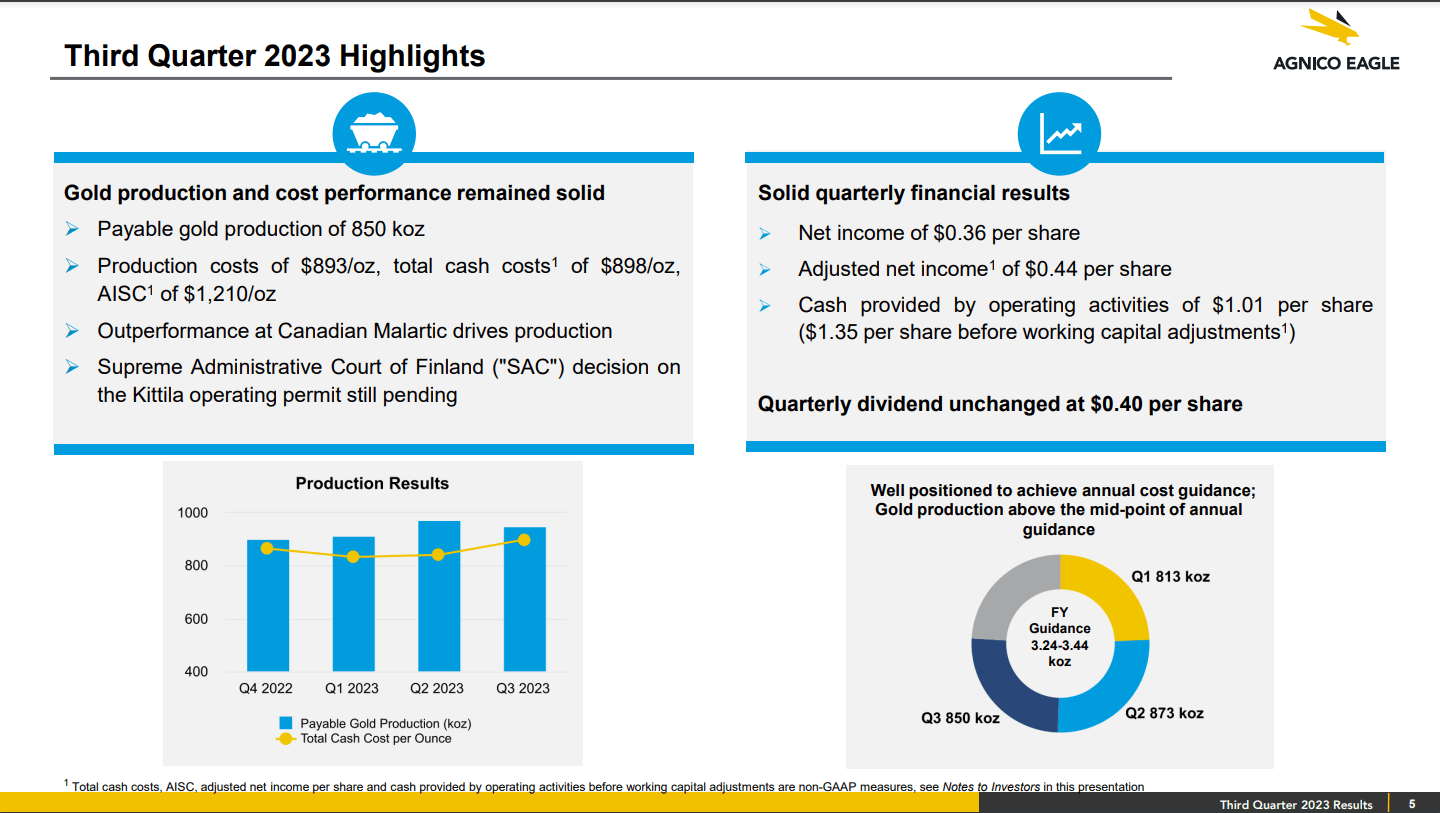

In the last report for 3Q23, Agnico declared strong performance. The company's revenue had increased significantly compared to 3Q22 and YTD22. The image below from 3Q23 report shows 3Q23 highlights.

{kind=link}

Agnico produced 850k ounces of gold at a cash cost of $898/oz. Year-to-date cash cost is $857/oz, lower than the company's guidelines of 840-890 $/oz. The average realized price was $1918/oz, compared to 2Q23 of $1726/oz. Agnico generated $1.62 billion in 3Q23, or 13.3% growth compared to 2Q22.

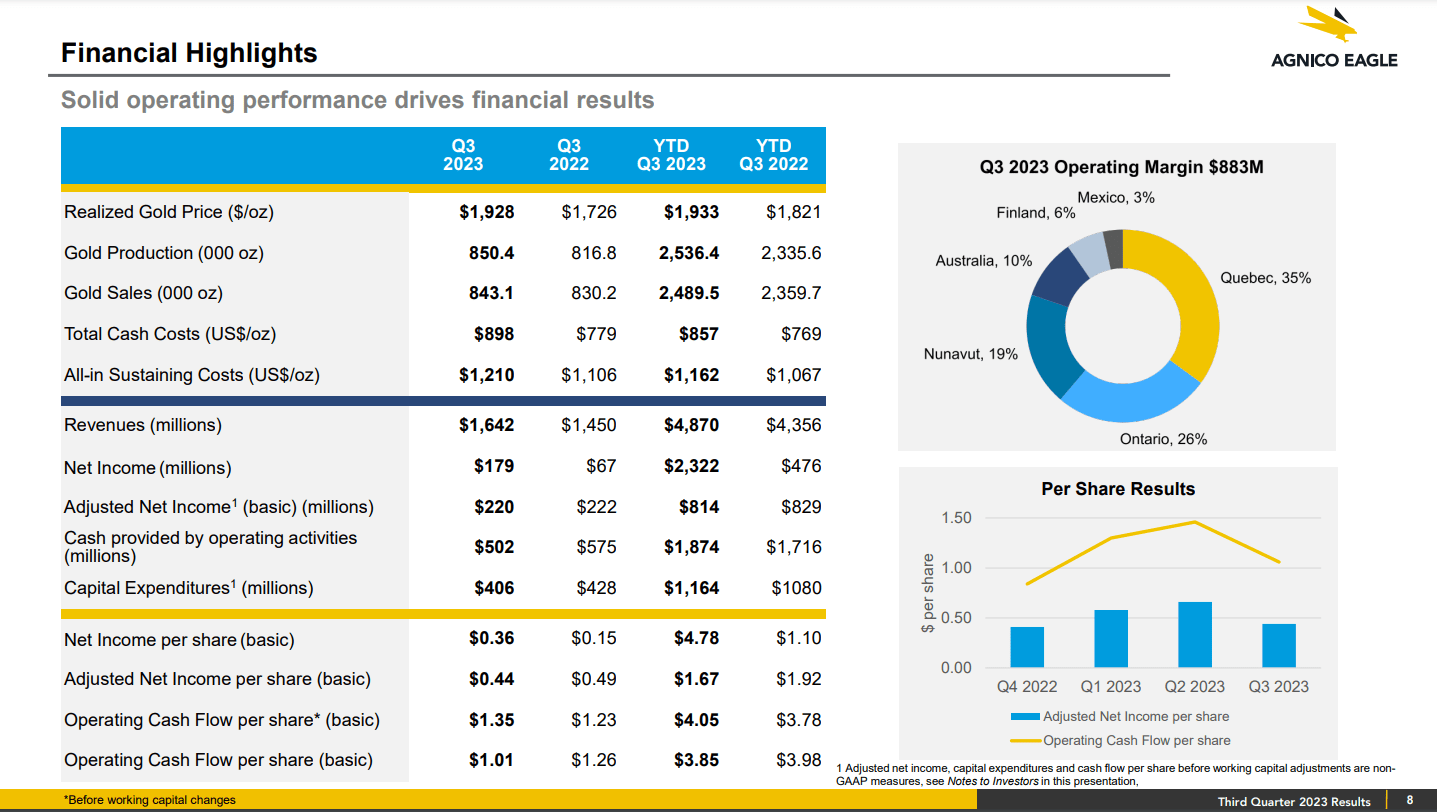

The chart below gives more details on the company's results.

{kind=link}

The highest margins maintain the company's Canadian mines. In Quebec, Agnico runs the Canadian Malartic complex. The complex includes two operations: the Canadian Malartic open pit mine and the Odyssey underground mine. The open pit mines' life is extended to 2029, while the underground mine is extended to 2039.

Company financial

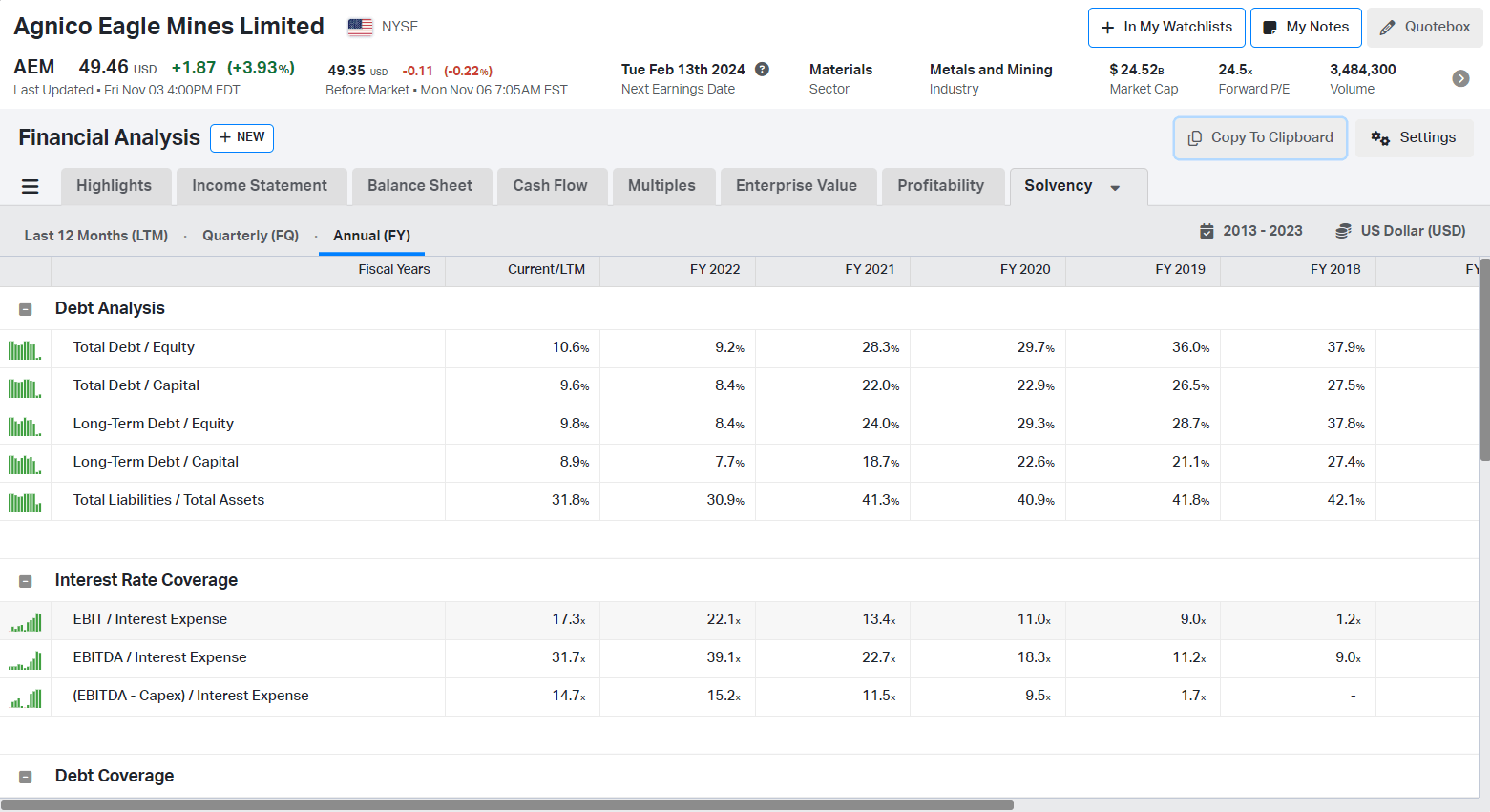

Gold miners had notably improved their balance sheets. Agnico is not an exception. Let's start with the company's solvency and liquidity figures. The chart below shows the company's debt and interest rate coverage.

{kind=link}

Total debt to capital has declined significantly for the last two years, reaching 9.6%. The total liabilities as a percentage of assets represent 31.8%, lower than the 2021 figures. Interest coverage is more than sufficient with 14.7 (EBITDA-CAPEX)/Interest expenses.

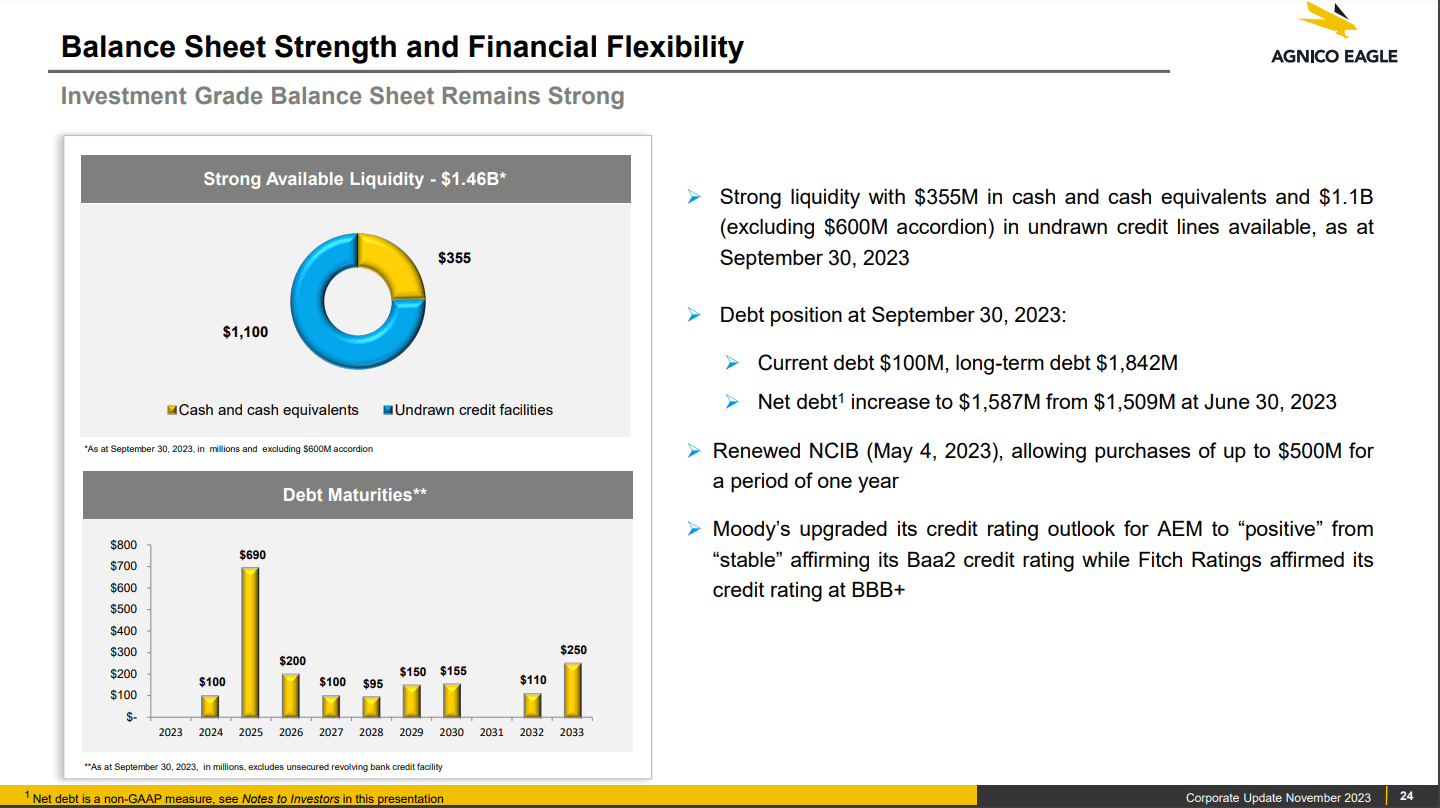

Agnico owns $364 million cash and $2.11 billion debt, or cash to total debt is 17%. Barrick and Newmont have a higher cash-to-total debt ratio, 89% and 52 respectively. The chart below shows Agnico's debt maturities.

{kind=link}

Current debt is $100 million. The next large portion to be repaid is $690 million in 2025. I do not expect troubled Agnico to pay its 2025 debt, given the company's operational cash flow ((TTM)) is $2.25 billion and its cash at $355 million. Moody's and Fitch upgraded the company's outlook from stable to positive. Besides that, Agnico's debt is investment grade.

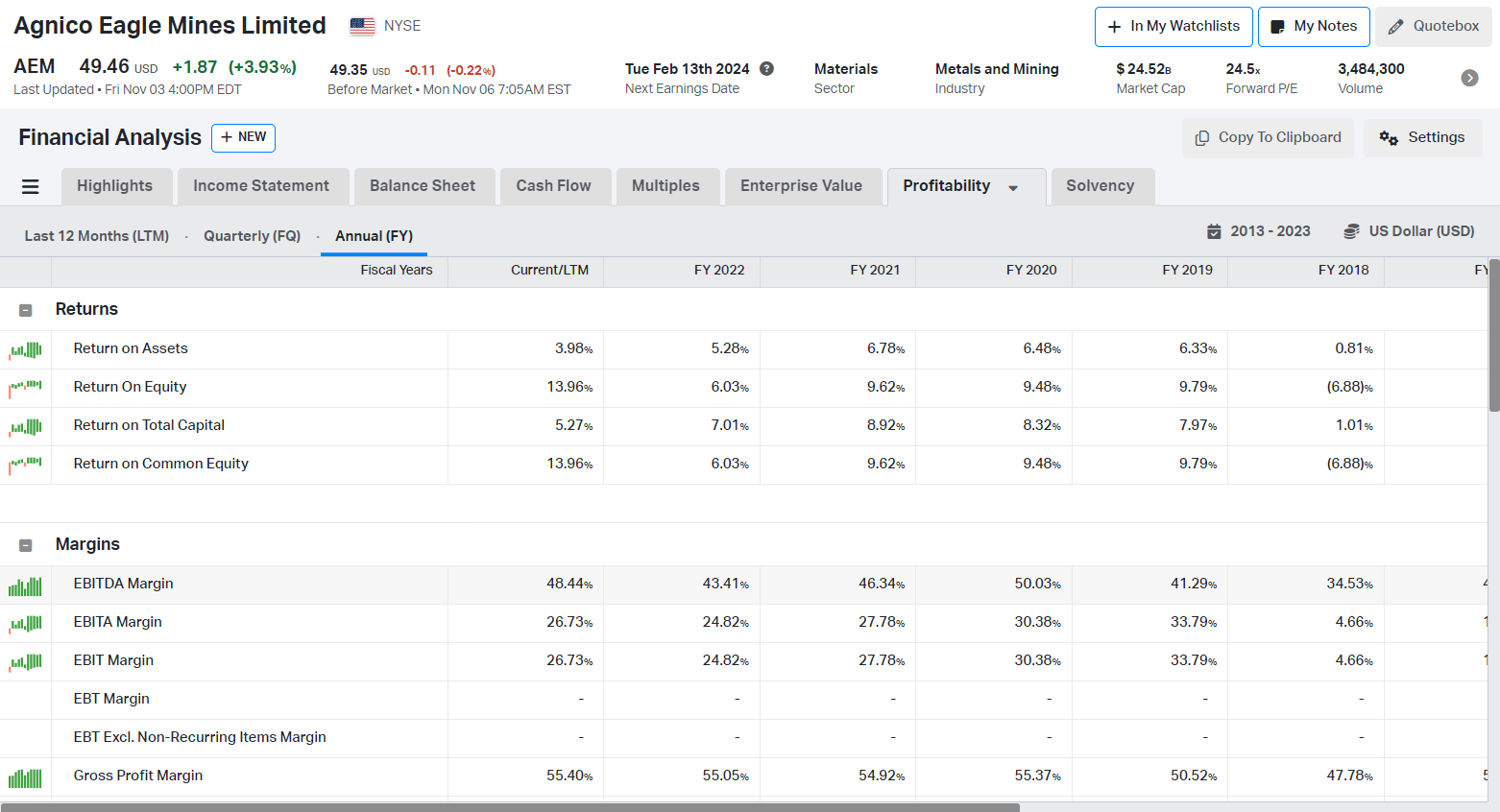

The company's profitability has improved notably. The table below presents Agnico's returns and margins.

{kind=link}

Return on Equity ((LTM)) reached 13.96% compared to single digits in the previous years. The gross profit margin remains stable despite inflation pressures. On the other hand, the EBITDA margin had grown for two consecutive years, reaching 48.44%.

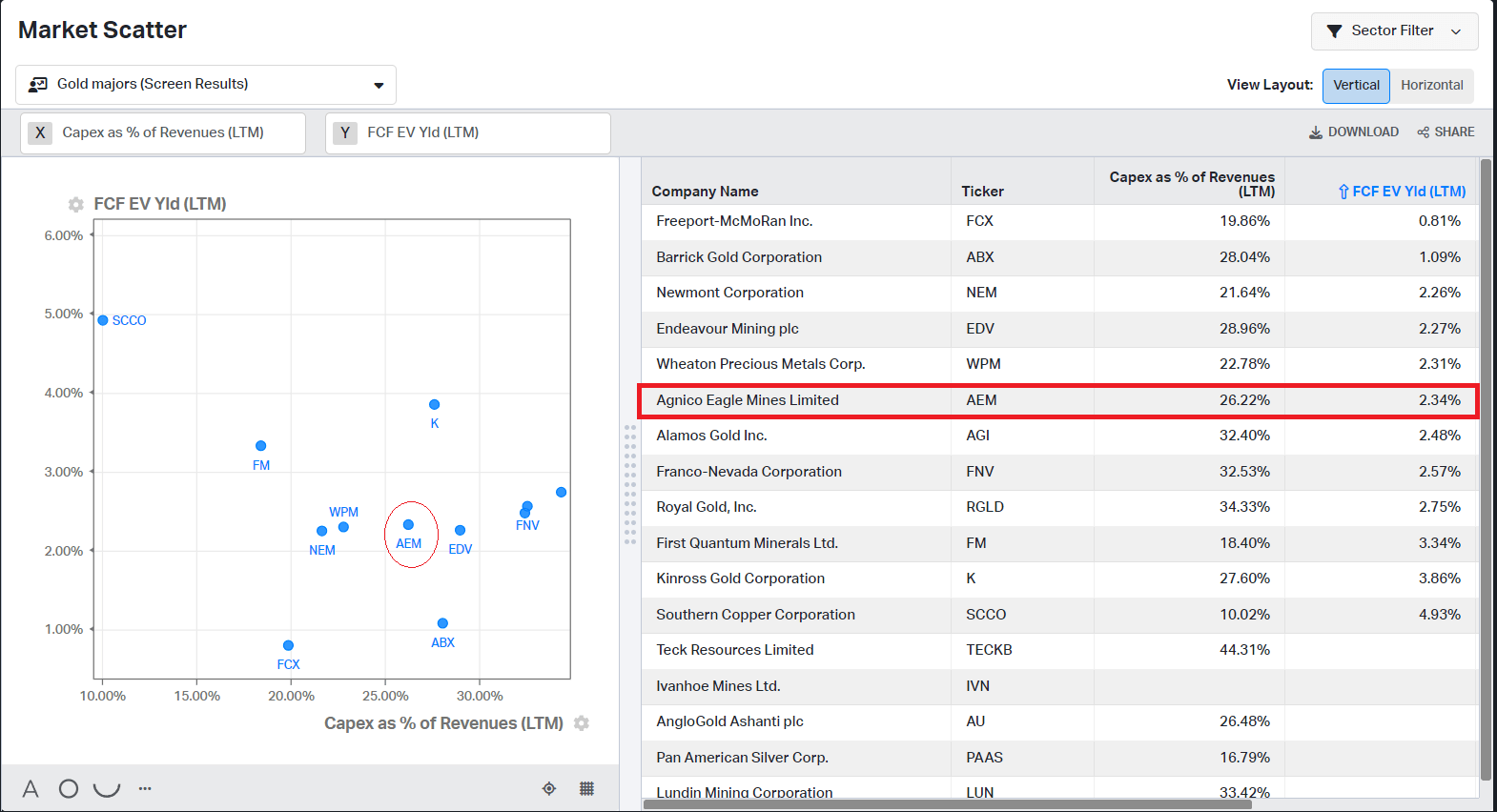

Let's look at how Agnico performs against their peers. The first chart compares Agnico and another major based on FCF yield and CAPEX/Revenue.

{kind=link}

Agnico has a 2.34% FCF yield and 26.22% CAPEX/Revenue. Those figures are similar to majors like Barrick, Kinross (KGC), and Endeavour (EDVMF). Unlike the previous bull market in 2010, the majors are prudent and do not spend hard-earned cash on questionable projects. However, Agnico has spare firepower whenever it decides to expand its business.

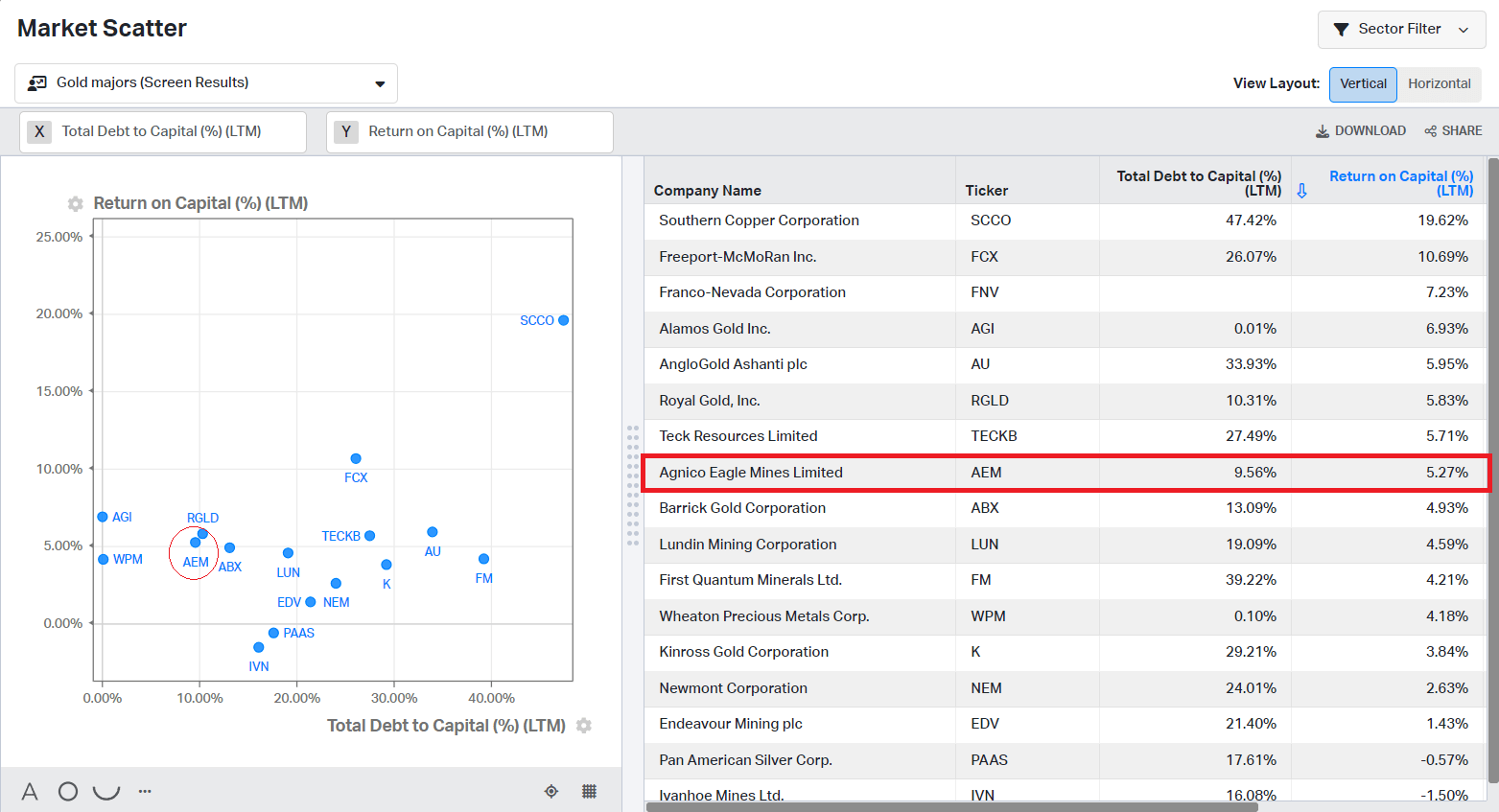

Investing means efficient capital allocation. This is equally important for us investors and the companies we invest in. To estimate how skillful a company's management is, I use Total debt/Total capital and Return on Capital.

{kind=link}

The last few years have been great for gold miners. The rising gold price improved its bottom line and helped them to reduce their debts. Agnico excels compared to Barrick, Kinross, and Newmont. 5.27% ROIC and 9.59% Total debt/Total capital shows management's ability to use leverage wisely.

Valuation

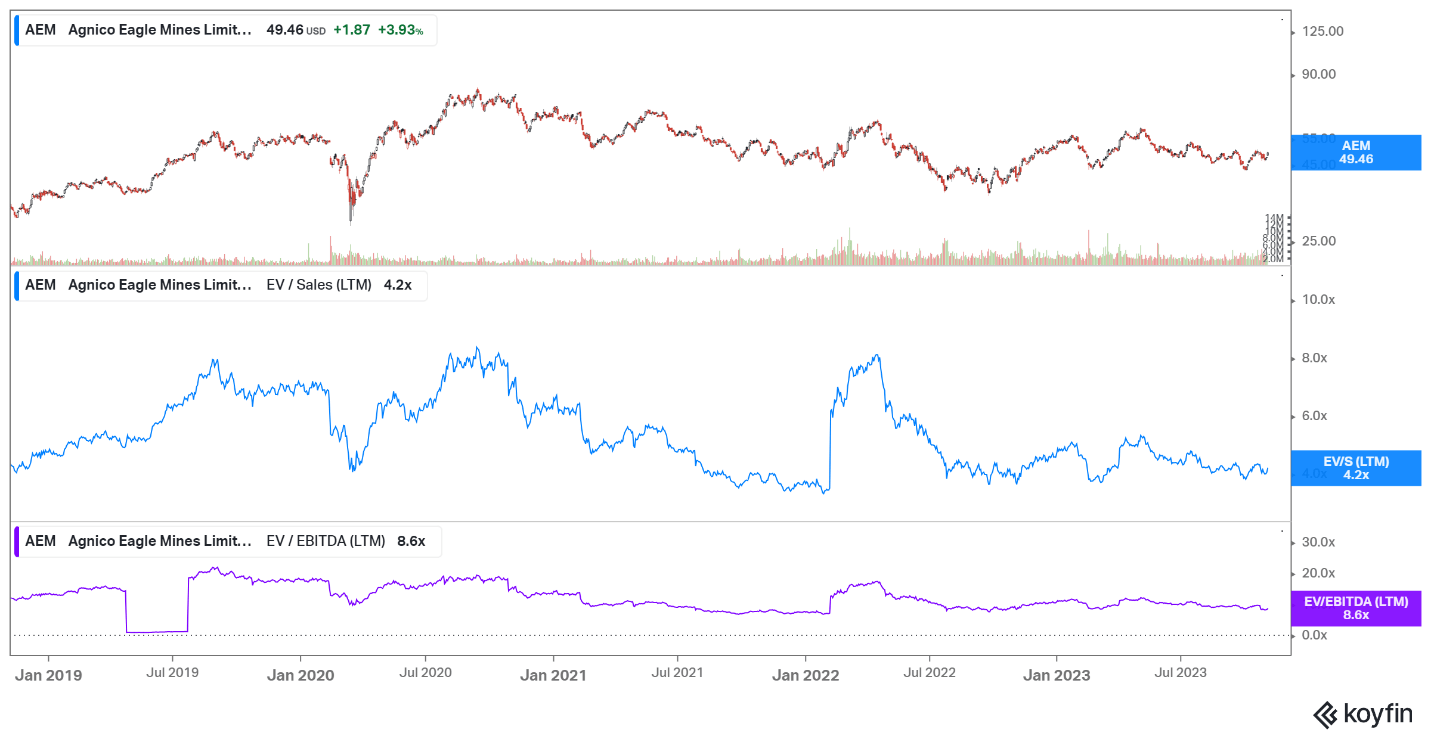

To estimate Agnico's value, I compared the company's past performance and compared it against its peers. The chart below shows Agnico's historical price, EV/Sales, and EV/EBITDA.

{kind=link}

Agnico trades at 8.6 EV/EBITDA and 4.2 EV/Sales. It's well below its previous peaks. Barrick trades at lower multiples: 3.42 EV/Sales, 6.92 EV/EBITDA. Newmont's EV/EBITDA is higher at 10.14, while EV/Sales is lower at 3.06.

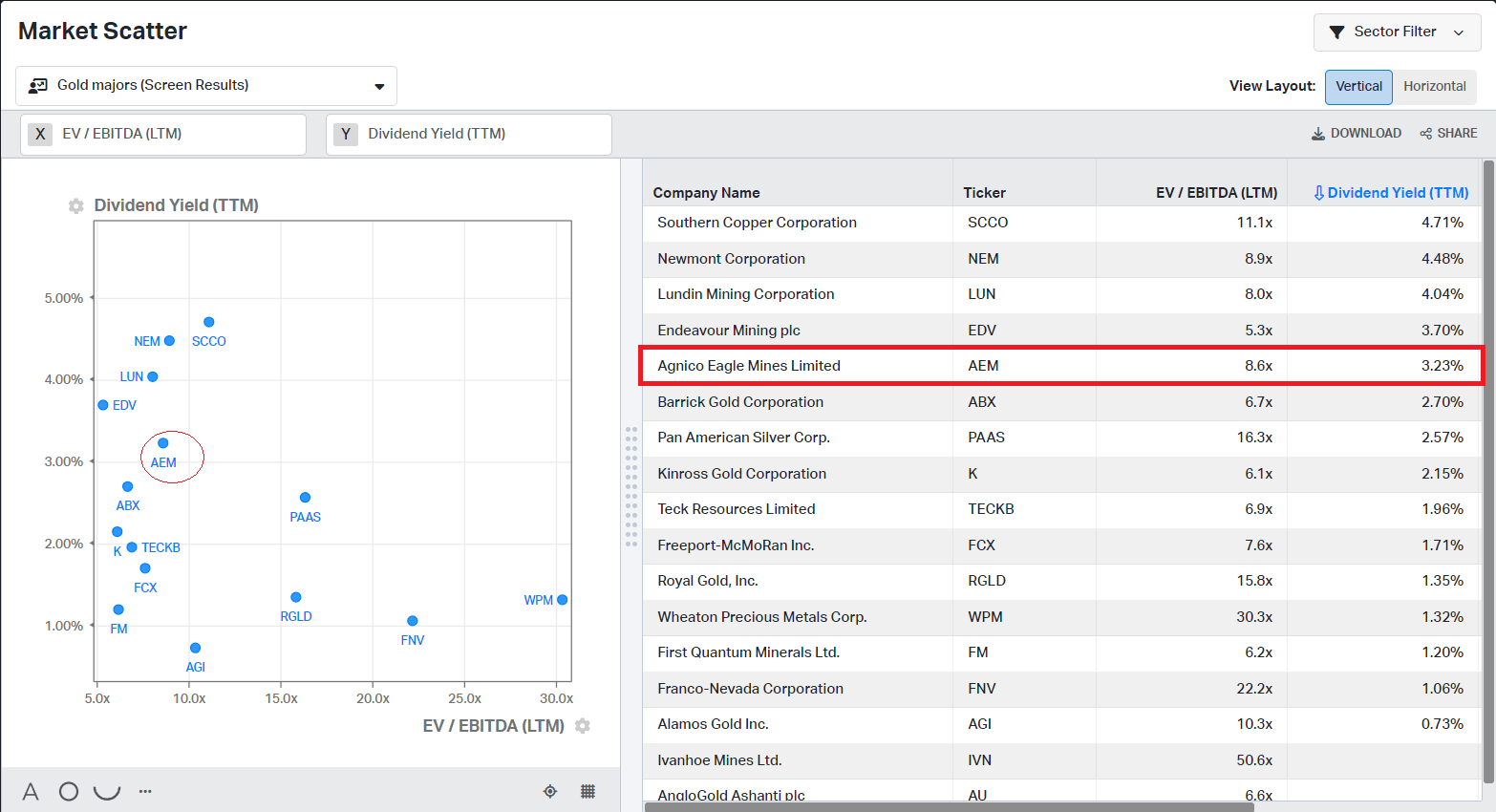

Being dividend-focused, I like to compare Dividend yield (value) vs EV/EBITDA (price). Agnico trades at 8.6 EV/EBITDA while offering dividends with a 3.22% yield.

{kind=link}

For comparison, Newmont trades at 8.9 EV/EBITDA and pays dividends with a 4.48% yield. Barrick trades at 6.7 EV/EBITDA and pays dividends with a 2.7% yield.

Agnico's EV/EBITDA and EV/Sales multiples are lower than their historical values. However, compared to Newmont and Barrick, Agnico is fairly priced.

Price action

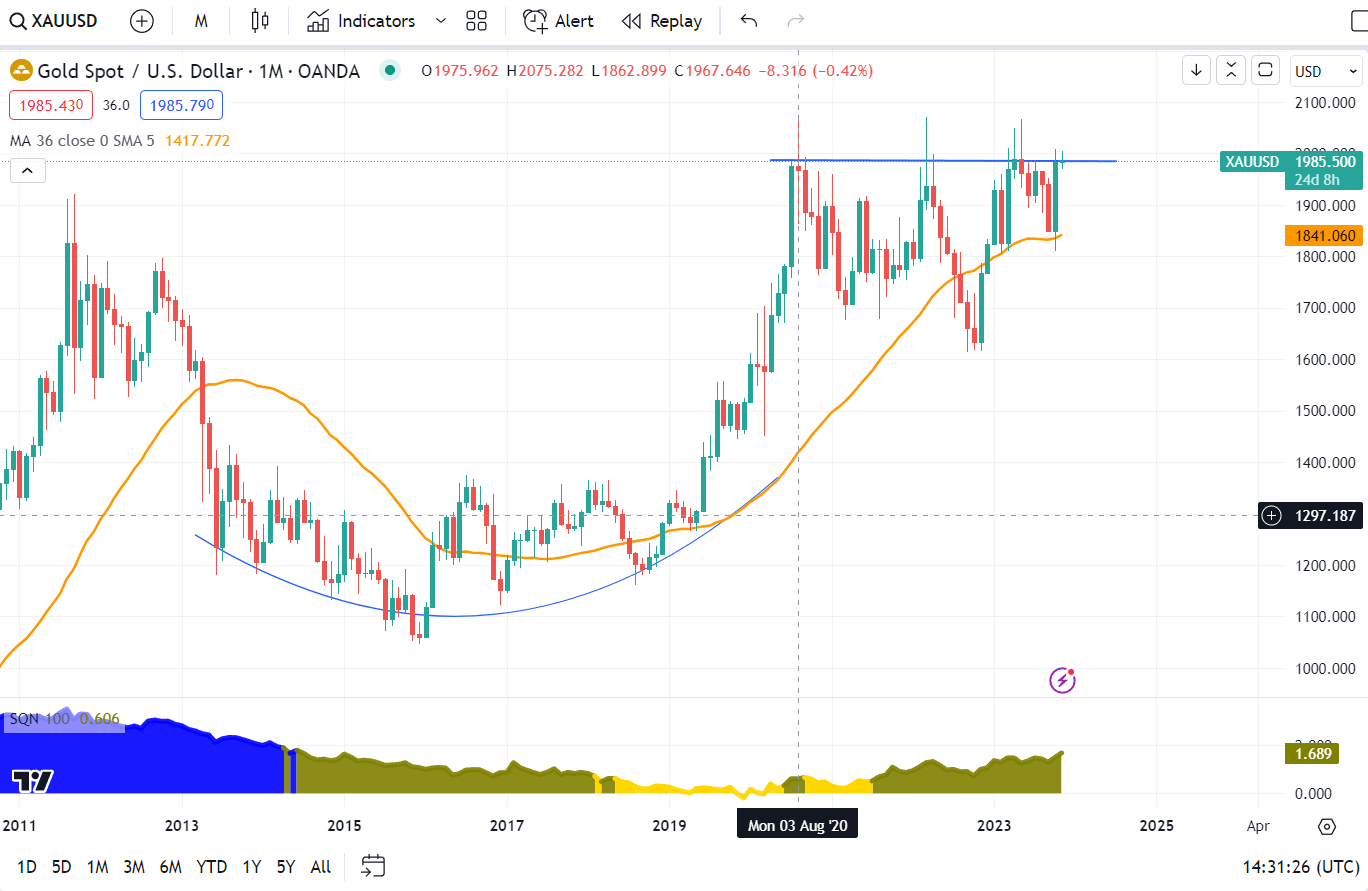

Before I discuss Agnico's chart, let's quickly look at the gold spot price.

{kind=link}

The pattern seems to triple top. October monthly candle closed just below $2000/oz. The previous failed breakout is evident with its long candle wicks. The SQN indicator is in a bull quiet regime, and the price is above 36 months simple average ((SMA)). Bull breakouts in the Bull Quiet regime have a higher success rate than in the other regimes. Besides that, the SMA is a support for March and October candles.

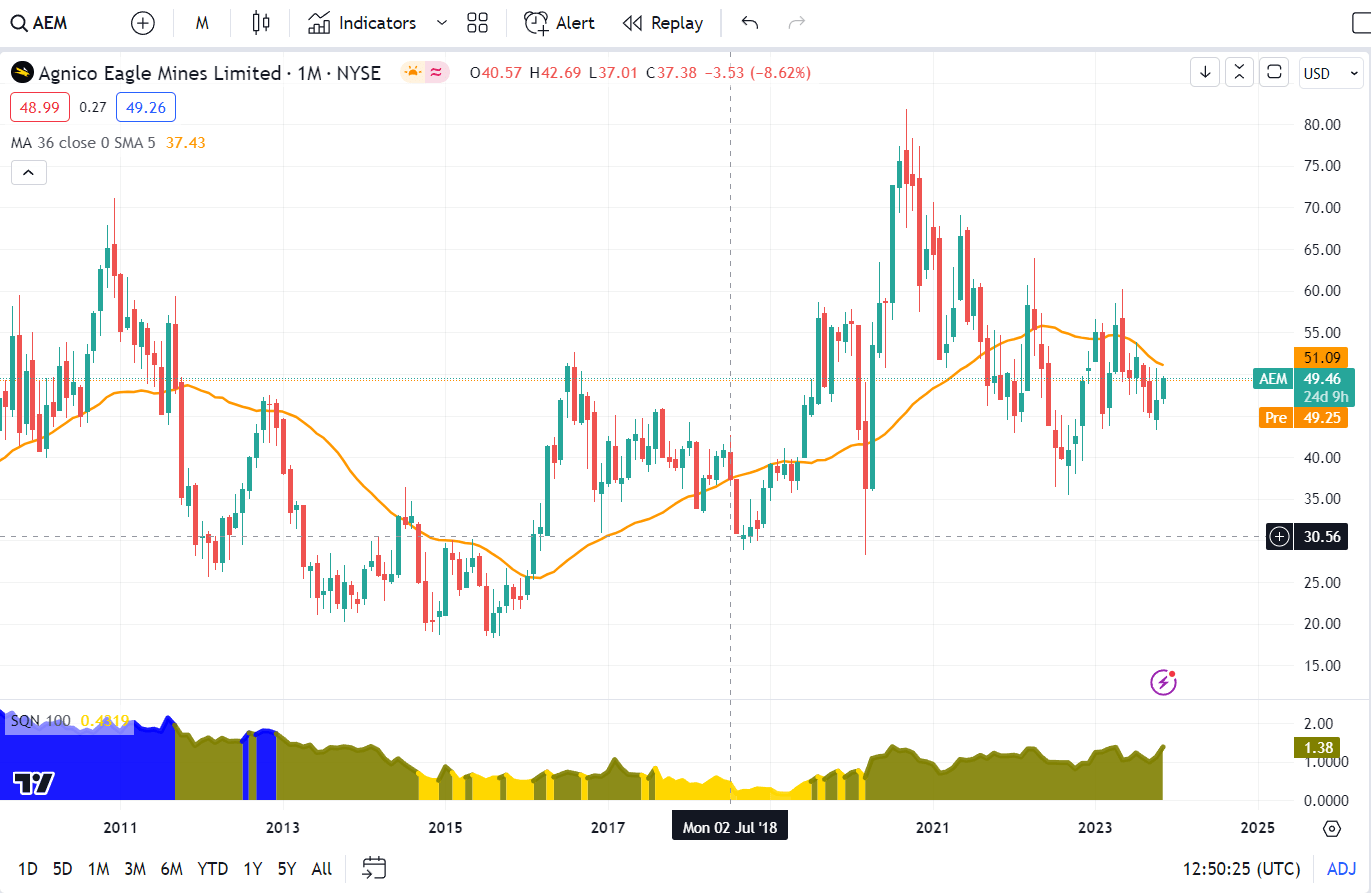

Let's look at Agnico's chart.

{kind=link}

The price action is very choppy and lagging in gold price return. However, the latter is common among gold equities. The November monthly candle is on the verge of breaking through the 36-month simple average, and SQN remains in a bull-quiet regime. I prefer to open a smaller position while waiting for a confirmed breakout. If the gold price breaks permanently above $2000/oz, it will push the gold miner stocks higher. So I can add more risk.

Risks

Among the majors, Agnico has the lowest political risk. Its assets are located exclusively in tier one jurisdiction, unlike Barrick, Kinross, or Endeavour. Financially, Agnico has sufficient cash position to cover its current debt. In the long term, I do not expect any issues with the 2025 debt payments, given the company's strong performance.

Gold miners' stocks are a function of the gold price, where resides the most pronounced risk for Agnico. In the long term, I expect the gold price to move up. Like other metal mining industries, gold mining suffers from a lack of investments and lower ore grades. On the demand side, we have central banks intensively buying gold. Besides that, global tensions focus on gold as a haven in such situations. However, those variables cause a long-term impact. In the meantime, the price might go south before breaking the resistance at $2000/oz.

Investors takeaway

Agnico Eagle is a top-quality, major gold miner. It owns tier-one mines in tier-one jurisdictions. In the last quarter, the company delivered solid results. The revenue increased significantly compared to 3Q23, while the cash costs decreased. Agnico is reasonably valued compared to its peers; however, it is cheaper than its historical multiples. The company pays dividends with a 3.3% yield.

The gold price is on the verge of a significant breakout. Besides that, Agnico's price action has been choppy. If successful, it will push gold miners' stocks higher. Given Agnico's qualities and dividend yield, I would take a small position while waiting for the breakout. If the price remains above $2000/oz, I will add more shares. Considering the fundamentals and the price action, my verdict is a buy rating.

For further details see:

Agnico Eagle: Tier One Assets, Strong Financials Makes This A Buy